Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Sylvamo Corporation (NYSE:SLVM) released its second quarter 2025 earnings presentation on August 8, 2025, revealing significant year-over-year declines in key financial metrics amid heavy planned maintenance outages. The market reacted negatively to the results, with the stock plunging 15.34% in premarket trading to $40.50, adding to recent pressure that has seen shares approach their 52-week low of $44.49.

The presentation comes after a disappointing first quarter where the company missed EPS forecasts by 34%, and continues to highlight operational challenges facing "The World’s Paper Company" as it navigates industry headwinds and executes necessary maintenance work.

Quarterly Performance Highlights

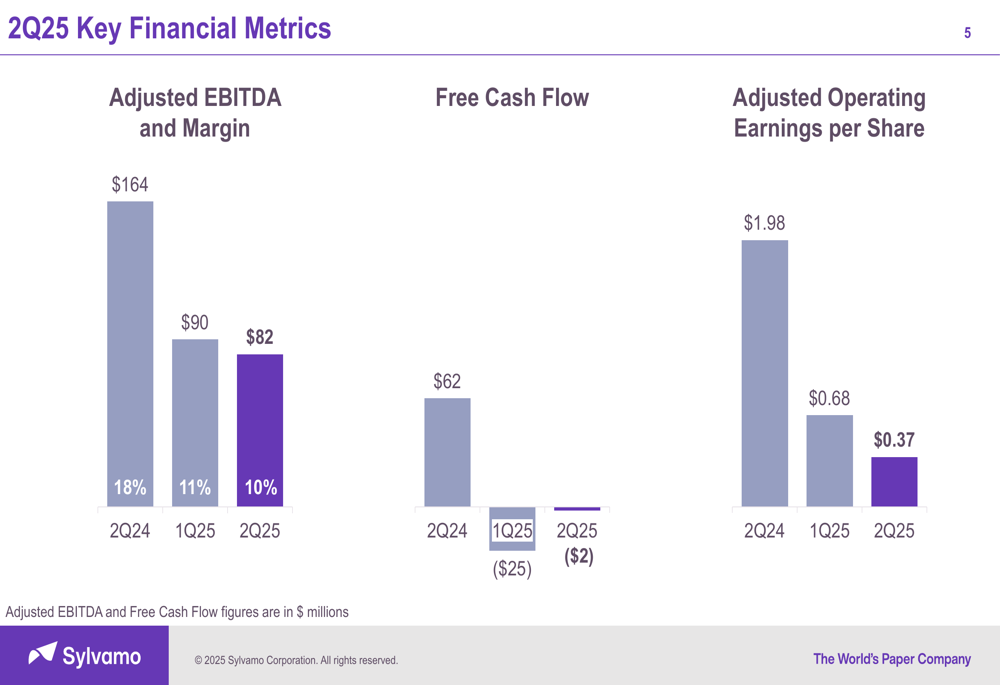

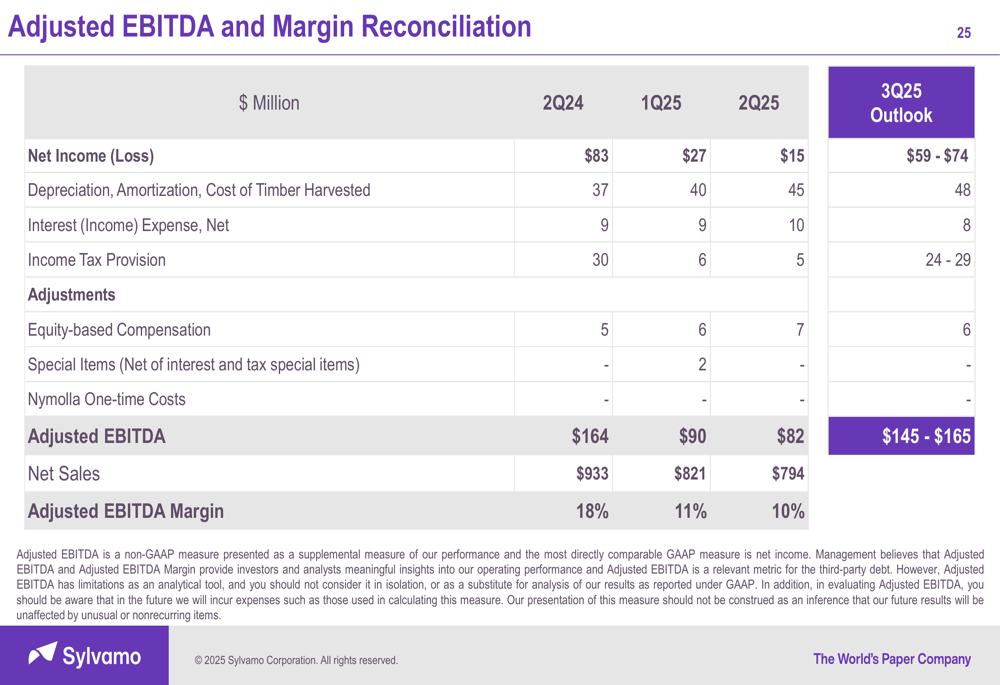

Sylvamo reported second quarter 2025 Adjusted EBITDA of $82 million with a 10% margin, representing a significant decline from $164 million (18% margin) in the same period last year. Adjusted operating earnings per share fell to $0.37, compared to $1.98 in Q2 2024.

As shown in the following chart of quarterly financial metrics, the company has experienced a consistent downward trend in profitability metrics since last year:

Free cash flow was negative $2 million for the quarter, a slight improvement from negative $25 million in Q1 2025, but substantially below the positive $62 million generated in Q2 2024. The company highlighted that it returned $38 million in cash to shareholders despite these challenges.

