Bitcoin price today: dips below $109k as recovery stalls, "Uptober" cheer fizzles

Shimmick Corporation (NASDAQ:SHIM) reported significant revenue growth and margin improvement in its second quarter 2025 earnings presentation released on August 14, 2025. The infrastructure solutions provider highlighted a 42% year-over-year revenue increase, strategic expansion into electrical contracting, and an evolving project backlog, while adjusting its full-year guidance.

Quarterly Performance Highlights

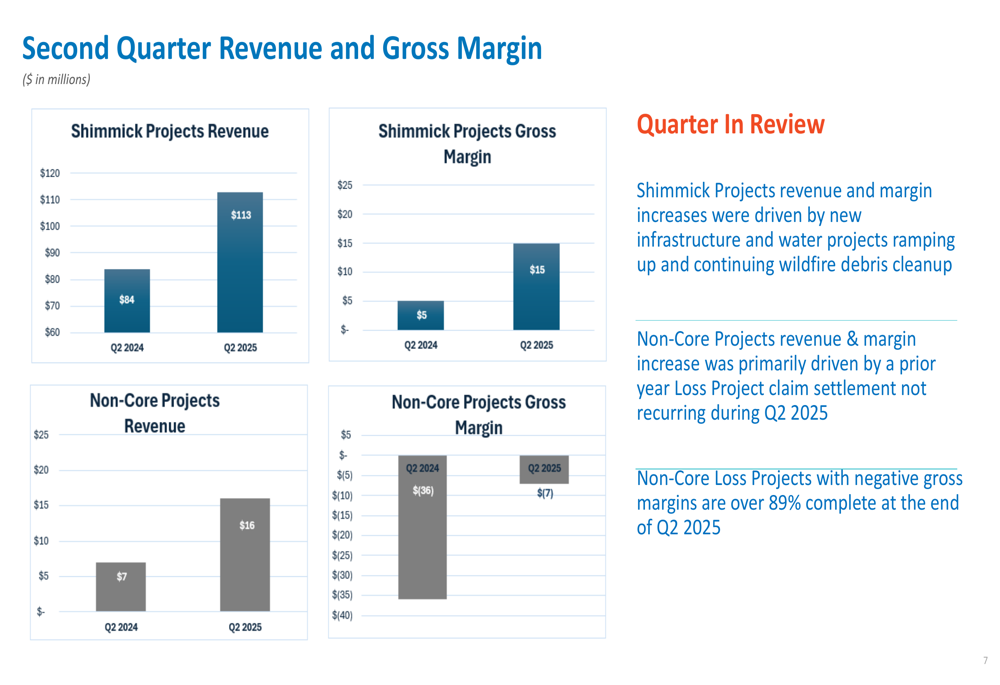

Shimmick reported Q2 2025 revenue of $128 million, representing a 42% increase compared to the same period last year. The company’s gross margin reached $8 million, a substantial improvement from the $(31) million loss reported in Q2 2024. This performance marks a recovery from the company’s challenging first quarter, where it missed both EPS and revenue forecasts.

The company’s core "Shimmick Projects" segment drove the positive results, contributing $113 million in revenue and $15 million in gross margin. Meanwhile, "Non-Core Projects" posted $16 million in revenue with a negative gross margin of $(7) million, though this represented an improvement from the $(36) million loss in the prior-year period.

As shown in the following quarterly performance chart:

"Shimmick Projects revenue and margin increases were driven by new infrastructure and water projects ramping up and continuing wildfire debris cleanup," noted the company in its presentation. The company also highlighted that selling, general, and administrative expenses decreased by 20% to $15 million due to its ongoing Transformation Plan.

Despite these improvements, Shimmick still reported a net loss of $8 million for the quarter, though Adjusted EBITDA was nearly flat at $(0.2) million, largely impacted by the Non-Core Projects segment. The company maintained a liquidity position of $73 million as of July 4, 2025, representing a $2 million increase from Q1 2025.

