Canopy Growth stock tumbles after announcing $200 million share sale plan

Introduction & Market Context

Solvay SA (EURONEXT:EBR:SOLB) presented its second quarter 2025 results on July 30, revealing continued pressure on sales and margins that prompted a downward revision to its full-year outlook. The specialty chemicals company, led by CEO Philippe Kehren and CFO Alexandre Blum, reported declining organic sales amid challenging market conditions, particularly in its Basic Chemicals segment.

The results come as Solvay continues to implement its structural cost savings program, which has delivered €55 million in the first half of 2025, though these savings have not fully offset pricing and volume pressures in key markets.

Executive Summary

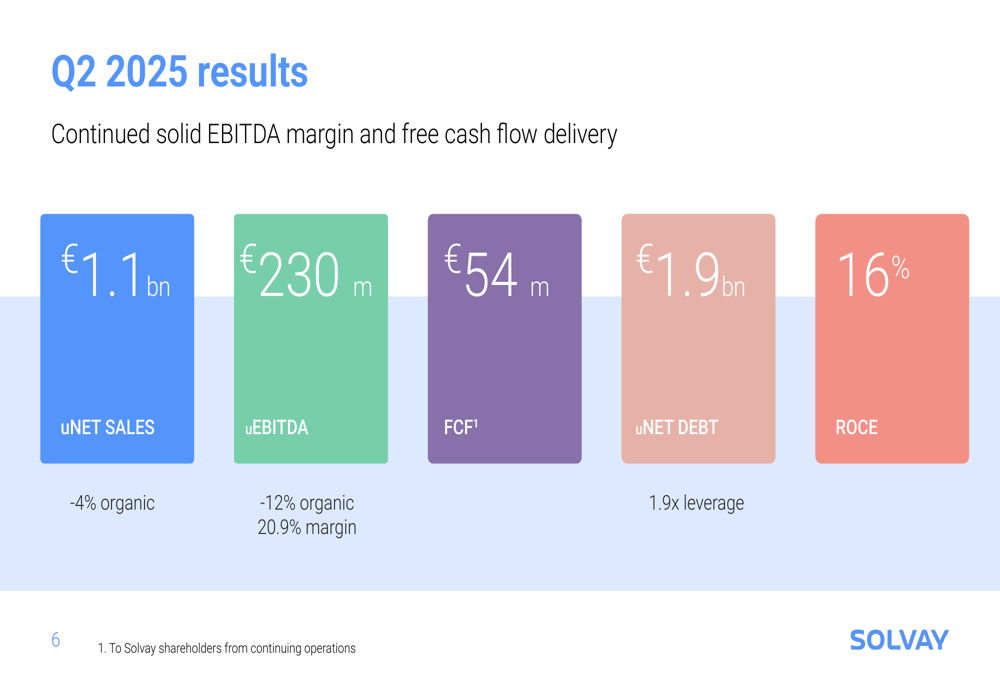

Solvay reported second quarter net sales of €1.1 billion, representing a 4% organic decline year-over-year. Underlying EBITDA fell more significantly by 12% organically to €230 million, with margins compressing from 22.8% in Q2 2024 to 20.9% in Q2 2025. The company generated €54 million in free cash flow during the quarter, while net debt increased to €1.9 billion, representing a leverage ratio of 1.9x.

As shown in the following overview of key financial metrics:

This performance represents a continuation of the challenging trends seen in Q1 2025, when the company reported a 6% year-over-year decline in underlying net sales while maintaining a 22% EBITDA margin. The further deterioration in Q2 has led management to revise its full-year guidance.

