Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

Swisscom AG (SWX:SCMN) presented its third quarter 2025 results on November 6, revealing a slight revenue decline but maintaining its full-year guidance as cost-saving initiatives and lower capital expenditures helped stabilize operational free cash flow. The Swiss telecommunications giant continues to face competitive pressures in its home market and integration challenges in Italy following its Vodafone Italia acquisition.

Despite these headwinds, Swisscom emphasized its network quality leadership in Switzerland and progress on strategic initiatives including AI services expansion and the ongoing integration of its Italian operations.

Quarterly Performance Highlights

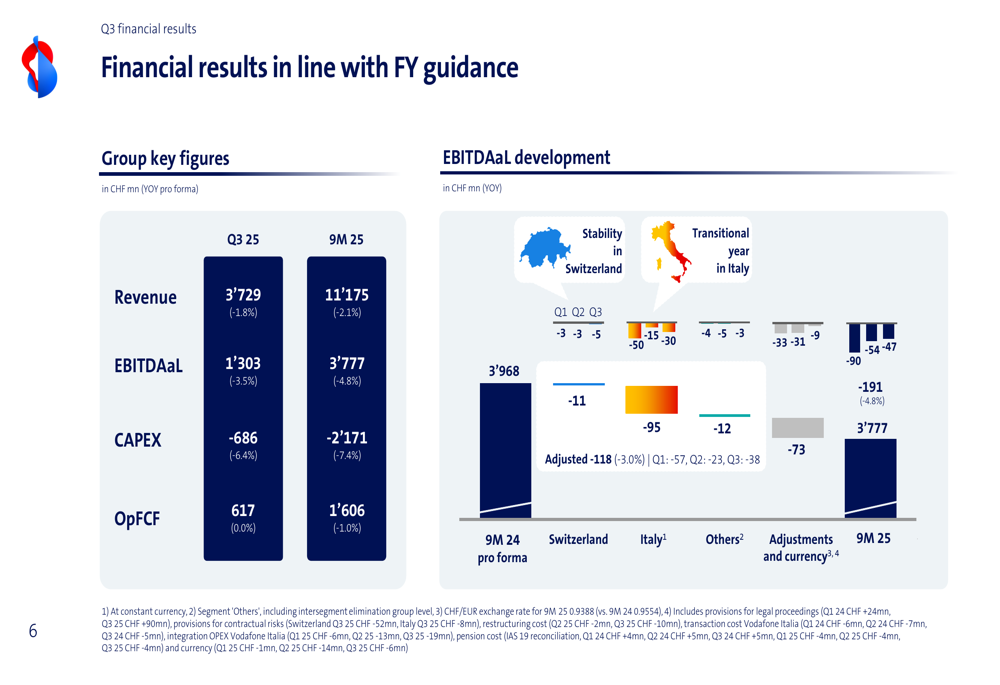

Swisscom reported Q3 2025 revenue of CHF 3,729 million, representing a 1.8% year-over-year decline. For the first nine months of 2025, revenue reached CHF 11,175 million, down 2.1% compared to the same period last year. EBITDAaL (EBITDA after lease) decreased by 3.5% to CHF 1,303 million for the quarter and by 4.8% to CHF 3,777 million for the nine-month period.

As shown in the following financial results chart, the company’s operational free cash flow remained stable despite revenue pressure:

The stability in operational free cash flow was achieved through reduced capital expenditures, which declined by 6.4% to CHF 686 million in Q3 and by 7.4% to CHF 2,171 million for the first nine months of 2025. This careful management of investments helped offset the impact of lower service revenues.

