Trump to appeal tariff ruling, warns of economic consequences

Introduction & Market Context

Synchrony Financial (NYSE:SYF) released its first quarter 2025 financial results on April 22, showing mixed performance with modest growth in key operational metrics but significant declines in earnings and revenue. The company’s stock responded positively in pre-market trading, rising 3.3% to $48.79, suggesting investors may have anticipated worse results or were encouraged by the company’s outlook.

The credit card issuer and consumer financial services company reported growth in active accounts, purchase volume, and loan receivables, but faced substantial pressure on earnings per share and net revenue compared to the same period last year. This performance comes after Synchrony reported stronger results in Q4 2024, when it posted earnings per share of $1.91, slightly above analyst expectations.

Quarterly Performance Highlights

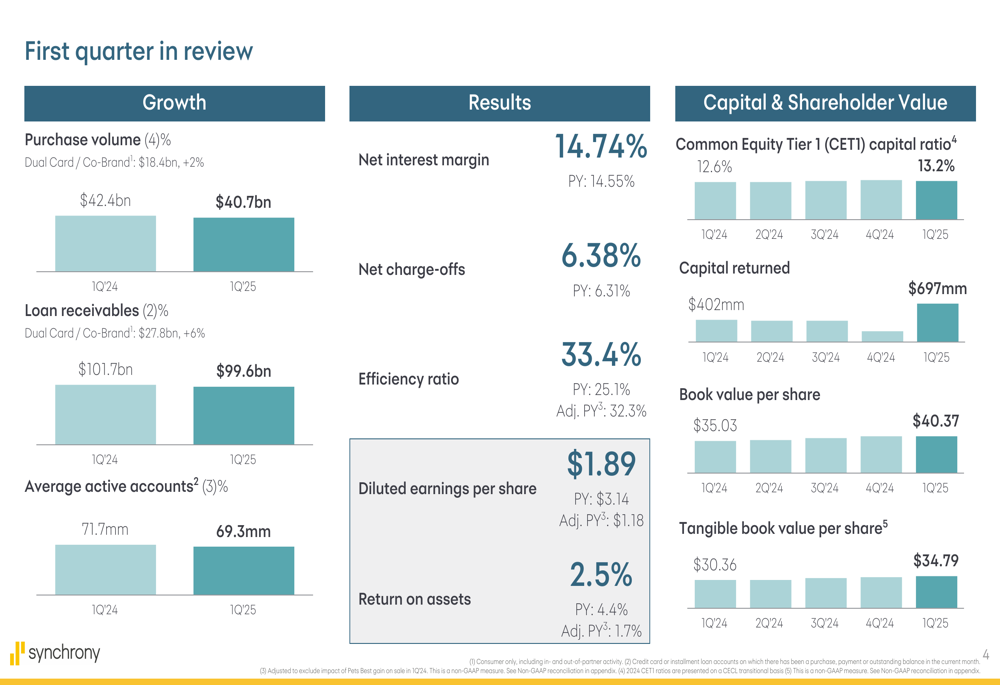

Synchrony reported modest growth in its core operational metrics for Q1 2025. Average active accounts increased by 3% year-over-year to 69 million, while purchase volume grew 4% to $41 billion and loan receivables expanded 2% to $100 billion.

As shown in the following chart of Synchrony’s first quarter performance metrics:

However, the company’s financial results showed significant pressure on profitability. Diluted earnings per share fell 40% year-over-year to $1.89, while return on assets was 2.5%. The efficiency ratio remained well-controlled at 33.4%, indicating the company is managing its expenses effectively despite revenue challenges.

