Microvast Holdings announces departure of chief financial officer

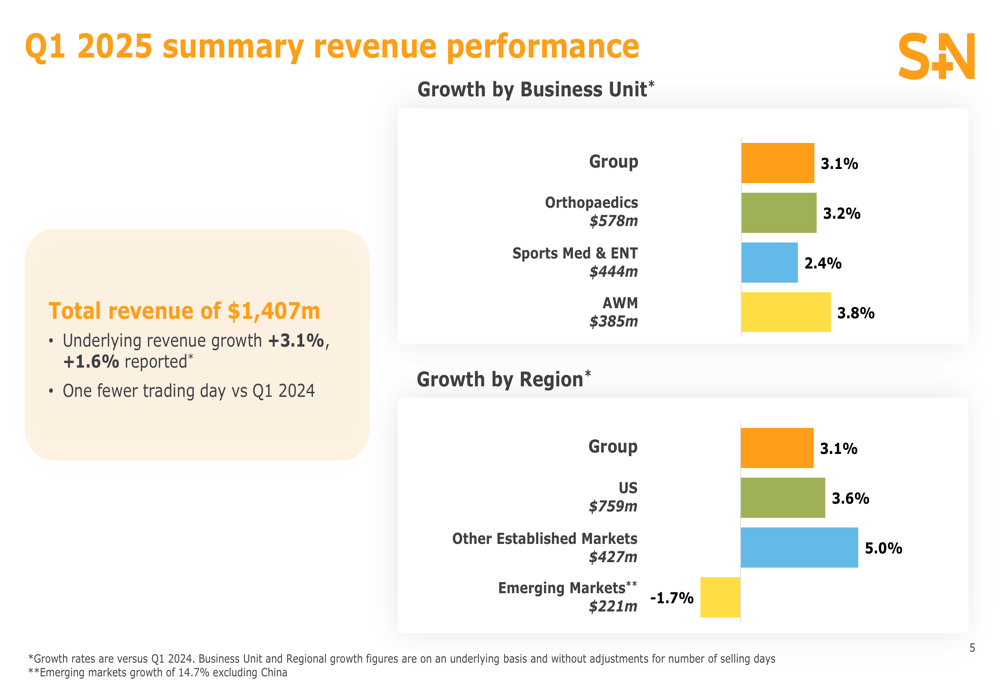

Smith & Nephew PLC (LSE:LON:SN) reported underlying revenue growth of 3.1% in its first quarter of 2025, according to the company’s presentation released on April 30. The medical technology company achieved this growth despite headwinds from China and one fewer trading day compared to the prior year period.

Quarterly Performance Highlights

The company reported total revenue of $1.407 billion for Q1 2025, representing 1.6% growth on a reported basis. The difference between underlying and reported growth was primarily due to a 1.5% negative currency impact.

Regional performance varied significantly, with the US market growing 3.6% to $759 million and Other Established Markets increasing by 5.0% to $427 million. Emerging Markets declined by 1.7% to $221 million, though the company noted strong growth of 14.7% when excluding China.

As shown in the following revenue breakdown by business unit and region:

Smith & Nephew’s CEO Deepak Nag emphasized that 2025 is "a key year of delivery," according to the earnings call transcript, highlighting the importance of strategic execution. The company maintained its full-year 2025 guidance of approximately 5% underlying revenue growth and trading margin of 19.0-20.0%, despite an expected $15-20 million tariff impact.

