Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

Secure Energy Services Inc. (TSX:SES) presented its latest investor deck on October 30, 2025, showcasing the company’s transformation into a waste management and energy infrastructure leader. With shares trading at $18.30, down 1.64% following the release of mixed Q3 results, the company faces both opportunities and challenges in its evolving business model.

The presentation highlights Secure’s strategic pivot from traditional energy services to a more stable waste management and infrastructure business, with 75% of its adjusted EBITDA now coming from waste management operations and 25% from energy infrastructure.

Business Transformation

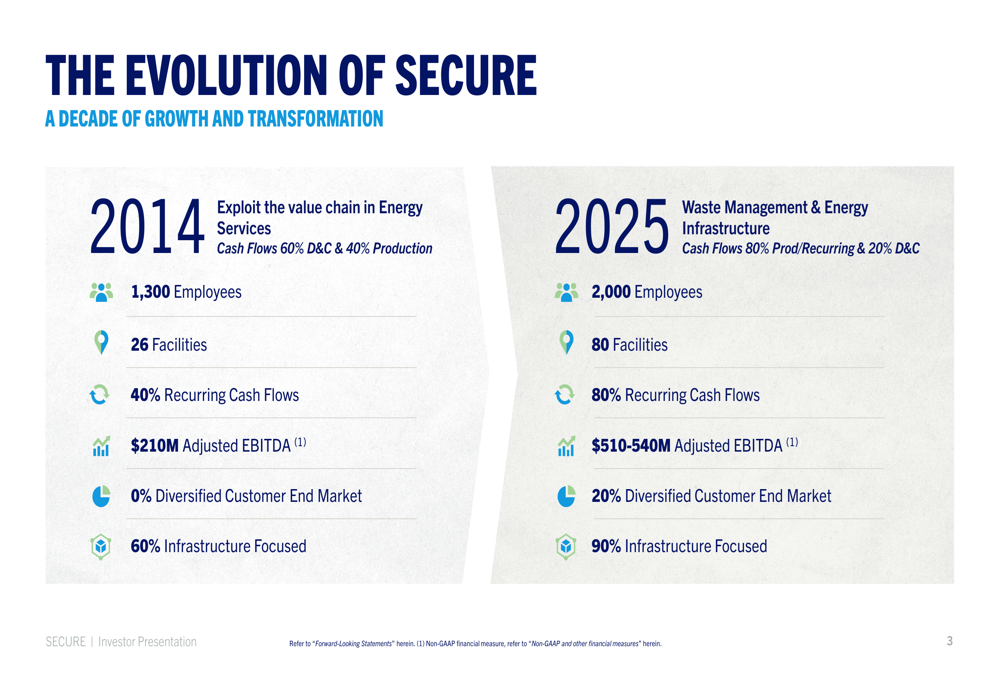

Secure has undergone a significant transformation over the past decade, evolving from an energy services company to a waste management and infrastructure leader. This strategic shift has resulted in more stable and recurring cash flows, with 80% of volumes now tied to production-related and recurring waste streams.

As shown in the following evolution chart:

The company has expanded its facility network from 26 in 2014 to 80 in 2025, while increasing recurring cash flows from 40% to 80%. This transformation has driven adjusted EBITDA growth from $210 million in 2014 to a projected $510-540 million in 2025.

Financial Performance Highlights

Secure’s financial metrics show strong operational performance, with adjusted EBITDA per share growing at an 8% CAGR from 2022 to 2024, reaching $2.00 in 2024. The company has also improved its adjusted EBITDA conversion ratio to 64% in 2024, up from 58% in previous years.

The corporate snapshot reveals key financial strengths:

However, Q3 2025 results revealed some challenges. While adjusted EBITDA rose 6% year-over-year to $135 million, revenue excluding oil purchase/resale decreased by 2% to $365 million. Most notably, net income plummeted to $1 million from $94 million in the previous year, raising investor concerns despite the company’s infrastructure-backed network.

