Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

Sterling Infrastructure, Inc. (NASDAQ:STRL) delivered exceptional third-quarter results on November 4, 2025, showcasing significant growth across key financial metrics. The infrastructure services provider, headquartered in The Woodlands, Texas, continues to benefit from its strategic transformation initiated in 2015, with particularly strong performance in its E-Infrastructure Solutions segment.

The company’s stock responded positively to the earnings announcement, rising 4.13% in pre-market trading to $409, approaching its 52-week high of $419.14. With approximately 4,900 employees and a market capitalization of $11.61 billion, Sterling has established itself as a leading player in the infrastructure services sector.

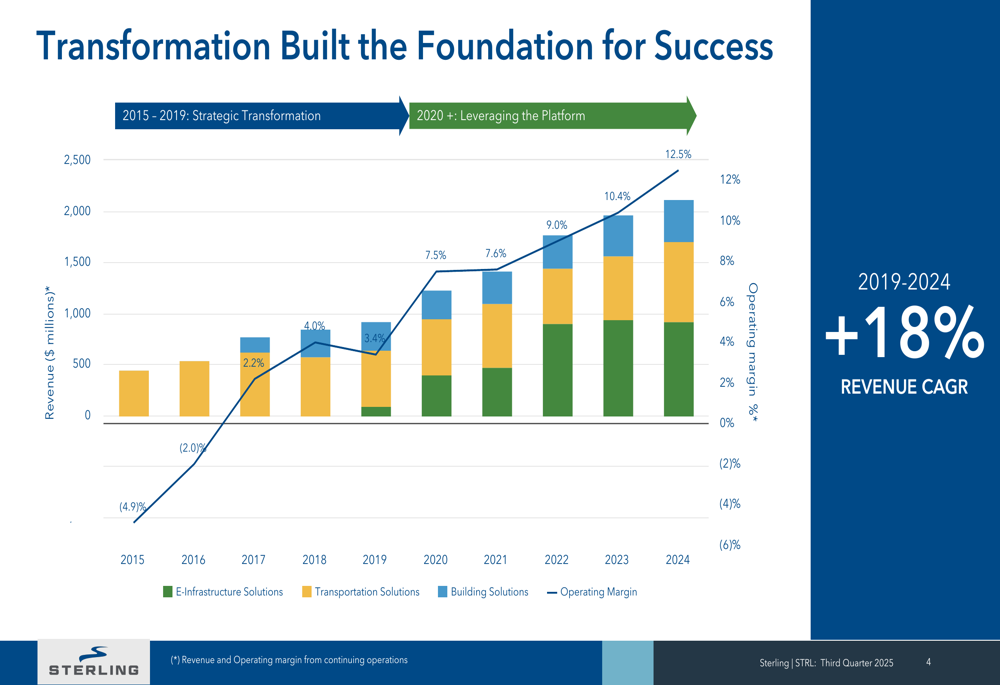

Sterling’s multi-year transformation has yielded impressive results, as evidenced by the company’s revenue and margin expansion over the past decade.

As shown in the following chart of revenue growth and operating margin improvement:

Quarterly Performance Highlights

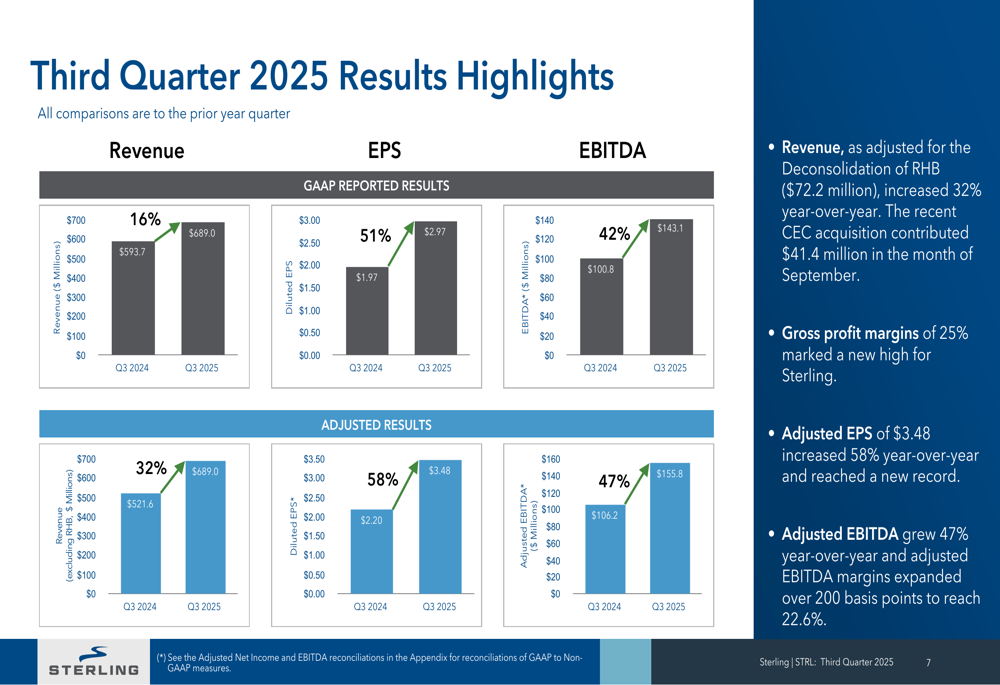

Sterling reported Q3 2025 revenue of $689.0 million, representing a 32% increase year-over-year when adjusted for the deconsolidation of RHB ($72.2 million). The CEC acquisition contributed $41.4 million to this growth. Gross profit margins reached a new high of 25%, while adjusted EPS surged 58% year-over-year to $3.48, significantly exceeding analyst expectations of $2.84.

Adjusted EBITDA grew 47% compared to the same period last year, with margins expanding over 200 basis points to 22.6%. The company’s strong execution and favorable project mix were key drivers of this performance.

The following chart illustrates Sterling’s Q3 2025 financial highlights compared to Q3 2024:

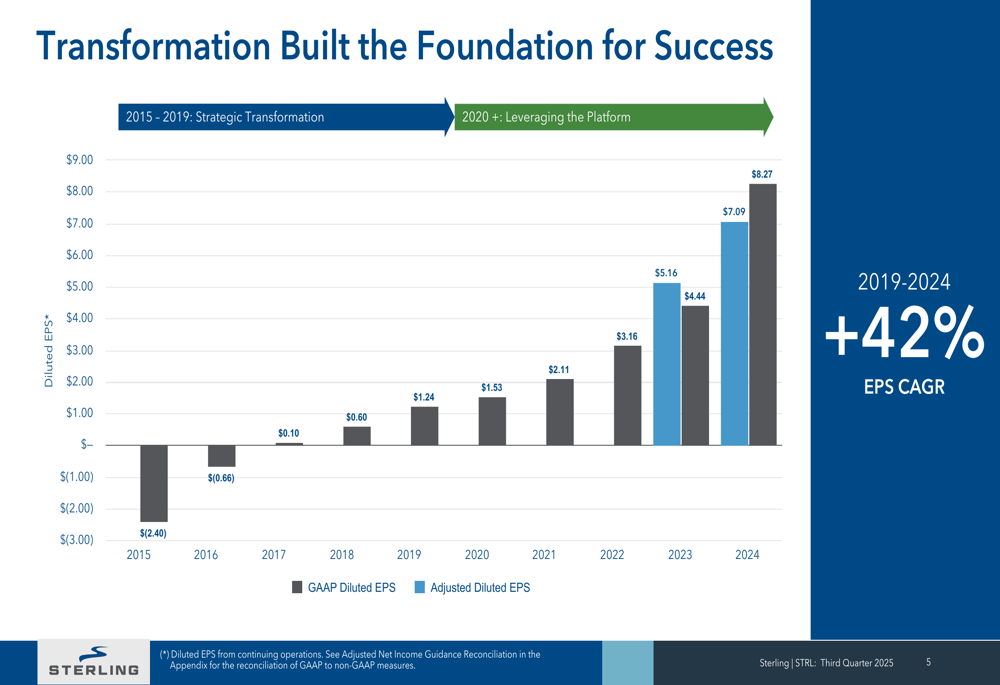

This impressive earnings growth continues the trend seen over recent years, as demonstrated by the company’s diluted EPS trajectory:

Segment Analysis

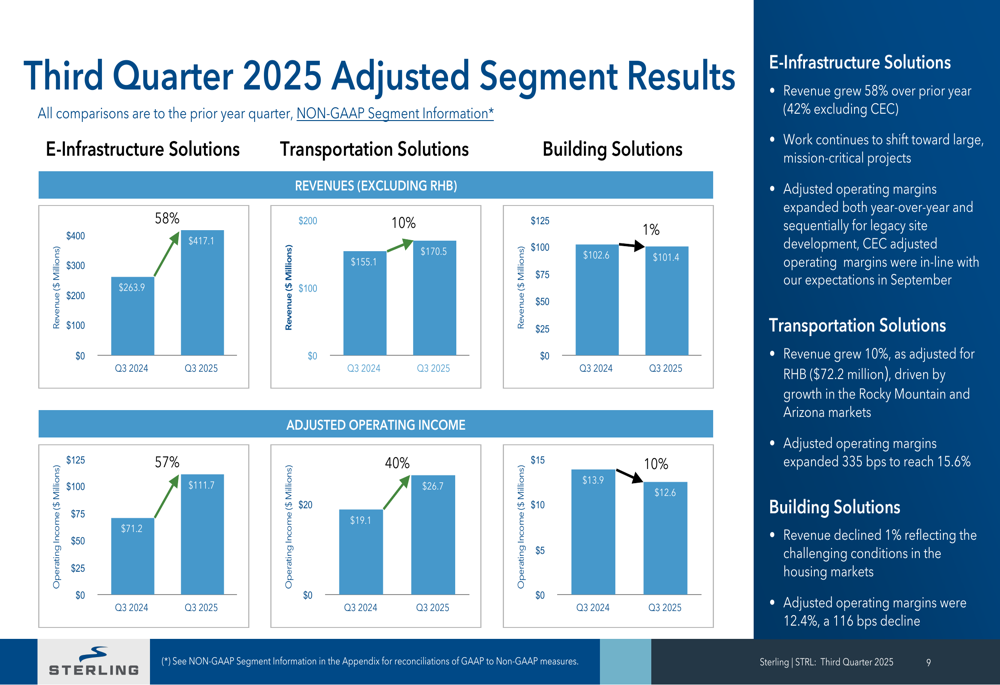

Sterling’s performance varied significantly across its three business segments, with E-Infrastructure Solutions leading the way in terms of growth and profitability.

The E-Infrastructure Solutions segment, which focuses on data centers, semiconductor fabrication, and e-commerce distribution centers, delivered exceptional results with revenue growing 58% over the prior year (42% excluding the CEC acquisition). Adjusted operating margins expanded, reflecting the segment’s strong execution and favorable market conditions.

Transportation Solutions saw revenue growth of 10% when adjusted for RHB deconsolidation, with adjusted operating margins expanding 335 basis points to reach 15.6%. This improvement reflects a favorable project mix shift and good execution despite challenges.

Building Solutions, however, experienced a 1% revenue decline due to softness in housing markets, with adjusted operating margins contracting 116 basis points to 12.4%.

The following chart breaks down Sterling’s segment performance for Q3 2025:

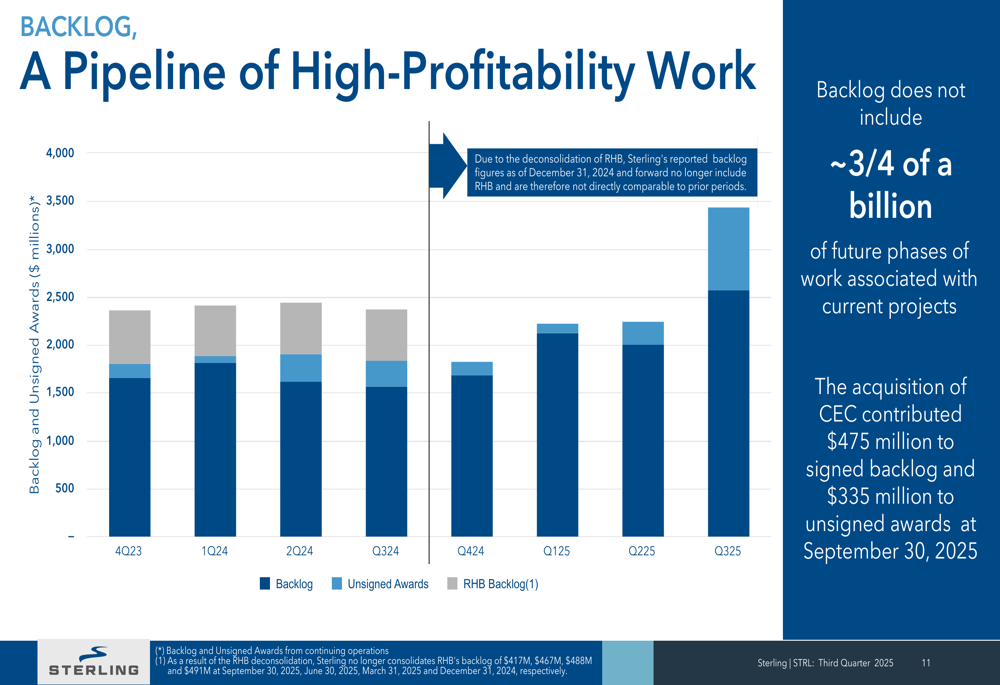

Backlog and Future Outlook

Sterling’s remaining performance obligations (RPOs), also referred to as backlog, reached $2,575.4 million as of September 30, 2025, representing a substantial increase from $1,693.2 million at the end of 2024. This growth was primarily driven by the E-Infrastructure Solutions segment, which saw its backlog increase from $1,032.1 million to $1,808.2 million during this period.

The acquisition of CEC contributed significantly to this backlog expansion, adding $475 million to signed backlog and $335 million to unsigned awards. Importantly, the company noted that current backlog figures don’t include approximately three-quarters of a billion dollars of future phases of work associated with current projects.

The following chart illustrates Sterling’s backlog and unsigned awards over time:

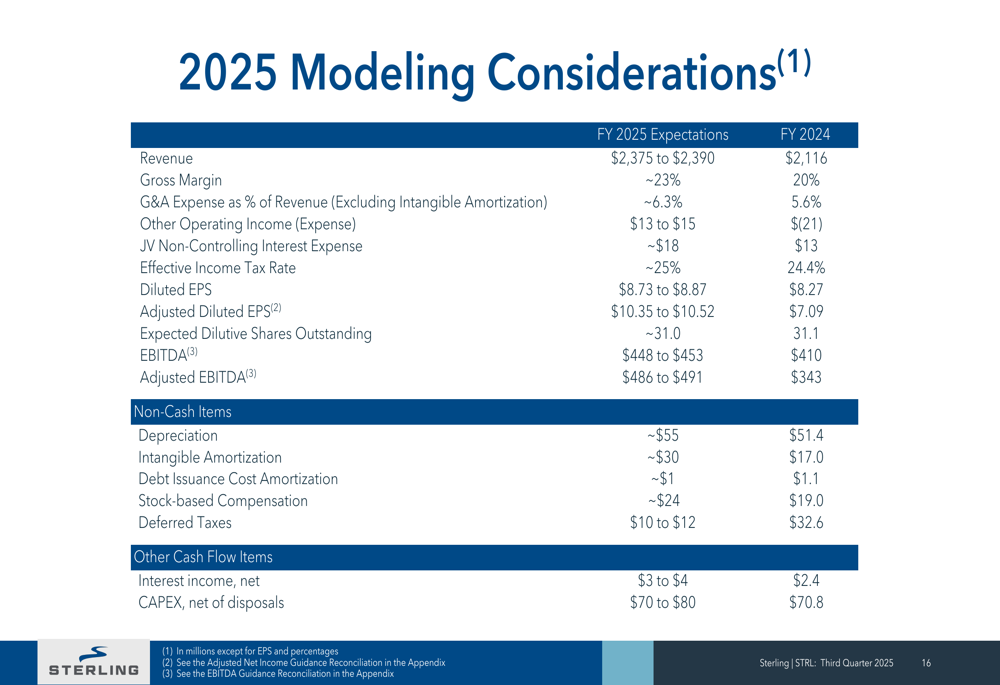

Looking ahead, Sterling provided guidance for full-year 2025, projecting revenue between $2,375 and $2,390 million, adjusted diluted EPS of $10.35 to $10.52, and adjusted EBITDA of $486 to $491 million. The company expects gross margins of approximately 23% and G&A expenses of around 6.3% of revenue.