Quarterly Performance Highlights

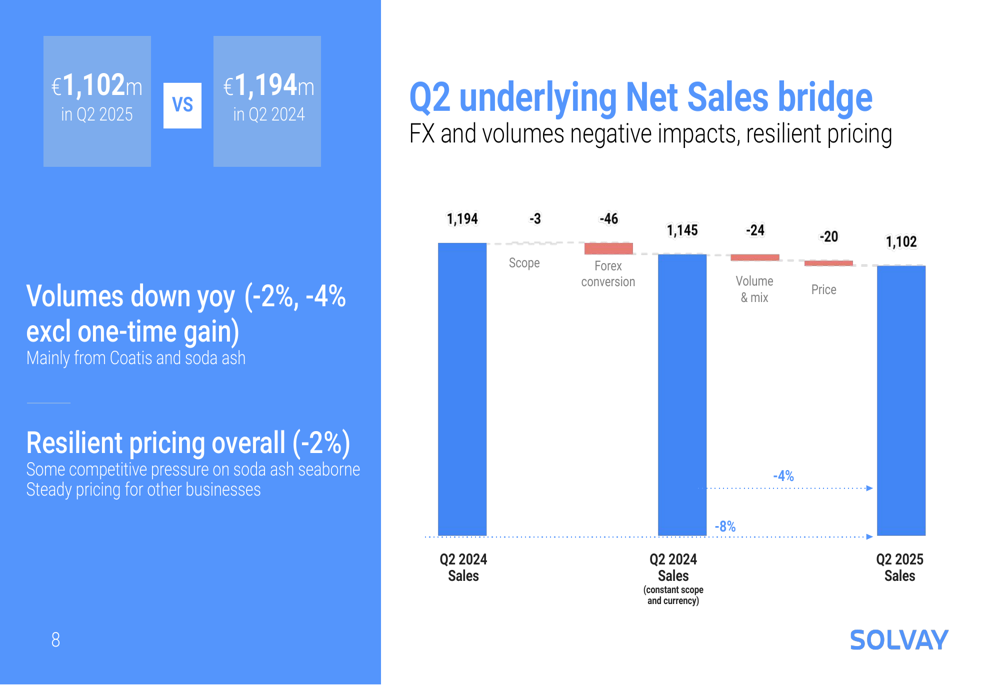

The sales decline was driven by both volume and pricing pressures. Volumes decreased by 2% year-over-year (4% excluding one-time gains), primarily due to weakness in Coatis and soda ash markets. Pricing also declined by 2%, though the company characterized overall pricing as "resilient."

The following bridge chart illustrates the factors contributing to the sales decline from Q2 2024 to Q2 2025:

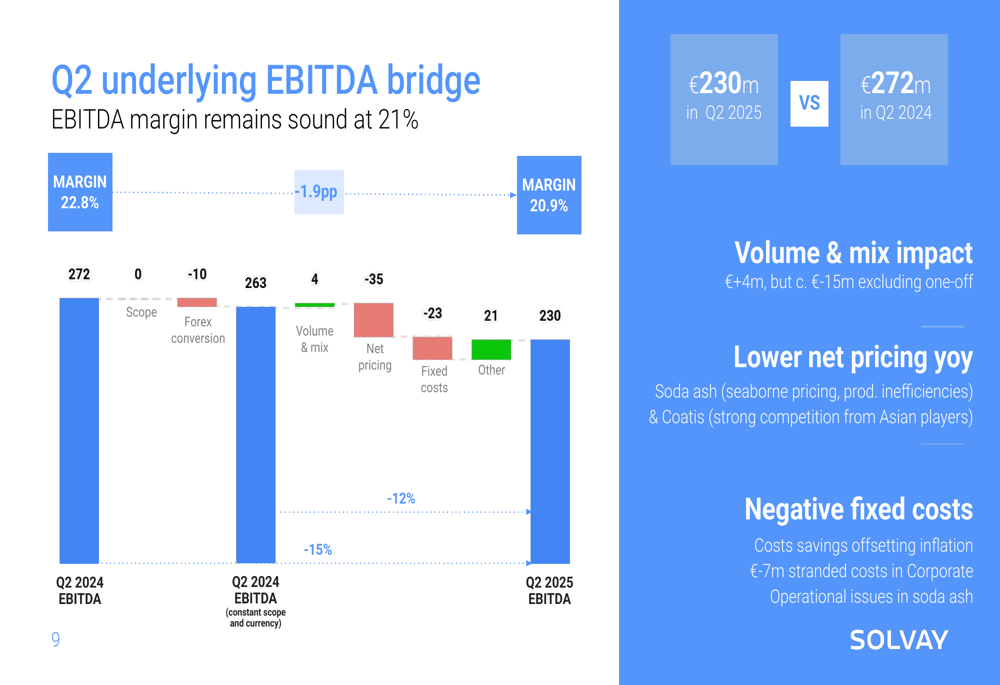

EBITDA performance was more severely impacted, with a 12% organic decline. The primary factors were negative net pricing (-€35 million) and increased fixed costs (-€23 million), which were only partially offset by positive volume/mix effects (+€4 million) and other factors (+€21 million).

The EBITDA bridge below shows these impacts:

Segment Performance

Solvay’s two main business segments showed divergent performance during the quarter. The Basic Chemicals segment, which includes Soda Ash & Derivatives and Peroxides, reported a 6% decline in net sales to €667 million and a more substantial 27% drop in EBITDA to €141 million. This segment’s margin compressed to 21.2%, reflecting significant pricing and cost pressures.