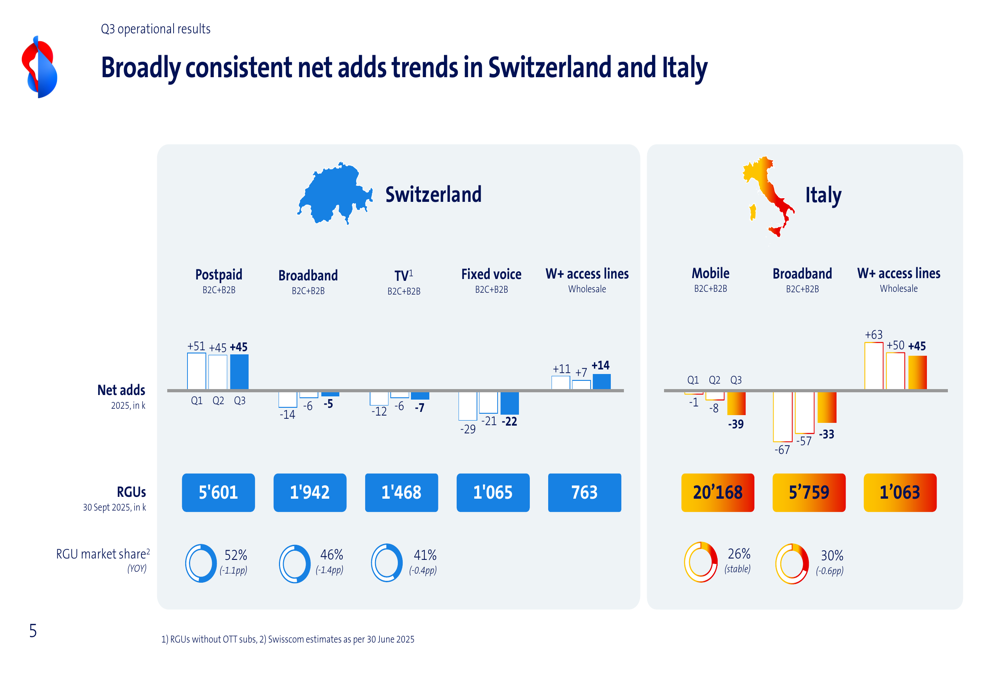

In terms of operational metrics, Swisscom maintained strong market positions in Switzerland while facing some competitive pressure:

The company’s Swiss market share stands at 52% for postpaid mobile (-1.1 percentage points year-over-year), 46% for broadband (-1.4 percentage points), and 41% for TV services (-0.4 percentage points). In Italy, mobile market share remained stable at 26%, while fixed market share decreased slightly to 30% (-0.6 percentage points).

