Behind US stock gains, gold’s climb reflects growing market uncertainty: Macquarie

Introduction & Market Context

Spire Inc. (NYSE:SR) presented its third quarter fiscal 2025 results on August 5, showing a return to profitability and announcing a major acquisition that will expand its footprint in the natural gas utility sector. Despite beating analyst expectations with adjusted earnings of $0.01 per share versus the forecasted loss of $0.14, Spire’s stock dipped slightly by 0.65% to close at $75.91.

The company’s presentation highlighted its strategic expansion plans while maintaining its long-term growth targets amid a challenging utility market environment. The results mark a significant improvement from the $0.14 per share loss recorded in the same quarter last year, driven by stronger performance across all business segments.

Quarterly Performance Highlights

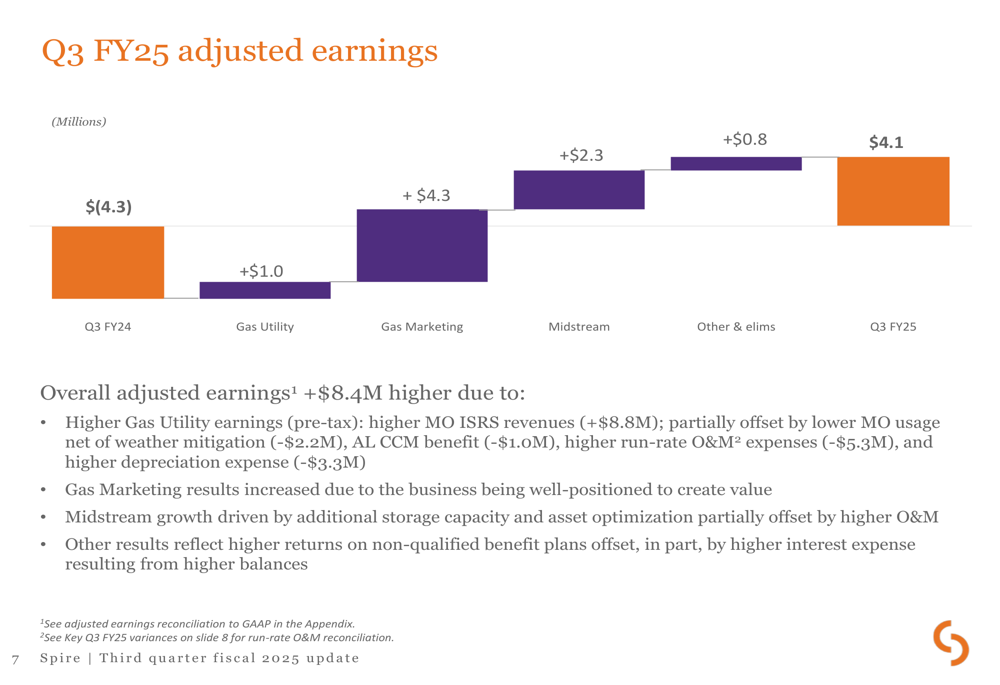

Spire reported adjusted earnings of $4.1 million ($0.01 per share) for Q3 FY25, compared to a loss of $4.3 million in Q3 FY24. This $8.4 million improvement was driven by gains across all business segments, with particularly strong performance in Gas Marketing and Midstream operations.

As shown in the following earnings breakdown chart:

The Gas Utility segment contributed an additional $1.0 million, primarily due to higher Missouri Infrastructure System Replacement Surcharge (ISRS) revenues of $8.8 million, partially offset by higher operating expenses. Gas Marketing showed the most significant improvement, adding $4.3 million as the business capitalized on market conditions. Midstream operations contributed an additional $2.3 million, driven by expanded storage capacity and asset optimization.

