Asia FX dithers as dollar steadies before Powell speech; yen muted after CPI data

Introduction & Market Context

Synaptics Incorporated (NASDAQ:SYNA) delivered strong fourth-quarter and full-year fiscal 2025 results, according to the company’s earnings presentation released on August 7, 2025. The semiconductor solutions provider reported double-digit revenue growth driven primarily by its rapidly expanding Core IoT segment, while continuing to advance its artificial intelligence capabilities.

The company’s performance comes amid increasing demand for high-performance semiconductor solutions across smart home, enterprise, and automotive applications. Synaptics has positioned itself at the intersection of several growth markets, leveraging its expertise in analog mixed-signal, multi-core processors, and wireless connectivity.

Quarterly Performance Highlights

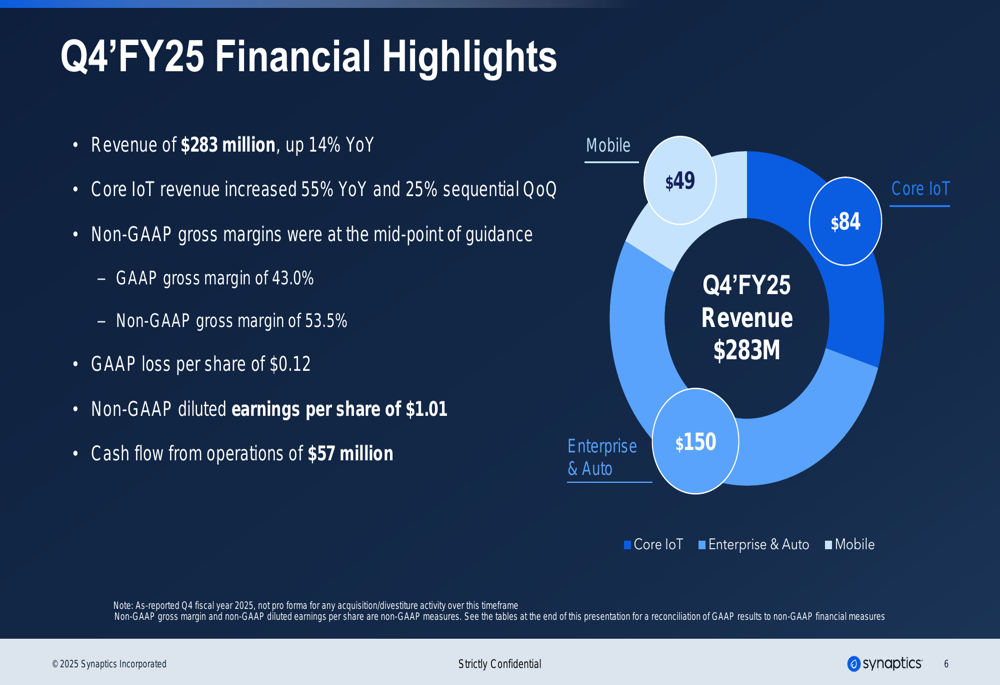

Synaptics reported Q4 FY2025 revenue of $282.8 million, representing a 14% year-over-year increase and a 6% sequential improvement from the previous quarter. The company’s Core IoT segment was the standout performer, growing 55% year-over-year and 25% quarter-over-quarter.

The quarterly revenue breakdown shows Enterprise & Automotive remains the largest segment at $150 million (53%), followed by Core IoT at $84 million (30%), and Mobile at $49 million (17%). This represents a significant shift in the company’s revenue mix, with Core IoT increasing from 22% of total revenue in Q4 FY2024 to 30% in Q4 FY2025.

As shown in the following revenue breakdown chart:

Non-GAAP gross margin held steady at 53.5%, in line with the previous quarter and slightly above the 53.4% reported in Q4 FY2024. The company’s Non-GAAP operating margin improved to 16.5%, up 208 basis points year-over-year and 95 basis points sequentially.

Non-GAAP diluted earnings per share reached $1.01, marking a substantial 58% increase from $0.64 in the same quarter last year and a 12% improvement from $0.90 in Q3 FY2025. This performance exceeded analyst expectations, as the previous quarter’s earnings call had forecasted EPS around $0.90.