Detailed Financial Analysis

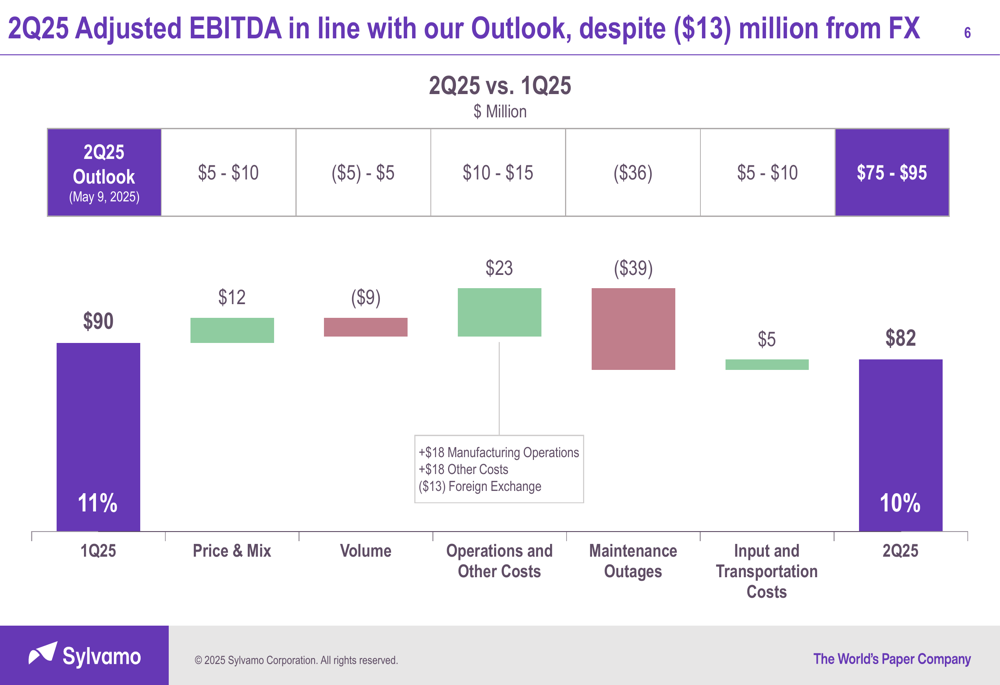

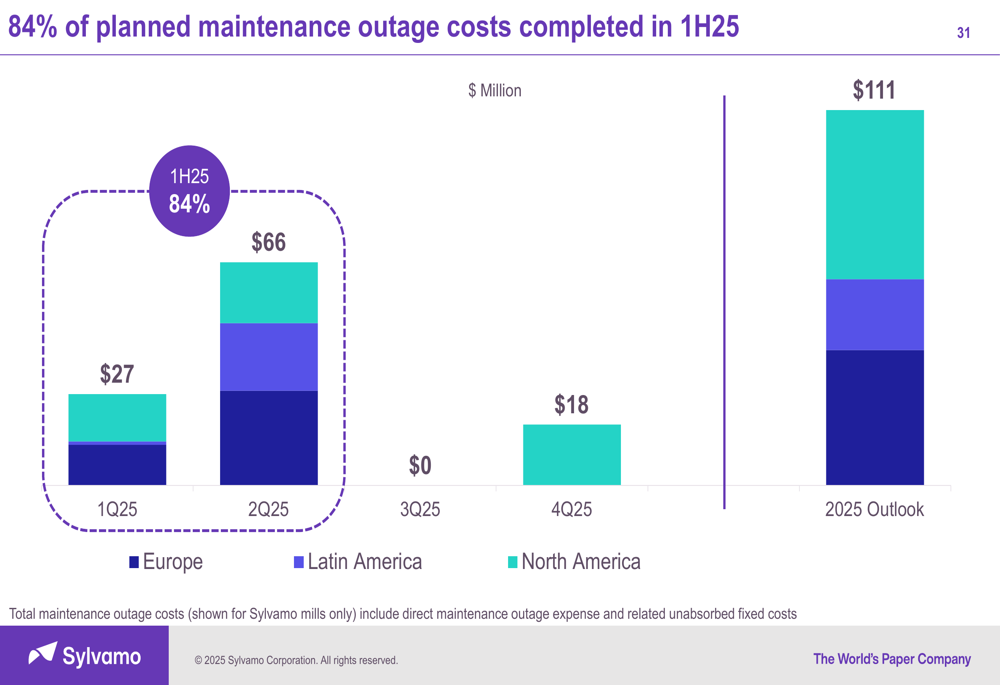

The primary factor impacting Q2 2025 results was the execution of planned maintenance outages, which cost the company $66 million during the quarter. This represents the heaviest planned maintenance quarter for the year, with 84% of annual maintenance costs now completed in the first half of 2025.

The following bridge analysis illustrates how various factors affected Adjusted EBITDA performance from Q1 to Q2:

Positive contributors included price and mix improvements ($12 million) and better operations and other costs ($23 million), which were offset by volume declines ($9 million) and the significant maintenance outage expenses ($39 million). The company noted that manufacturing operations improved by $18 million and other costs improved by $18 million, though these gains were partially offset by negative foreign exchange impacts of $13 million.