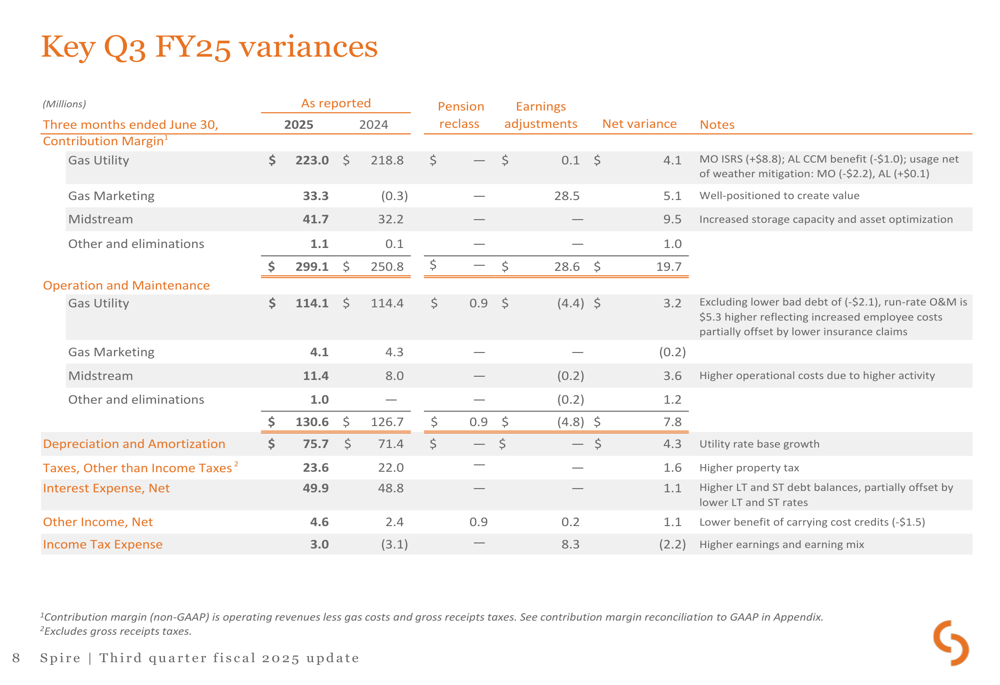

The detailed quarterly variances further illustrate the drivers behind Spire’s improved performance:

Total (EPA:TTEF) contribution margin increased by $19.7 million year-over-year to $299.1 million, with the Midstream segment showing the largest percentage gain. Operating expenses remained relatively stable in the Gas Utility segment but increased in Midstream operations to support growth initiatives.

Strategic Acquisition Details

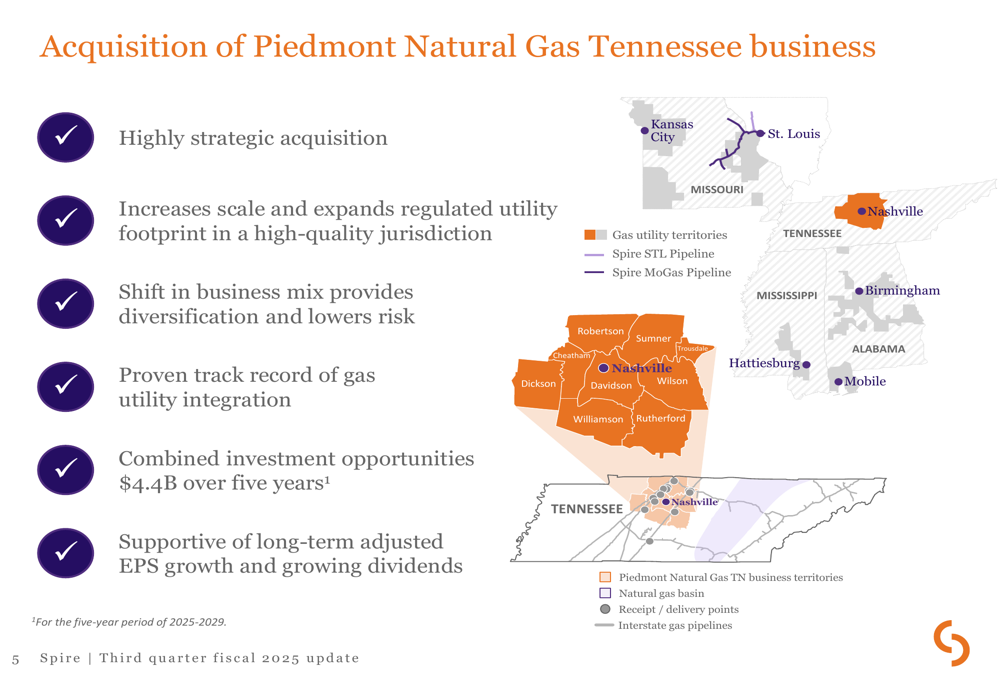

The most significant announcement in Spire’s presentation was the agreement to acquire Piedmont Natural Gas Tennessee business from Duke Energy (NYSE:DUK) for $2.48 billion. This acquisition represents a major strategic expansion for Spire, extending its regulated utility footprint into Tennessee.

