TSX runs higher on rate cut expectations

Introduction & Market Context

SouthState Corporation (NYSE:SSB) presented its second quarter 2025 earnings results on July 25, 2025, revealing strong financial performance across key metrics. The regional bank, which ranks as the fifth largest in the South with $66 billion in assets, reported significant improvements in profitability, margin expansion, and balance sheet growth compared to both the previous quarter and year-over-year results.

The company’s stock closed at $97.22 on July 24, down 1.23% in regular trading, but rebounded 2% to $99.16 in pre-market trading on July 25 following the earnings release, suggesting positive market reception to the results.

Quarterly Performance Highlights

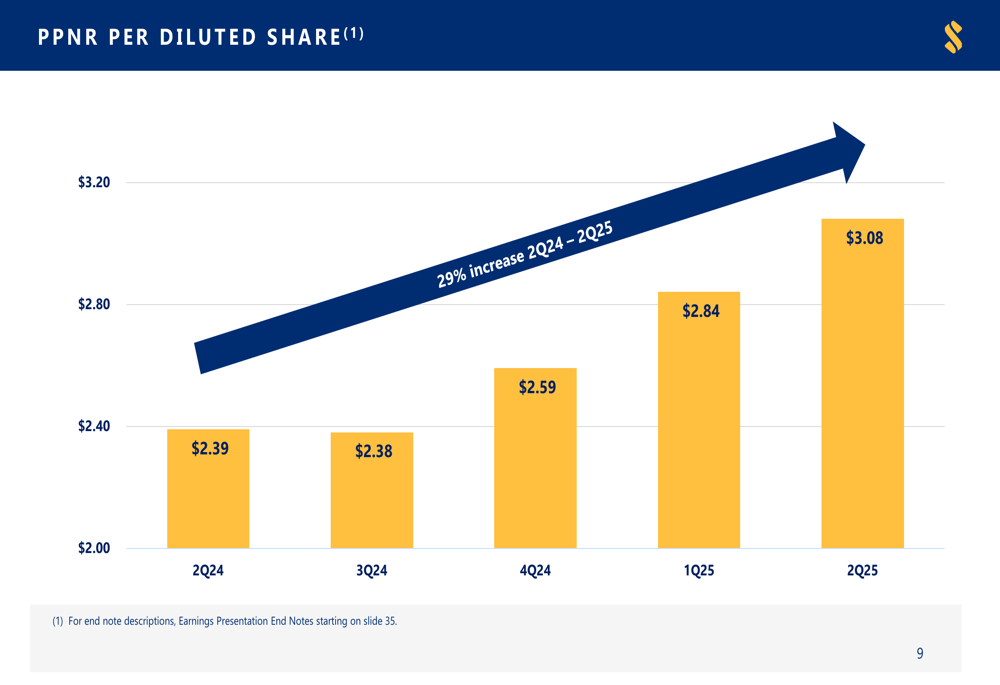

SouthState reported GAAP earnings per share of $2.11 for Q2 2025, with adjusted (non-GAAP) EPS of $2.30, continuing its trend of strong performance following Q1’s adjusted EPS of $2.15. Pre-provision net revenue (PPNR) reached $314.1 million, representing a substantial 29% year-over-year growth on a per-share basis.

As shown in the following chart of PPNR per diluted share, the company has demonstrated consistent growth over five consecutive quarters:

