Morgan Stanley again adjusts its Fed forecast, now sees 4 cuts in 2026

Introduction & Market Context

SPIE SA (EPA:SPIE), a leading European provider of multi-technical services, presented its H1 2025 results on July 31, 2025, showing solid growth and margin expansion despite mixed regional performance. The company’s stock closed at €49.00 on July 30, 2025, near its 52-week high of €49.34, reflecting investor confidence in the company’s performance and outlook.

The results demonstrate SPIE’s continued execution of its growth strategy, with a particular focus on energy transition and digital transformation services. After reporting strong Q1 2025 results with 21.1% organic growth earlier this year, the company has maintained positive momentum through the first half, though with a notable deceleration in organic growth during Q2.

H1 2025 Performance Highlights

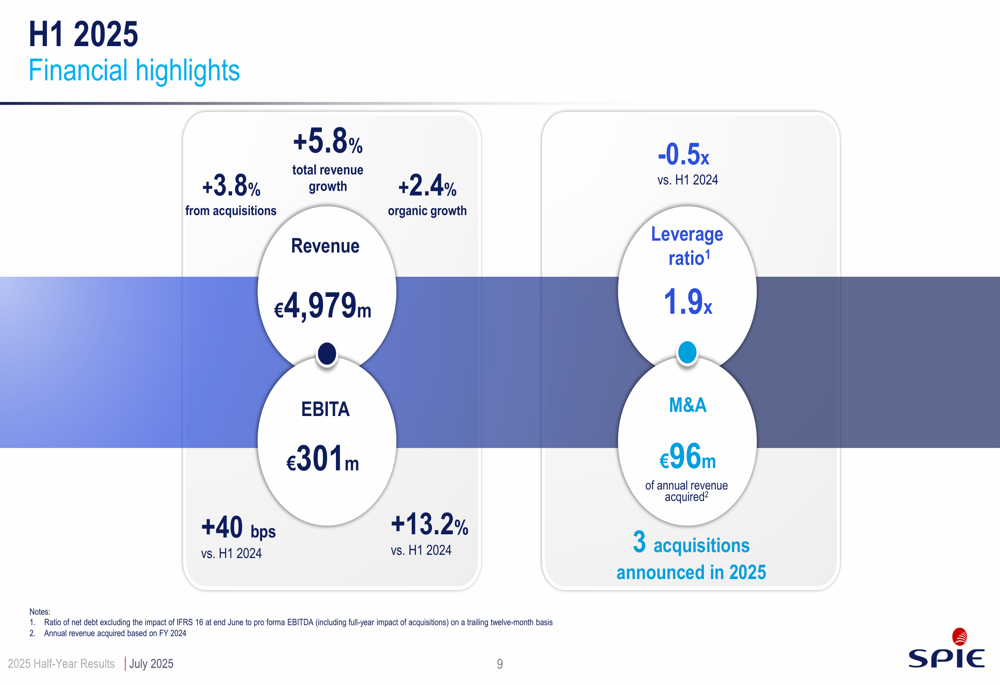

SPIE delivered solid financial results for the first half of 2025, with revenue reaching €4,979 million, representing a 5.8% increase compared to H1 2024. This growth was driven by a combination of organic growth (+2.4%) and acquisitions (+3.8%), partially offset by disposals (-0.3%).

