Palantir to report; Trump on Nvidia chip exports - what’s moving markets

Introduction & Market Context

Sensata Technologies (NYSE:ST) released its third-quarter 2025 earnings presentation on October 28, highlighting financial performance that exceeded guidance across key metrics. The sensing solutions provider maintained its stock price at $50.64 amid a challenging macroeconomic environment, demonstrating resilience in its core business segments.

The company reported $932 million in revenue for Q3 2025, representing a 5.2% year-over-year decline in reported terms, but with 3% organic growth when adjusting for currency effects and acquisitions. This performance comes as Sensata continues to navigate global market uncertainties while positioning itself for future growth through strategic leadership appointments and product innovation.

Quarterly Performance Highlights

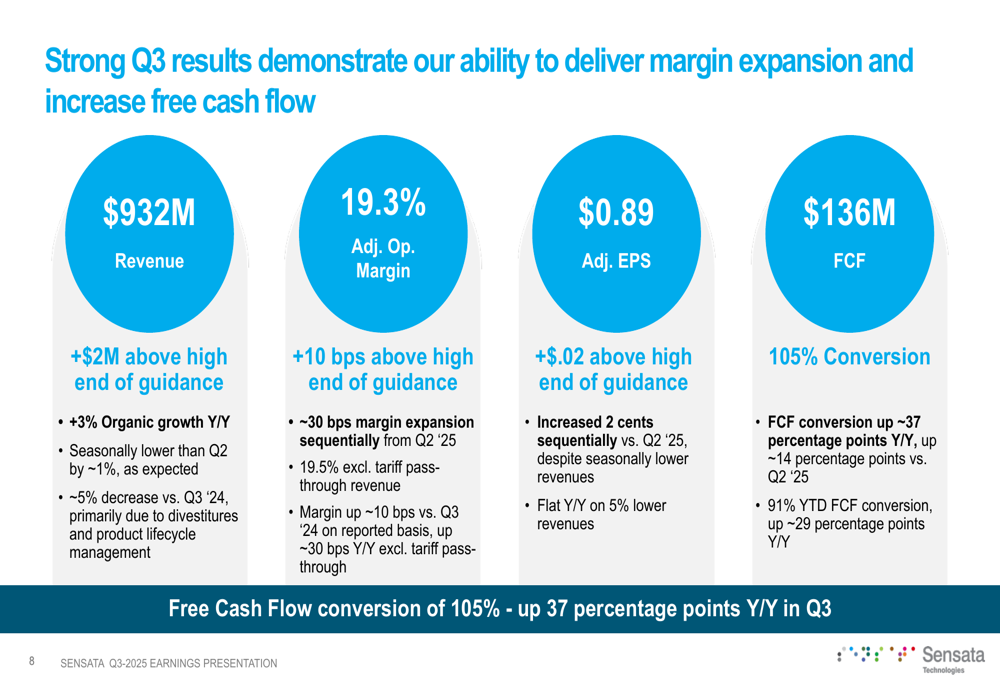

Sensata’s third-quarter results exceeded the high end of its guidance across all key financial metrics. Revenue reached $932 million, $2 million above the high end of guidance, while adjusted operating margin of 19.3% was 10 basis points above the high end of guidance.

As shown in the following performance summary:

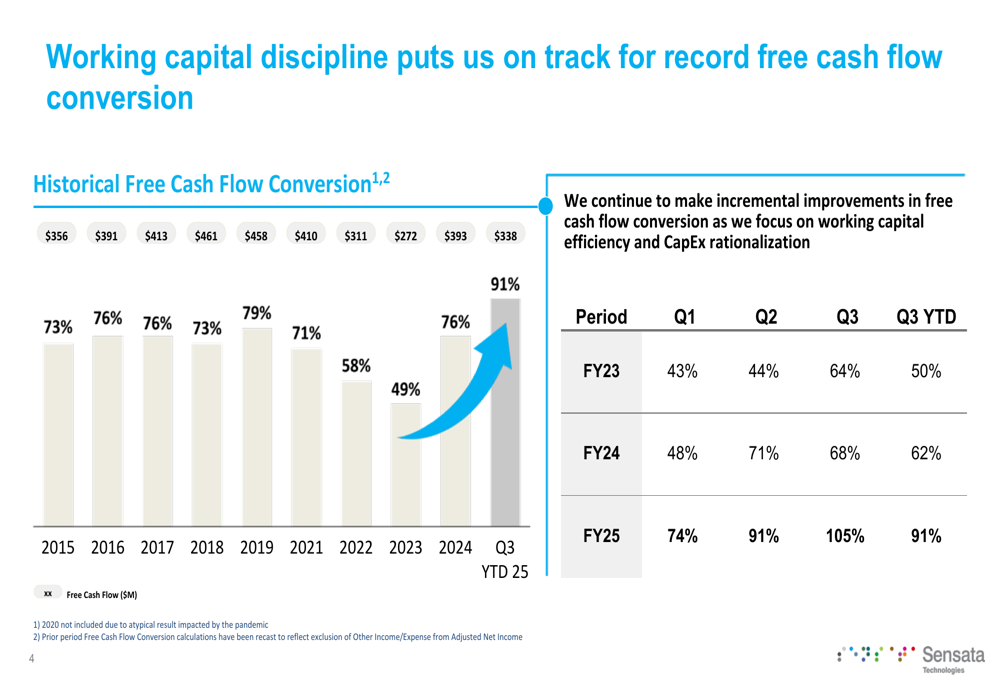

Particularly noteworthy was Sensata’s free cash flow performance, which reached $136 million with a 105% conversion rate – a 37 percentage point improvement year-over-year. This strong cash generation reflects the company’s enhanced working capital discipline and operational efficiency initiatives.

The company’s historical free cash flow conversion shows a clear upward trajectory:

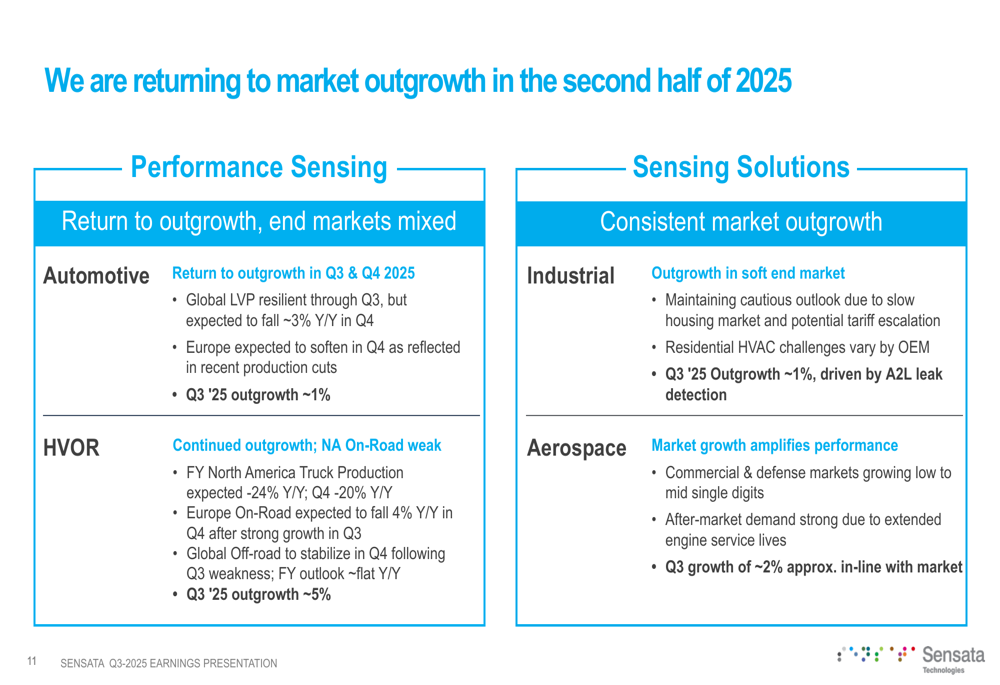

Both of Sensata’s reporting segments delivered year-over-year organic growth. The Performance Sensing segment, which accounts for approximately 70% of total revenue, achieved automotive market outgrowth of approximately 1%, while the Heavy Vehicle & Off-Road (HVOR) segment demonstrated stronger outgrowth of approximately 5%. The Sensing Solutions segment maintained consistent market outgrowth, with industrial applications growing approximately 1%, driven by A2L leak detection products.