Competitive Industry Position

Secure positions itself as a market share leader in industrial waste management across Western Canada and North Dakota, with approximately 80 locations providing critical infrastructure. The company’s network includes 55 waste processing and transfer facilities, 12 industrial landfills, 12 metal recycling facilities, and 3 oil pipeline systems.

The company’s geographic footprint demonstrates its market leadership:

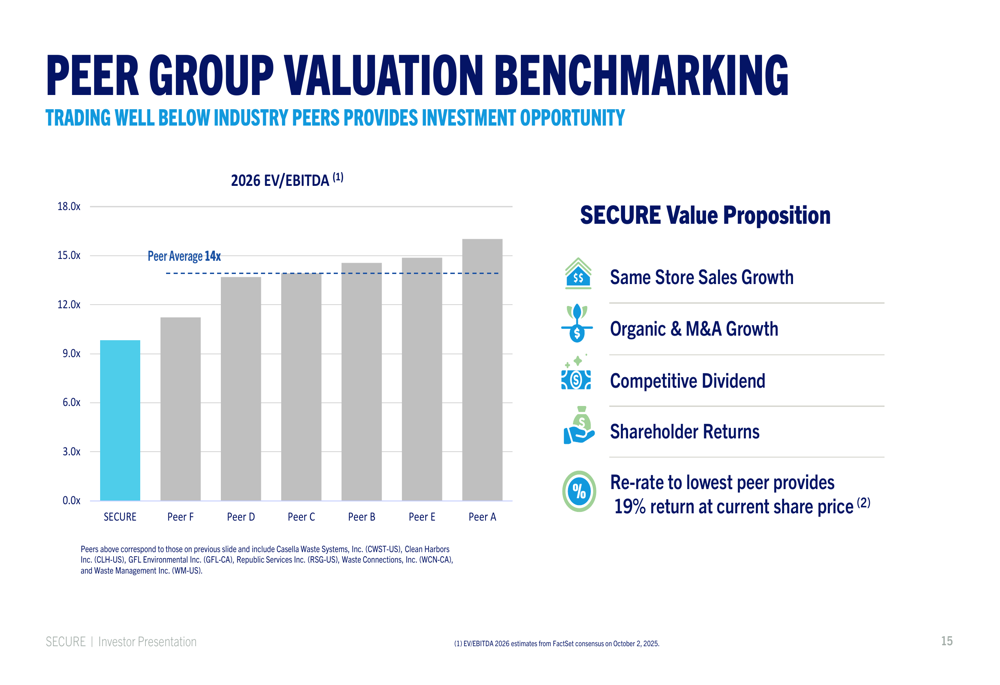

When benchmarked against waste management peers, Secure outperforms in key financial metrics:

The company leads peers in adjusted free cash flow conversion (>50%), adjusted EBITDA margin (33.6%), and return on invested capital (21.1%). Despite this strong performance, Secure trades at a valuation discount to its peer group.