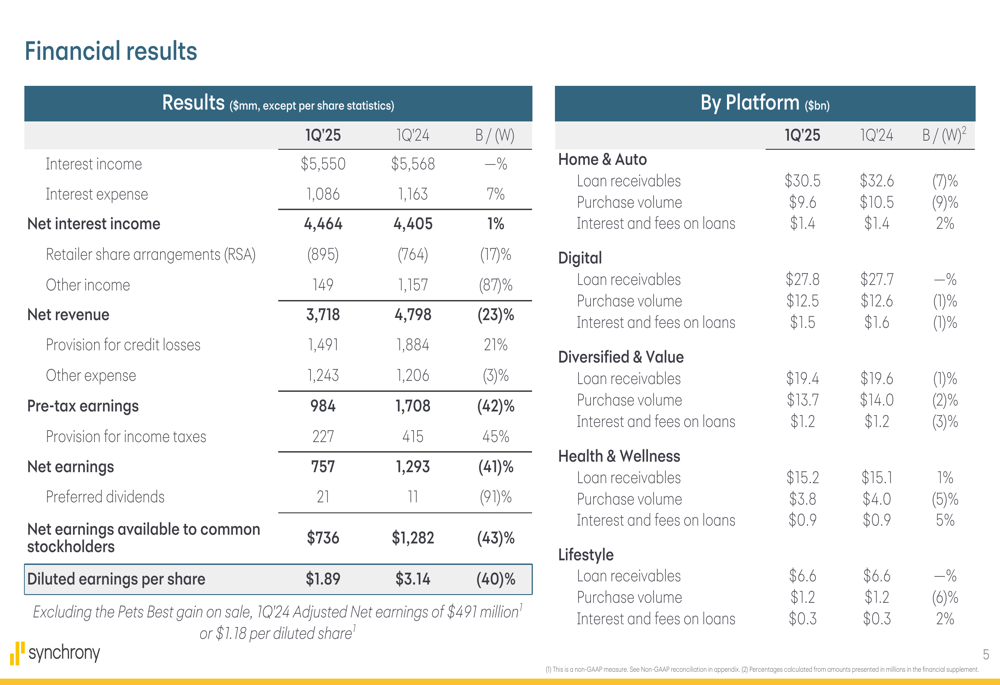

Net revenue decreased substantially by 23% from $4,798 million to $3,718 million. This decline was primarily driven by an 87% decrease in other income to $149 million, partially offset by a 1% increase in net interest income to $4,464 million. Retailer share arrangements increased 17% to $(895) million.

The detailed breakdown of financial results by platform and category is illustrated in this comprehensive table:

Credit Trends and Risk Management

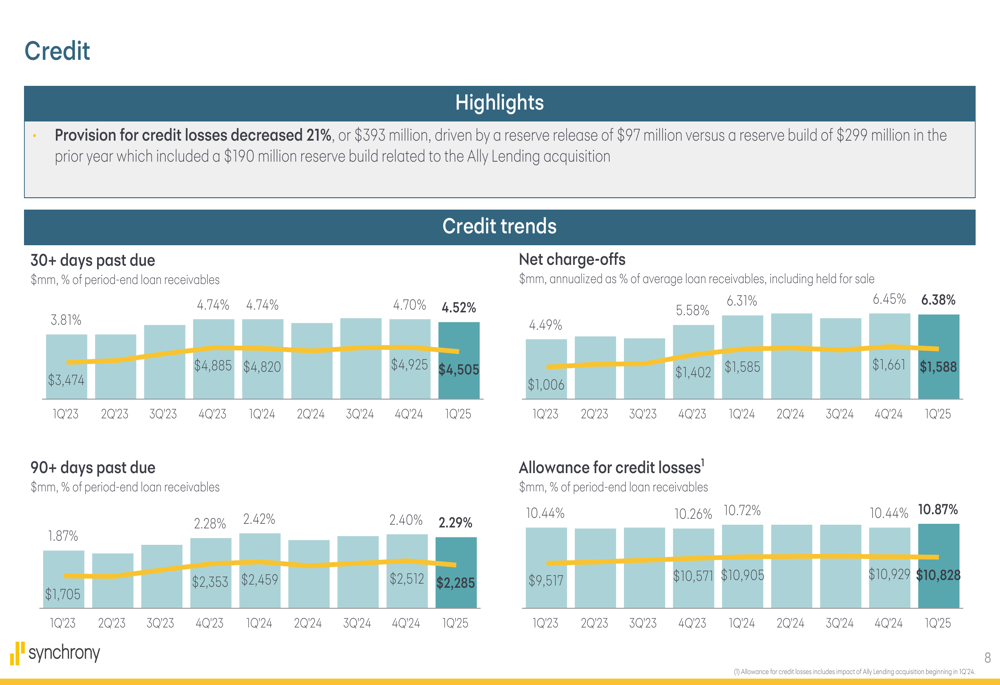

Synchrony’s credit metrics showed continued pressure in Q1 2025, with delinquency rates and net charge-offs increasing year-over-year. The 30+ days past due rate rose from 3.81% to 4.52%, while the 90+ days past due rate increased from 1.87% to 2.29%. Net charge-offs climbed significantly from 4.49% to 6.38%.