The following map illustrates how this acquisition will expand Spire’s geographical presence:

The acquisition is described as "highly strategic" in Spire’s presentation, with several key benefits highlighted:

- Increased scale and expanded regulated utility footprint in a high-quality jurisdiction

- Diversification of business mix, which lowers overall risk profile

- Leveraging Spire’s proven track record of gas utility integration

- Combined investment opportunities of $4.4 billion over five years

- Support for long-term adjusted EPS growth and growing dividends

This move aligns with Spire’s strategy of focusing on regulated utility operations, which provide more stable and predictable returns compared to other energy segments.

Regulatory Developments

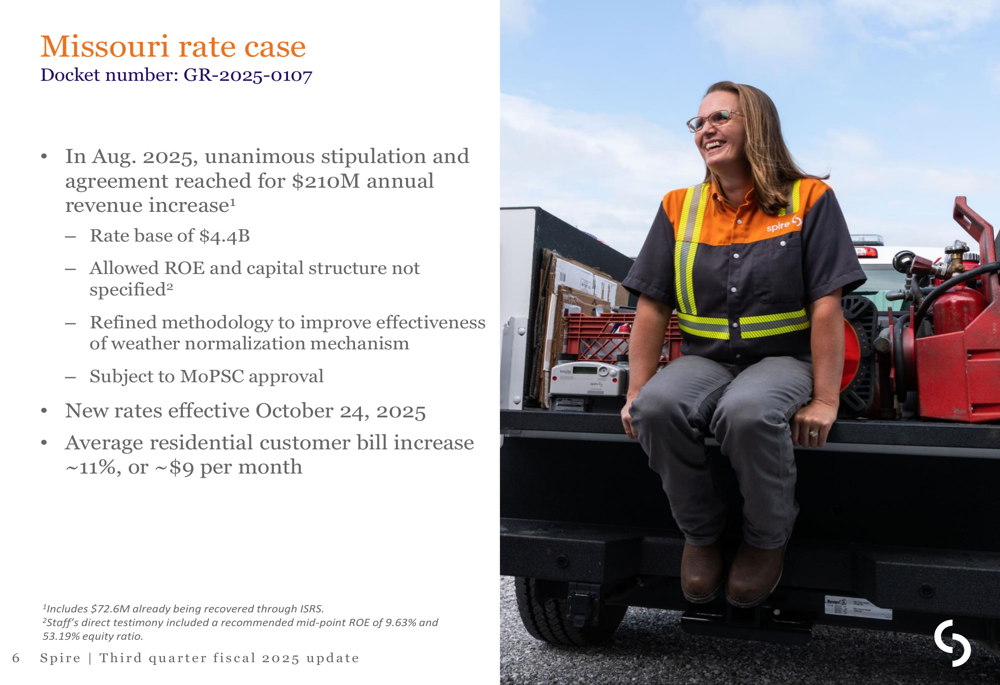

A significant regulatory milestone was achieved with a unanimous settlement agreement filed on August 4 in the Missouri rate case. The Missouri Public Service Commission approved a $210 million annual revenue increase and established a rate base of $4.4 billion.

The details of the Missouri rate case settlement include:

New rates will become effective on October 24, 2025, resulting in an average residential customer bill increase of approximately 11%, or about $9 per month. Additionally, the Missouri PSC approved $19.0 million in ISRS revenues effective May 2025.

These regulatory developments provide Spire with increased revenue stability and support for its ongoing infrastructure investments, which are critical to the company’s long-term growth strategy.

