ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

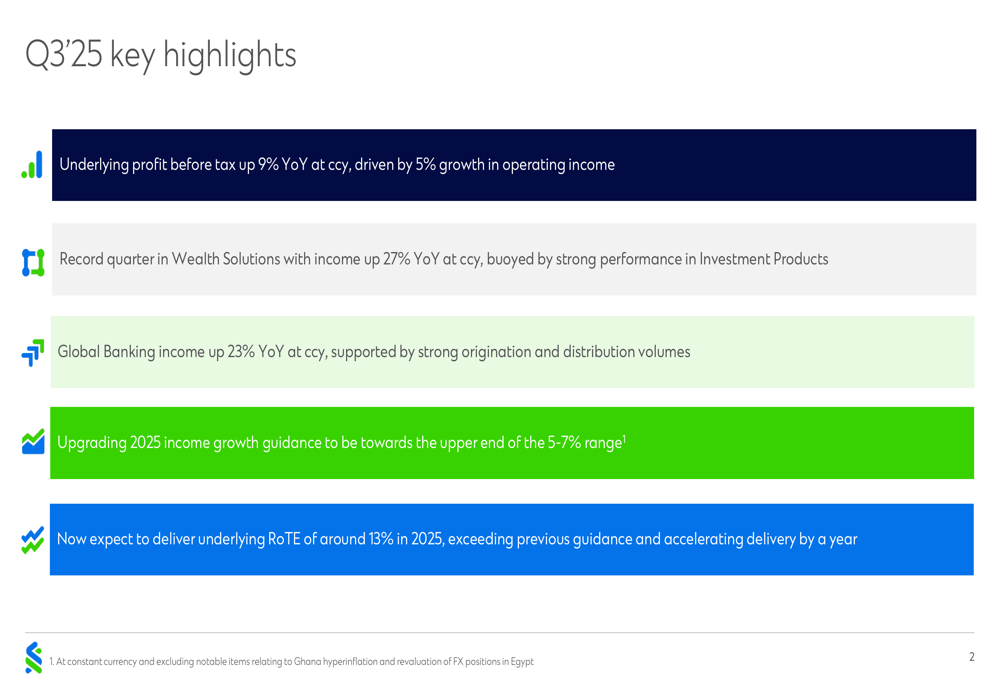

Standard Chartered PLC (LSE:STAN) presented its third quarter 2025 financial results on October 30, showing solid performance with underlying profit before tax increasing 9% year-over-year at constant currency. The bank’s shares responded positively, with a modest 0.18% increase following the earnings release.

The banking giant highlighted strong performance in its key growth engines, particularly in Wealth Solutions and Global Banking, which helped offset headwinds from lower interest rates affecting net interest income. Based on these results, Standard Chartered upgraded its 2025 income growth guidance to the upper end of the 5-7% range and now expects to achieve its return on tangible equity (RoTE) target of around 13% a year ahead of schedule.

As shown in the following key highlights slide, the bank delivered strong performance across its strategic priorities:

Quarterly Performance Highlights

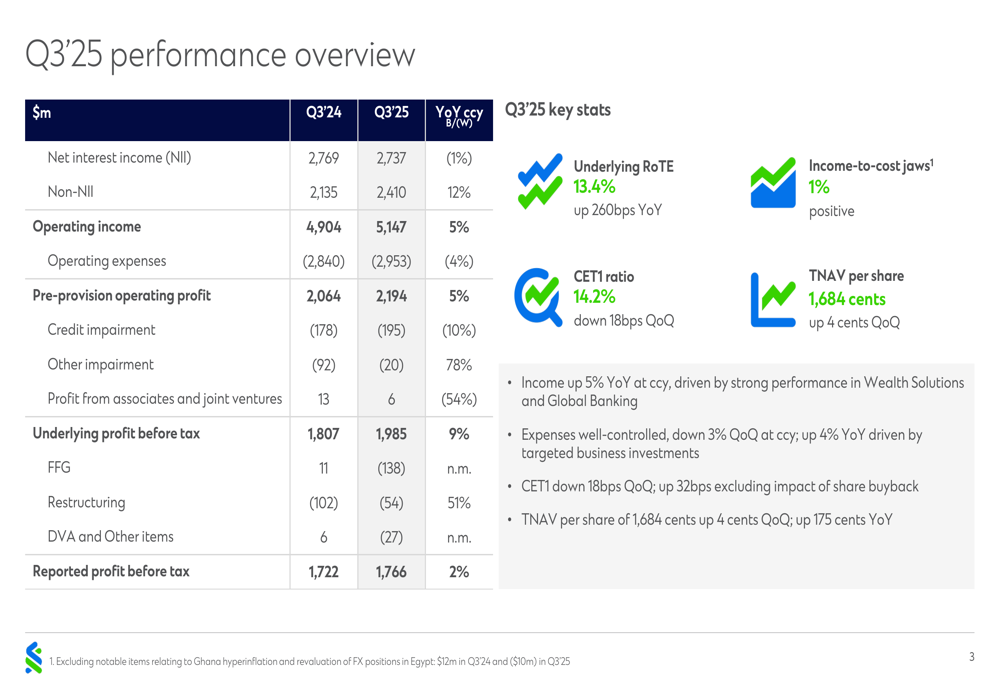

Standard Chartered reported operating income of $5.1 billion for Q3 2025, representing a 5% increase year-over-year at constant currency. This growth was primarily driven by a 12% increase in non-interest income, which helped offset a 1% decline in net interest income. The bank maintained positive income-to-cost jaws of 1%, with operating expenses increasing by 4% year-over-year to $3.0 billion.

The detailed performance overview below shows the key financial metrics for the quarter:

The bank’s net interest income (NII) faced pressure from lower global interest rates but showed resilience with a 1% quarter-on-quarter increase. This growth was driven by higher deposit volumes and an additional $30 million from higher day count in Q3, partially offset by declining rates and margins. Meanwhile, non-interest income continued to show strong momentum, up 12% year-over-year, supported by robust performance in wealth management and investment banking activities.

Standard Chartered maintained disciplined expense management despite investing in business growth. Operating expenses increased by 4% year-over-year to $2.95 billion, with inflation accounting for $52 million of the increase. The bank has achieved approximately $0.6 billion of run-rate savings from its Financial Framework for Growth (FFG) program to date and expects to reach around 85% of targeted run-rate savings by the end of 2026.

Segment Performance

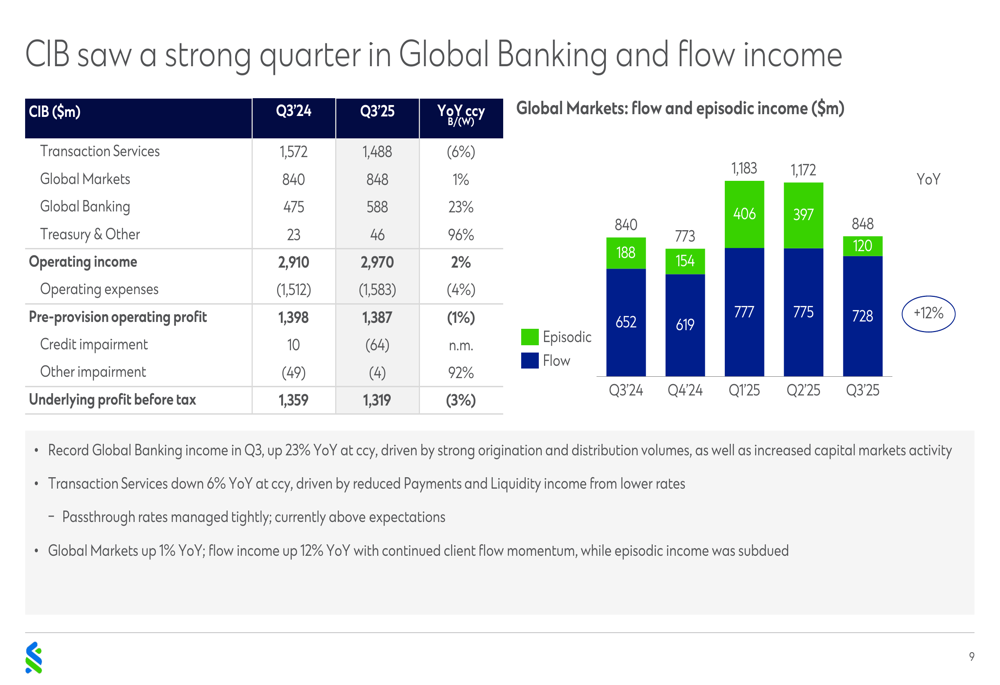

The Corporate & Investment Banking (CIB) division delivered mixed results, with overall income up 2% year-over-year to $2.97 billion. Global Banking was the standout performer with a 23% increase in income, driven by strong origination and distribution volumes, as well as increased capital markets activity. Transaction Services income declined by 6% due to reduced Payments and Liquidity income from lower rates, while Global Markets income increased by 1%.