Strategic Initiatives and Leadership Changes

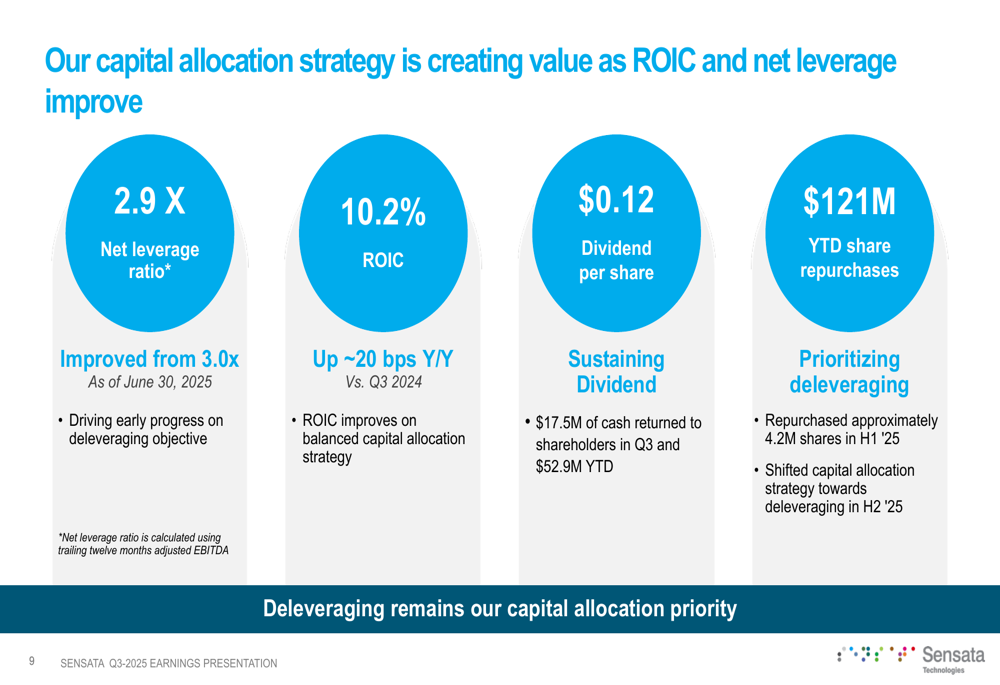

CEO Stephan von Schuckmann emphasized the company’s focused execution in his statement: "We have exceeded expectations across all key financial metrics, delivering adjusted operating margins of 19.3%. Our disciplined approach to working capital has driven robust Free Cash Flow of $136.2 million at a 105% conversion rate, enabling us to reduce net leverage to 2.9x."

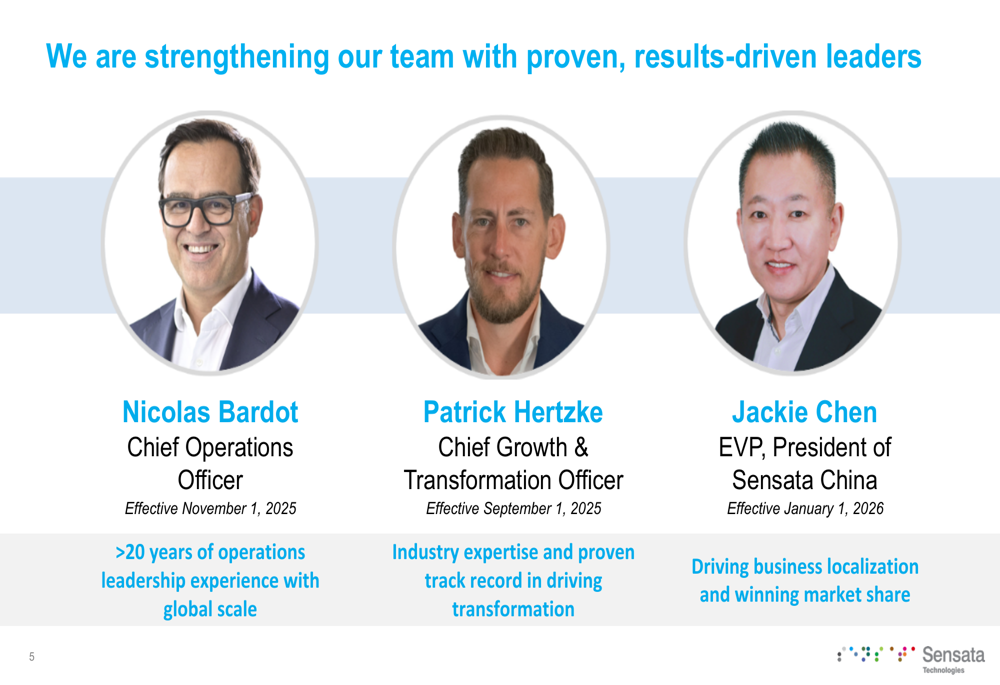

Sensata announced three strategic leadership appointments to strengthen its executive team and drive future growth. These include Nicolas Bardot as Chief Operations Officer, Patrick Hertzke as Chief Growth & Transformation Officer, and Jackie Chen as EVP, President of Sensata China.

