IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

Stepan Company (NYSE:SCL) presented its first quarter 2025 earnings results on April 29, showing a significant rebound from its disappointing fourth quarter 2024 performance. The specialty chemical manufacturer reported substantial year-over-year growth in both reported and adjusted net income, along with increased sales volumes across all business segments.

The company’s stock, which closed at $48.19 on April 28, saw a 1.04% increase in premarket trading following the earnings announcement, signaling positive investor sentiment. This comes after Stepan’s shares have traded between $44.23 and $94.77 over the past 52 weeks, with the current price still well below the high point of that range.

Quarterly Performance Highlights

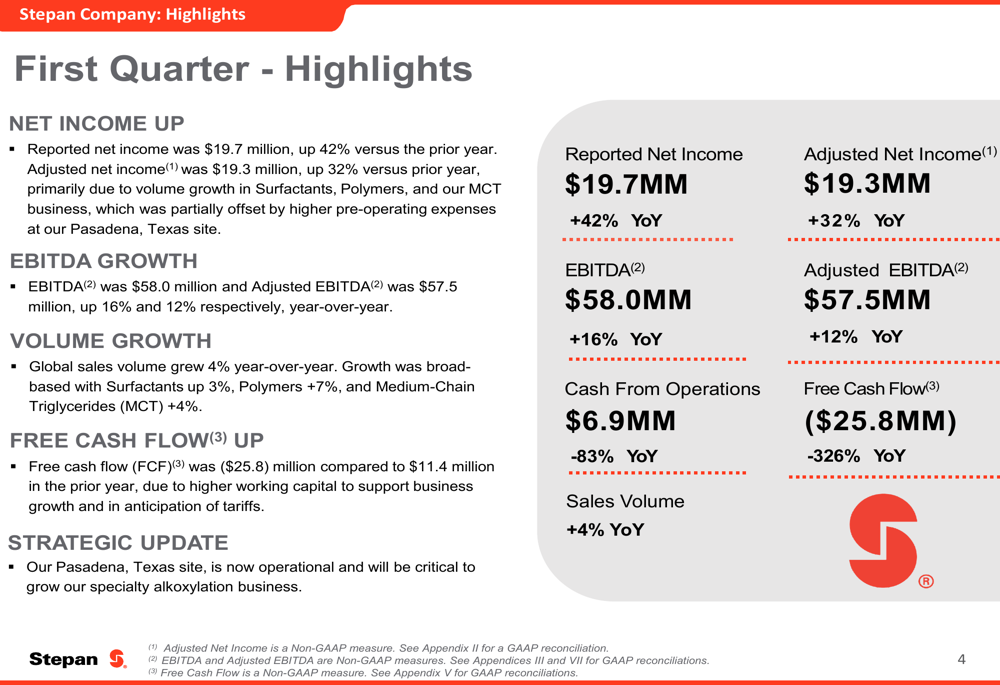

Stepan reported net income of $19.7 million for Q1 2025, representing a substantial 42% increase compared to the same period last year. Adjusted net income, which excludes deferred compensation expenses and environmental remediation costs, reached $19.3 million, up 32% year-over-year.

As shown in the following financial highlights:

EBITDA and adjusted EBITDA also showed strong growth, reaching $58.0 million (up 16%) and $57.5 million (up 12%) respectively. Global sales volume increased by 4% year-over-year, with all three business segments contributing positively: Surfactants (+3%), Polymers (+7%), and Specialty Products (+4%).

The company’s net sales for the quarter totaled $593.3 million, compared to $551.4 million in Q1 2024, representing a 7.6% increase. Earnings per share improved to $0.86, up from $0.61 in the first quarter of 2024.