The following slide provides a detailed breakdown of CIB’s performance:

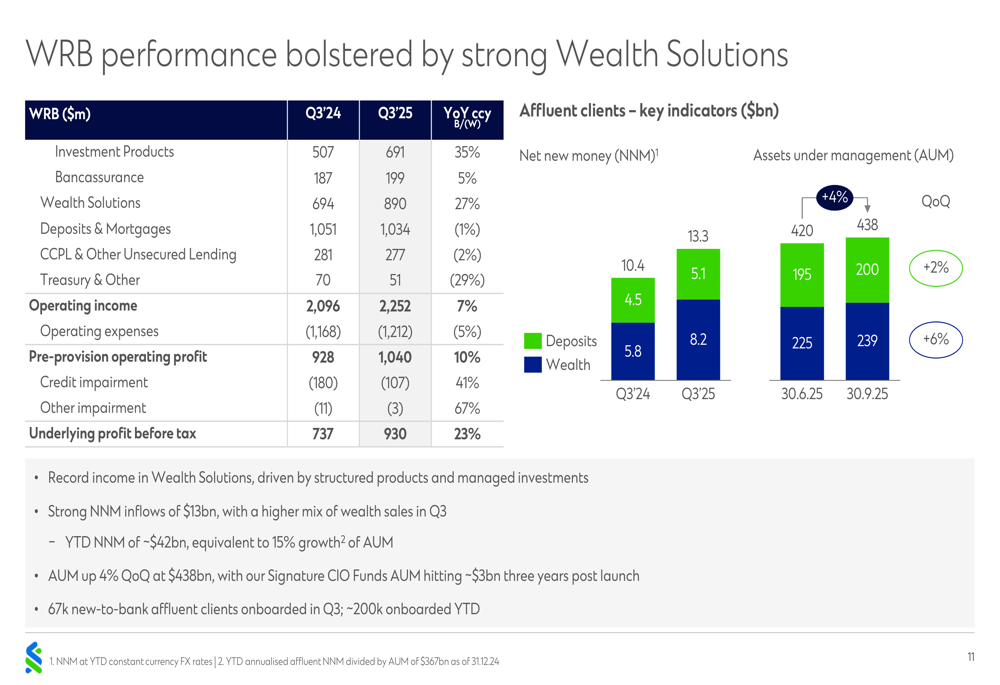

The Wealth and Retail Banking (WRB) segment showed exceptional performance, with income up 7% year-over-year to $2.25 billion. Wealth Solutions achieved record quarterly income, up 27% year-over-year to $890 million, driven by a 35% increase in Investment Products income. This strong performance helped offset the slight decline in Deposits & Mortgages income, which was down 1% due to interest rate headwinds.

As illustrated in the WRB performance slide, the segment’s underlying profit before tax increased by 23% year-over-year to $930 million, benefiting from both income growth and a 41% reduction in credit impairment:

Balance Sheet and Capital Position

Standard Chartered maintained a strong balance sheet with customer loans up 1% quarter-on-quarter to $285 billion, primarily driven by growth in WRB wealth lending and mortgages. Customer deposits increased by 2% quarter-on-quarter to $526 billion, with growth in both WRB and CIB segments.

The bank’s capital position remained robust with a Common Equity Tier 1 (CET1) ratio of 14.2%, down 18 basis points quarter-on-quarter but still well above regulatory requirements. This slight decrease was primarily due to the impact of the share buyback program, which reduced the ratio by approximately 50 basis points.

The Tangible Net Asset Value (TNAV) per share increased by 4 cents quarter-on-quarter to 1,684 cents, representing a 175 cents increase year-over-year. This growth reflects the bank’s continued focus on capital generation and shareholder value creation.

Strategic Initiatives

Standard Chartered continues to focus on growing its affluent client base, which is a key strategic priority. The bank attracted strong net new money inflows of $13.3 billion in Q3, with year-to-date net new money of approximately $42 billion, equivalent to 15% growth in assets under management (AUM). Total AUM for affluent clients increased from $420 billion in Q2 2025 to $438 billion in Q3 2025.

The bank maintains a conservative approach to credit risk management, with a loan loss rate of 24 basis points in the quarter. While this is below the historical through-the-cycle range of 30-35 basis points, management expects it to normalize towards this range in the future. The bank has also increased its overlay for Hong Kong commercial real estate exposures by $25 million in the quarter, reflecting a prudent approach to potential risks in this sector.

