Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Silvaco Group Inc (NASDAQ:SVCO) reported its second quarter 2025 financial results on August 6, 2025, showing continued revenue challenges while emphasizing strategic acquisitions and AI-focused market expansion. The semiconductor design software company, which went public in May 2024, saw its stock decline 6.17% to $4.87 following the earnings release, extending a significant downward trend from its 52-week high of $17.01.

The Q2 results follow a disappointing first quarter that sent shares tumbling nearly 14% after a significant earnings miss. Despite these challenges, Silvaco maintains its full-year guidance, suggesting management expects substantial improvement in the second half of fiscal 2025.

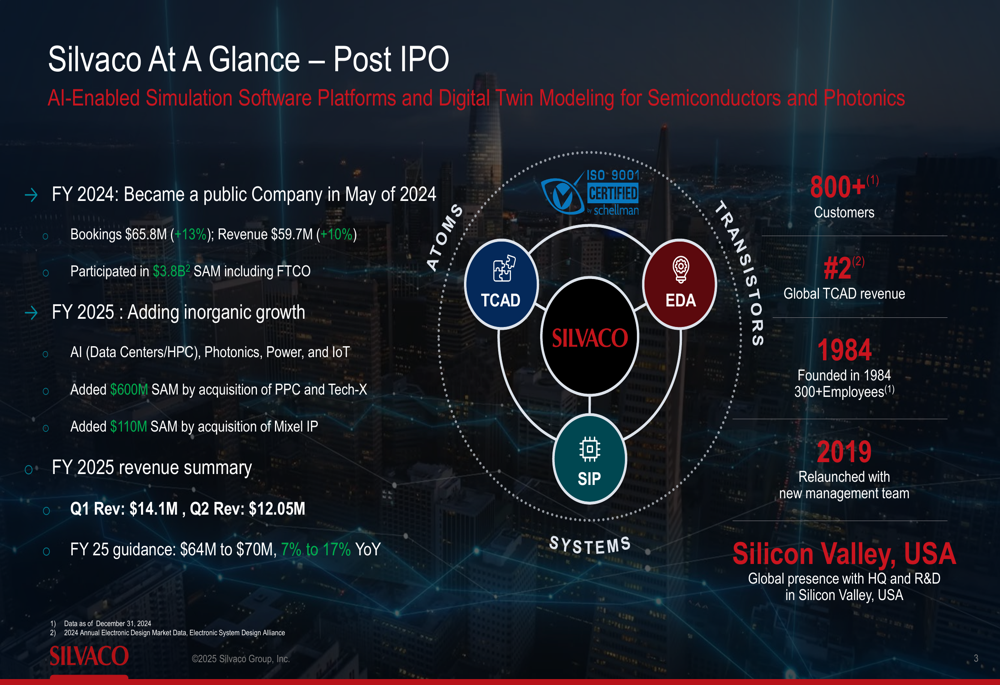

As shown in the company’s post-IPO overview slide, Silvaco positions itself as the #2 global player in TCAD (Technology Computer-Aided Design) with over 800 customers worldwide:

