Oil prices steady near 1-mth high on US-Iran sanctions; OPEC+ meeting awaited

South Plains Financial Inc (NASDAQ:SPFI) reported strong second-quarter 2025 results in its earnings presentation on July 16, with net income rising to $14.6 million and diluted earnings per share increasing 19% quarter-over-quarter to $0.86, significantly exceeding the $0.72 reported in Q1 2025.

The bank’s stock jumped 3.14% in after-hours trading following the announcement, reaching $37.78.

Quarterly Performance Highlights

South Plains Financial delivered substantial improvement in its key performance metrics during the second quarter. Net interest margin (NIM) expanded to 4.07%, up from 3.81% in the previous quarter. Even excluding a $1.7 million one-time interest recovery from a previously nonaccrual loan, the NIM still improved to 3.90%.

Net interest income increased to $42.5 million, up from $38.5 million in Q1 2025, while noninterest income rose to $12.2 million from $10.6 million, primarily due to a $1.5 million increase in mortgage banking revenues.

As shown in the following chart detailing the company’s quarterly performance metrics:

The efficiency ratio improved significantly to 61.1% from 66.9% in the previous quarter, reflecting better operational efficiency despite a $513,000 increase in noninterest expenses. Tangible book value per share grew to $26.70, up from $26.05 at the end of Q1 2025.

Loan and Deposit Analysis

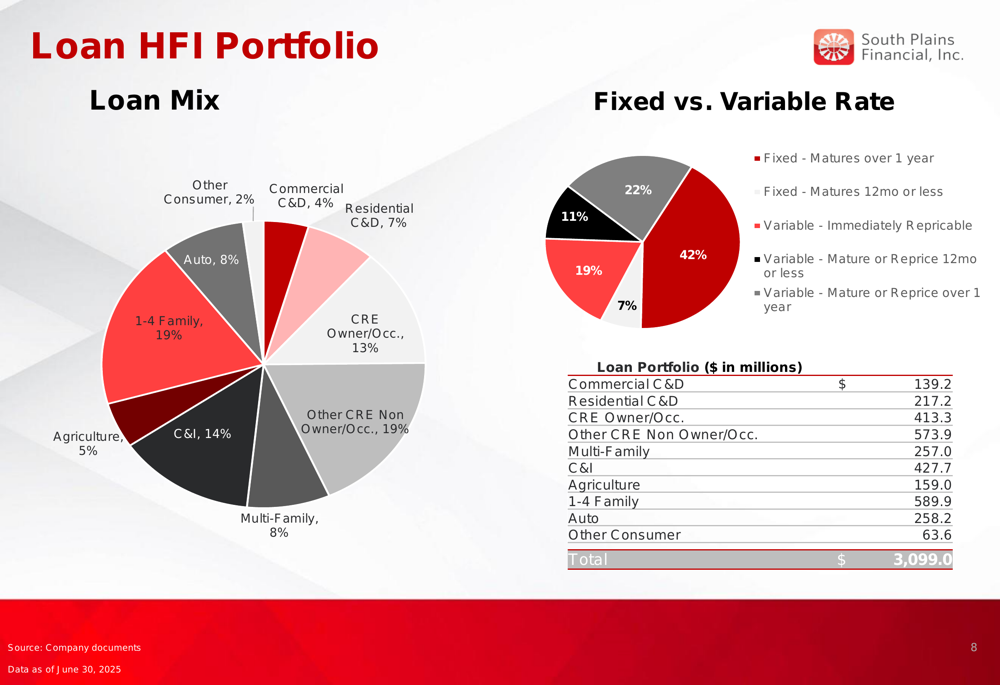

South Plains Financial reported modest loan growth, with loans held for investment (HFI) increasing by $23.1 million to $3.10 billion. The average yield on loans improved to 6.99% from 6.67% in Q1 2025, or 6.76% excluding the one-time interest recovery.

The following chart illustrates the company’s loan portfolio growth trend:

The bank maintains a diversified loan portfolio, with significant concentrations in 1-4 family residential (19%), other CRE non-owner occupied (19%), and commercial and industrial loans (14%). The portfolio is balanced between fixed and variable rate loans, with 42% in immediately repriceable variable rate loans.

The loan mix breakdown is detailed in this chart:

Total (EPA:TTEF) deposits decreased slightly to $3.74 billion from $3.79 billion at the end of Q1 2025, primarily due to a $73.7 million seasonal decrease in public fund deposits, partially offset by organic growth in retail and commercial deposits. Positively, the cost of deposits decreased by 5 basis points to 2.14%, and noninterest-bearing deposits increased to 26.7% of total deposits, up from 25.5% in the previous quarter.

The deposit trends and composition are illustrated in the following chart:

Credit Quality and Risk Management

While overall performance improved, South Plains Financial reported some credit quality concerns. The provision for credit losses increased substantially to $2.5 million in Q2 2025, compared to $420,000 in Q1 2025. This increase was attributed to specific reserves, net charge-off activity, increased loan balances, and several credit quality downgrades.

Classified loans increased by $24.3 million during the quarter, primarily due to the downgrade of a $32 million multi-family property loan, partially offset by the full collection of a $19 million credit.

The following chart shows the company’s credit quality metrics:

The non-owner occupied (NOO) commercial real estate portfolio, which represents 38.3% of total loans HFI (down from 40.0% at the end of Q1), includes $138.4 million in office loans with a weighted average loan-to-value ratio of 58%. The company noted that NOO CRE loans past due 90+ days or nonaccrual represented only 4 basis points of the portfolio.

Net Interest Income and Margin Expansion

South Plains Financial’s net interest income and margin showed significant improvement in Q2 2025. The expansion in NIM to 4.07% (or 3.90% excluding the one-time interest recovery) represents a substantial improvement from the 3.81% reported in Q1 2025.

This positive trend is illustrated in the following chart:

The improvement in NIM was driven by higher loan yields and lower deposit costs, demonstrating the bank’s effective balance sheet management in the current interest rate environment.

Market Position and Strategic Focus

South Plains Financial continues to operate in key Texas markets including Dallas/Fort Worth, El Paso, Houston, and Lubbock. The company’s major metropolitan market loan portfolio represents 32.7% of total loans HFI, though it decreased by $26 million during the quarter due to $49.1 million in early loan payoffs related to three multi-family property loans.

The bank maintains a strong capital position with ample liquidity, including $1.95 billion of available borrowing capacity through the Federal Home Loan Bank of Dallas and the Federal Reserve Bank of Dallas, with no borrowings utilized during Q2 2025.

South Plains Financial emphasized its relationship-based business model, stating its core purpose as "To use the power of relationships to help people succeed and live better." This approach appears to be supporting the bank’s continued growth and profitability improvement despite some credit quality challenges.

With the significant improvement in profitability metrics and continued focus on relationship banking, South Plains Financial appears well-positioned to navigate the current economic environment, though investors should monitor the increase in classified loans and provision for credit losses in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.