Raytheon awarded $71 million in Navy contracts for missile systems

State Street Corporation (NYSE:STT) presented its second quarter 2025 financial results on July 15, showing strong fee revenue growth and record asset levels, though shares traded down nearly 5% in pre-market trading despite the largely positive results.

Introduction & Market Context

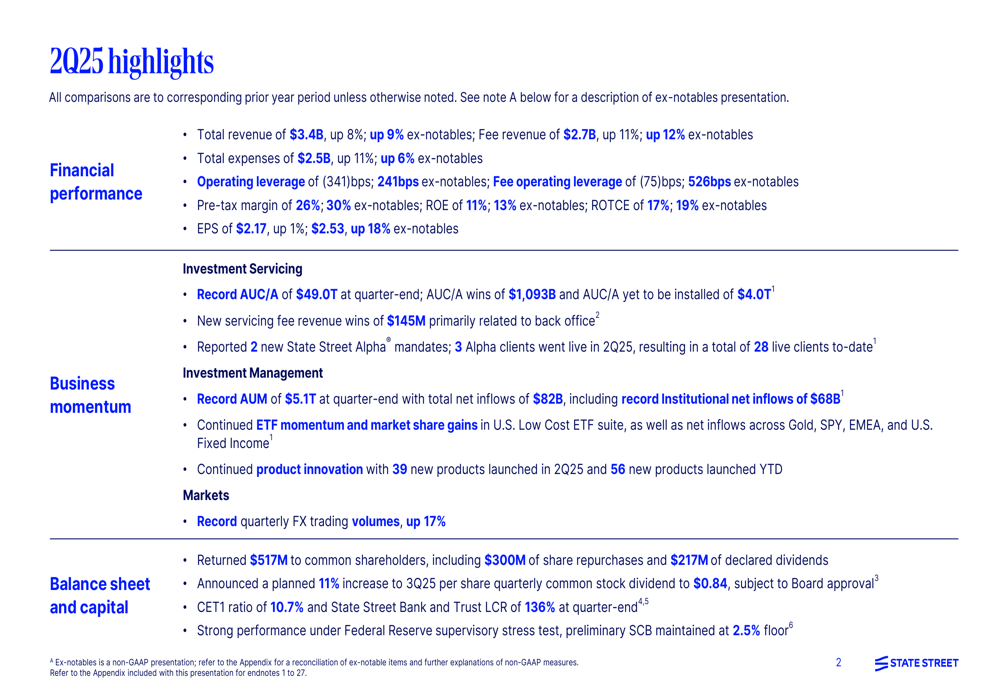

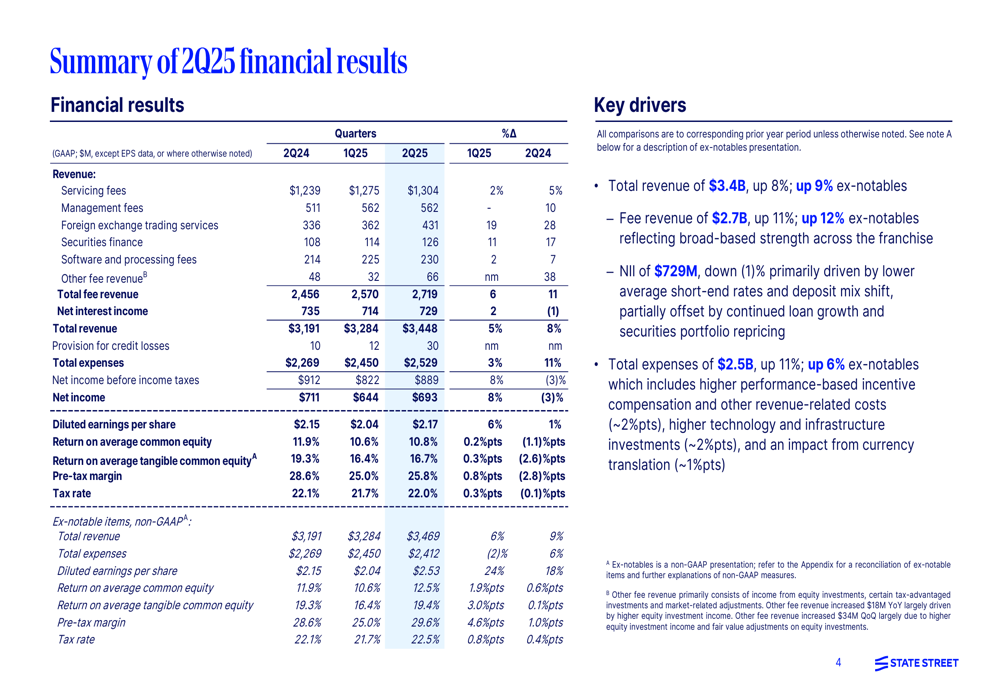

State Street reported total revenue of $3.4 billion for Q2 2025, up 8% year-over-year (9% excluding notable items), with fee revenue climbing 11% to $2.7 billion. The company achieved earnings per share of $2.17, up 1% from the prior year, or $2.53 excluding notable items, representing an 18% increase.