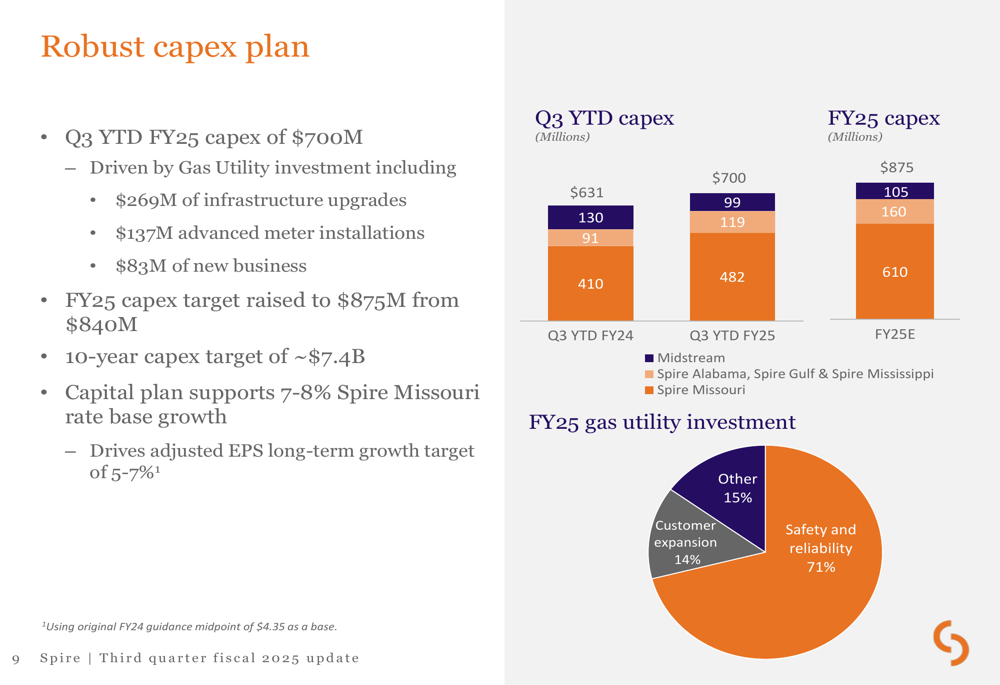

Capital Expenditure & Growth Outlook

Spire has increased its capital expenditure target for FY25 to $875 million, up from the previous target of $840 million. Year-to-date capital expenditures through Q3 FY25 reached $700 million, driven primarily by Gas Utility investments.

The breakdown of capital expenditures shows Spire’s focus on safety and reliability:

The company’s 10-year capital expenditure plan remains at $7.4 billion, with 71% of FY25 Gas Utility investments directed toward safety and reliability improvements. This includes $269 million for infrastructure upgrades and $137 million for advanced meter installations.

Spire maintained its long-term adjusted EPS growth target of 5-7% and affirmed its FY25 adjusted EPS guidance range of $4.40 to $4.60. The company’s growth outlook is supported by:

- Spire Missouri’s projected 7-8% rate base growth

- Spire Alabama and Spire Gulf’s approximately 6% equity growth

- Continued dividend growth, with the FY25 dividend increased by 4.0% to $3.14 per share

