Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

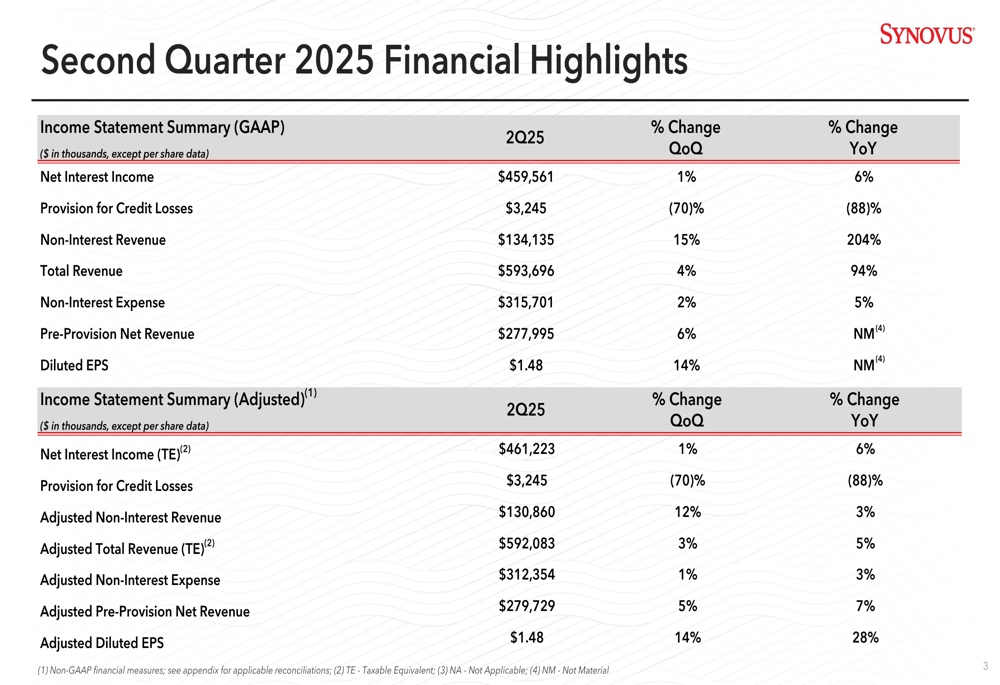

Synovus Financial Corp (NYSE:SNV) reported strong second-quarter 2025 results on July 17, showcasing improved profitability metrics and raising its full-year guidance. The regional bank, which has seen its stock rise to $52.87, delivered diluted earnings per share of $1.48, representing a 14% increase from the previous quarter and continuing its momentum from Q1’s earnings beat.

Quarterly Performance Highlights

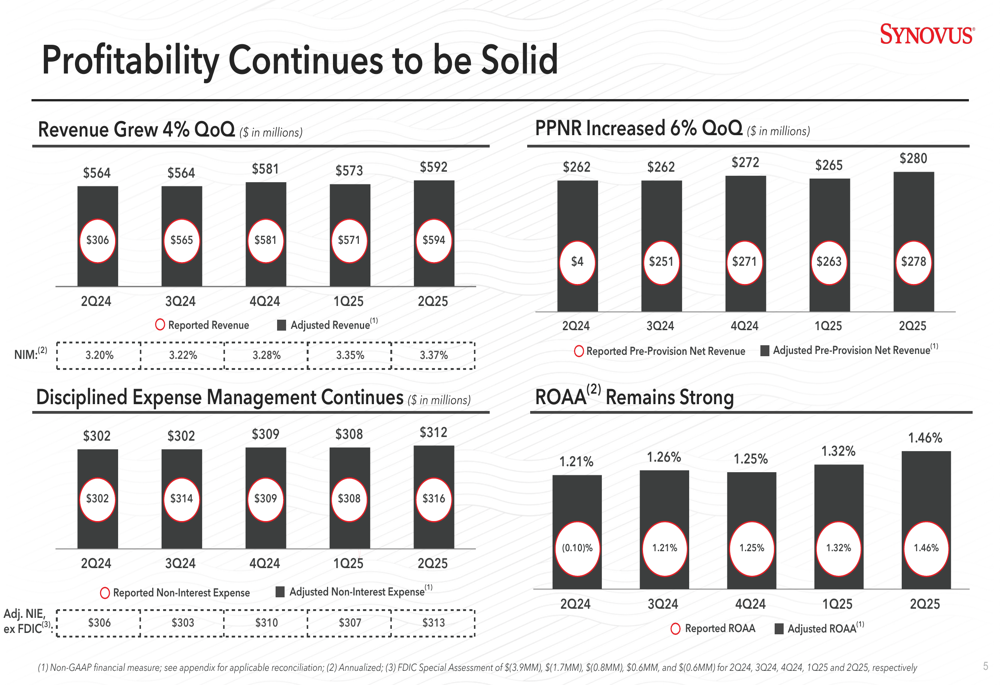

Synovus demonstrated solid financial performance across key metrics in Q2 2025. The company reported total revenue of $593.7 million, up 4% quarter-over-quarter and 94% year-over-year. Adjusted pre-provision net revenue reached $279.7 million, increasing 5% from the previous quarter and 7% from the same period last year.

