SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Superior Group of Companies (NASDAQ:SGC), a diversified provider of healthcare apparel, branded products, and contact center services, recently presented its August 2025 investor deck following disappointing Q1 2025 results. The company’s stock has struggled, trading near its 52-week low of $9.11 after falling 9.07% following its earnings miss, with shares down nearly 39% over the past six months.

The presentation highlights SGC’s long-term growth potential across its three business segments while acknowledging near-term challenges. The contrast between the company’s optimistic growth narrative and recent financial performance provides important context for investors evaluating the stock’s potential.

Business Segment Overview

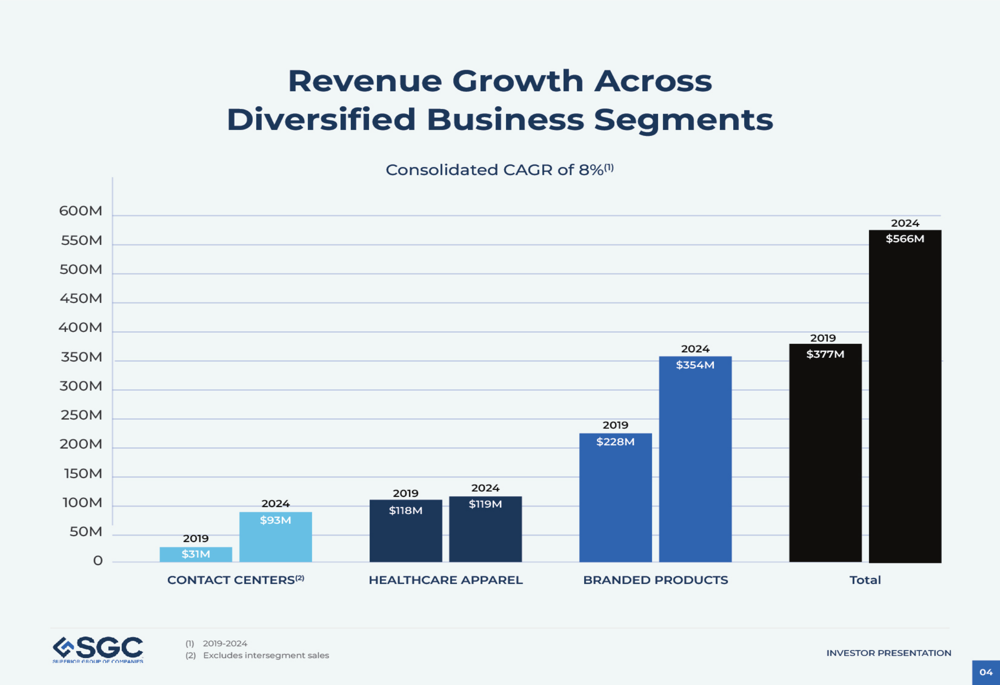

Superior Group operates across three distinct business segments, each targeting large addressable markets with varying growth trajectories. The company has achieved a consolidated compound annual growth rate (CAGR) of 8% between 2019 and 2024, with total revenue increasing from $377 million to $566 million.

As shown in the following revenue growth chart across business segments:

The Contact Centers segment has been the standout performer, growing from $31 million in 2019 to $93 million in 2024, while Healthcare Apparel has remained relatively flat, increasing only from $118 million to $119 million during the same period. Branded Products has shown solid growth, rising from $228 million to $354 million.

The Contact Centers business, operated under "The Office Gurus" brand, represents SGC’s highest-margin and fastest-growing segment. The company highlights several competitive advantages in this space, including nearshore centers with English-fluent agents, multiple locations offering redundancy, cost savings for clients, and a more personalized approach compared to larger providers.

As illustrated in the Contact Center growth opportunities slide:

With a 21.6% five-year CAGR through 2024, 12.6% EBITDA margin, and 103% net revenue retention, the Contact Centers segment presents significant growth potential given SGC’s minimal 0.1% share of a $121 billion U.S. market.