Quarterly Performance Highlights

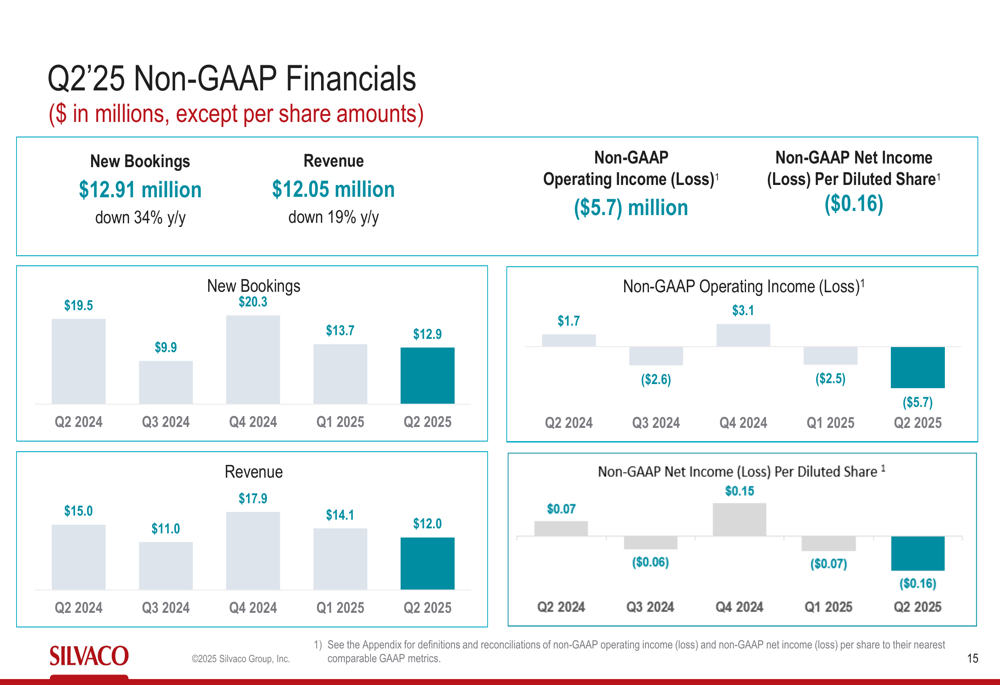

Silvaco’s Q2 2025 financial results showed significant year-over-year declines across key metrics. Revenue fell 19% to $12.05 million compared to $15.0 million in Q2 2024. New bookings declined even more sharply, down 34% to $12.91 million from $19.5 million in the prior year period, though the company attributes this largely to a high-value FTCO (Fab Technology Co-Optimization) booking in Q2 2024.

The company reported a non-GAAP operating loss of $5.7 million, compared to operating income of $1.7 million in the same quarter last year. Non-GAAP net loss per diluted share was $0.16, versus earnings of $0.07 per share in Q2 2024.

The following chart illustrates Silvaco’s quarterly financial performance trends:

Gross margin also declined to 76% in Q2 2025 from 86% in the prior year period. Despite these challenges, the company highlighted that 14% of revenue came from 10 new customers ($3.9 million in bookings), while 40% came from expansion in existing customers ($4.3 million in bookings).