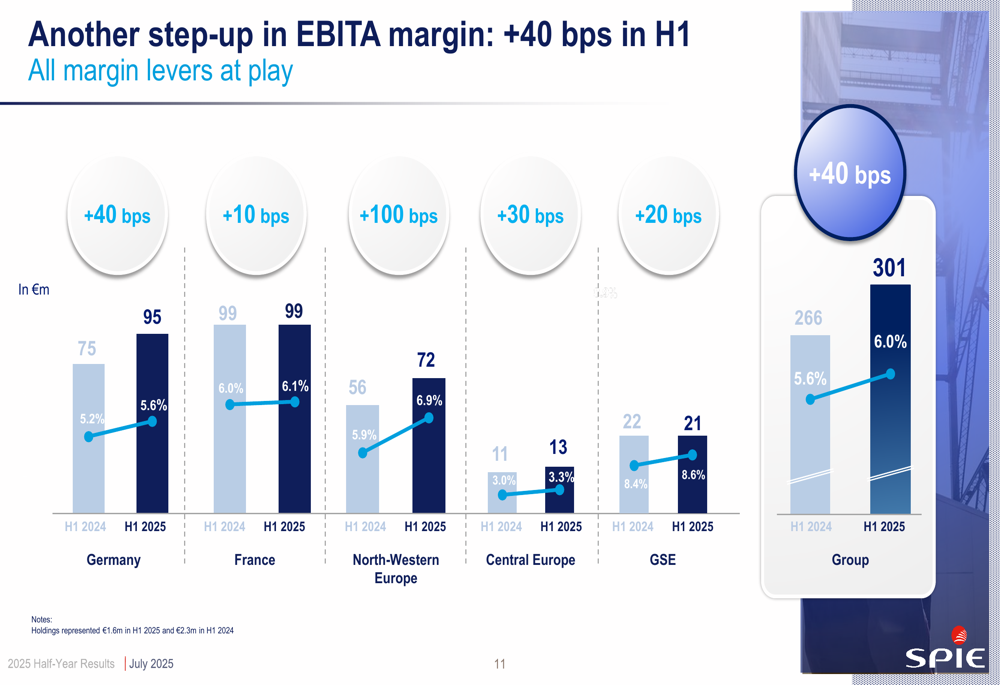

As shown in the following financial highlights chart, EBITA reached €301 million, up 13.2% compared to the previous year, while the EBITA margin expanded by 40 basis points to 6.0%:

The company’s adjusted net income (Group share) increased by 5.7% to €167 million. However, reported net income (Group share) was negative at -€13 million, primarily due to a significant fair value adjustment of the ORNANE convertible bond.

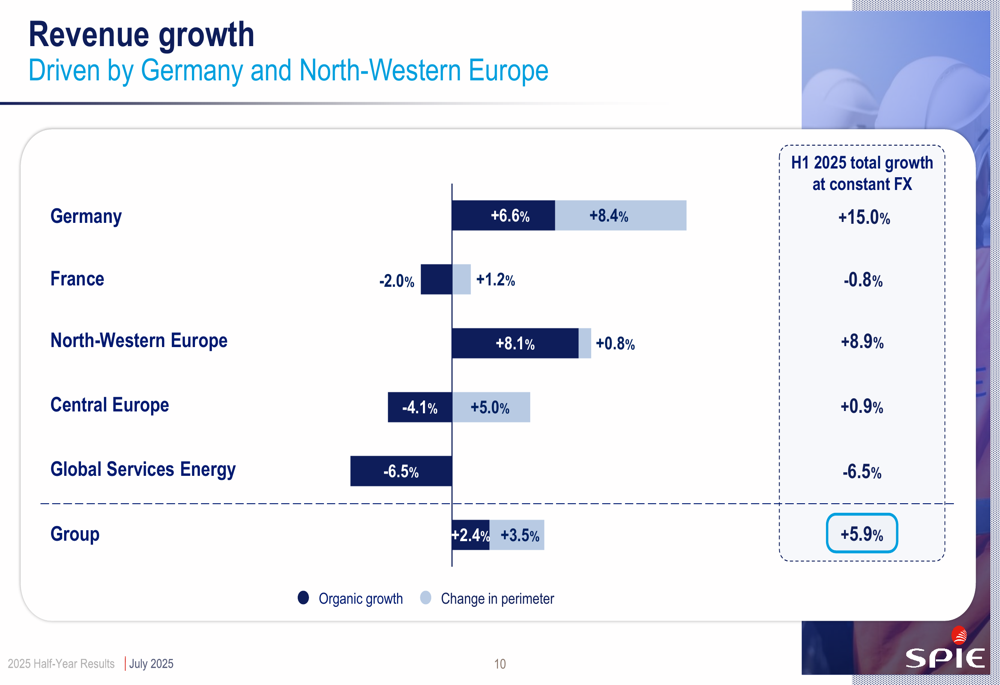

Regional performance varied significantly, with Germany and North-Western Europe showing strong growth, while France experienced a slight contraction and Global Services Energy declined. The following chart illustrates the revenue growth breakdown by region:

Regional Performance Analysis

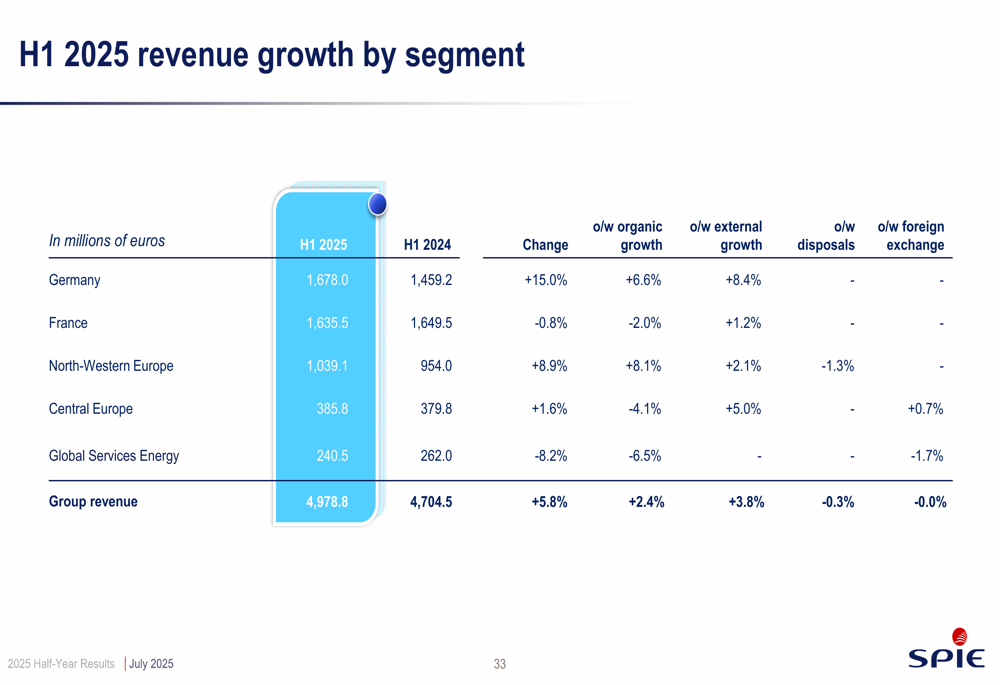

Germany has emerged as SPIE’s largest market, contributing 34% of H1 2025 revenue (€1,678 million), surpassing France for the first time. The German operations delivered impressive growth of 15.0% at constant exchange rates, including 6.6% organic growth and 8.4% from acquisitions.

As shown in the following EBITA margin breakdown, profitability improved across most regions, with particularly strong performance in North-Western Europe:

France, now representing 33% of group revenue (€1,635.5 million), experienced a slight revenue contraction of -0.8%, with -2.0% organic decline partially offset by +1.2% contribution from acquisitions. Despite this, the EBITA margin in France slightly improved to 6.1% from 6.0% in H1 2024.

North-Western Europe showed strong performance with 8.9% revenue growth (8.1% organic) and significant margin improvement, reaching 6.9% compared to 5.9% in H1 2024. Central Europe delivered modest 1.6% revenue growth but faced organic decline of -4.1%, while Global Services Energy experienced an 8.2% revenue decrease.

The detailed revenue growth by segment provides further insight into regional performance:

Financial Position and Cash Flow

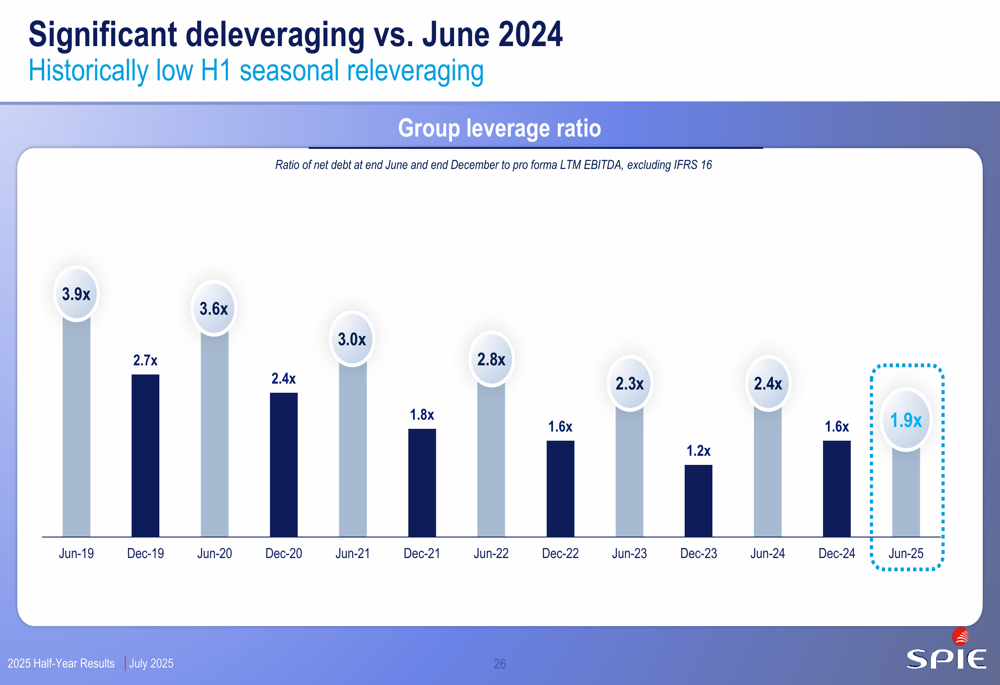

SPIE maintained a strong financial position, with continued deleveraging and improved working capital performance. The leverage ratio decreased to 1.9x (excluding IFRS 16 impact), down from 2.4x in June 2024, reflecting the company’s strong cash generation capabilities.