As shown in the following financial highlights chart, the bank’s profitability metrics improved significantly:

Return on average assets (ROAA) strengthened to 1.46%, up from 1.32% in Q1 2025 and a substantial improvement from -0.10% in Q2 2024. The company’s net interest margin also expanded to 3.37%, compared to 3.35% in the previous quarter and 3.20% in the year-ago period.

The following chart illustrates Synovus’ consistent profitability improvement across key metrics:

"We enter this environment in a position of strength," CEO Kevin Blair had stated during the previous quarter’s earnings call, a sentiment that appears validated by these Q2 results.

Detailed Financial Analysis

Balance Sheet and Credit Quality

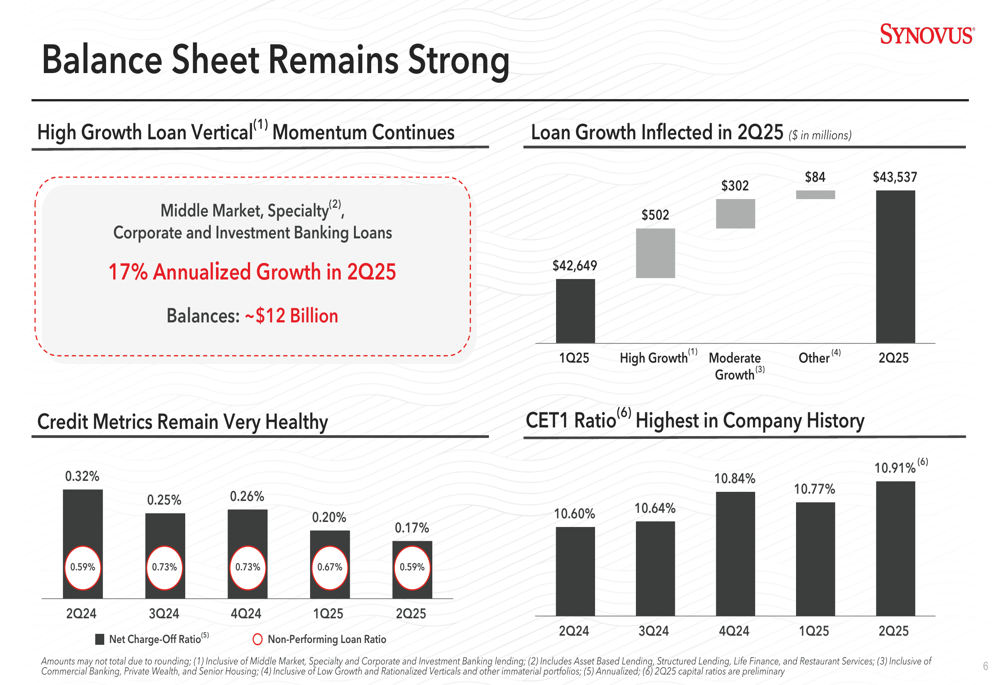

Synovus’ loan portfolio grew to $43.5 billion, representing a 2% increase quarter-over-quarter and 1% year-over-year. The growth was primarily driven by the bank’s high-growth loan verticals, which expanded at a 17% annualized rate in Q2.

The following chart shows the strength of Synovus’ balance sheet, including improving credit metrics and capital position:

Credit quality metrics showed notable improvement, with net charge-offs declining to 0.17% of average loans, down from 0.20% in Q1 2025 and 0.32% in Q2 2024. Non-performing loans as a percentage of total loans decreased to 0.59% from 0.67% in the previous quarter.

The company’s allowance for credit losses declined slightly to 1.18% of loans, compared to 1.24% in Q1 2025, reflecting the improved credit environment partially offset by a more adverse economic outlook.