Despite these strong results, State Street shares were trading down 4.93% in pre-market at $104.60, suggesting investors may be concerned about expense growth, which increased 11% year-over-year, or potential margin pressures.

Quarterly Performance Highlights

State Street reported significant growth across key metrics in Q2 2025, with fee revenue showing particular strength at $2.7 billion, up 11% year-over-year or 12% excluding notable items.

As shown in the following comprehensive overview of the quarter’s performance:

The company achieved a pre-tax margin of 26% (30% excluding notable items) and return on equity of 11% (13% excluding notable items). Notable items in the quarter had a negative impact of $0.36 per share, primarily related to a $100 million repositioning charge for workforce rationalization.

The detailed financial summary shows the company’s performance across key metrics:

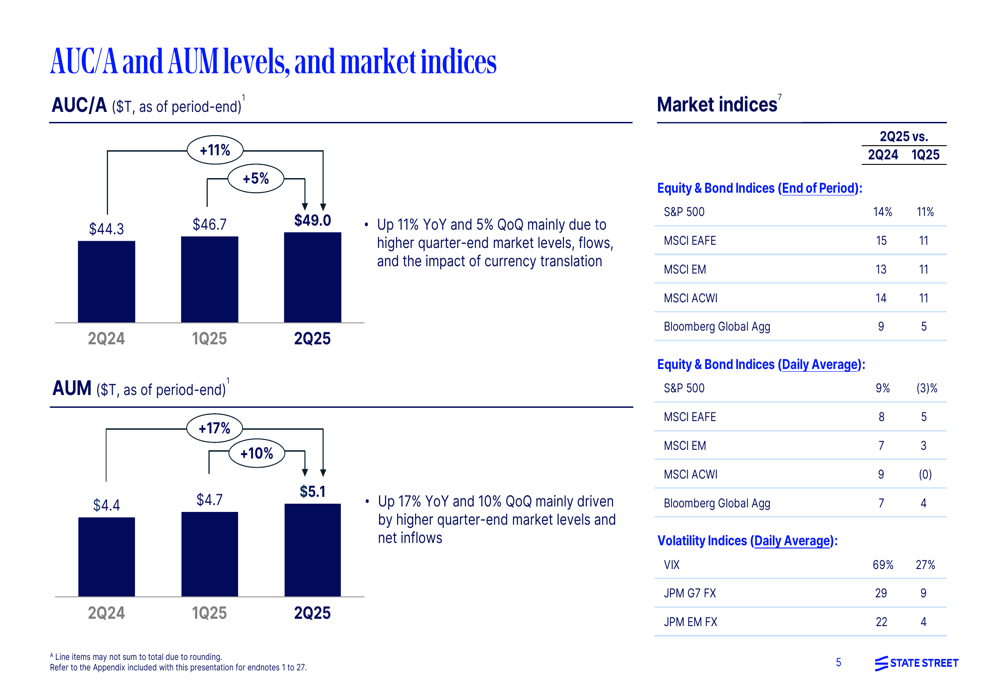

Assets under custody and administration (AUC/A) reached a record $49.0 trillion, up 5% from the previous quarter and 11% year-over-year. Similarly, assets under management (AUM) hit a record $5.1 trillion, representing a 10% increase quarter-over-quarter and 17% year-over-year.

The following chart illustrates the growth in these key metrics alongside relevant market indices:

Segment Performance

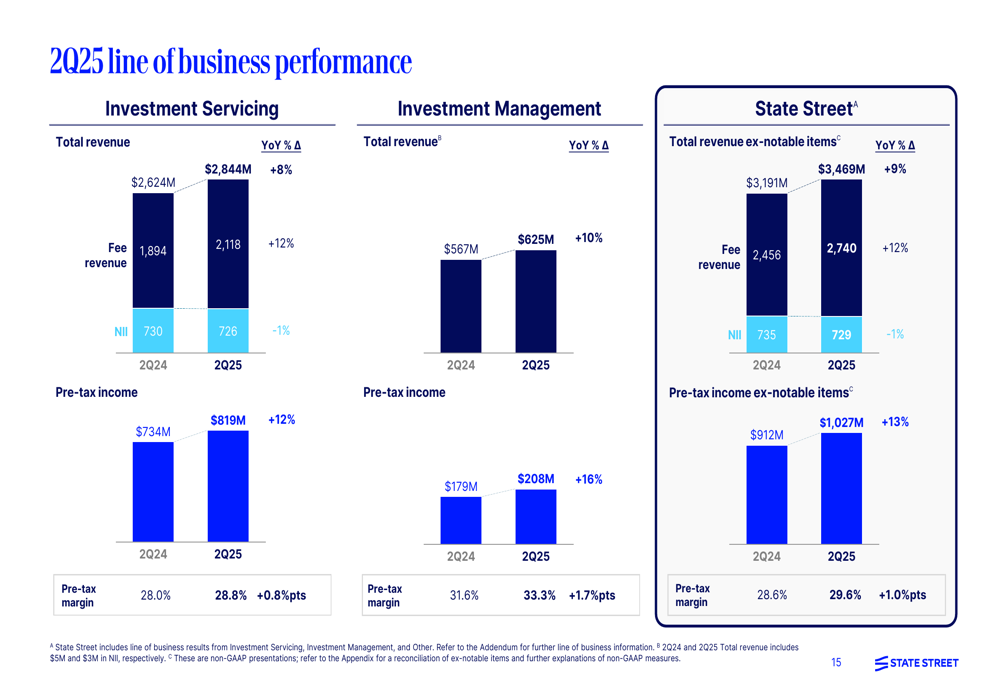

State Street’s business segments both showed strong performance in the quarter. The Investment Servicing business, which accounts for the majority of the company’s revenue, reported total revenue of $2.84 billion, up 8% year-over-year, with fee revenue increasing 12%. The segment’s pre-tax margin improved to 28.8%, up 0.8 percentage points from the prior year.

The Investment Management segment delivered $625 million in revenue, up 10% year-over-year, with a pre-tax margin of 33.3%, an improvement of 1.7 percentage points. This segment benefited from higher average market levels and net inflows from prior periods.

The breakdown of performance by business segment demonstrates the company’s balanced growth:

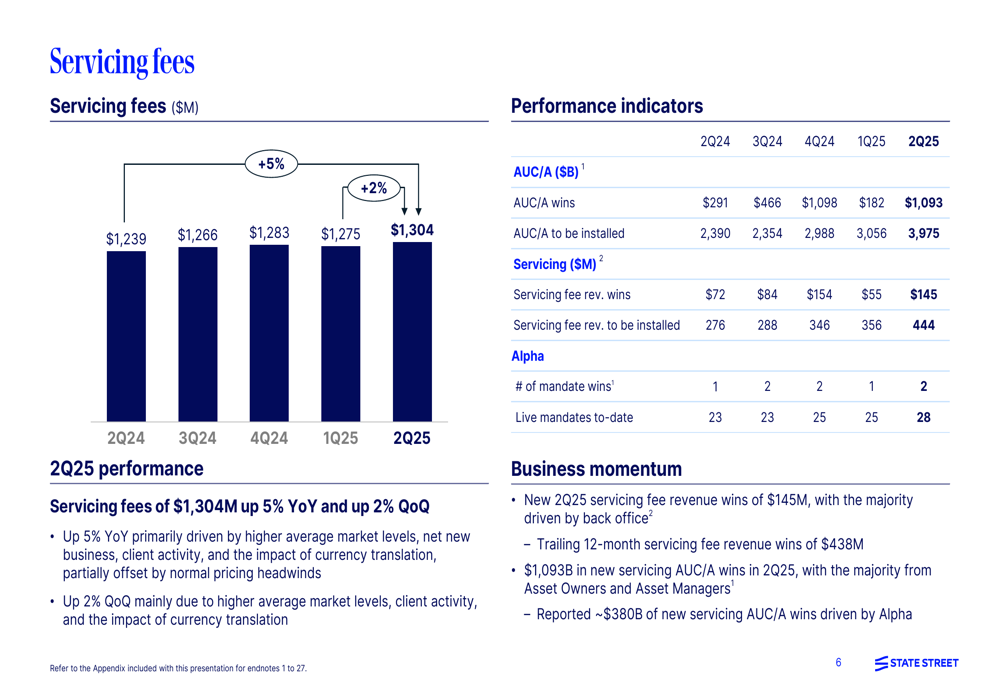

Servicing fees, a key revenue driver, increased 5% year-over-year to $1.3 billion, driven by higher average market levels, net new business, client activity, and favorable currency translation, partially offset by pricing headwinds.