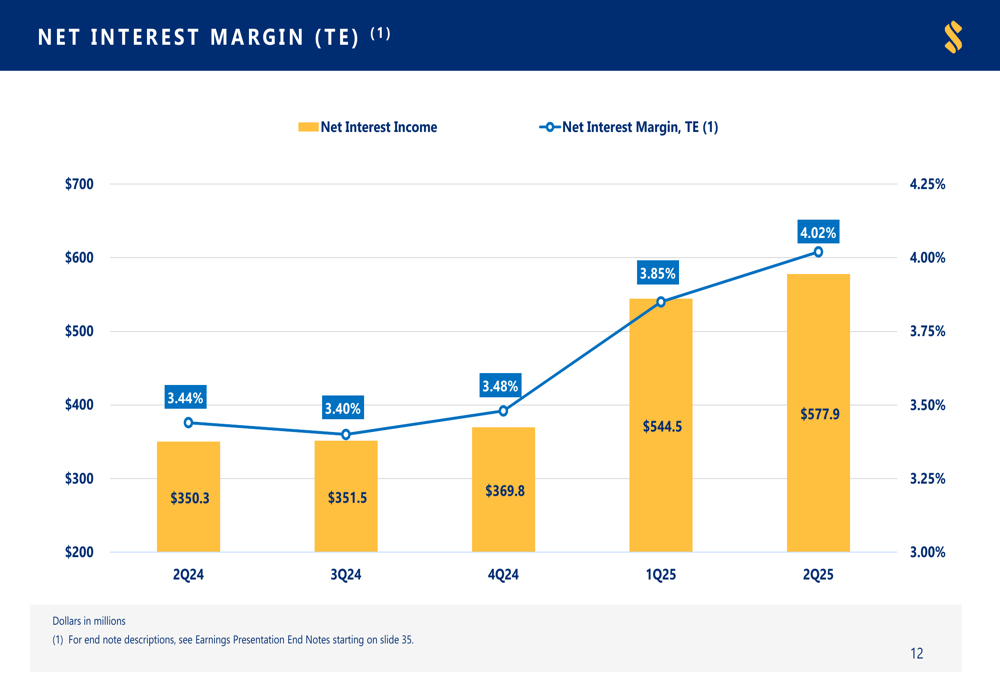

The bank’s net interest margin (NIM) expanded significantly to 4.02% in Q2 2025, up 18 basis points from 3.85% in Q1 2025. This improvement was driven by higher loan yields, securities restructuring, and lower deposit costs. Total (EPA:TTEF) loan yield increased to 6.33% (up 8 basis points quarter-over-quarter), while deposit costs decreased to 1.84% (down 5 basis points).

The following chart illustrates the steady improvement in net interest income and margin over the past five quarters:

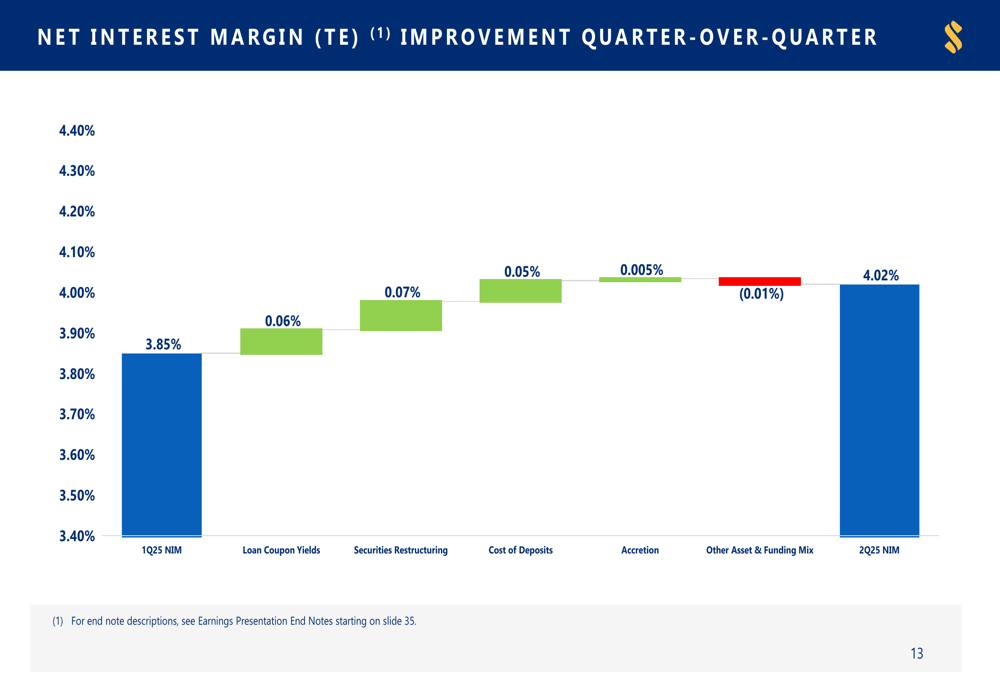

The company provided a detailed breakdown of the factors contributing to NIM expansion, with loan coupon yields contributing 6 basis points, securities restructuring adding 7 basis points, and lower deposit costs adding 5 basis points:

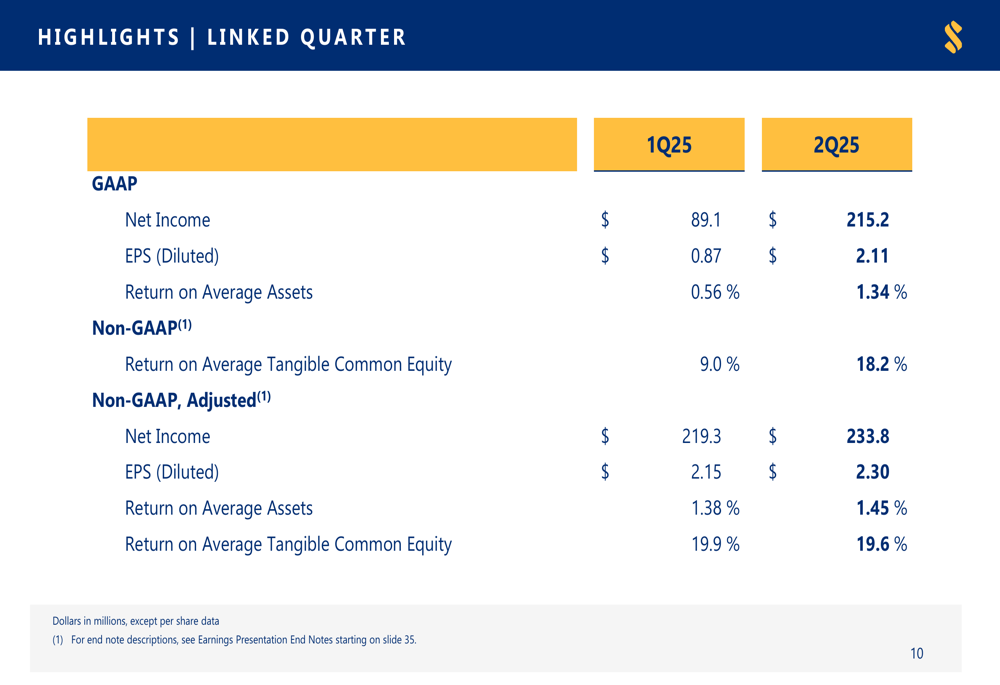

A comparison of key financial metrics between Q1 and Q2 2025 shows substantial improvement across the board:

Strategic Positioning in Growth Markets

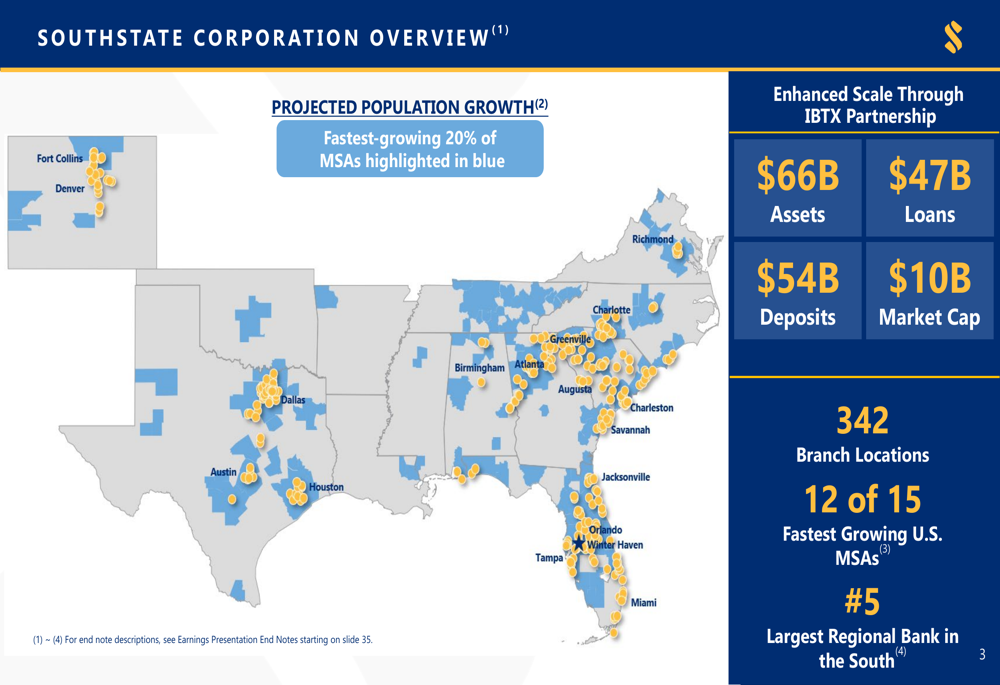

SouthState’s strategic focus on high-growth markets in the Southern United States continues to be a key driver of its performance. The bank operates 342 branches across some of the fastest-growing metropolitan statistical areas (MSAs) in the country, with particularly strong presence in Florida, Texas, and the Carolinas.

The following map illustrates SouthState’s geographic footprint and scale following its merger with Independent Bank (NASDAQ:INDB) Group (NASDAQ:IBTX):

The company highlighted how its presence in high-growth markets positions it for continued success, with employment growth in its key markets significantly outpacing national averages. Austin, Orlando, Dallas, Charlotte, and other Southern cities where SouthState operates show employment growth ranging from 11.1% to 20.4% since February 2020.