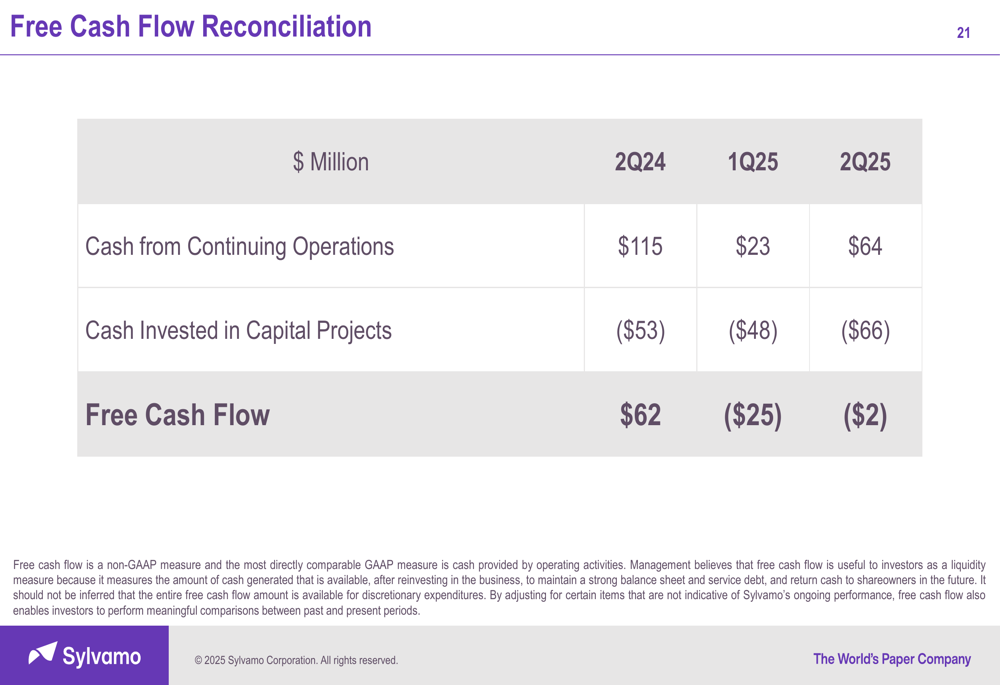

The free cash flow reconciliation shows how operating cash flow of $64 million was offset by capital expenditures of $66 million:

Strategic Initiatives

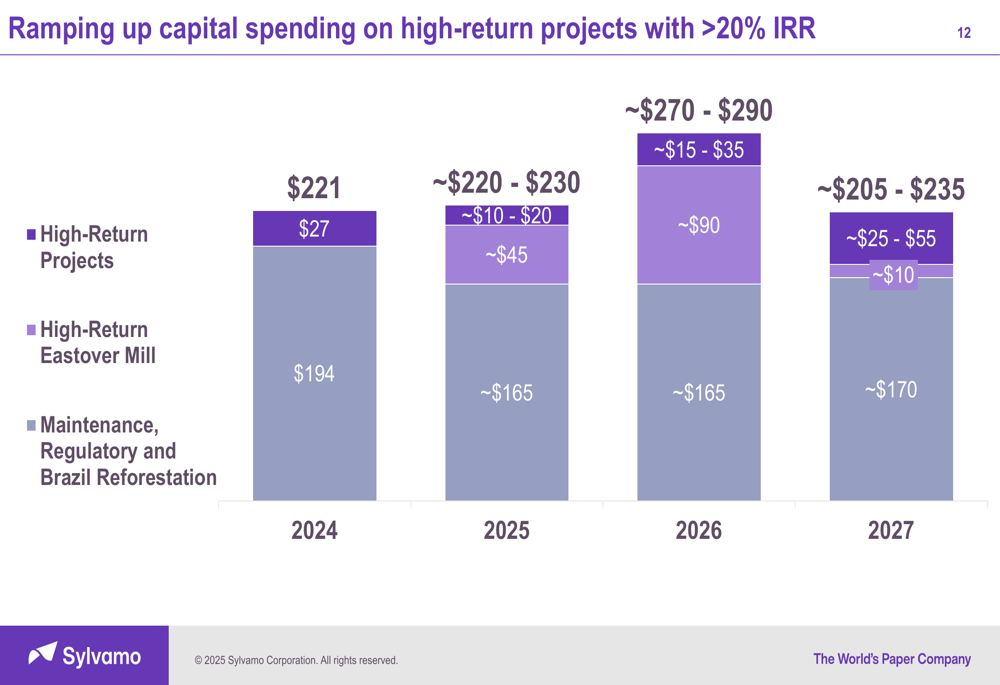

Despite current earnings pressure, Sylvamo outlined an ambitious capital spending plan focused on high-return projects with expected IRRs exceeding 20%. The company plans to increase capital expenditures from $221 million in 2024 to approximately $220-230 million in 2025, with further increases to $270-290 million in 2026.