Financial Performance & Outlook

Superior Group’s long-term revenue growth has been impressive, with an 11% annualized growth rate since 2014, as shown in this comprehensive revenue chart:

However, recent performance has fallen short of expectations. In Q1 2025, SGC reported a loss of $0.05 per share, missing the forecasted $0.12 EPS, while revenue came in at $137.1 million, slightly below the anticipated $139.85 million. The company’s gross margin decreased to 36.8% from 39.8% year-over-year, and it reported a net loss of $800,000 compared to a $3.9 million net income in Q1 2024.

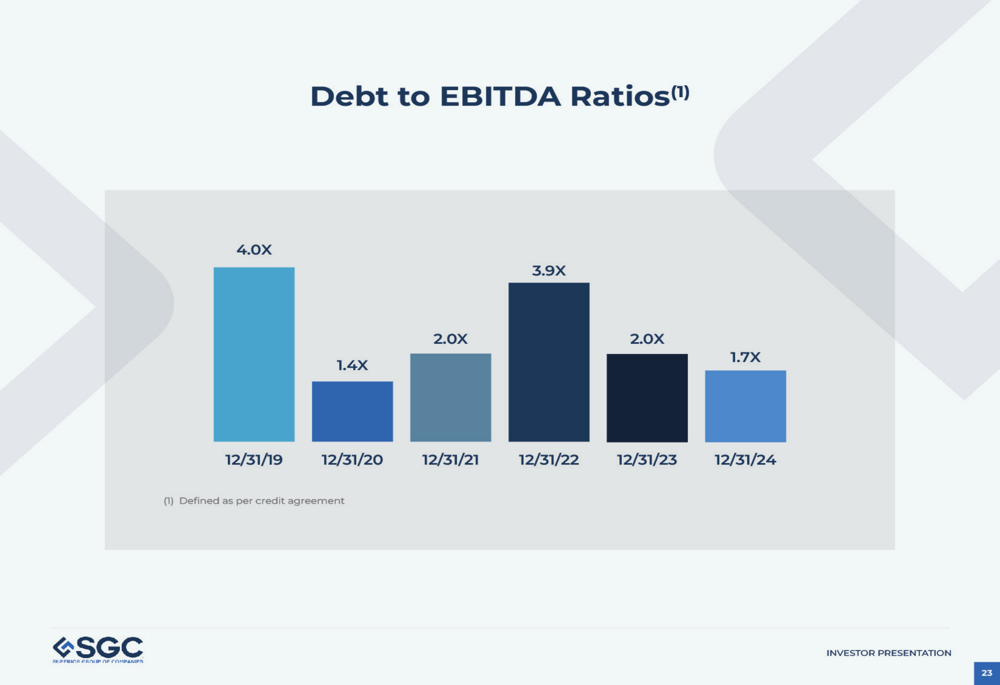

The company has made progress in strengthening its balance sheet, with debt to EBITDA ratios improving from 4.0x in 2019 to 1.7x in 2024:

Following the Q1 results, Superior Group revised its full-year 2025 revenue guidance downward to $550-$575 million from the previous $585-$595 million, citing economic uncertainty and potential supply chain disruptions.

Growth Strategy & Market Opportunity (SO:FTCE11B)

Despite recent challenges, Superior Group’s presentation emphasizes significant growth opportunities across all three business segments due to their modest market shares in large addressable markets.

