ACV Auctions shares tumble as guidance disappoints

Introduction & Market Context

Sensient Technologies Corporation (NYSE:SXT) presented its second quarter 2025 earnings results on July 25, highlighting strong performance across its business segments. The company’s stock closed up 3.52% at $110 following the presentation, reflecting positive investor sentiment despite a 2.91% decline in premarket trading.

The flavor and color manufacturer continues to build on its momentum from Q1, when the stock rose 6% despite slight misses on revenue and EPS forecasts. Sensient’s shares are now trading near their 52-week high of $113.87, significantly above their 52-week low of $66.15.

Quarterly Performance Highlights

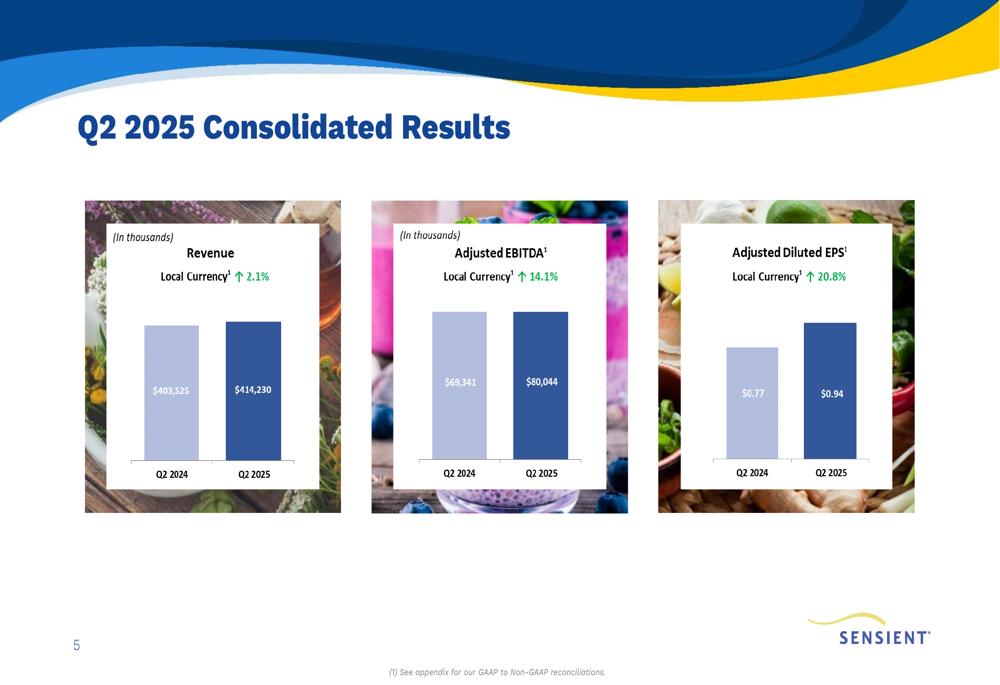

Sensient reported Q2 2025 revenue of $414.23 million, a 2.1% increase in local currency compared to $403.53 million in Q2 2024. More impressively, adjusted EBITDA rose 14.1% to $80.04 million, and adjusted diluted EPS jumped 20.8% to $0.94, demonstrating substantial margin improvement.

As shown in the following consolidated results chart:

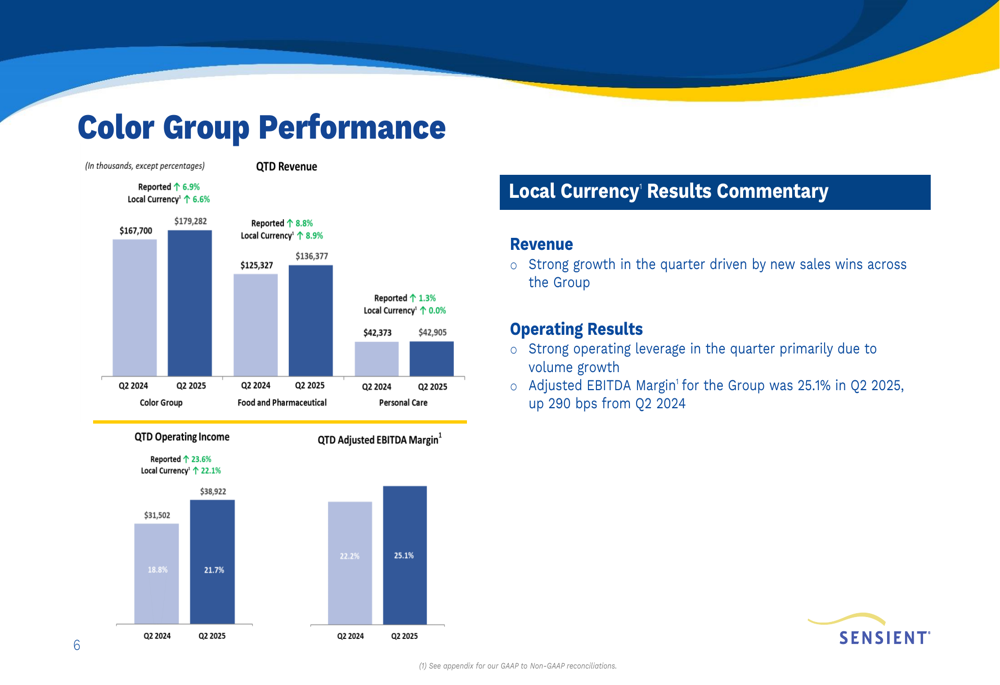

The Color Group emerged as the standout performer, with revenue increasing 6.9% (6.6% in local currency) and operating income surging 23.6%. The segment’s adjusted EBITDA margin expanded significantly from 22.2% to 25.1%, driven by new sales wins and improved operating leverage.

The detailed Color Group performance metrics illustrate this strong growth:

The Flavors & Extracts Group delivered mixed results, with overall revenue increasing 2.8% (3.2% in local currency). While the Flavors, Extracts, and Flavor Ingredients business grew by 5.2%, the Natural Ingredients segment declined by 17.4%. Despite this mixed performance, the group’s adjusted EBITDA margin improved from 16.2% to 17.8%.

The Asia Pacific Group also performed strongly, with revenue increasing 10.8% (7.6% in local currency) and operating income rising 13.5%. The segment’s adjusted EBITDA margin increased slightly from 22.0% to 22.3%.