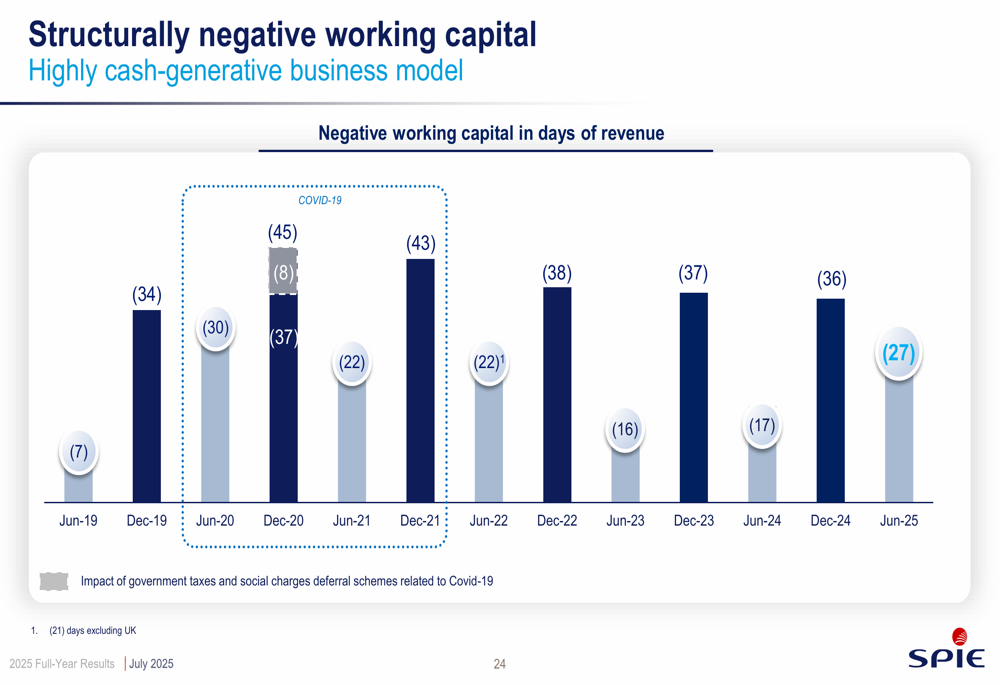

The following chart illustrates SPIE’s consistent improvement in working capital management, with negative working capital reaching -27 days of revenue in June 2025, compared to -17 days in June 2024:

This historical view of the company’s leverage ratio demonstrates SPIE’s commitment to maintaining a solid financial structure:

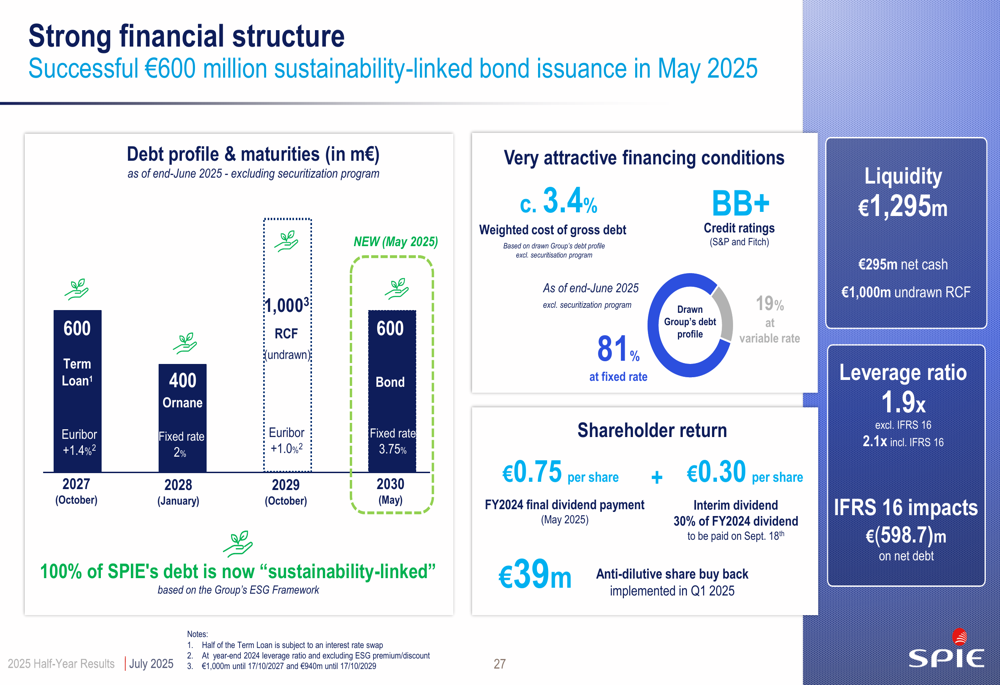

The company’s financial structure remains robust, with €1,295 million in liquidity (€295 million net cash and €1,000 million undrawn revolving credit facility). In May 2025, SPIE issued a €600 million sustainability-linked bond, further strengthening its financial position:

Strategic Initiatives and M&A Activity

SPIE continued its bolt-on M&A strategy in H1 2025, announcing three acquisitions representing approximately €96 million in annual revenue. These acquisitions strengthen the company’s position in key growth areas, including city networks and grids, building technology and automation, and ICT services.

The company highlighted several strategic projects in its presentation, including a new data center project in Frankfurt, Germany, where SPIE is delivering comprehensive technical services for a 16 MW facility designed to maximize energy efficiency. Other notable projects include a 500 kWh battery system installation at Volvo (OTC:VLVLY)’s headquarters in the Netherlands and ventilation system studies for France’s future EPR2 nuclear reactors.

2025 Outlook and Guidance

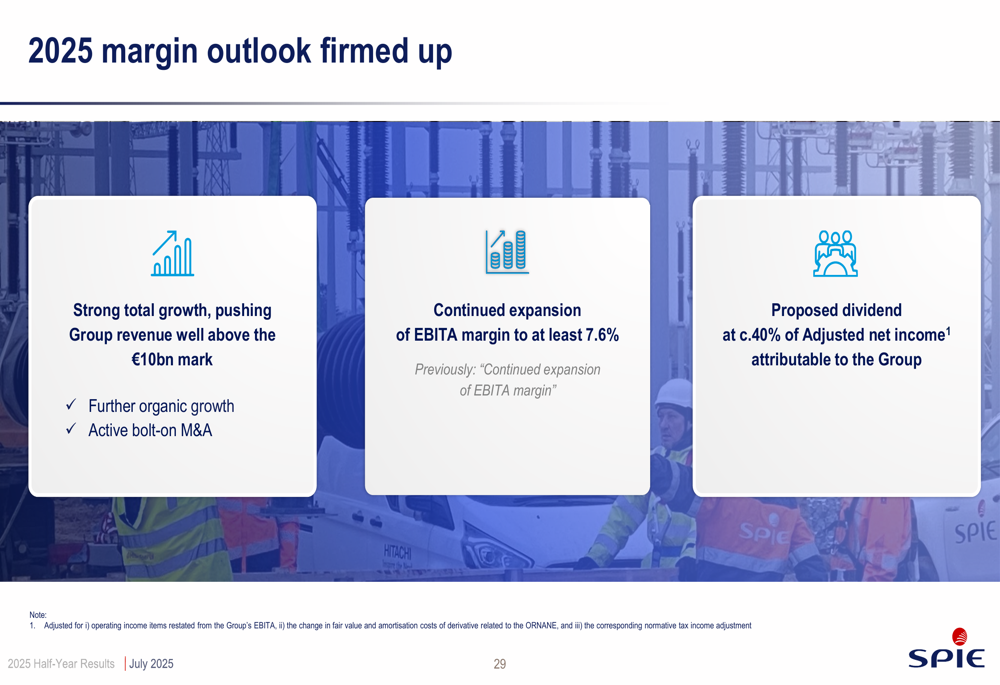

SPIE has firmed up its outlook for 2025, expecting strong total growth that will push group revenue well above the €10 billion mark. This growth will be driven by continued organic expansion and active bolt-on M&A activity.

The company also anticipates further expansion of its EBITA margin to at least 7.6% for the full year 2025, as illustrated in the following outlook slide:

This outlook aligns with statements made during the Q1 2025 earnings call, where CEO Gauthier Lwet noted, "It’s a good time to be a European Electrical Engineer," highlighting the favorable market conditions. The company maintains its dividend policy of distributing approximately 40% of adjusted net income attributable to the Group.

While SPIE’s H1 2025 organic growth of 2.4% represents a significant deceleration from the 21.1% reported in Q1, the company’s overall performance remains solid, with continued margin expansion and strong execution of its strategic initiatives. The company’s focus on energy transition and digital transformation positions it well to capitalize on long-term growth opportunities in the European market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.