The Performance Chemicals segment, comprising Silica, Coatis, and Special Chem, saw a 10% decline in net sales to €434 million. However, EBITDA for this segment increased by 2% to €104 million, with margins expanding to 23.9%. The Special Chem business was a particular bright spot, with 6% organic sales growth.

Strategic Initiatives

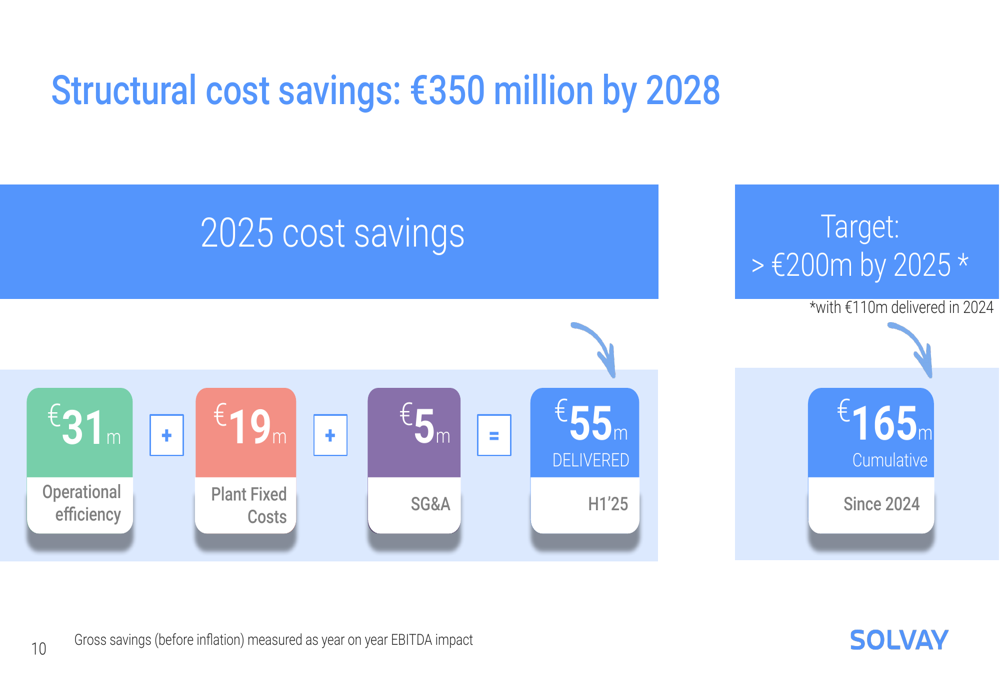

Solvay continues to implement its structural cost savings program, targeting €350 million in savings by 2028. In the first half of 2025, the company delivered €55 million in savings, broken down as €31 million from operational efficiency, €19 million from plant fixed costs, and €5 million from SG&A reductions.

The following chart illustrates the progress on cost savings initiatives:

Cumulatively, Solvay has achieved €165 million in cost savings since 2024, with €110 million delivered in 2024 and €55 million in H1 2025. The company remains on track to deliver more than €200 million in savings by the end of 2025.