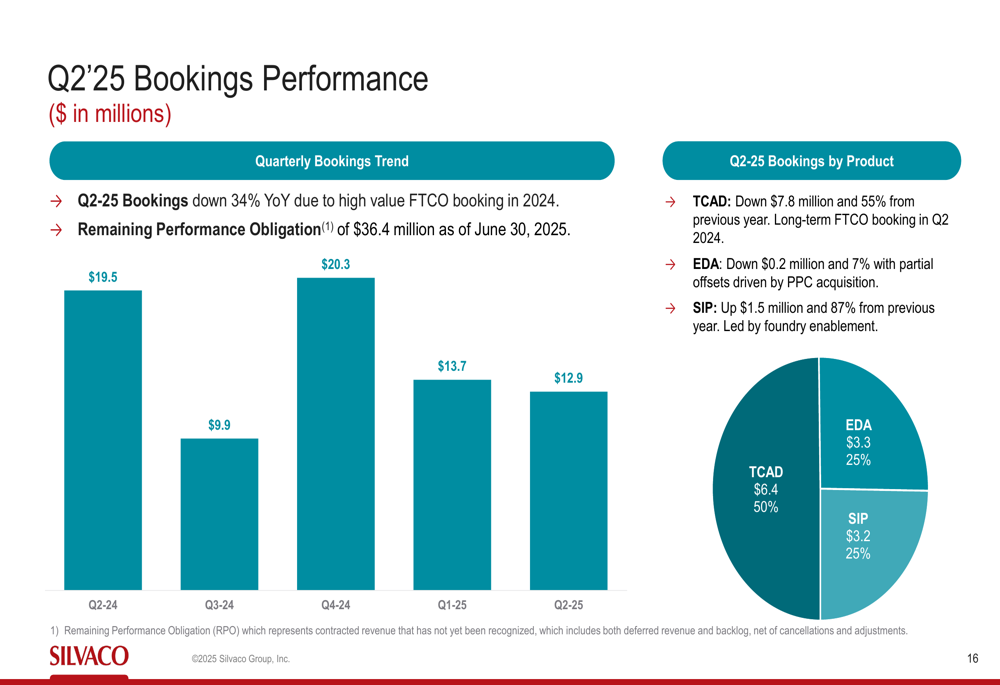

The company’s bookings performance breakdown reveals that TCAD bookings were down 55% year-over-year, while EDA (Electronic Design Automation) declined 7%, partially offset by the PPC acquisition. Silicon IP (SIP) bookings provided a bright spot, up 87% from the previous year, led by foundry enablement:

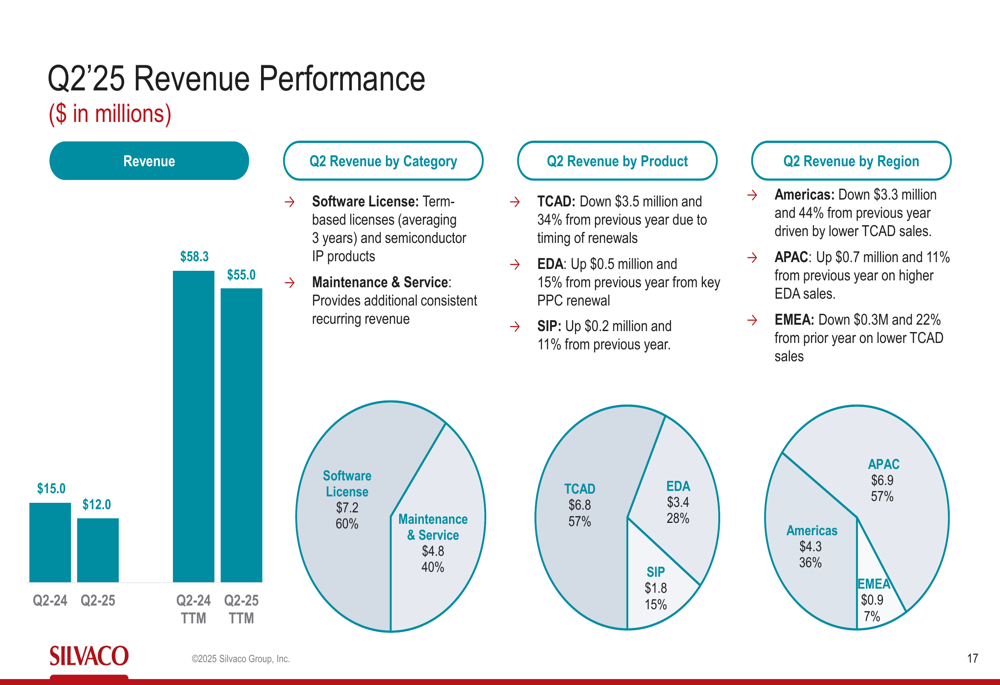

Revenue by product category and region shows diversification across the company’s portfolio:

Strategic Initiatives

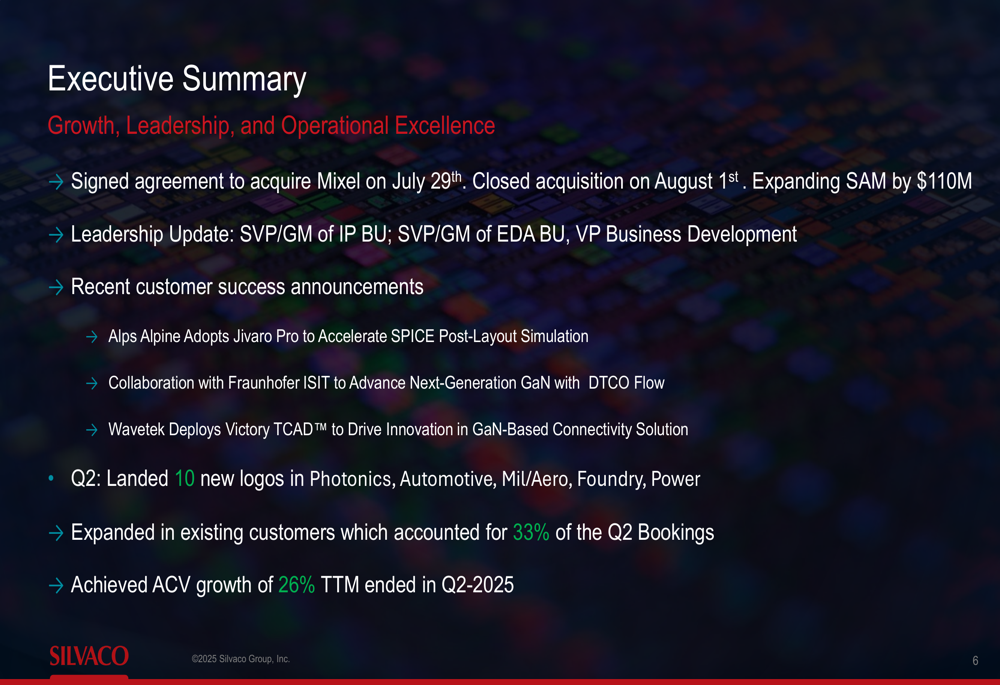

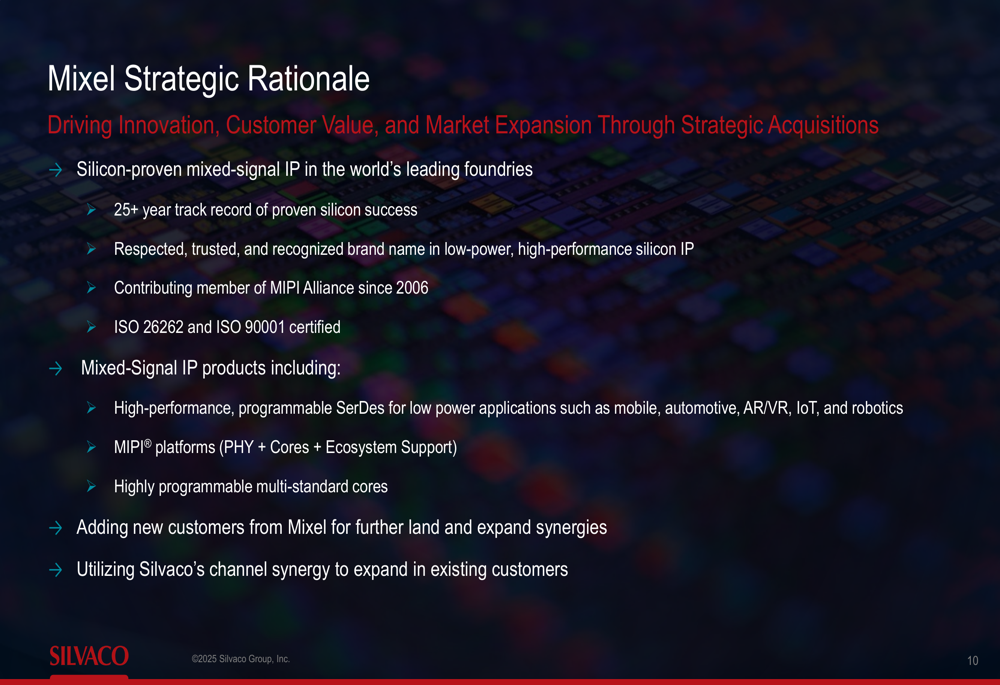

Despite current financial challenges, Silvaco emphasized its strategic acquisitions and market expansion initiatives. The company announced the signing and closing of its acquisition of Mixel, a provider of mixed-signal IP, expanding Silvaco’s serviceable addressable market (SAM) by $110 million.