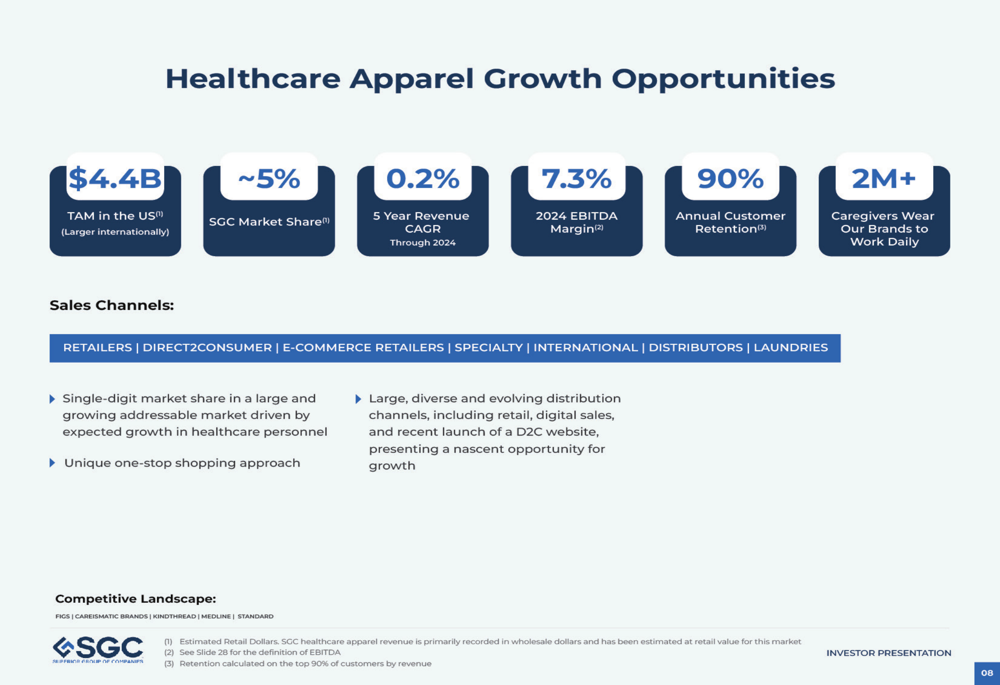

The Healthcare Apparel segment, which includes brands like Fashion Seal Healthcare, Wink Scrubs, and Carhartt Medical (TASE:BLWV), targets a $4.4 billion U.S. market where SGC holds approximately 5% market share:

With 90% annual customer retention and over 2 million caregivers wearing SGC brands daily, the company sees growth potential through multiple distribution channels despite the segment’s flat recent performance.

Similarly, the Branded Products segment operates in a highly fragmented $26 billion U.S. market where SGC holds roughly 1% market share:

The company serves major brands across various industries, leveraging its position as one of the top ten largest branded products distributors among more than 25,000 in the U.S.

Capital Allocation & Corporate Responsibility

Superior Group’s capital allocation strategy focuses on balancing shareholder returns with investments for growth:

The company has maintained an uninterrupted dividend since 1977, authorized share repurchase plans in 2024 and 2025, and continues to invest in organic growth opportunities while remaining open to strategic acquisitions.

SGC also highlights its corporate social responsibility initiatives, including significant plastic bottle recycling efforts and workforce diversity metrics:

These ESG initiatives may appeal to socially conscious investors and potentially help the company attract and retain talent in competitive labor markets.

Challenges & Risks

While the investor presentation paints an optimistic picture of SGC’s long-term prospects, the company faces significant near-term challenges. During the Q1 2025 earnings call, management cited economic uncertainty, tariff announcements contributing to market volatility, and supply chain disruptions expected to persist for 6-9 months.

The institutional healthcare market remains particularly slow, which may explain the flat performance of the Healthcare Apparel segment. CEO Michael Benstock emphasized a conservative approach in navigating the current economic climate, stating, "Never waste a crisis."

The company has implemented $13 million in annualized cost savings to mitigate these challenges, but investors should monitor whether these efficiency measures can offset the headwinds facing the business.

Investment Highlights

Superior Group summarizes its investment case with four key points:

The company emphasizes its diversified business model operating in large, profitable growth industries; organic growth potential across all segments; historically high-margin operations; and a solid balance sheet facilitating strategic investments and capital returns to shareholders.

However, investors should weigh these long-term opportunities against the near-term challenges evidenced by the recent earnings miss and stock price decline. The contrast between the optimistic presentation and current financial performance highlights the importance of monitoring execution in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.