Backlog and Project Wins

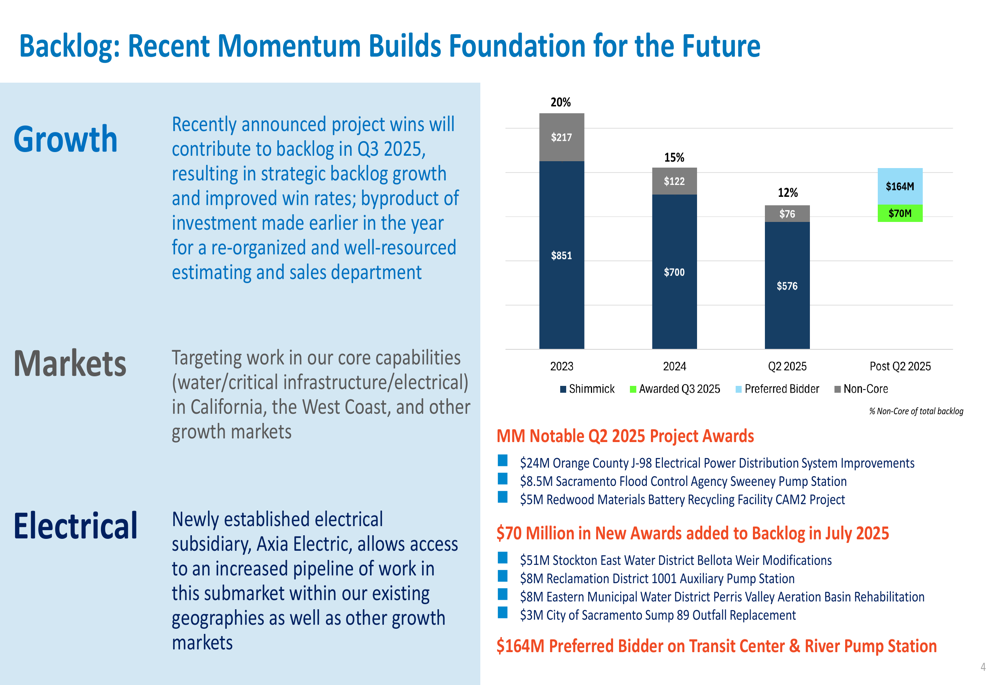

Shimmick’s backlog stood at approximately $652 million as of July 4, 2025, with over 88% classified as Shimmick Projects. The company reported significant momentum in new project awards that will contribute to its Q3 2025 backlog, including $70 million in new awards added in July 2025 and selection as preferred bidder on $164 million worth of projects including a Transit Center and River Pump Station.

The company’s backlog development and recent project wins are illustrated in the following chart:

Notable recent project awards include a $51 million Stockton East Water District Bellota Weir Modifications project, a $24 million Orange County electrical power distribution system improvement project, and several other water infrastructure projects ranging from $3 million to $8.5 million.

The presentation highlighted that the percentage of Non-Core projects in the backlog has decreased from 20% to 12%, reflecting the company’s strategic shift toward its core competencies. Additionally, Non-Core Loss Projects with negative gross margins are now over 89% complete, suggesting diminishing drag on future financial performance.

Strategic Initiatives

A key strategic development highlighted in the presentation was the launch of Axia Electric, a new dedicated electrical subsidiary. This expansion aims to capitalize on growing opportunities in the electrical contracting services market for complex infrastructure projects.

The company provided the following overview of its new subsidiary:

Based in California, Axia Electric will deliver electrical contracting services across the United States, focusing on industrial, transportation, commercial, advanced manufacturing, and data center markets. The subsidiary is actively pursuing new work in California, Oregon, Washington, Idaho, Hawaii, Tennessee, Georgia, and Texas.

This expansion aligns with Shimmick’s broader market strategy, which targets an addressable market estimated at $100 billion per year across four major segments: Water Resources, Energy Transition & Technology, Climate Resilience, and Sustainable Transportation.

The company’s addressable market and client base are detailed in this slide:

"Investments in strategic backlog growth are showing results," the company noted in its closing remarks, adding that it remains "optimistic about opportunities in the electrical market with Axia Electric."