The executive summary highlighted key achievements for the quarter:

The Mixel acquisition represents a significant strategic move to enhance Silvaco’s position in mixed-signal IP, particularly for mobile, automotive, AR/VR, IoT, and robotics applications:

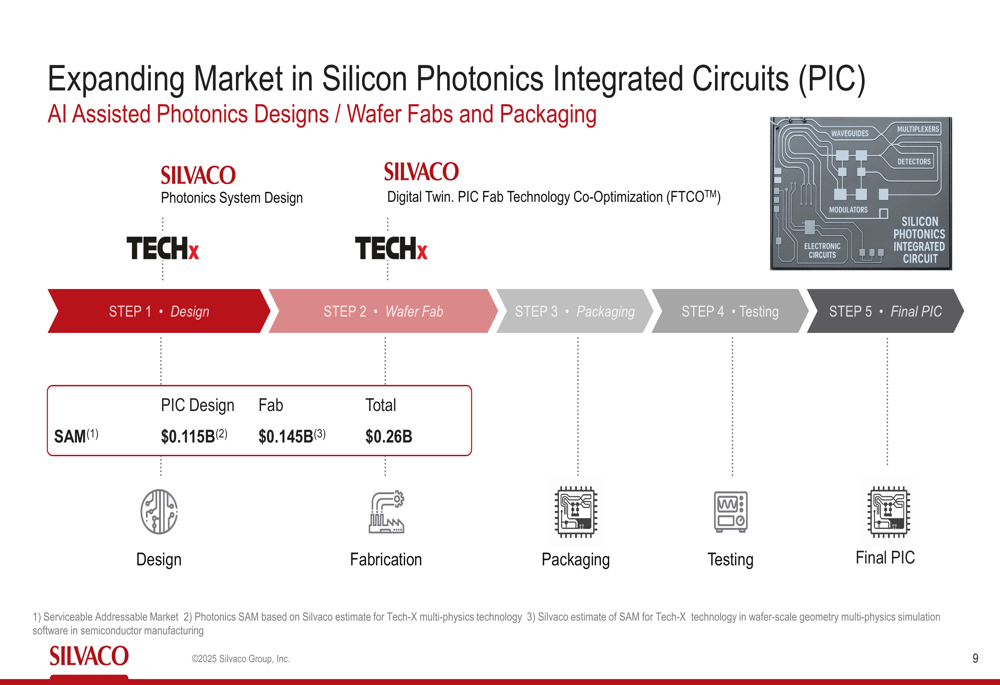

Silvaco is focusing on AI-assisted design/wafer fabs and photonics circuits/packaging as its main growth engines. The company is particularly targeting expansion in Silicon Photonics Integrated Circuits (PIC) for AI end-markets including high-performance computing, automotive, and sensing:

Forward-Looking Statements

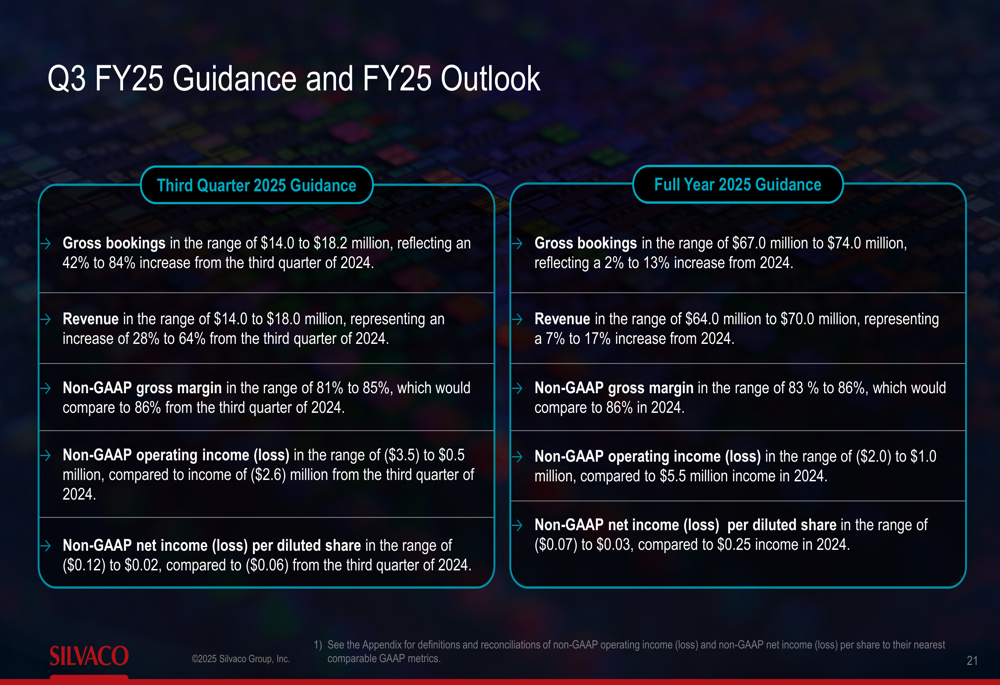

Despite the Q2 revenue decline, Silvaco maintained its full-year 2025 guidance, suggesting management expects significant improvement in the second half of the fiscal year. For Q3 2025, the company projects:

- Gross bookings of $14.0 to $18.2 million (42% to 84% increase from Q3 2024)

- Revenue of $14.0 to $18.0 million (28% to 64% increase from Q3 2024)

- Non-GAAP gross margin of 81% to 85%

- Non-GAAP operating loss between $3.5 million and $0.5 million

- Non-GAAP net loss per diluted share between $0.12 and $0.02

For the full fiscal year 2025, Silvaco continues to project:

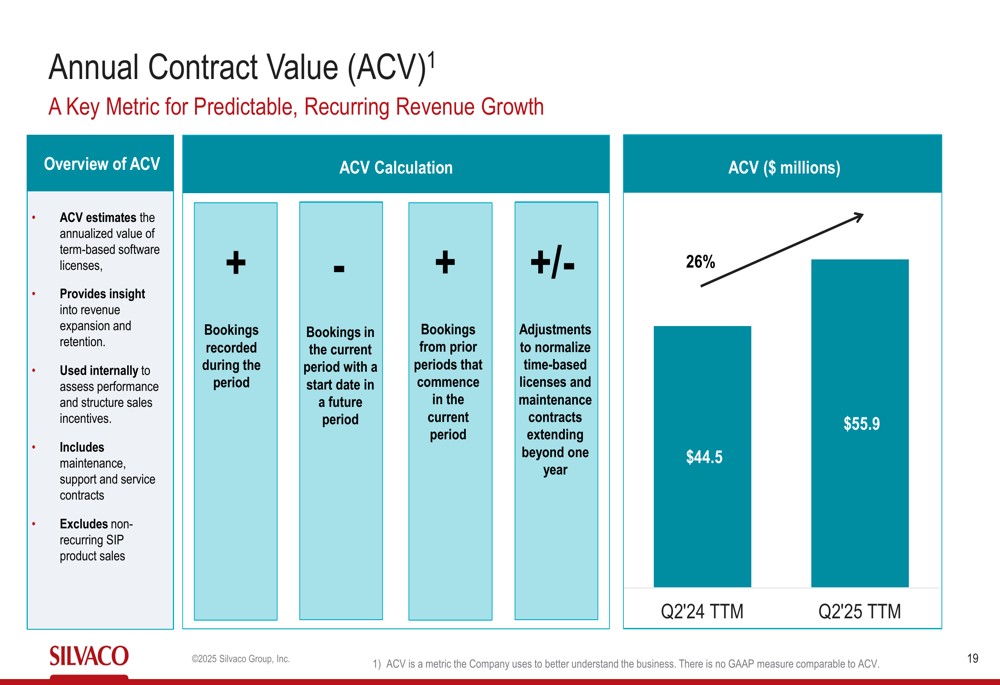

The company emphasized its Annual Contract Value (ACV) growth of 26% for the trailing twelve months ended Q2 2025, highlighting the strengthening of its recurring revenue base:

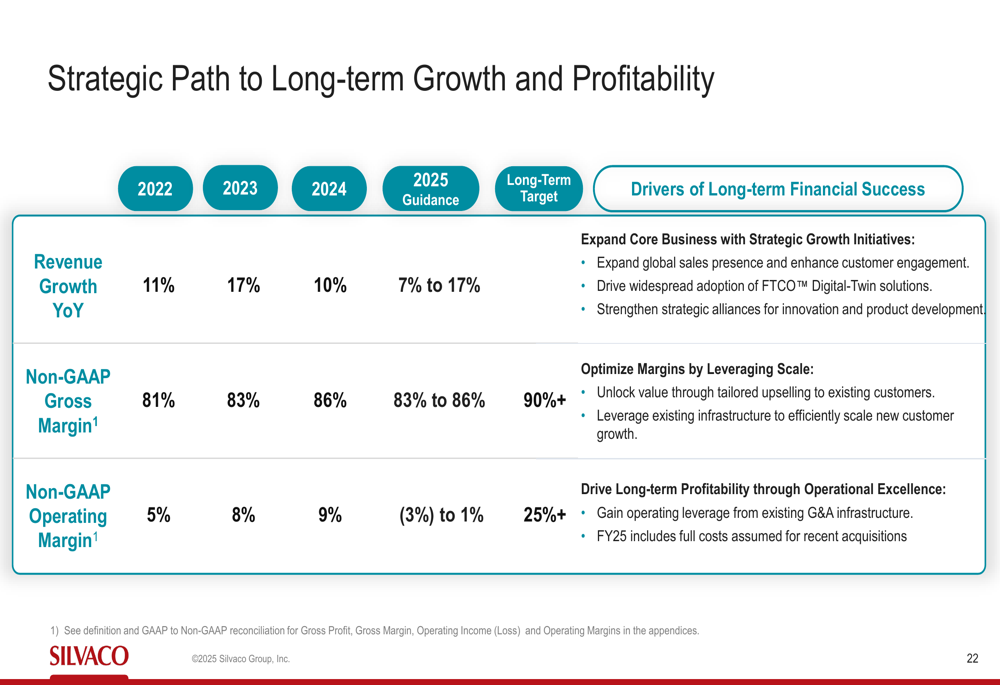

Looking further ahead, Silvaco outlined its strategic path to long-term growth and profitability:

Conclusion

Silvaco’s Q2 2025 results present a mixed picture for investors. The continued revenue decline and widening losses are concerning, particularly following the disappointing Q1 results that sent the stock tumbling. However, the company’s maintained full-year guidance suggests management expects a significant turnaround in the second half of fiscal 2025.

The strategic acquisitions, particularly Mixel, and focus on high-growth AI and photonics markets could position Silvaco for future growth if executed successfully. The 26% growth in Annual Contract Value indicates some underlying strength in recurring revenue, despite the quarterly revenue declines.

Investors will likely be watching Q3 results closely to determine whether Silvaco can deliver on its projected recovery and maintain its full-year guidance. With the stock trading near its 52-week low, market sentiment appears cautious about the company’s near-term prospects despite its long-term strategic vision.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.