Strategic Initiatives

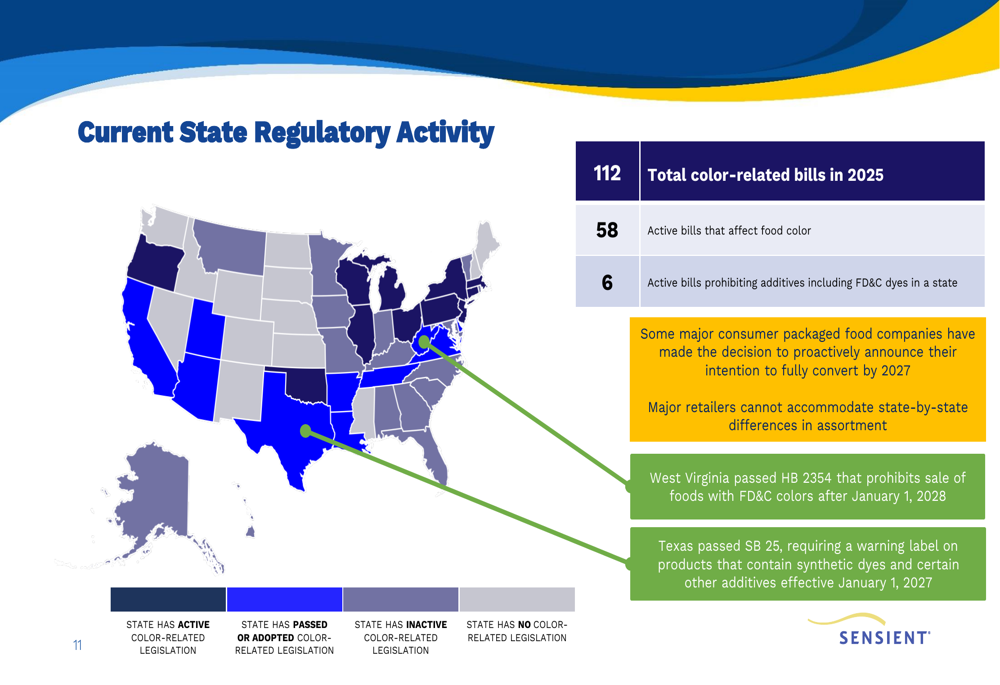

A significant focus of the presentation was the opportunity presented by regulatory changes affecting synthetic colors. Sensient highlighted several upcoming regulatory actions, including the first School Lunch Ban in West Virginia (August 2025), a potential federal Red 3 Ban (January 2027), state-wide warning labels in Texas (January 2027), and the first state-wide Synthetic Color Ban in West Virginia (January 2028).

The regulatory landscape and conversion opportunity is illustrated in this slide:

Sensient estimates that its synthetic colors revenue for the food and pharmaceutical market in the U.S. and Latin America is approximately $110 million. The company noted that conversion from synthetic to natural colors can result in a conversion factor of nearly 10-to-1, representing a substantial growth opportunity.

The current state of regulatory activity across the U.S. shows widespread legislative interest in color additives:

To capitalize on this opportunity, Sensient highlighted its innovative natural color offerings, including Microfine™ and Butterfly Pea Flower Extract. These products are specifically designed for various applications and offer benefits such as heat stability, extensive shade range, and clean label attributes.

The company’s natural color innovations are showcased in this product highlight:

This strategic focus on natural colors aligns with CEO Paul Manning’s statement from the Q1 earnings call that "the conversion from synthetics to naturals is the largest revenue opportunity that we have seen in our company’s history."

Financial Analysis

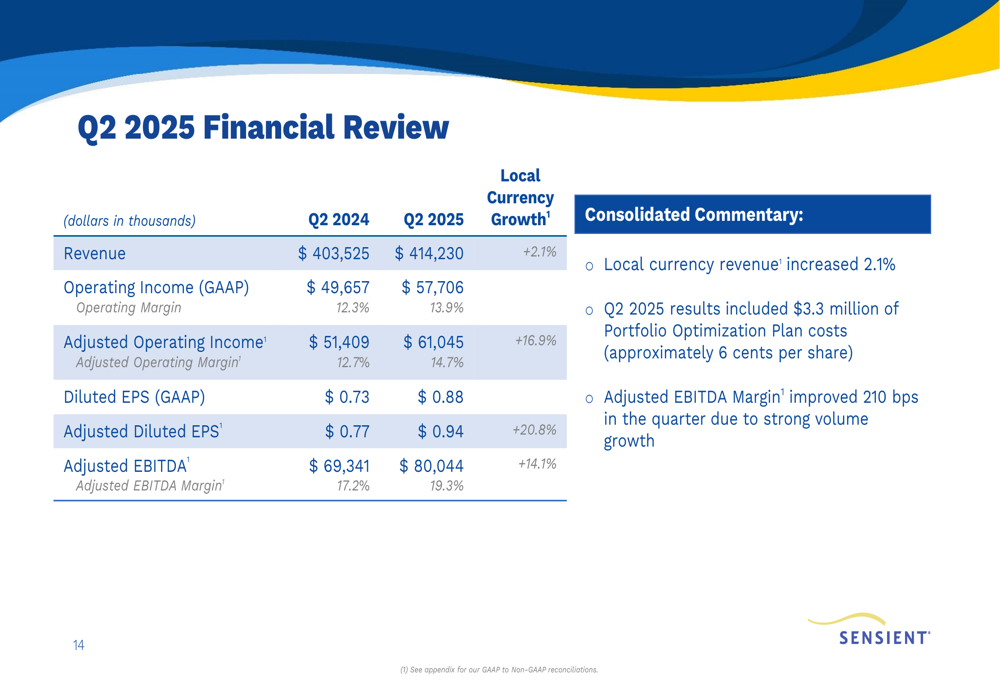

Sensient’s financial position continued to strengthen in Q2 2025. Cash flow from operations increased 10.2% to $48.3 million, compared to $43.8 million in Q2 2024, driven by improved earnings and working capital management.