The company’s capital allocation strategy has shifted toward deleveraging in the second half of 2025, after repurchasing approximately 4.2 million shares in the first half of the year. This approach has already yielded results, with net leverage improving to 2.9x from 3.0x at the end of the previous quarter. Meanwhile, Return on Invested Capital (ROIC) increased to 10.2%, up approximately 20 basis points year-over-year.

Product Innovation for Future Growth

Sensata highlighted several product innovations that are expected to drive future growth. The company has secured market leadership in A2L gas leak sensing with major OEM contracts, positioning it to potentially generate over $100 million in revenue run-rate in the US market alone.

In the automotive sector, Sensata has secured business with two OEMs in China for its Tire Burst Detection technology, with growing interest from other regions. Additionally, the company’s intelligent, switchable solution for next-generation electric vehicles was a finalist for the Electric Vehicle Charging Innovation Excellence Award at the 2025 North American Battery Show.

Financial Outlook and Guidance

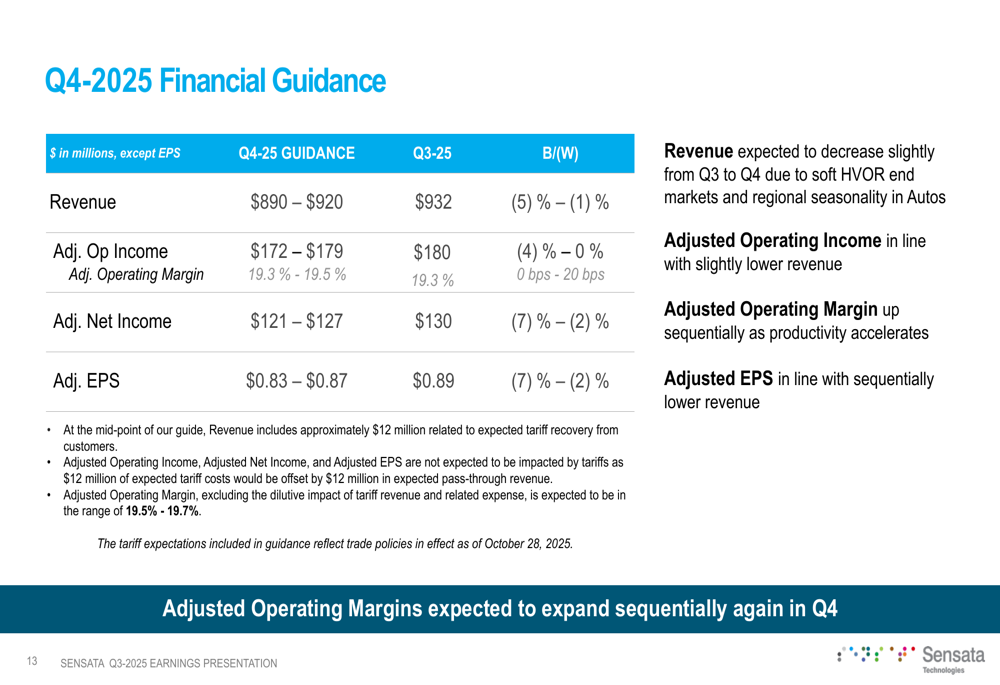

Looking ahead to the fourth quarter of 2025, Sensata provided guidance that suggests continued margin improvement despite slightly lower sequential revenue. The company expects Q4 revenue between $890 million and $920 million, with adjusted operating income of $172-$179 million, representing margins of 19.3-19.5%.

Adjusted EPS is projected to be between $0.83 and $0.87 for Q4 2025, reflecting the slightly lower sequential revenue but benefiting from accelerating productivity initiatives. Management noted that adjusted operating margins are expected to expand sequentially again in Q4.