Cost Transformation and Strategic Initiatives

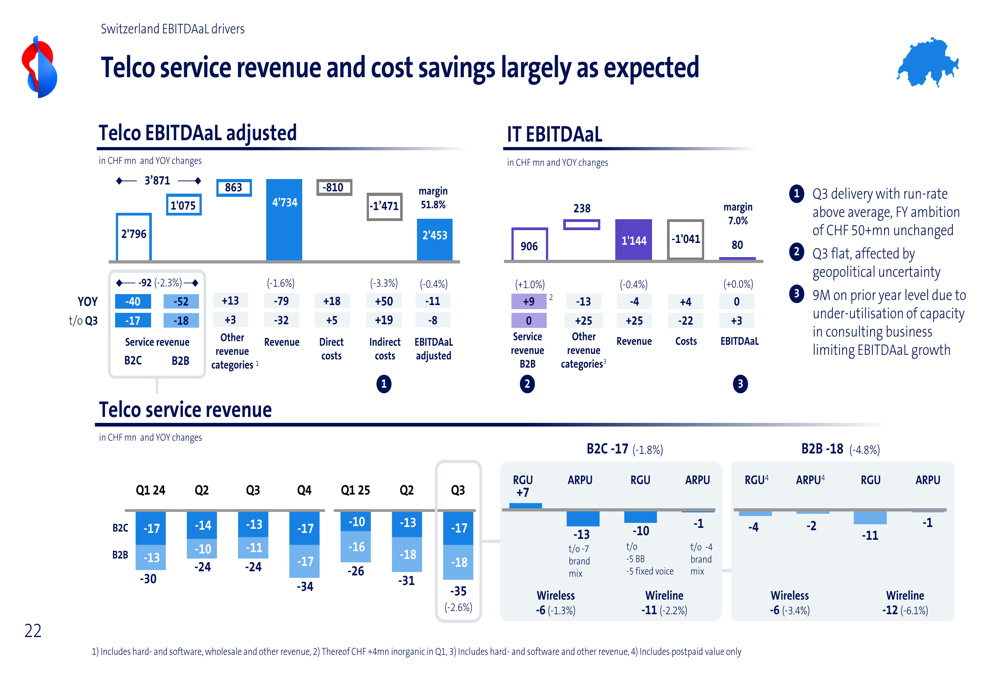

A key element of Swisscom’s strategy has been its cost transformation program, which has delivered over CHF 50 million in savings by the third quarter. The company has focused on digital initiatives and innovative shop formats to drive efficiency.

The breakdown of service revenues and cost savings impact is illustrated in this detailed analysis:

Swisscom has reinforced its multi-brand strategy in Switzerland, with the repositioning of Migros Mobile and new offerings to address different market segments. The company also highlighted its AI initiatives, including the launch of Swisscom myAI with a Pro version priced at CHF 14.90 per month, as part of its strategy to expand beyond core telecommunications services.

Network quality remains a priority, with Swisscom winning all connect tests in 2025 and targeting 90% coverage for its 5G+ network by year-end. The company continues its fiber-to-the-home (FTTH) rollout while managing capital expenditures carefully.

Italian Integration Progress

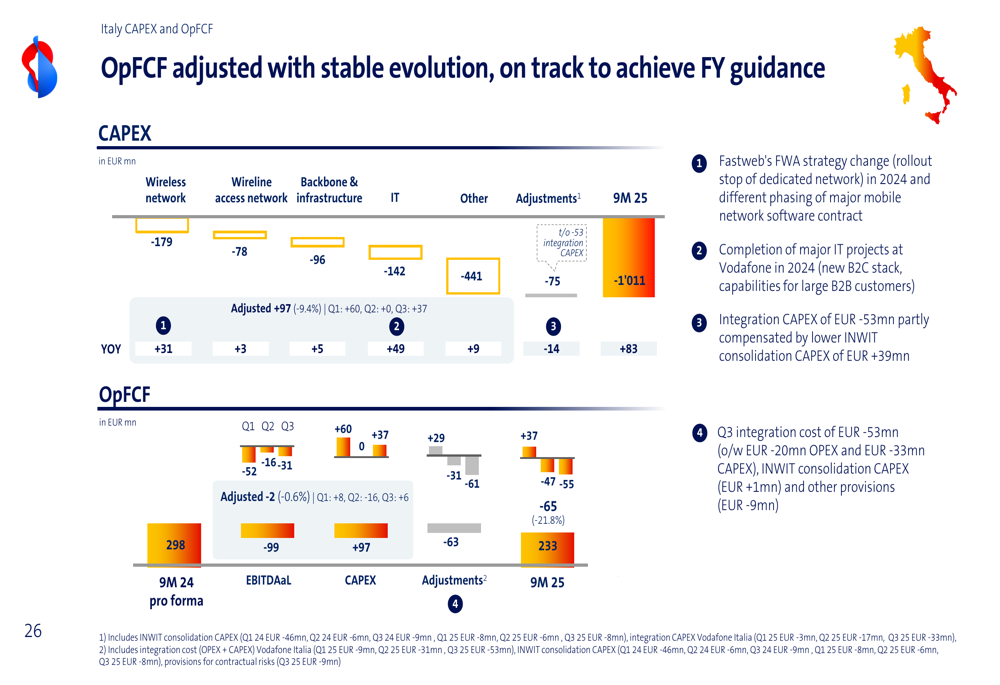

Swisscom provided updates on the integration of Fastweb and Vodafone Italia, reporting that the process is progressing as planned with synergy capture on track. The company has launched a joint mobile portfolio and new fixed offerings to stabilize the Italian business.