The following chart details the servicing fees performance and business momentum:

FX trading services showed particularly strong performance, up 27% year-over-year to $428 million (excluding notable items), driven by higher volumes and spreads associated with increased FX volatility. Securities finance revenue increased 17% year-over-year to $126 million, largely due to higher client lending balances.

Strategic Initiatives

State Street continued to make progress on strategic initiatives during the quarter. The company reported $1.1 trillion in new assets under custody/administration wins and $145 million in new servicing fee revenue wins, primarily related to back office services.

In the Investment Management business, State Street reported record institutional net inflows of $68 billion, contributing to the Institutional franchise’s record AUM of $2.9 trillion. The ETF business continued to show momentum with market share gains in the U.S. Low Cost ETF suite and net inflows across Gold, SPY, EMEA, and U.S. Fixed Income products, bringing the ETF franchise to a record AUM of $1.7 trillion.

Product innovation remained a focus, with 39 new products launched in Q2 2025 and 56 new products launched year-to-date. The company also made a strategic investment in smallcase, a wealth technology platform based in India, expanding its global footprint.

State Street’s Alpha platform, a key technology initiative, continued to gain traction with two new mandates in the quarter and three clients going live, bringing the total to 28 live clients.

Capital and Outlook

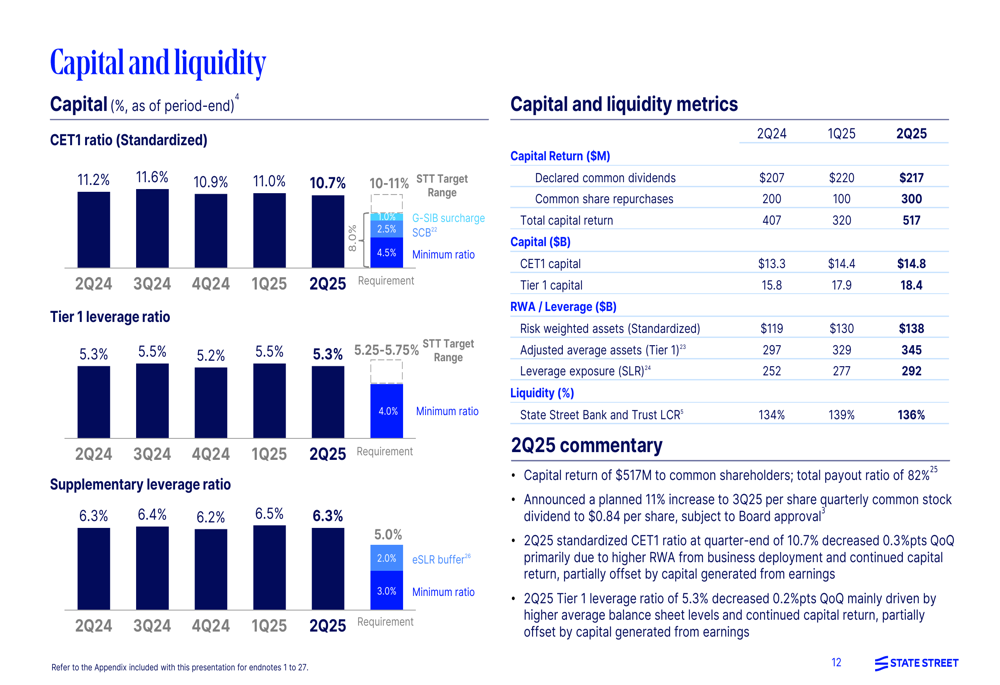

State Street maintained a strong capital position with a CET1 ratio of 10.7% and a State Street Bank and Trust liquidity coverage ratio of 136% at quarter-end. The company returned $517 million to common shareholders during the quarter, including $300 million in share repurchases and $217 million in dividends.

The following chart details the company’s capital and liquidity metrics:

Looking ahead, State Street announced a planned 11% increase to its quarterly dividend to $0.84 per share, subject to board approval. The company also reported strong performance under the Federal Reserve’s supervisory stress test, with its preliminary stress capital buffer maintained at the 2.5% floor.

Expenses remain an area of focus, with total expenses increasing 11% year-over-year to $2.5 billion, though up only 6% excluding notable items. The increase was driven by higher performance-based incentive compensation, technology and infrastructure investments, and currency translation impacts.

State Street’s Q2 2025 results demonstrate strong fee revenue growth and record asset levels, though the market reaction suggests investors may be concerned about expense growth and potential margin pressures. The company’s strategic initiatives in ETFs, institutional asset management, and technology platforms position it well for continued growth, but managing expenses will be crucial to improving shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.