Capital expenditures nearly doubled to $21.2 million from $11.8 million in the prior year, reflecting the company’s investment in growth initiatives, particularly in natural color capabilities. This aligns with the company’s Q1 decision to defer its stock buyback program to focus on these investments.

The company’s debt position and leverage metrics also improved, with net debt to credit adjusted EBITDA decreasing to 2.4x from 2.6x in Q2 2024.

The comprehensive financial review provides a clear picture of the company’s performance:

Forward-Looking Statements

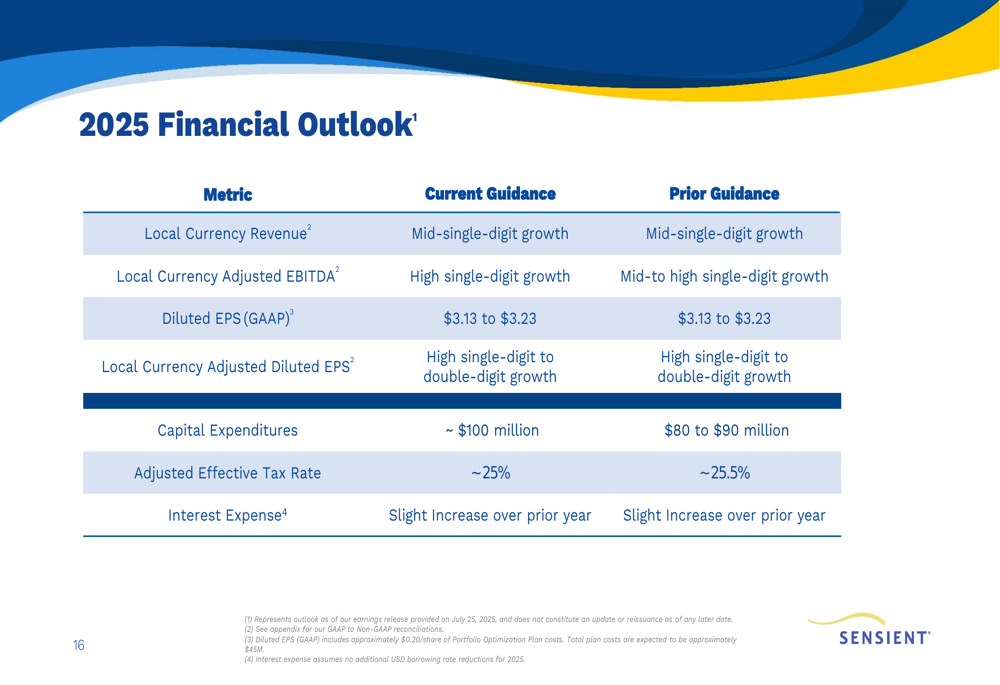

Sensient maintained its full-year 2025 outlook, projecting mid-single-digit growth for local currency revenue and high single-digit growth for local currency adjusted EBITDA. The company expects local currency adjusted diluted EPS to grow at a high single-digit to double-digit rate.

The detailed financial outlook is presented in this guidance table:

Capital expenditures for 2025 are estimated at approximately $100 million, significantly higher than previous years, reflecting the company’s investment in growth opportunities, particularly in natural colors. The adjusted effective tax rate is projected to be around 25%, and interest expense is expected to increase slightly over the prior year.

For the long term, Sensient continues to project mid-single-digit growth for local currency revenue and high single-digit growth for local currency adjusted EBITDA, indicating confidence in sustainable growth beyond 2025.

The company remains well-positioned to capitalize on the ongoing shift from synthetic to natural colors, which it views as a transformative opportunity for its business. With strong performance across its segments, improving margins, and a clear strategic direction, Sensient appears poised for continued growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.