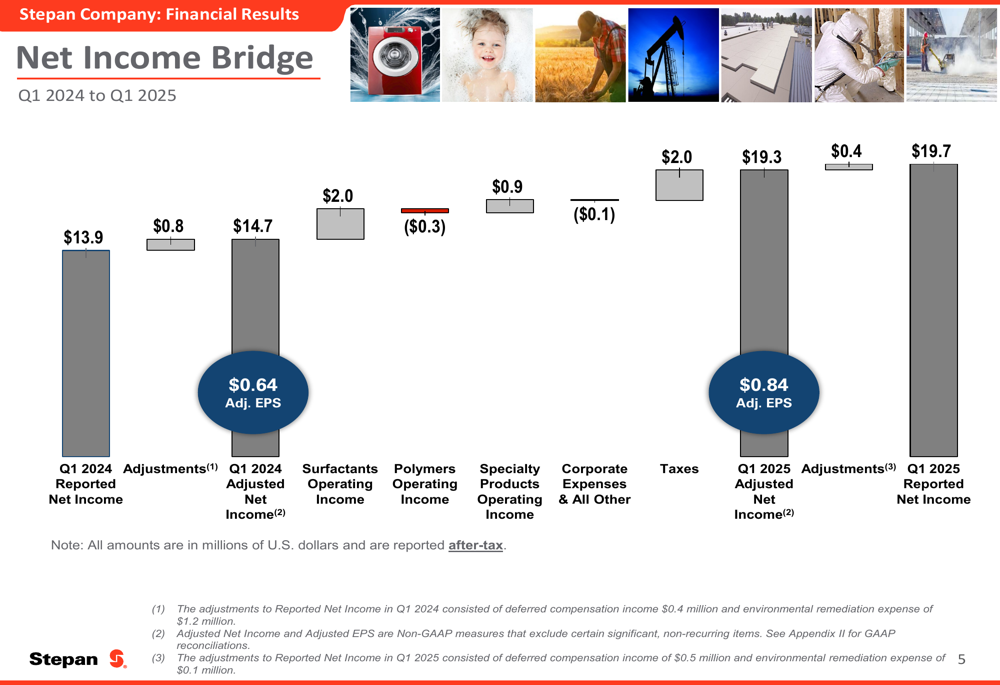

The following bridge chart illustrates the factors contributing to the net income growth:

Segment Analysis

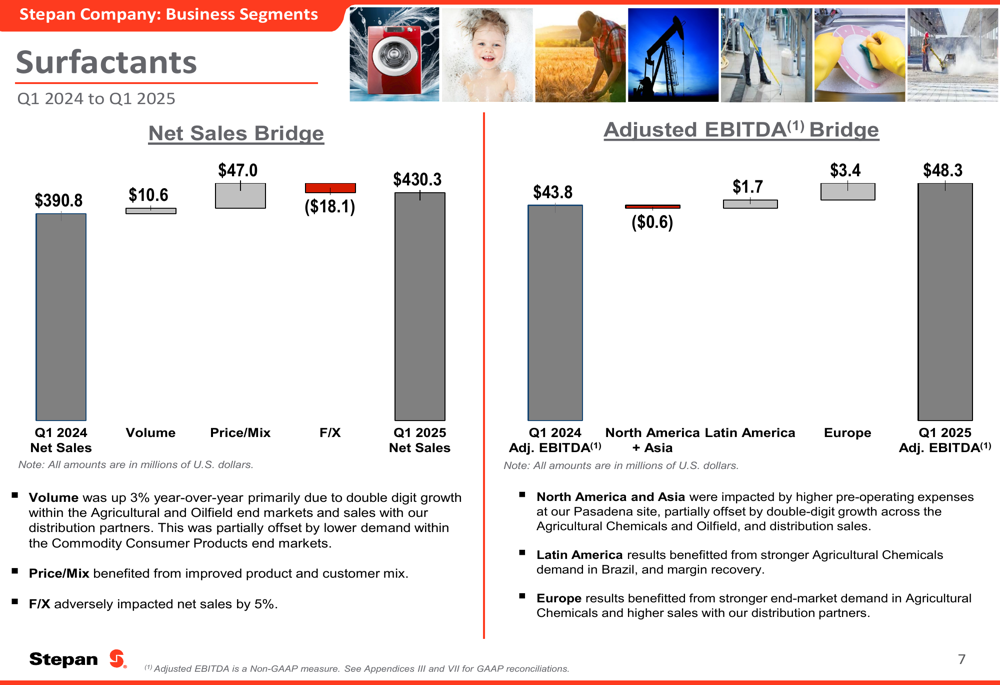

The Surfactants segment, Stepan’s largest business unit, delivered strong performance with net sales of $430.3 million, up from $390.8 million in Q1 2024. This growth was primarily driven by favorable price/mix effects (+$47.0 million) and increased volume (+$10.6 million), partially offset by negative foreign exchange impacts (-$18.1 million).