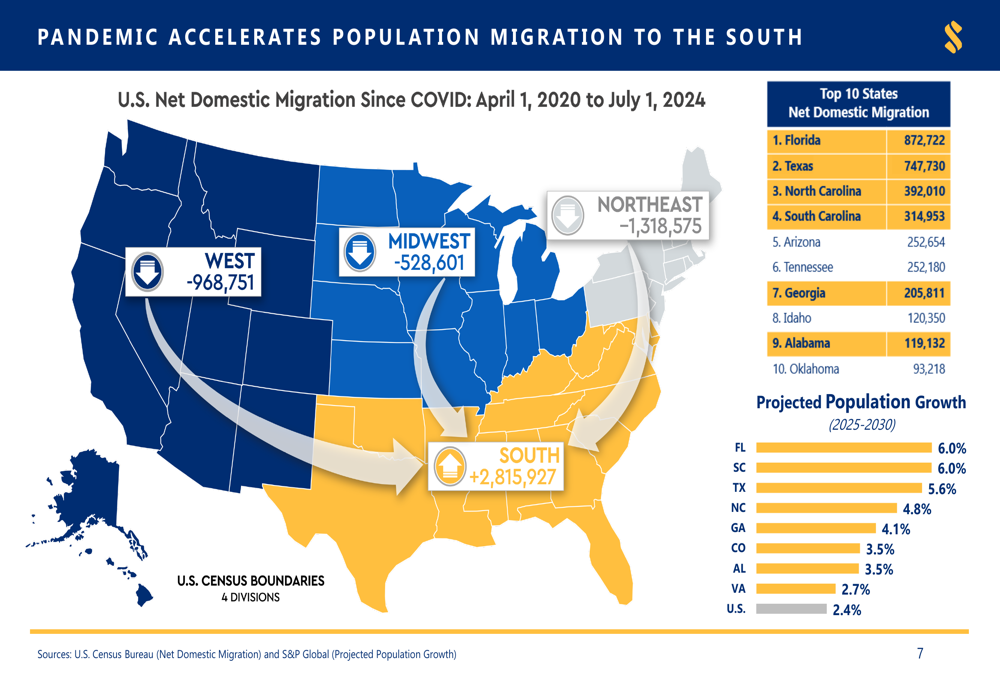

This strategic positioning is further supported by demographic trends showing significant population migration to the South from other regions of the country. Since April 2020, the South has gained over 2.8 million residents through domestic migration, while the Northeast, Midwest, and West have all experienced net population losses.

Balance Sheet and Credit Quality

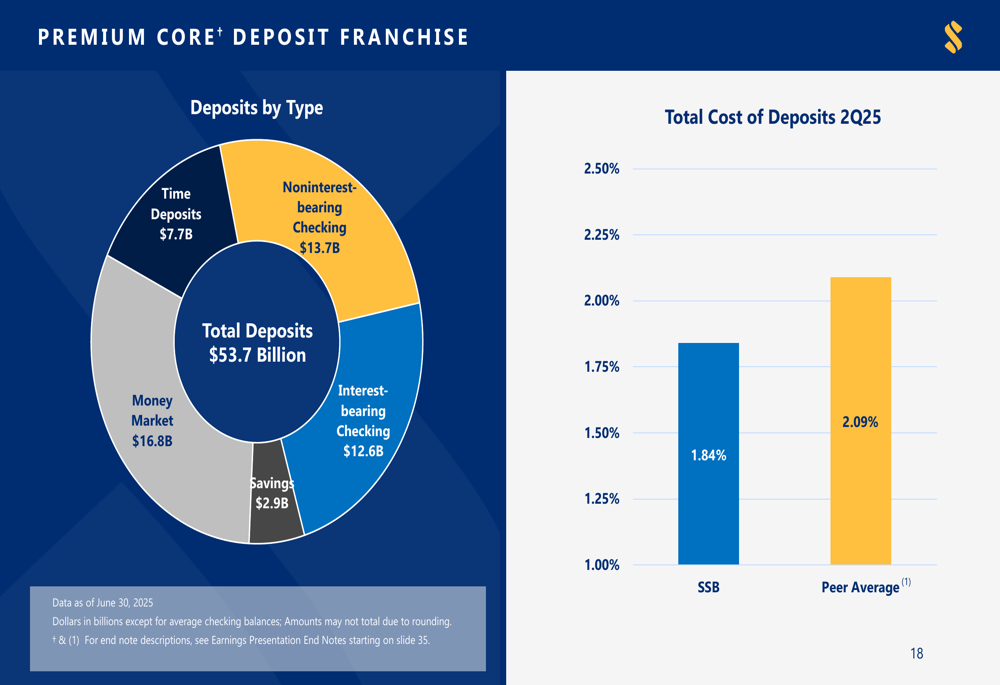

SouthState reported solid balance sheet growth in Q2 2025, with loans increasing by $501 million (4% annualized) and deposits growing by $359 million (3% annualized). Total loans reached $47.3 billion, while deposits stood at $53.7 billion.