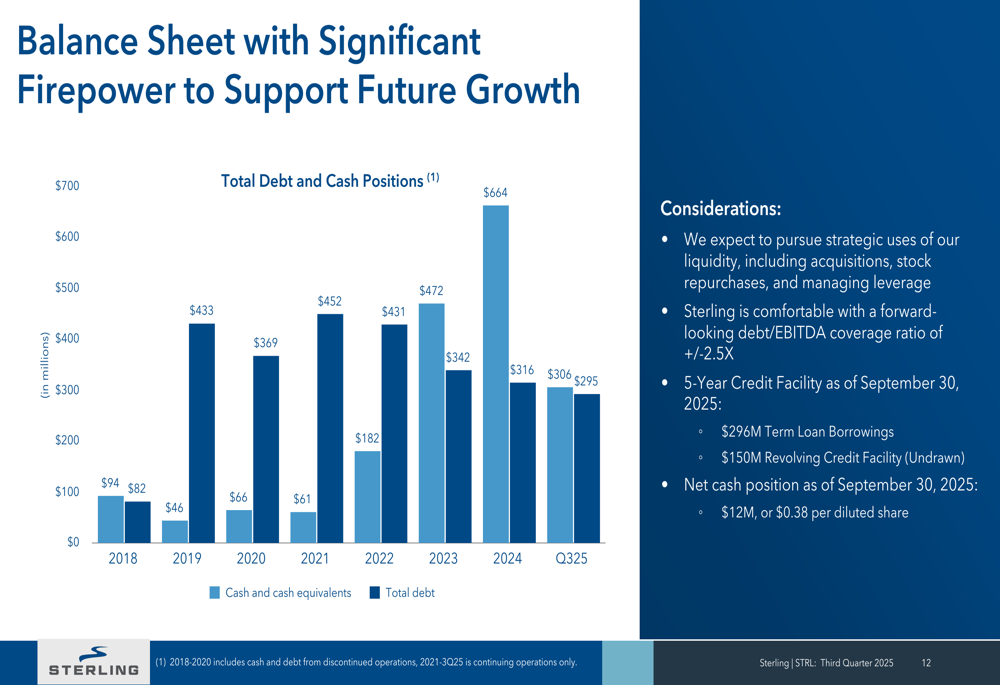

Financial Position

Sterling has maintained a strong balance sheet, with a net cash position of $12 million ($0.38 per diluted share) as of September 30, 2025. The company has a 5-year credit facility with $296 million in term loan borrowings and an undrawn $150 million revolving credit facility.

Management expressed comfort with a forward-looking debt/EBITDA coverage ratio of approximately 2.5x and indicated plans to pursue strategic uses of liquidity, including potential acquisitions and stock repurchases.

The following chart shows Sterling’s debt and cash positions from 2018 to Q3 2025:

Competitive Industry Position

Sterling has successfully positioned itself as a leading provider of infrastructure services across three key solution areas. The company’s strategic transformation, initiated in 2015, has created a strong, diversified platform with multi-year secular growth drivers.

The E-Infrastructure segment, which includes data centers, semiconductor fabrication, and e-commerce distribution centers, has become the company’s primary growth engine, benefiting from increased investment in digital infrastructure. The Transportation Solutions segment continues to provide stable performance with improving margins, while Building Solutions faces challenges from the current housing market environment.

Sterling’s robust backlog, strong balance sheet, and consistent free cash flow generation position the company well for continued growth and potential strategic acquisitions. The company’s focus on mission-critical infrastructure projects and expansion through acquisitions like CEC have bolstered its market position, despite challenges in certain segments.

As Sterling continues to execute its growth strategy, the company remains well-positioned to capitalize on infrastructure investment trends while maintaining its focus on margin expansion and operational excellence.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.