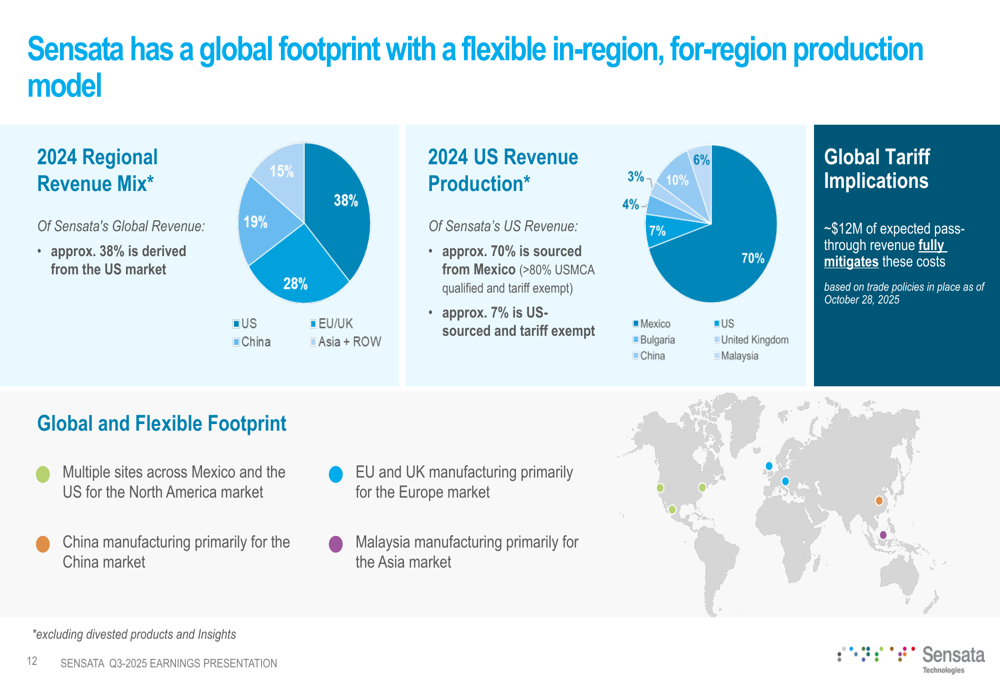

Regarding global trade concerns, Sensata indicated that approximately $12 million of expected pass-through revenue would fully mitigate potential tariff costs based on trade policies in place as of the presentation date. The company’s diversified global footprint, with manufacturing facilities across multiple regions, provides some insulation against geopolitical and trade-related disruptions.

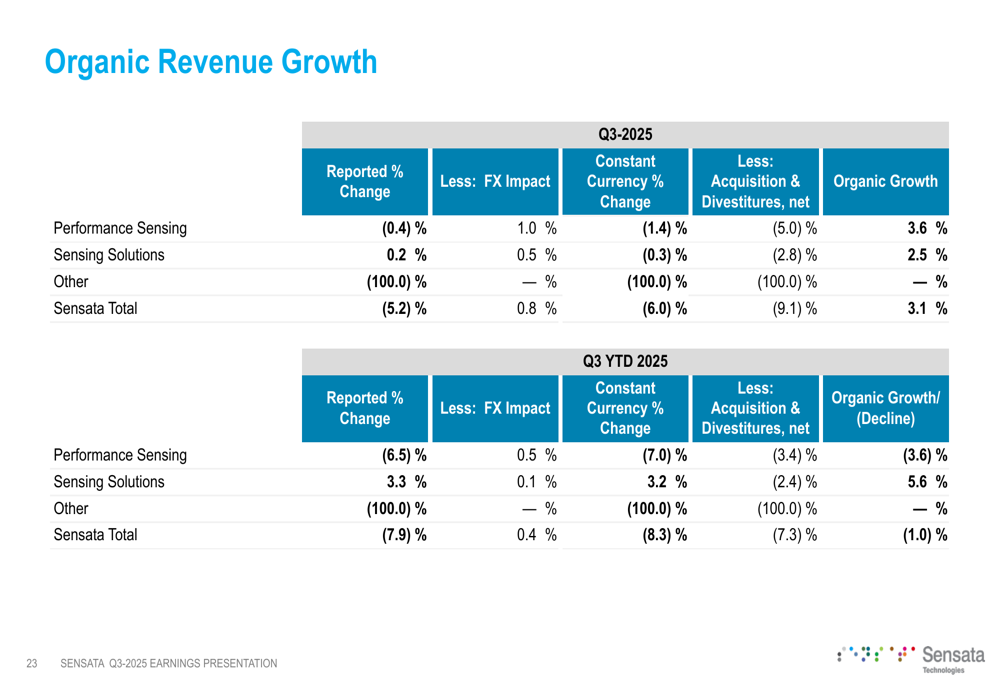

The company’s organic revenue growth of 3.1% in Q3 2025 demonstrates its ability to outpace market growth in key segments, with Performance Sensing achieving 3.6% organic growth and Sensing Solutions delivering 2.5% organic growth:

As Sensata continues to execute on its three key pillars of operational excellence, capital allocation optimization, and return to growth, investors will be watching closely to see if the company can maintain its momentum of exceeding guidance while continuing to improve its balance sheet metrics and free cash flow conversion in the quarters ahead.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.