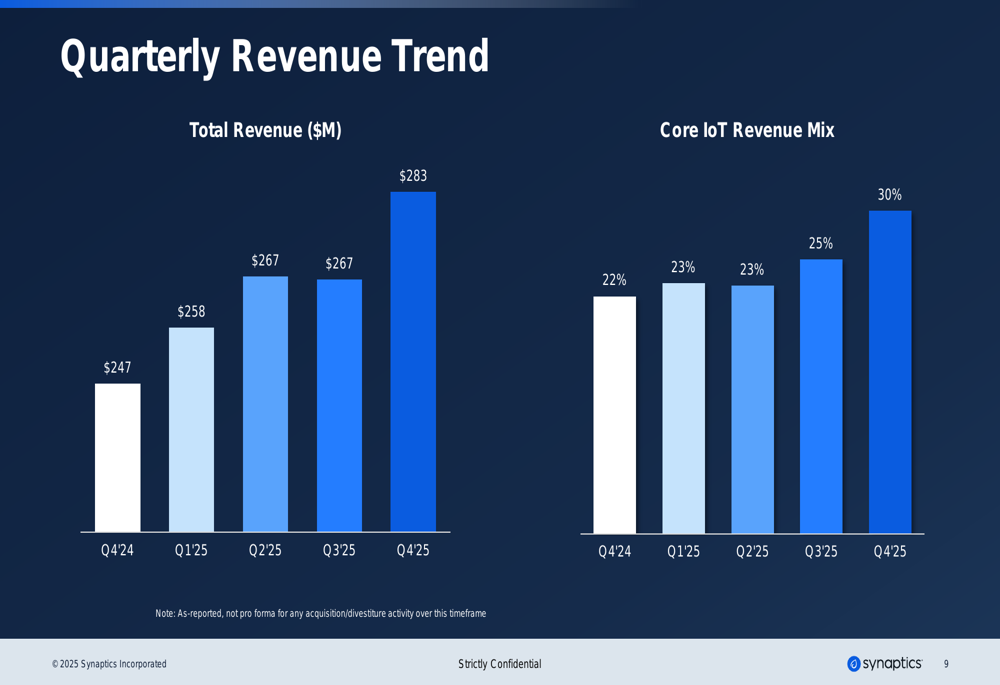

The quarterly revenue trend illustrates Synaptics’ consistent growth trajectory throughout fiscal 2025:

Full-Year Results

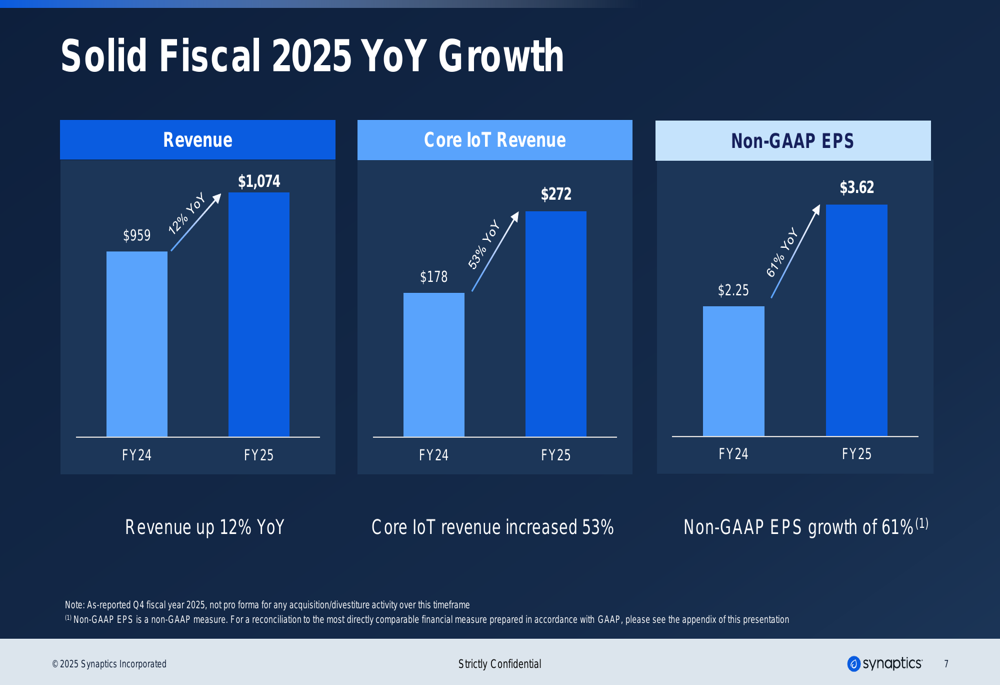

For the full fiscal year 2025, Synaptics achieved total revenue of $1.074 billion, up 12% from $959.4 million in FY2024. Core IoT revenue grew an impressive 53% year-over-year, underscoring the company’s successful pivot toward this high-growth segment.

The company’s annual financial performance shows significant improvement across key metrics, as illustrated in the following comparison:

Non-GAAP gross margin for FY2025 improved to 53.6%, up 60 basis points from 53.0% in FY2024. Non-GAAP operating margin expanded substantially to 16.5%, a 310 basis point improvement from 13.4% in the previous year. This margin expansion, coupled with revenue growth, drove a 61% increase in Non-GAAP diluted EPS to $3.62, compared to $2.25 in FY2024.

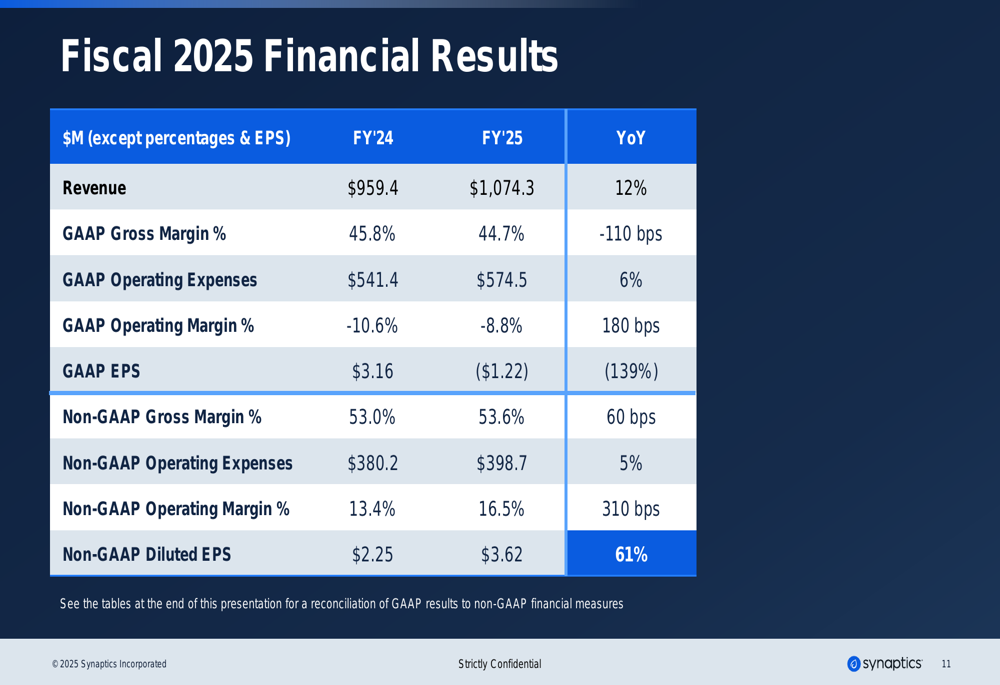

The comprehensive financial results for fiscal 2025 compared to 2024 show improvements across most metrics:

Strategic Initiatives

During Q4, Synaptics made significant progress on its strategic initiatives, particularly in advancing its artificial intelligence capabilities. The company announced it had taped out its first ground-up Astra SoC (System on Chip) solution featuring a neural processor for AI inference, marking an important milestone in its AI development roadmap.

Additionally, Synaptics secured a marquee Astra processor design win with a leading audio OEM, validating its technology leadership in this space. The company also reported that its Wi-Fi 7 design pipeline continues to grow at a solid pace, positioning it well for future growth in wireless connectivity solutions.