Despite these increases in delinquencies and charge-offs, the provision for credit losses decreased by 21% or $393 million, reflecting the company’s confidence in its credit management strategies and possibly improved outlook on future credit performance.

The following chart illustrates these credit trends:

The company’s allowance for credit losses as a percentage of loan receivables increased from 10.44% to 10.87%, providing additional cushion against potential future losses. This conservative approach to credit risk management aligns with the company’s focus on maintaining a strong balance sheet through economic cycles.

Strategic Initiatives

Synchrony continued to expand its partnership network in Q1 2025, securing new and renewed partnerships with retailers including Ashley, American Eagle (NYSE:AEO), Aerie, Discount Tire, and Sun Country Airlines. These partnerships are crucial to Synchrony’s business model, driving account growth and purchase volume.

The company also highlighted its recognition as the #2 Best Company to work for in the U.S., which strengthens its employer brand and ability to attract talent.

Synchrony’s customer engagement metrics and sales trends are illustrated in the following slide:

The company’s sales data reveals interesting demographic trends, with Millennial and Gen Z consumers accounting for 39-41% of sales, Gen X representing 34-35%, and Baby Boomers and older generations making up 25-26%. This relatively balanced generational mix suggests Synchrony is successfully engaging consumers across age groups.

Capital Position and Shareholder Returns

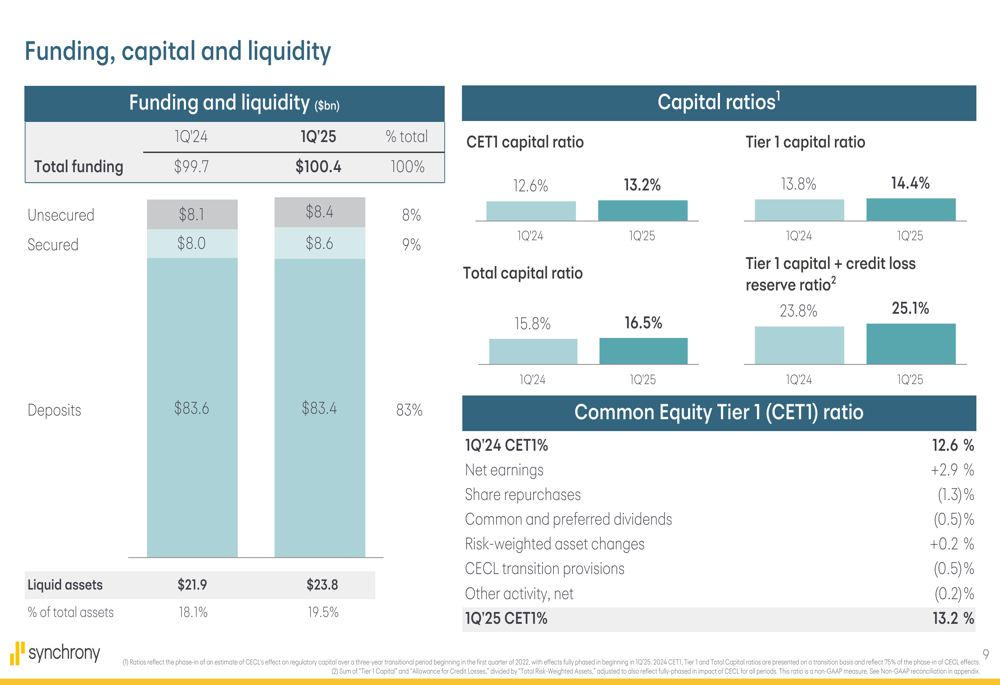

Synchrony maintained a strong capital position in Q1 2025, with a Common Equity Tier 1 (CET1) capital ratio of 13.2%. The company returned $697 million to shareholders during the quarter, demonstrating its commitment to shareholder value.