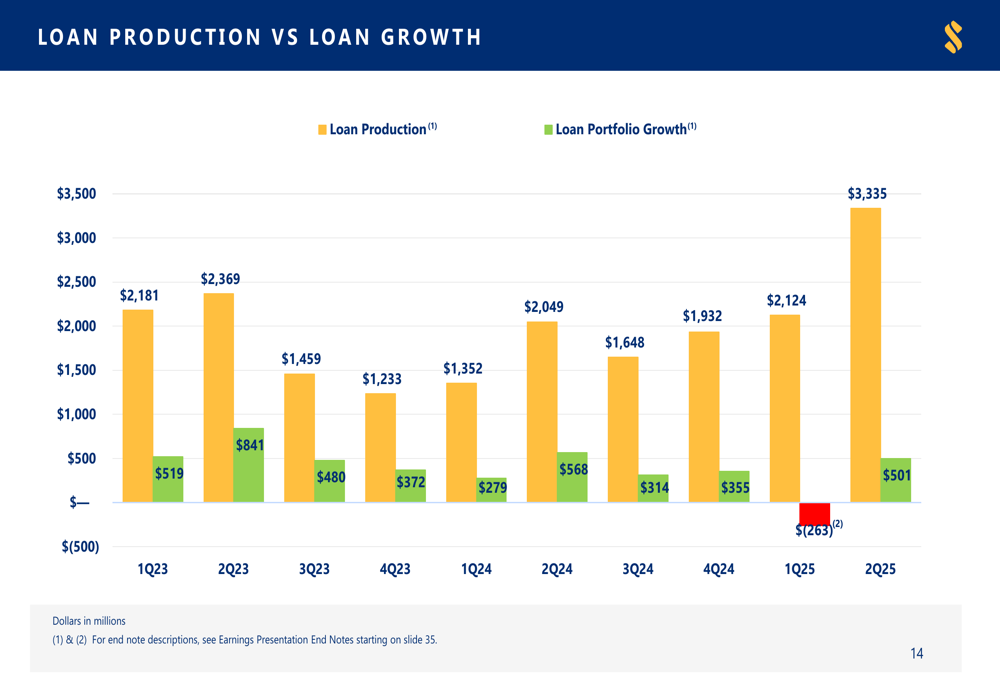

Loan production surged to $3.3 billion in Q2 2025, significantly higher than the $2.1 billion in Q1 2025 and the highest level in recent quarters:

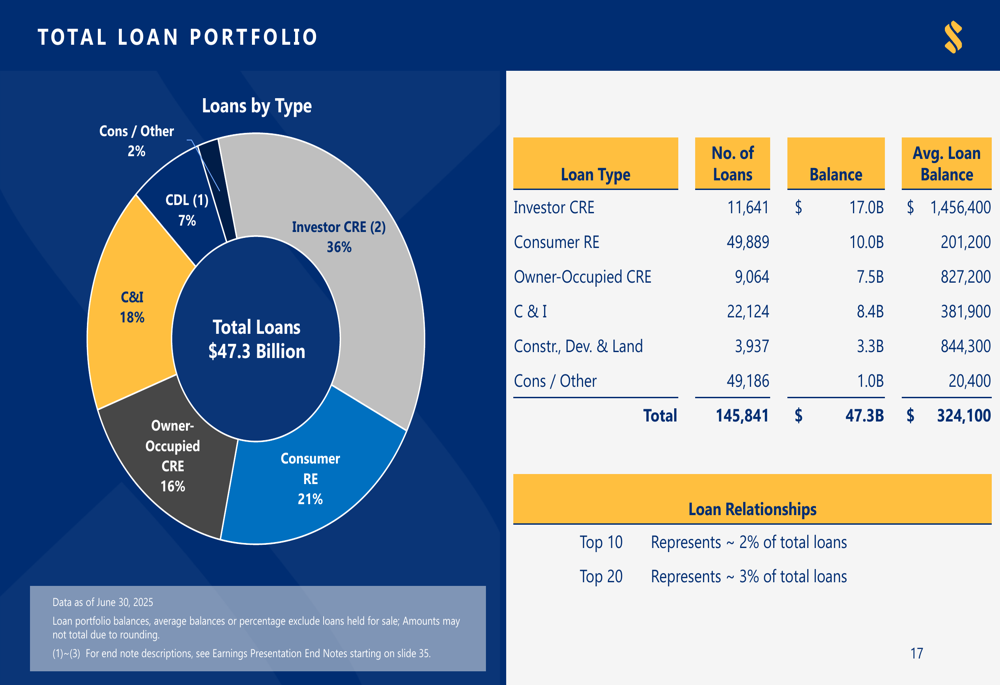

The loan portfolio remains well-diversified, with investor commercial real estate (CRE) representing 36%, consumer real estate at 21%, commercial and industrial (C&I) loans at 18%, and owner-occupied CRE at 16%:

On the funding side, SouthState maintains a premium deposit franchise with costs below peer averages. The deposit base is diversified across various categories, with money market accounts representing the largest portion at $16.8 billion, followed by noninterest-bearing checking at $13.7 billion:

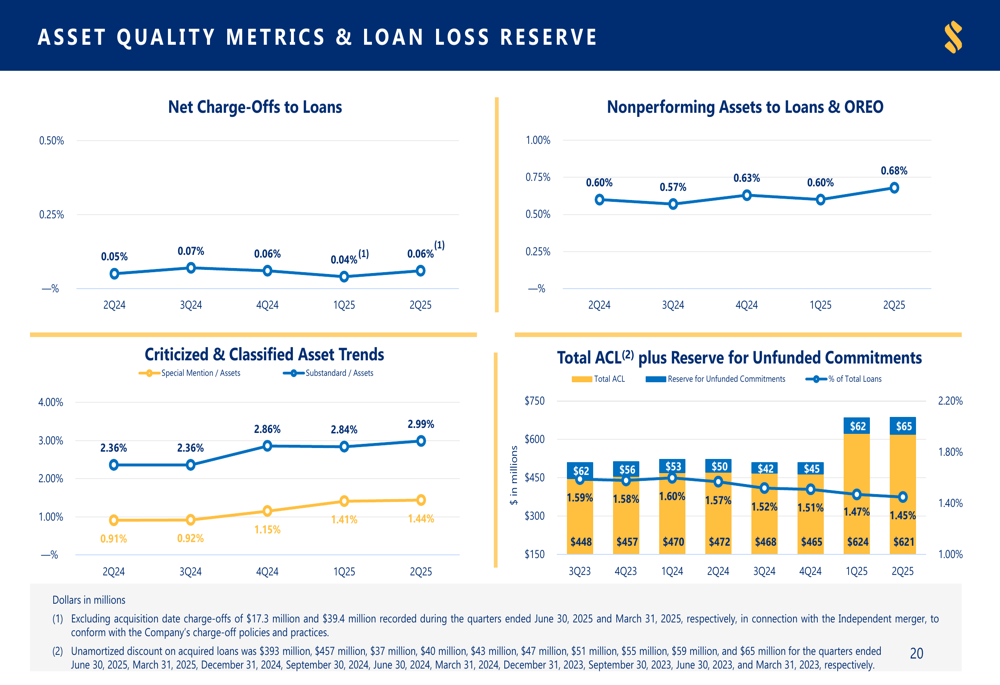

Credit quality metrics remain strong, with nonperforming assets to loans and OREO at 0.66% and net charge-offs to loans at 0.06%. The allowance for credit losses plus reserve for unfunded commitments stands at $624 million, providing solid coverage for potential credit issues:

Capital Position and Outlook

SouthState strengthened its capital position in Q2 2025, with improvements across all key capital ratios. The tangible common equity ratio increased to 8.5% from 8.2% in Q1, while the total risk-based capital ratio rose to 14.5% from 13.7%. The company also completed the issuance of $350 million in 7% fixed-to-floating rate subordinated notes during the quarter, further enhancing its capital structure.

The company’s history of resilient credit performance positions it well for future economic cycles, with net charge-offs consistently below peer averages over the past decade.

Looking ahead, SouthState appears well-positioned to continue its strong performance, leveraging its presence in high-growth markets, expanding net interest margin, and solid capital position. The integration with Independent Bank Group, which was completed in Q1 2025, has enhanced the bank’s scale and geographic footprint, providing additional opportunities for growth and operational efficiencies.

The Q2 2025 results demonstrate SouthState’s ability to execute on its strategic priorities while maintaining strong financial discipline, as evidenced by the consistent improvement in profitability metrics and the strengthening of its balance sheet.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.