The company’s technology leadership spans multiple product categories and applications, as shown in this portfolio overview:

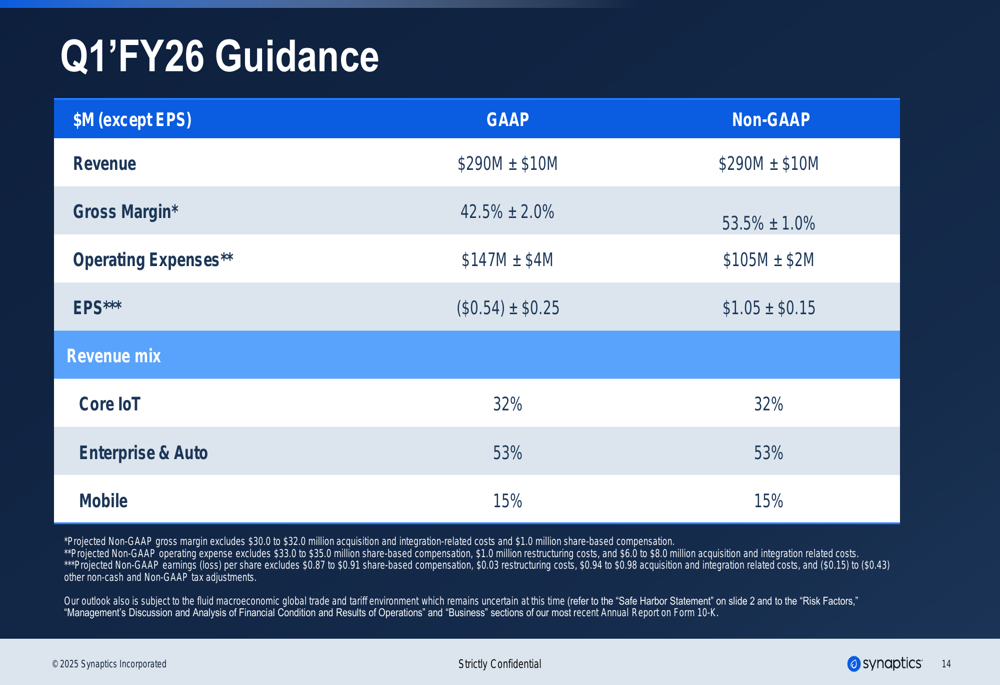

Forward Guidance

Looking ahead to the first quarter of fiscal 2026, Synaptics provided positive guidance, projecting revenue of $290 million (±$10 million), which represents continued sequential growth from Q4 FY2025. The company expects Non-GAAP gross margin to remain stable at 53.5% (±1.0%) and forecasts Non-GAAP EPS of $1.05 (±$0.15), suggesting continued earnings growth.

The Q1 FY2026 revenue mix is expected to consist of 32% from Core IoT, 53% from Enterprise & Auto, and 15% from Mobile, indicating further expansion of the Core IoT segment’s contribution to overall revenue.

The detailed guidance for the upcoming quarter is presented below:

Balance Sheet and Cash Flow

Synaptics ended fiscal 2025 with $452.5 million in cash and short-term investments, up from $421.4 million in the previous quarter but down from $876.9 million a year ago. The year-over-year reduction in cash reserves likely reflects the company’s share repurchase activities, which included $128 million in buybacks during the previous quarter as mentioned in their Q3 earnings report.

Total (EPA:TTEF) debt stood at $834.8 million, relatively unchanged from the previous quarter but down from $972.9 million in Q4 FY2024, indicating progress in deleveraging. The company generated $57 million in cash flow from operations during the fourth quarter, demonstrating solid cash generation capabilities.

Inventory levels increased to $139.5 million from $132.9 million in the previous quarter and $114.0 million a year ago, potentially reflecting preparations for anticipated growth or supply chain adjustments.

Market Reaction

Following the release of the Q4 results, Synaptics’ stock showed minimal movement in after-hours trading, with the price at $59.70. The stock had closed the regular trading session at $59.70, down 0.67% for the day. This relatively muted reaction came despite the strong quarterly results, suggesting that positive performance may have already been priced into the stock following the company’s previous guidance.

According to the most recent data, Synaptics’ stock has traded between $41.80 and $89.81 over the past 52 weeks, indicating significant volatility. The current price positions the stock near the middle of this range, potentially reflecting a balanced market assessment of the company’s growth prospects and competitive challenges in the semiconductor industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.