Forward-Looking Statements

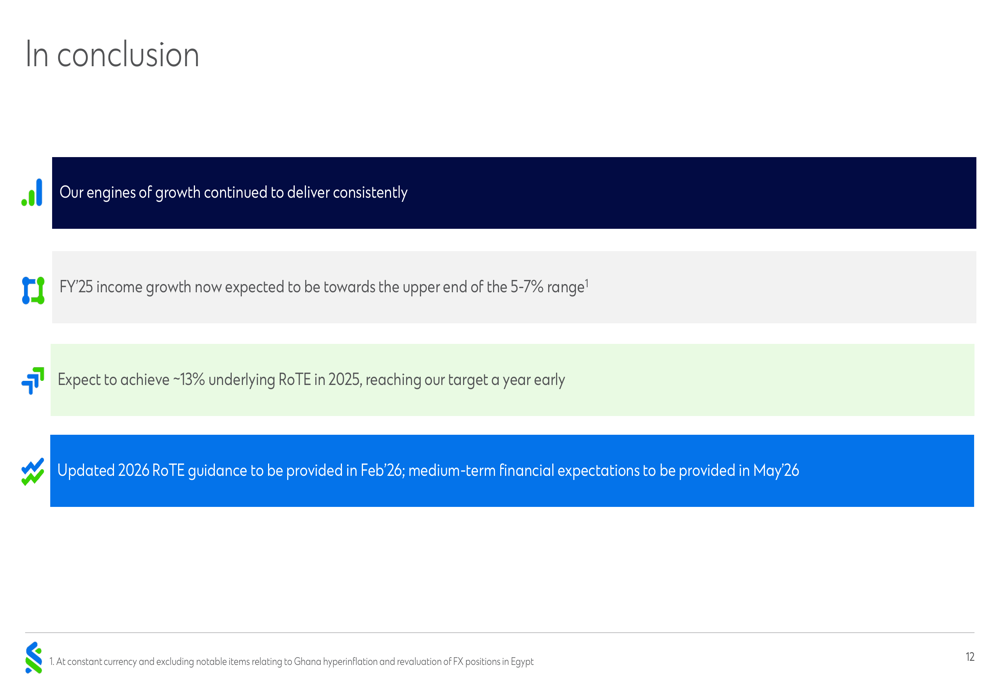

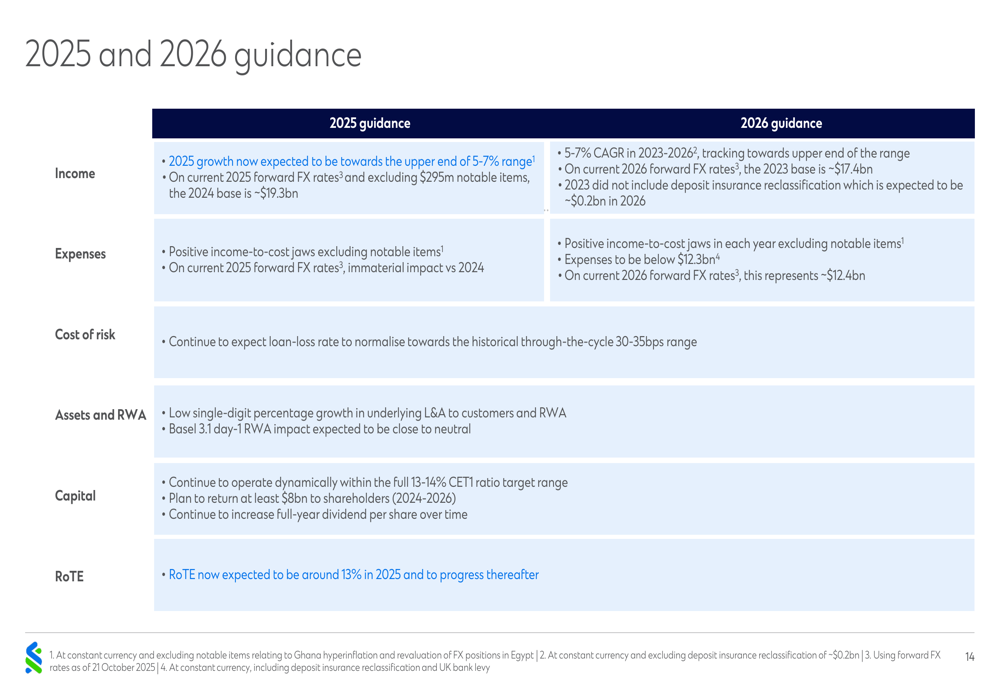

Based on the strong performance in Q3 2025, Standard Chartered has upgraded its guidance for the full year and beyond. The bank now expects 2025 income growth to be towards the upper end of the 5-7% range and anticipates achieving an underlying RoTE of around 13% in 2025, a year earlier than previously guided.

As shown in the conclusion slide, the bank’s engines of growth continue to deliver consistently, positioning it well for future success:

For 2026, Standard Chartered maintains its guidance of 5-7% compound annual growth rate (CAGR) in income for 2023-2026, tracking towards the upper end of the range. The bank also reaffirms its commitment to keeping expenses below $12.3 billion in 2026, supporting continued positive income-to-cost jaws.

The bank plans to provide updated 2026 RoTE guidance in February 2026, along with medium-term financial expectations in May 2026, giving investors a clear roadmap for its future financial trajectory.

Standard Chartered’s Q3 2025 results demonstrate the bank’s ability to navigate a challenging interest rate environment while delivering strong growth in its strategic focus areas. With upgraded guidance and accelerated delivery of its RoTE target, the bank appears well-positioned to continue creating value for shareholders in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.