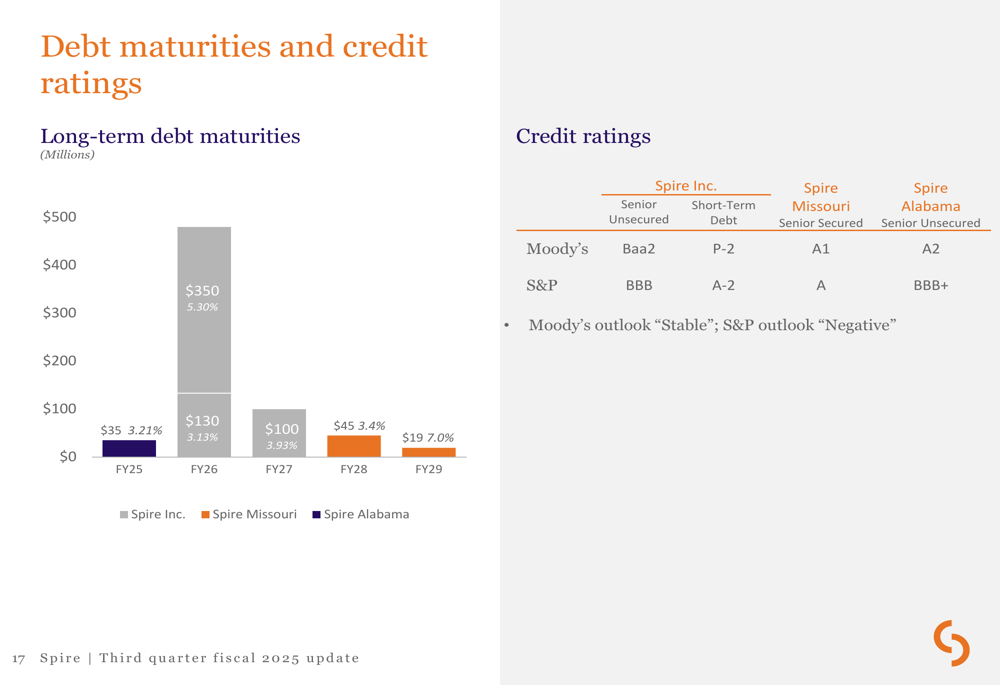

The company’s debt maturity profile and credit ratings provide additional context for its financial position:

While Moody’s maintains a stable outlook on Spire’s Baa2 rating, S&P’s outlook is negative on its BBB rating, which could potentially impact the company’s borrowing costs for future capital investments.

Forward-Looking Statements

Looking ahead, Spire’s management remains confident in the company’s growth trajectory, supported by its expanded footprint and regulatory frameworks. The acquisition of Piedmont Natural Gas Tennessee business is expected to be a significant driver of future growth, along with continued infrastructure investments across all service territories.

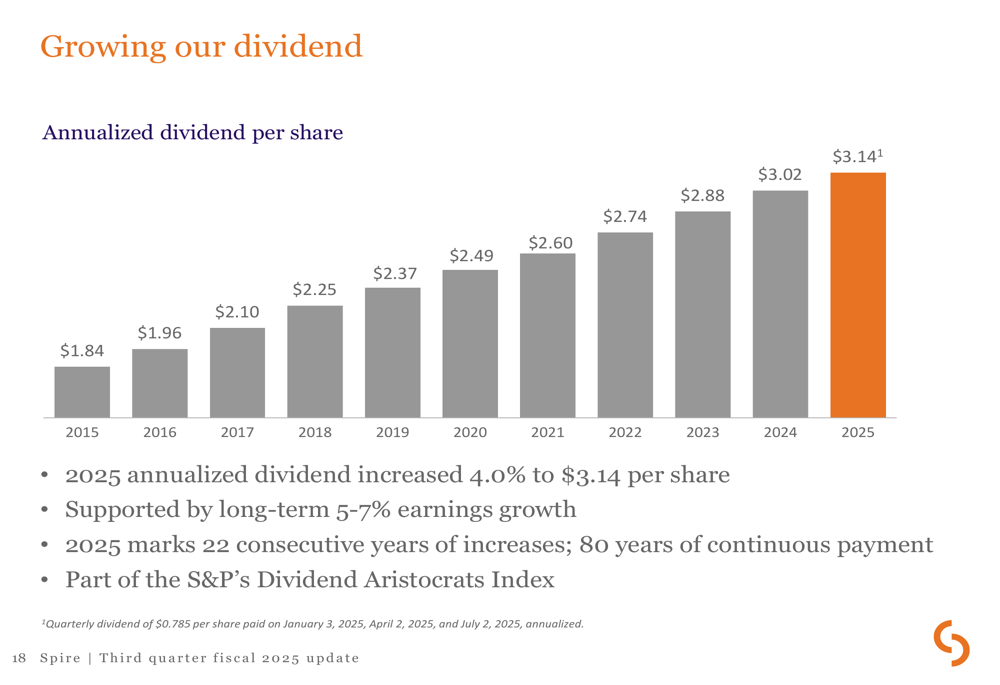

The company’s dividend growth trend illustrates its commitment to shareholder returns:

Spire has consistently increased its dividend from $1.84 per share in 2015 to $3.14 per share in 2025, representing a steady growth trajectory that management expects to maintain with the support of its 5-7% earnings growth target.

For FY25, Spire has outlined clear business priorities focused on operational excellence, regulatory engagement, financial discipline, and successful integration of its acquisition. The company’s ability to execute on these priorities while managing the integration of its Tennessee acquisition will be critical factors for investors to monitor in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.