Business Unit Performance

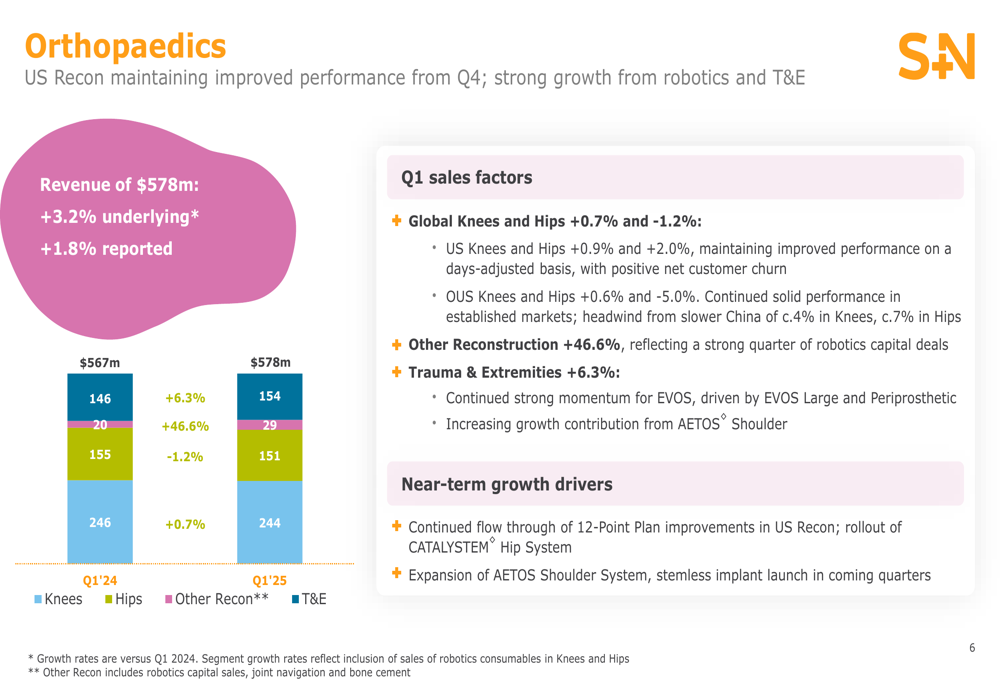

The Orthopaedics business unit, which includes knees, hips, and trauma & extremities products, delivered 3.2% underlying growth, generating $578 million in revenue. The company reported continued improvement in US reconstruction, with US Knees growing 0.9% and US Hips increasing by 2.0%. Trauma & Extremities showed particularly strong performance with 6.3% growth.

The detailed breakdown of Orthopaedics performance shows:

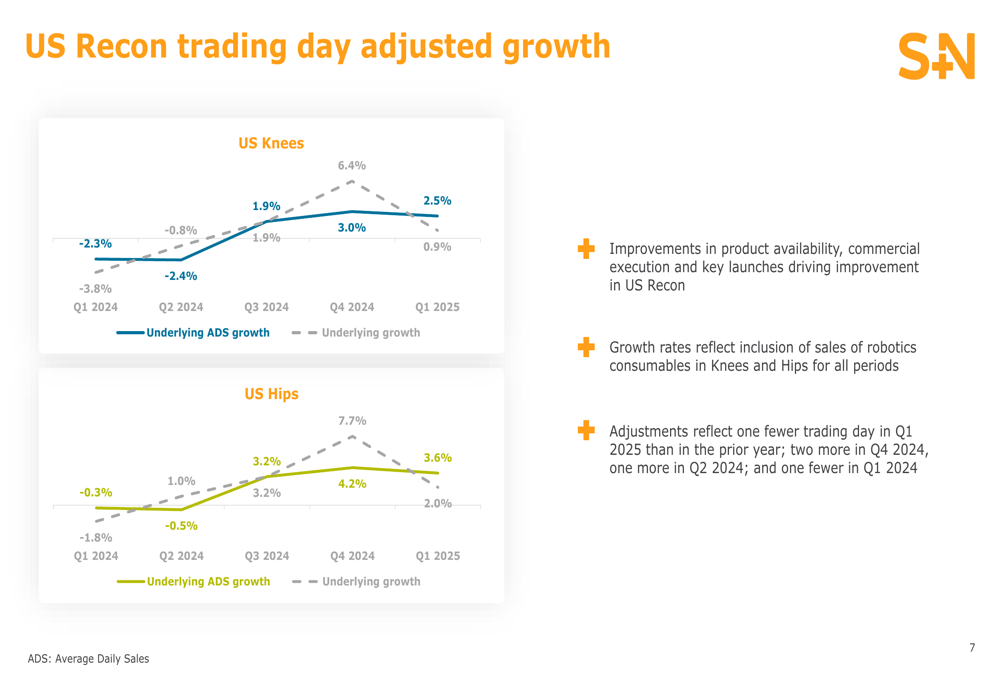

Smith & Nephew highlighted the sustained improvement in US reconstruction business, which has been a focus area under the company’s 12-Point Plan. The trading day adjusted growth rates show the positive trajectory:

The Sports Medicine & ENT business unit achieved 2.4% underlying growth, reaching $444 million in revenue. When excluding China, this segment delivered impressive 7.8% underlying growth, demonstrating the significant impact of China’s volume-based procurement (VBP) program on this business unit. Sports Medicine Joint Repair grew 10.6% excluding China, while ENT delivered solid growth of 7.8%.

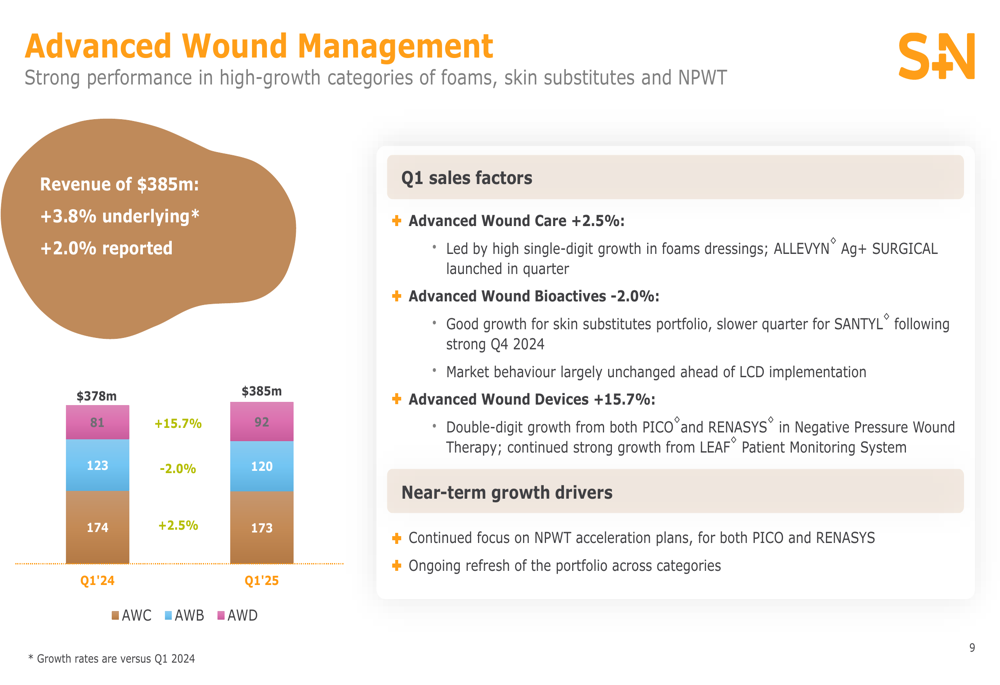

The Advanced Wound Management business unit was the strongest performer with 3.8% underlying growth, generating $385 million in revenue. Advanced Wound Devices was the standout category with 15.7% growth, while Advanced Wound Care grew 2.5%. Advanced Wound Bioactives declined by 2.0%.

The detailed breakdown of Advanced Wound Management performance reveals:

Innovation and Product Pipeline

Smith & Nephew emphasized its continued focus on innovation as a key growth driver. The company highlighted several recent product launches and new clinical evidence supporting its existing portfolio.