The following chart shows the stable operational free cash flow development, supported by the integration progress:

The company confirmed its integration cost and synergy targets for the full year, with EUR 36 million in synergies realized against a target of EUR 60 million. Network upgrades have been secured through new agreements, and the company is focused on aligning the go-to-market approach between Fastweb and Vodafone.

EBITDAaL Development and Adjustments

Swisscom’s EBITDAaL has been impacted by various factors, including service revenue decline and energy costs. The company provided a detailed breakdown of these adjustments:

As shown in the chart, the adjusted EBITDAaL has been primarily impacted by Telco service revenue decline, particularly in the Italian market. However, energy revenue growth has partially compensated for this decline, helping to stabilize overall performance.

Forward-Looking Statements

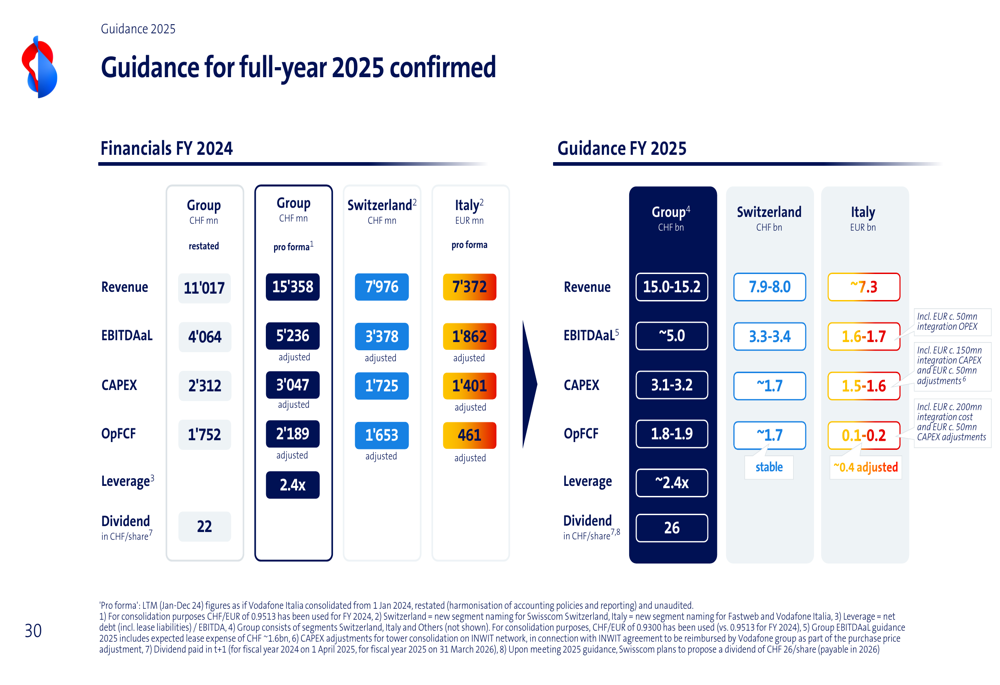

Swisscom confirmed its full-year 2025 guidance, targeting revenue of CHF 15.0-15.2 billion, EBITDAaL of approximately CHF 5.0 billion, capital expenditures of CHF 3.1-3.2 billion, and operational free cash flow of CHF 1.8-1.9 billion.

The guidance confirmation reflects the company’s confidence in its ability to navigate current market challenges:

Looking ahead, Swisscom aims to cement its leading position in Switzerland through managing telco top-line performance, executing cost transformation, and achieving profitable IT growth. In Italy, the focus remains on integrating Vodafone Italia, capturing synergies, stabilizing B2C telco revenue, and scaling up B2B IT and wholesale operations.

CEO Christoph Aeschlimann emphasized the company’s achievements in network quality and service excellence, noting that Swisscom is "pushing very heavily in providing AI consultancy and AI infrastructure services" as part of its strategy to expand beyond traditional telecommunications.

Despite the current revenue pressure, Swisscom’s stable operational free cash flow and confirmed guidance suggest the company is effectively managing its transition in a challenging market environment while investing in future growth areas like AI and network infrastructure.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.