Updated 2025 Guidance

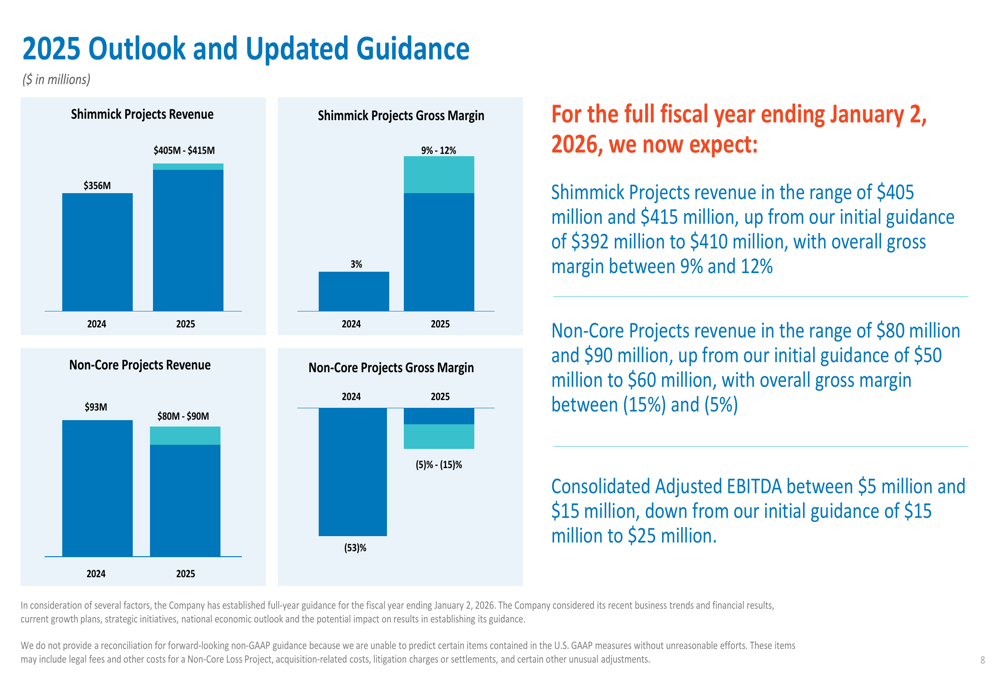

Shimmick provided updated guidance for fiscal year 2025 (ending January 2, 2026), revising some of its previous projections:

For Shimmick Projects, the company now expects revenue between $405 million and $415 million, up from its initial guidance of $392 million to $410 million, with overall gross margin between 9% and 12%. For Non-Core Projects, revenue is projected between $80 million and $90 million, higher than the initial guidance of $50 million to $60 million, with gross margin between (15%) and (5%).

However, the company reduced its Consolidated Adjusted EBITDA guidance to between $5 million and $15 million, down from the initial projection of $15 million to $25 million. This adjustment suggests ongoing challenges despite the revenue growth.

Forward-Looking Statements

Shimmick expressed optimism about its future prospects, citing increased bidding activity and a robust pipeline as macroeconomic concerns ease. The company highlighted strong investment in water, industrial, power, data center, and manufacturing sectors, noting that it has available capacity to take on additional volume.

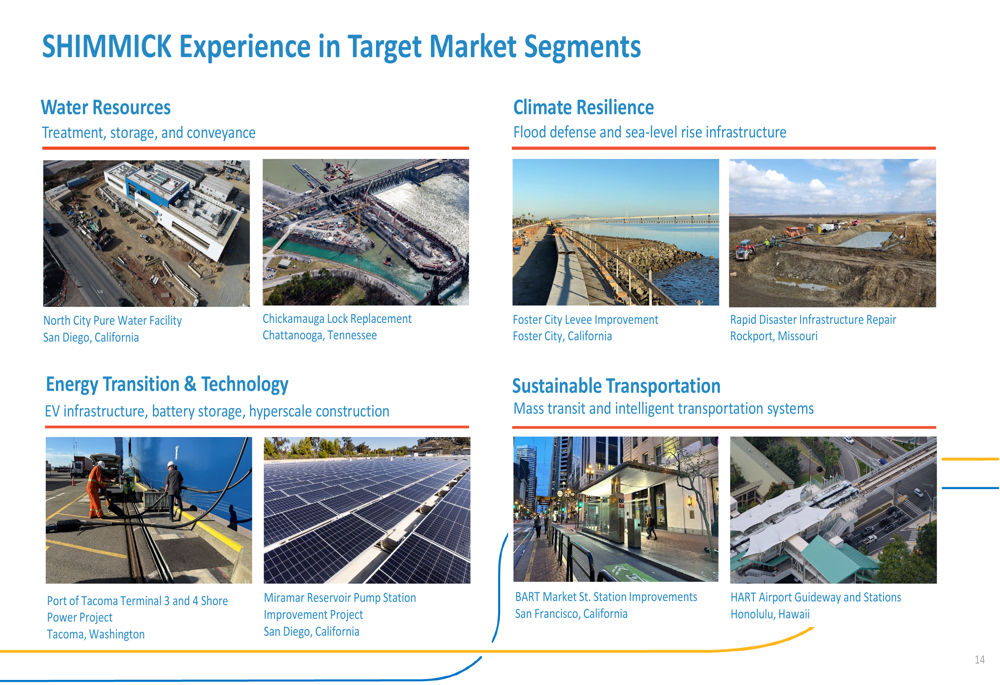

The company’s experience across its target market segments is illustrated in the following slide:

Looking ahead, Shimmick expects overall margins to continue improving as it completes its remaining Non-Core Projects and focuses on higher-margin core business segments. The company’s stock closed at $2.19 on August 14, 2025, down 3.65% for the day, but remains above its 52-week low of $1.30.

While the Q2 results show significant improvement over both the previous quarter and the prior year, investors will likely be watching closely to see if Shimmick can maintain its revenue momentum while delivering on its revised EBITDA guidance for the remainder of fiscal year 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.