Book value per share stood at $40.37, while tangible book value per share was $34.79. These metrics provide a solid foundation for future growth and capital returns.

The following chart details Synchrony’s funding, capital, and liquidity position:

Total (EPA:TTEF) funding increased slightly from $99.7 billion to $100.4 billion, with deposits representing the largest component at $83.4 billion. Liquid assets totaled $23.8 billion, accounting for 19.5% of total assets and providing ample liquidity for operational needs and growth opportunities.

Forward-Looking Statements

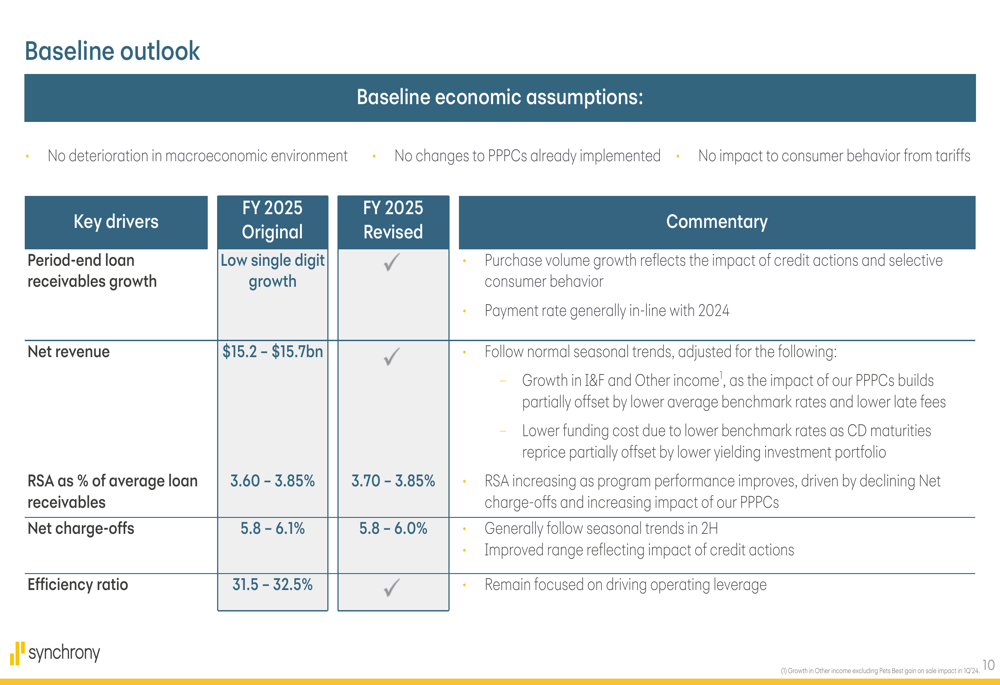

Synchrony provided a baseline outlook for fiscal year 2025, projecting low single-digit growth in loan receivables. Net revenue is expected to be between $15.2 billion and $15.7 billion, while net charge-offs are anticipated to range between 5.8% and 6.0%, slightly below the 6.38% reported in Q1 2025.

The company expects its efficiency ratio to be between 31.5% and 32.5%, suggesting continued focus on cost management. These projections assume no deterioration in the macroeconomic environment and no significant changes to consumer behavior from tariffs.

The detailed baseline outlook and key drivers are presented in this slide:

This guidance suggests that Synchrony expects some improvement in credit metrics throughout the year, with charge-offs potentially moderating from current levels. The company’s outlook aligns with its previous statements about maintaining disciplined growth while managing credit risk effectively.

Conclusion

Synchrony Financial’s Q1 2025 results present a mixed picture, with operational growth in accounts, purchase volume, and loan receivables offset by significant declines in earnings and revenue. The company faces continued pressure on credit metrics but has maintained a strong capital position and returned substantial capital to shareholders.

Looking ahead, Synchrony’s baseline outlook for FY 2025 suggests modest growth and potential improvement in credit performance. The company’s strategic partnerships and customer engagement metrics provide a foundation for future growth, though challenges remain in navigating the current credit environment.

Investors will likely focus on whether Synchrony can achieve its projected improvement in charge-off rates and maintain its efficiency targets while returning to earnings growth in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.