Strategic Initiatives

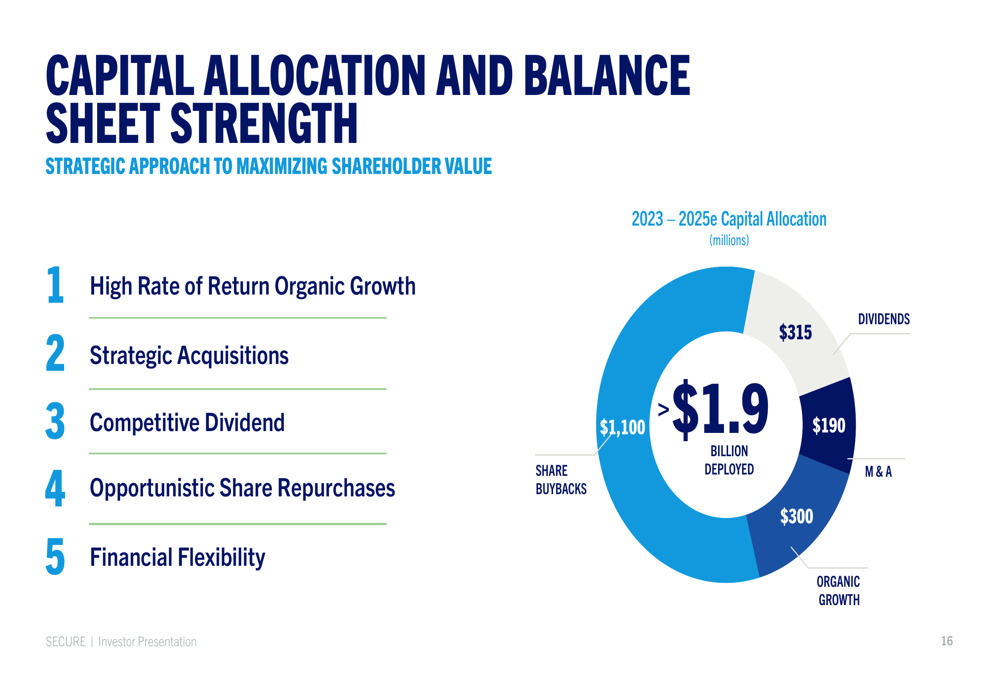

Secure’s capital allocation strategy focuses on balancing growth investments with shareholder returns. The company has allocated $1.9 billion between 2023-2025, with significant portions directed toward share buybacks ($1.1 billion), dividends ($315 million), organic growth ($300 million), and strategic acquisitions ($190 million).

The capital allocation breakdown illustrates this balanced approach:

For 2025, Secure has planned an organic growth capital program of $125 million, primarily focused on Montney region water disposal infrastructure. Key investments include two new water disposal facilities secured by 10-year contracts, oil terminal expansion, waste processing facility upgrades, and logistics efficiency improvements.

Challenges and Outlook

Despite the company’s strategic positioning, Secure faces several challenges that were evident in its Q3 2025 results. During the earnings call, management acknowledged a 15% drop in rig count quarter-over-quarter, impacting drilling and completion activity. The ferrous metals recycling business has also experienced difficulties due to tariffs, though CEO Alan Grant noted that "We’ve effectively transitioned now 95% to the U.S. market."

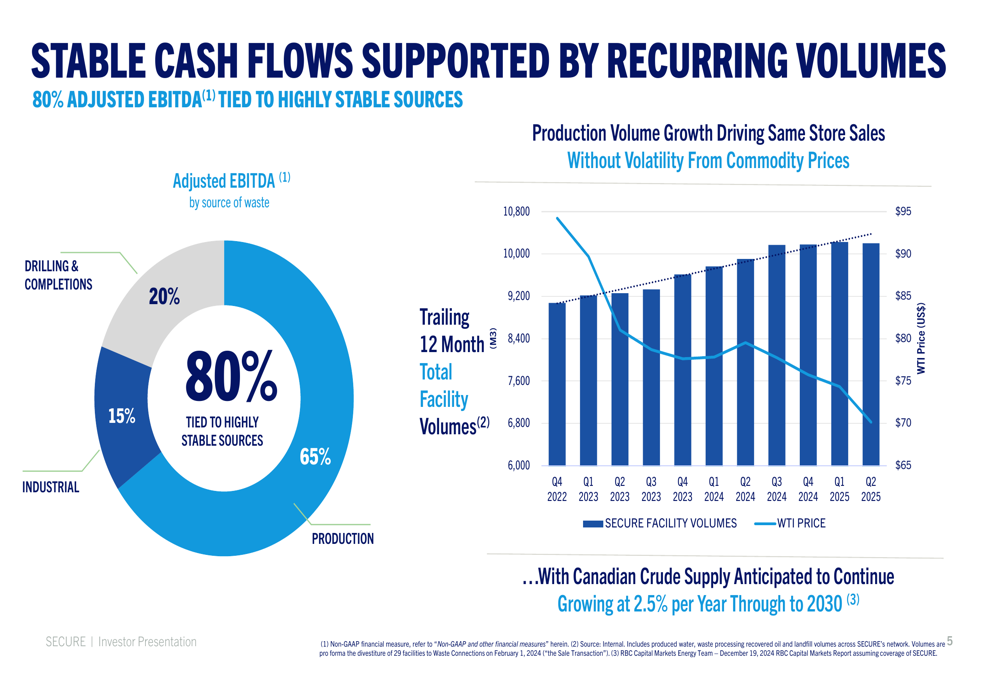

The company’s waste management business remains resilient, with stable cash flows supported by recurring volumes:

Looking forward, Secure anticipates growth in EBITDA for 2026, driven by new infrastructure projects and improved logistics in metals recycling. The company maintains a strong financial position with a Total Debt to EBITDA ratio of 2.1x, providing financial flexibility to fund capital allocation priorities.

Forward-Looking Statements

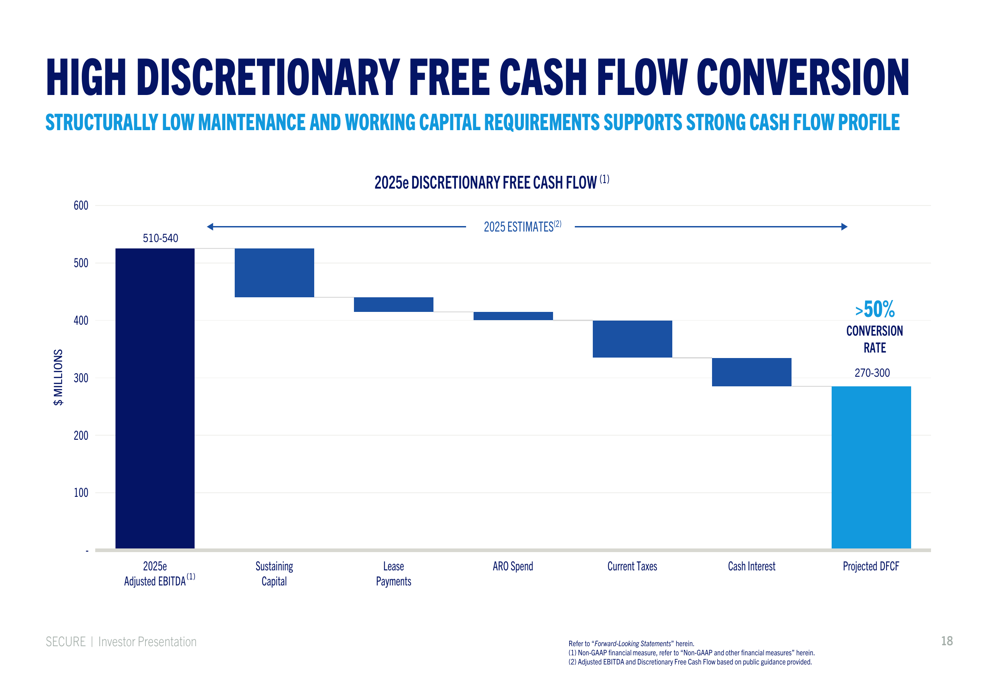

Secure projects adjusted EBITDA of $510-540 million for 2025, with a discretionary free cash flow conversion rate exceeding 50%. This strong cash generation capability is supported by structurally low maintenance and working capital requirements.

The company’s cash flow profile is illustrated in this waterfall chart:

Management expects long-term industrial fundamentals to remain supportive, with further guidance to be provided in February 2026. The company continues to focus on its waste management infrastructure, which provides critical processing, recycling, and disposal solutions with high barriers to entry.

Investment Thesis

Secure summarizes its investment case with five key points: a resilient business model, strong performance metrics, capital deployment optionality, industry fundamentals driving growth, and attractive valuation compared to peers.

While the recent quarterly results show some challenges, particularly in net income performance, the company’s infrastructure-backed network continues to generate stable cash flows. With its strategic positioning in waste management and energy infrastructure, along with its valuation discount to peers, Secure presents an interesting investment opportunity for those looking at the environmental services sector, though investors should monitor the company’s ability to address current headwinds in metals recycling and drilling activity.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.