The segment’s adjusted EBITDA increased to $48.3 million from $43.8 million in the prior year, with European operations contributing the largest improvement (+$3.4 million) followed by Latin America (+$1.7 million). North America and Asia results decreased slightly (-$0.6 million) due to higher pre-operating expenses.

As shown in the following Surfactants segment performance breakdown:

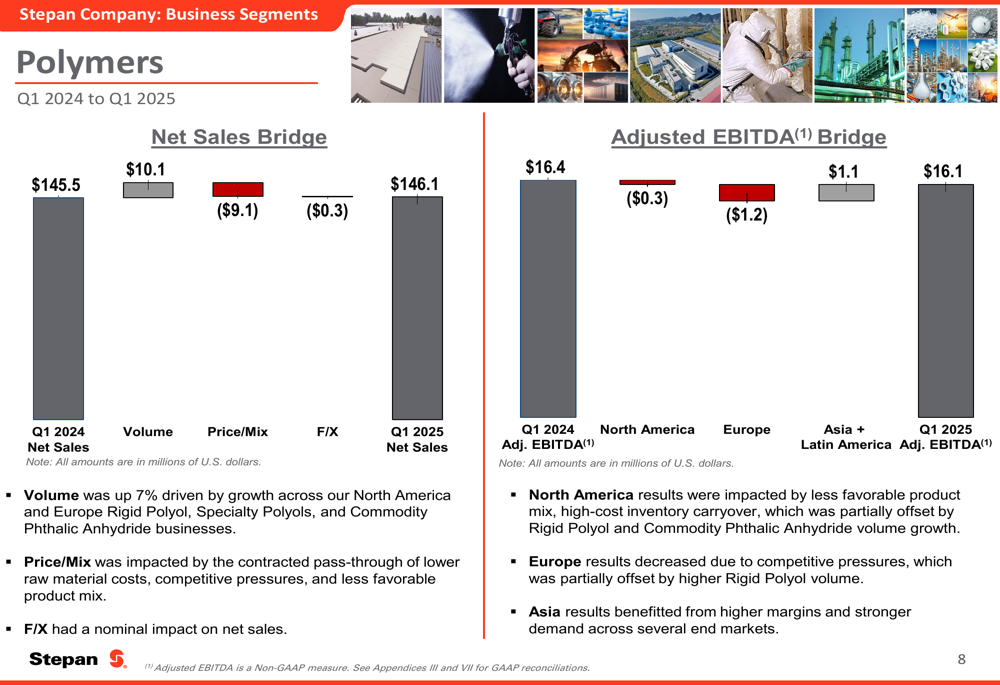

The Polymers segment showed more modest growth, with net sales of $146.1 million compared to $145.5 million in Q1 2024. While volume increased significantly (+$10.1 million), this was largely offset by negative price/mix effects (-$9.1 million) and slight foreign exchange headwinds (-$0.3 million).

Adjusted EBITDA for the Polymers segment decreased slightly to $16.1 million from $16.4 million, with declines in North America (-$0.3 million) and Europe (-$1.2 million) partially offset by improvements in Asia and Latin America (+$1.1 million). The European results were impacted by competitive pressures, while North American performance suffered from less favorable product mix.

The following chart details the Polymers segment performance:

Strategic Initiatives and Capital Investments

A major highlight of the quarter was the operational start of Stepan’s new alkoxylation facility in Pasadena, Texas. This $265 million capital investment provides 75,000 tons of annual alkoxylation capacity, a core surfactant technology for the company. The facility is strategically located to support continued volume growth in this business area.

As detailed in the strategic capital investments update:

The company continues to focus on four strategic priorities: targeting high-margin growth markets, customer-centric innovation, operational excellence, and strategic investments. Stepan aims to achieve growth rates exceeding GDP, with an emphasis on accretive margins and expanding its customer base, particularly in Tier 2 and Tier 3 segments.