As illustrated in the following chart, this capital allocation strategy balances maintenance and regulatory requirements with strategic investments:

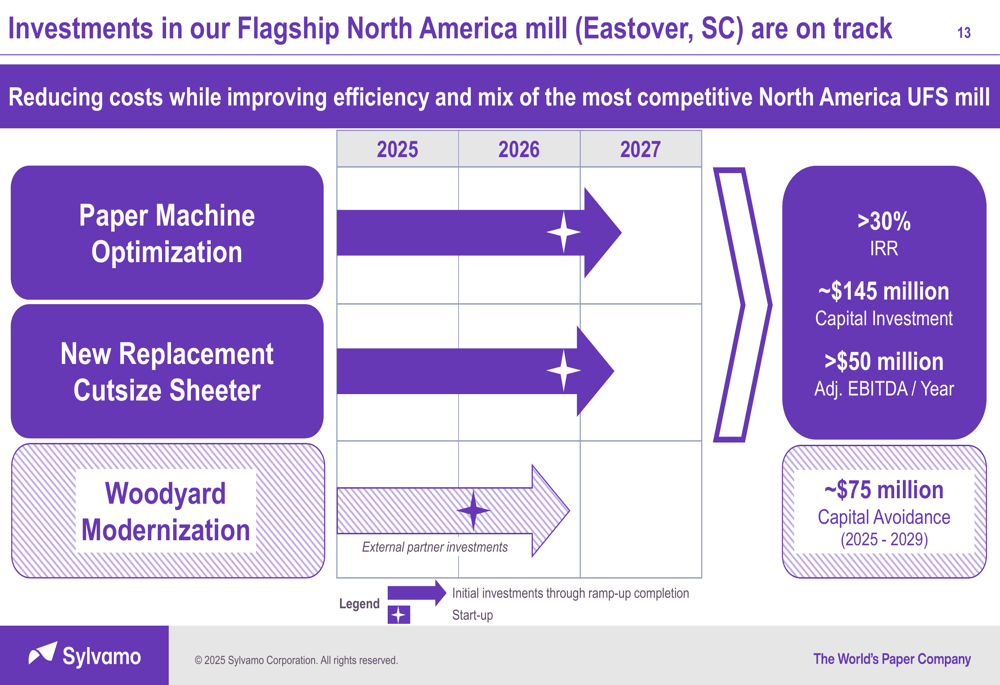

A centerpiece of this investment strategy is the company’s flagship North America mill in Eastover, South Carolina. The presentation detailed a $145 million capital investment in paper machine optimization expected to generate over $50 million in annual Adjusted EBITDA:

Sylvamo also emphasized its strengthened financial position, having reduced gross debt from $1.5 billion at spinoff to $0.8 billion as of June 2025. The company reported a net debt-to-adjusted EBITDA ratio of 1.3x and a gross debt-to-adjusted EBITDA ratio of 1.5x as of June 30, 2025.

Forward-Looking Statements

The most encouraging aspect of the presentation was Sylvamo’s outlook for the third quarter of 2025. The company projects Q3 Adjusted EBITDA to reach between $145 million and $165 million, representing a substantial improvement from Q2’s $82 million.

This expected improvement is driven by several factors:

- Favorable volume trends ($15-20 million) due to stronger seasonality in Latin America and North America

- Favorable operations and other costs ($0-5 million)

- Stable input and transportation costs (-$5 to $5 million)

- Significantly lower planned maintenance outage expenses ($66 million improvement)

These positive factors are expected to be partially offset by unfavorable price and mix (-$15 to -$20 million), primarily due to paper and pulp prices in Europe.

The detailed reconciliation of expected Q3 2025 Adjusted EBITDA shows the components contributing to the projected improvement:

Industry Position

The presentation addressed industry dynamics affecting Sylvamo’s performance, noting that uncoated freesheet supply has decreased by 7% in Europe and 10% in North America in the first half of 2025 compared to the same period in 2024. Demand has also declined, particularly in Europe (8%) and Latin America (2%), though Brazil showed positive demand growth of 6%.

The company also highlighted uncertainty related to U.S. tariffs, which could impact global trade flows, currency fluctuations, inflation, and economic activity. Despite these challenges, management emphasized its long-term strategy remains intact, focusing on uncoated freesheet paper, investing to strengthen competitive advantages, and leveraging strengths to drive high returns on invested capital.

Sylvamo’s maintenance outage costs for 2025 are expected to total $111 million, with the majority already incurred in the first half of the year:

While the Q2 2025 results reflect significant challenges, the company’s projected improvement in the second half of the year and strategic investments suggest management is positioning Sylvamo for longer-term recovery. Investors will be watching closely to see if the anticipated Q3 rebound materializes as projected.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.