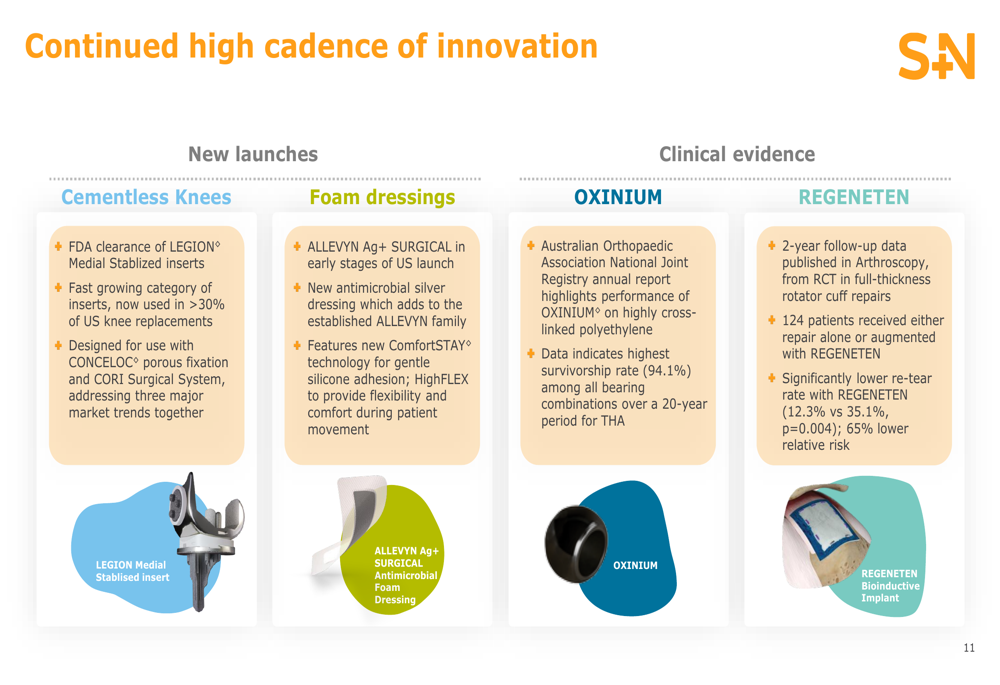

In the reconstruction segment, the company received FDA clearance for LEGION Medial Stabilized inserts for cementless knees. In wound care, the ALLEVYN Ag+ SURGICAL foam dressing is in the early stages of US launch.

The company also presented compelling clinical evidence for its OXINIUM technology, which demonstrated the highest survivorship rate among all bearing combinations over a 20-year period for total hip arthroplasty. Additionally, the REGENETEN Bioinductive Implant showed a significantly lower re-tear rate (12.3% vs 35.1%) and 65% lower relative risk compared to alternatives.

As illustrated in the company’s innovation highlights:

Forward Guidance and Outlook

Smith & Nephew maintained its full-year 2025 guidance, projecting underlying revenue growth of approximately 5% and a trading margin between 19.0-20.0%. The company expects higher growth for the remainder of the year as external headwinds ease.

The guidance includes the anticipated impact of tariffs, estimated at $15-20 million for 2025. With 54% of revenue coming from the US market, the company is monitoring the tariff situation closely but has incorporated expected impacts into its outlook.

Management expressed confidence in achieving a step-up in profitability as benefits from cost savings and network optimization flow through to the P&L. According to the earnings call transcript, the company has closed four manufacturing plants to streamline operations, though this was not explicitly mentioned in the presentation slides.

The company’s full-year outlook remains unchanged:

Smith & Nephew’s stock saw a modest increase of 0.23% following the presentation, reflecting steady investor confidence in the company’s strategic direction and innovation focus. The company’s ability to maintain guidance despite various headwinds suggests management’s confidence in the underlying business momentum for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.