Balance Sheet and Financial Position

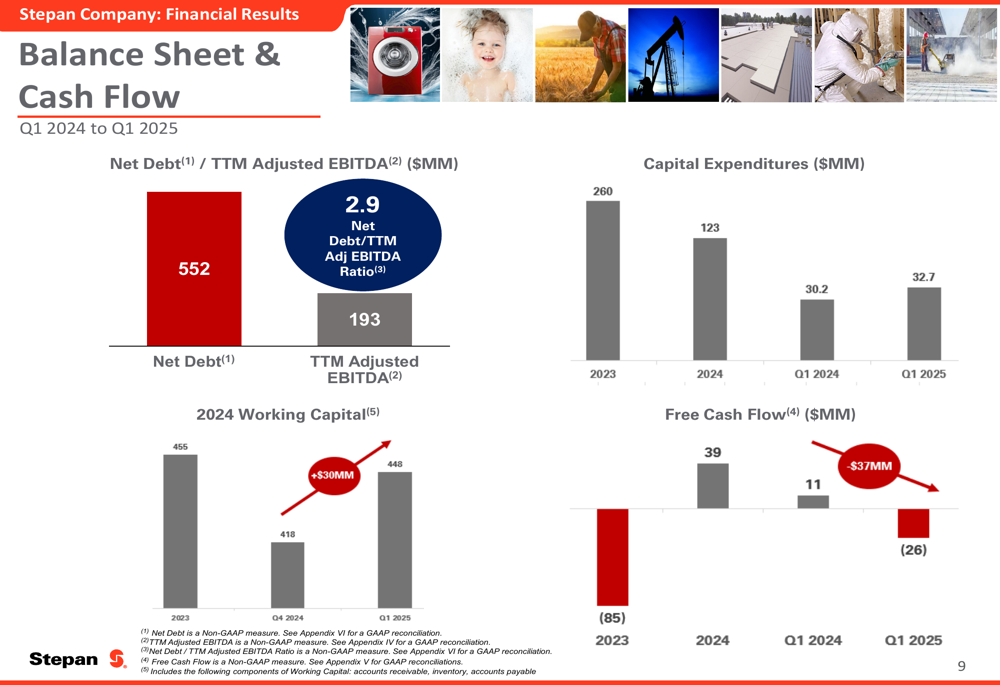

Despite the strong operating performance, Stepan reported negative free cash flow of $25.8 million for Q1 2025, compared to positive $11.4 million in Q1 2024. This decline was primarily due to lower cash flow from operations ($6.9 million vs. $41.6 million) while capital expenditures remained relatively stable at $32.7 million.

The company’s net debt to total capitalization ratio stood at 31% as of March 31, 2025, unchanged from December 31, 2024. The net debt to trailing twelve months adjusted EBITDA ratio was 2.9, indicating moderate leverage.

As shown in the following balance sheet and cash flow summary:

Forward-Looking Statements

Looking ahead to the remainder of 2025, Stepan provided guidance on several key financial metrics. The company expects capital expenditures of $125-135 million, significantly lower than the $260 million spent in 2023 and slightly higher than the $123 million in 2024. This reduction reflects the completion of major projects like the Pasadena facility.

Interest expenses are projected to increase to $24-26 million, up from $14 million in 2024, likely due to higher debt levels and interest rates. Depreciation and amortization is expected to reach $125-130 million, compared to $112 million in 2024, reflecting the addition of new assets. The effective tax rate is forecast at 23-25%, higher than the 17% reported in 2024.

These projections suggest that while Stepan has made significant investments in growth initiatives, the company now faces higher financing costs and depreciation expenses that will impact bottom-line results in the coming quarters. However, the operational start of the Pasadena facility is expected to contribute positively to volume growth and supply chain savings in the second half of the year.

The first quarter results represent a strong start to 2025 for Stepan, particularly compared to the disappointing fourth quarter of 2024 when the company missed EPS forecasts by a significant margin. The operational status of the Pasadena facility fulfills management’s previous guidance that it would come online in Q1 2025, demonstrating execution of strategic initiatives as planned.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.