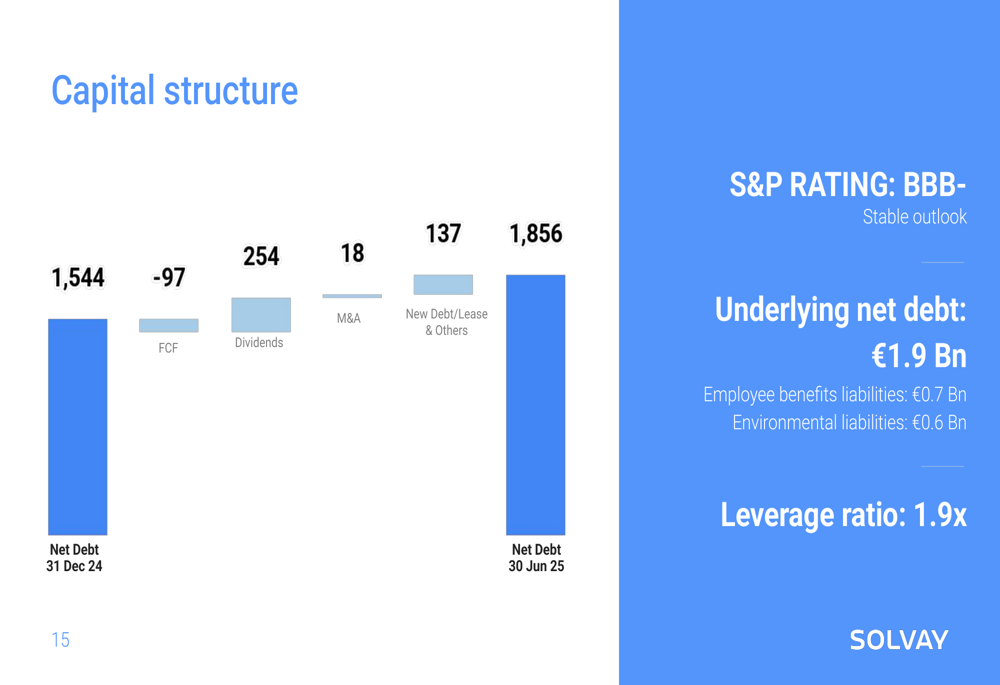

Capital Structure and Cash Flow

Solvay’s net debt increased from €1,544 million at the end of December 2024 to €1,856 million as of June 30, 2025. This increase was primarily driven by dividend payments (€254 million) and other factors, partially offset by free cash flow generation.

The company’s capital structure evolution is illustrated below:

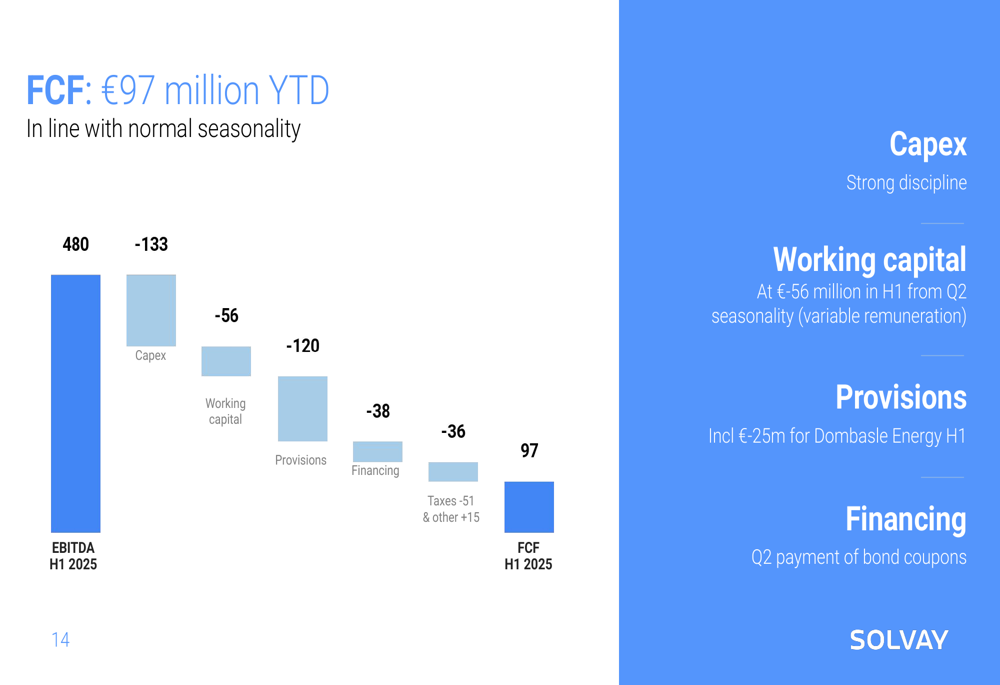

Free cash flow for the first half of 2025 totaled €97 million, with EBITDA of €480 million partially offset by capital expenditures (-€133 million), working capital changes (-€56 million), provisions (-€120 million), financing costs (-€38 million), and taxes and other items (-€36 million).

The free cash flow breakdown is shown here:

Forward-Looking Statements

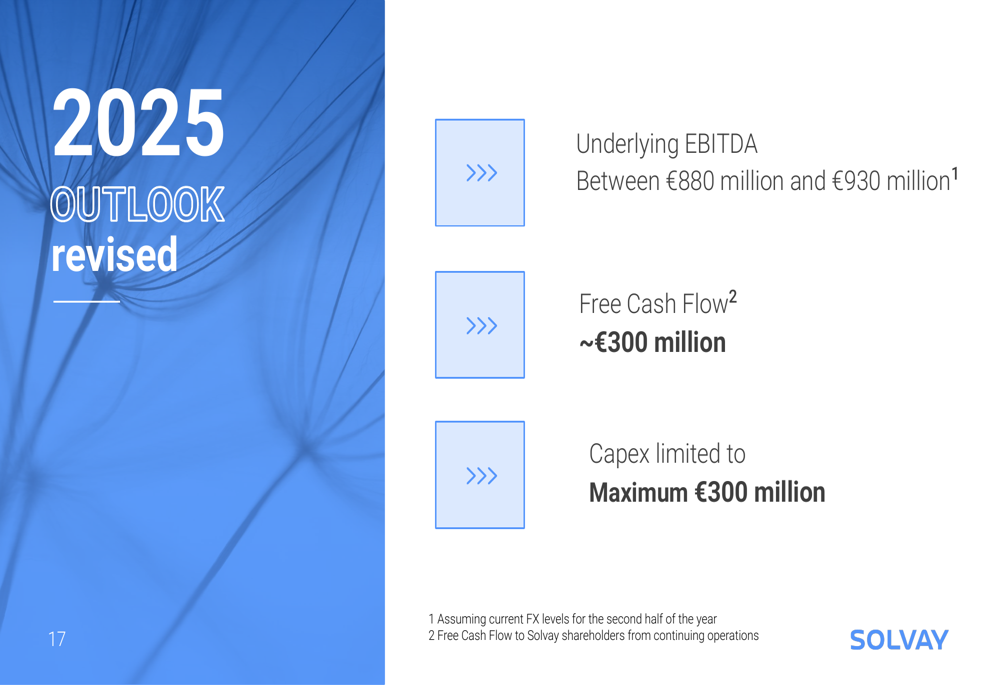

In light of the challenging first half performance, Solvay has revised its full-year 2025 outlook downward. The company now expects:

- Underlying EBITDA between €880 million and €930 million (previously in the lower half of €1,000-1,100 million)

- Free cash flow of approximately €300 million

- Capital expenditures capped at €300 million

The revised outlook is presented in the following slide:

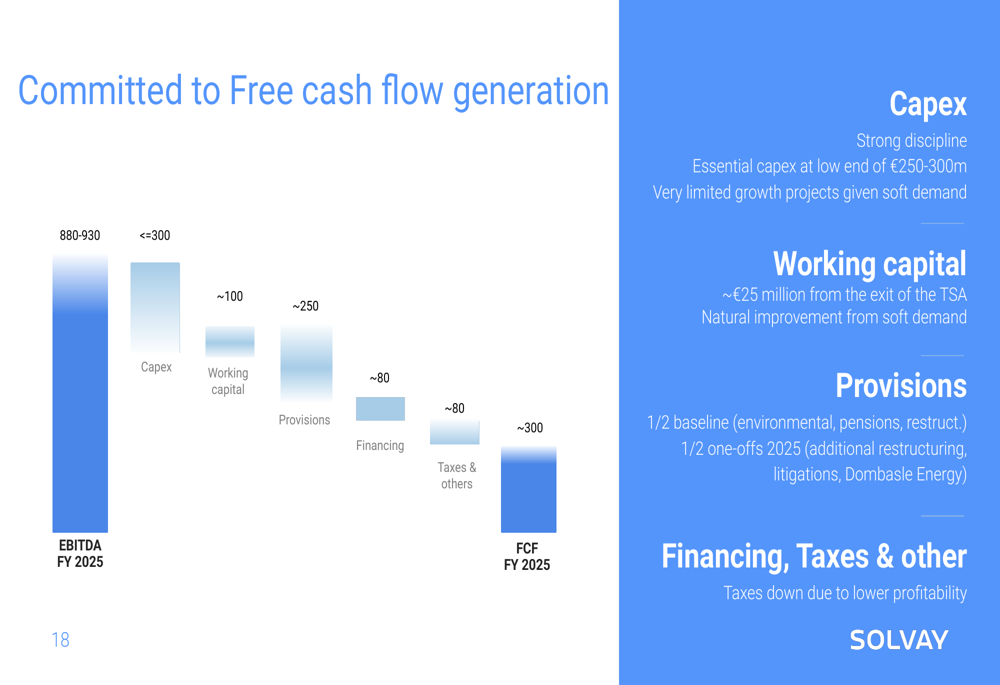

Despite the downward revision, Solvay remains committed to free cash flow generation, with a detailed breakdown of expected cash flow components for the full year 2025:

The company maintains its BBB- stable credit rating from S&P, though its leverage ratio has increased to 1.9x from 1.7x in the previous quarter. Management emphasized its focus on cost control and operational efficiency to navigate the challenging market environment and deliver on its revised commitments for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.