Revenue Components

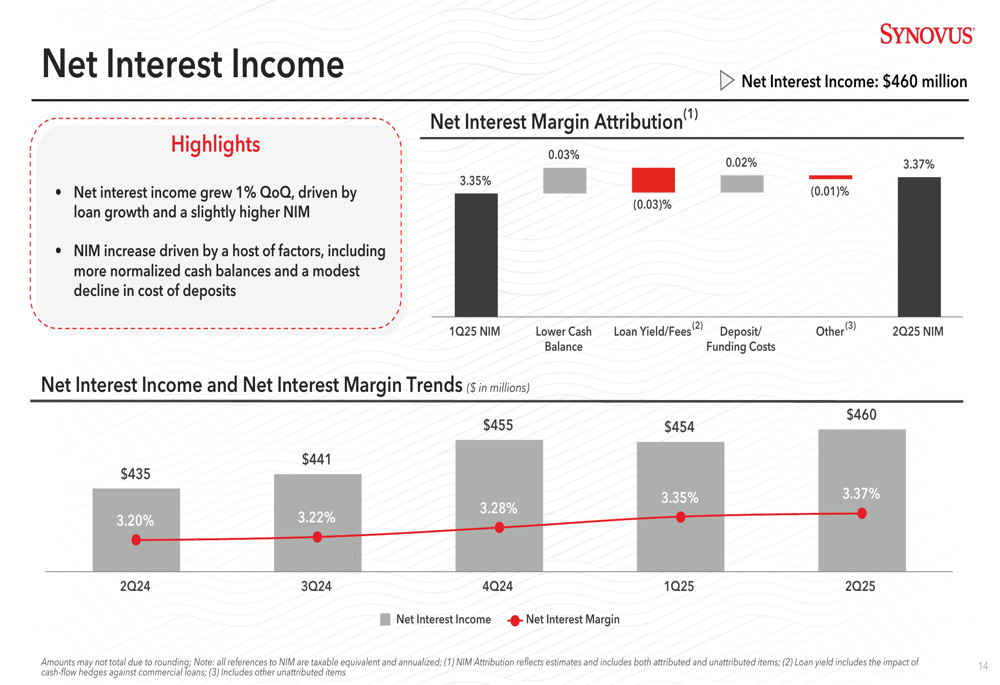

Net interest income grew to $460 million, up 1% quarter-over-quarter and 6% year-over-year, driven by loan growth and a slight improvement in net interest margin.

As illustrated in the following chart, net interest income has shown consistent growth over the past year:

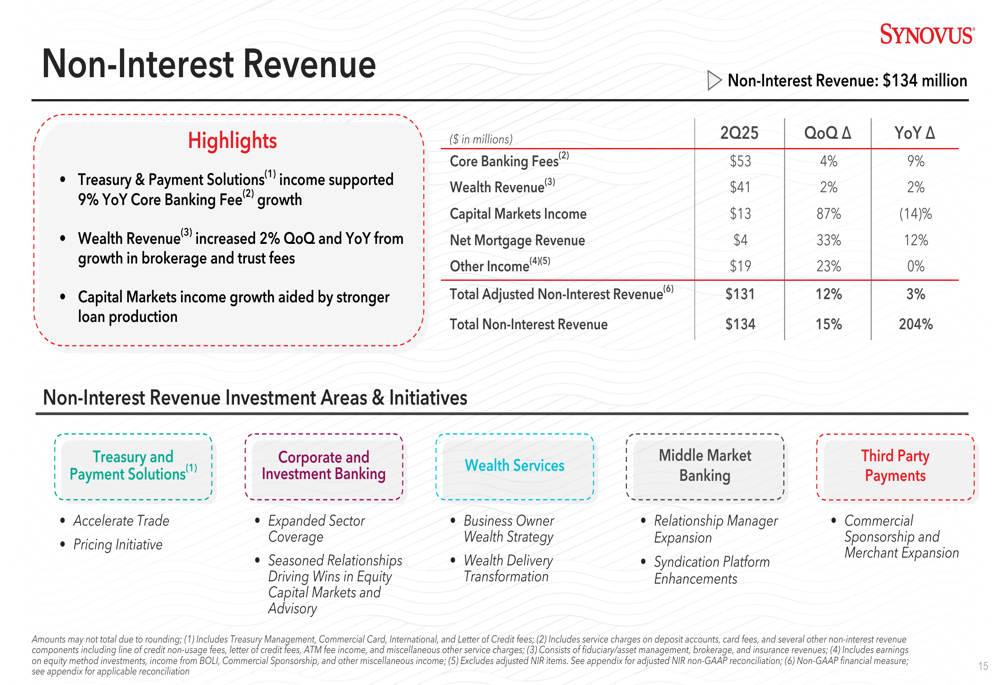

Non-interest revenue reached $134 million, increasing 15% from the previous quarter and 204% year-over-year. The bank’s Treasury & Payment Solutions income supported 9% year-over-year growth in core banking fees, while wealth revenue increased 2% both quarter-over-quarter and year-over-year.

The following chart breaks down the non-interest revenue components:

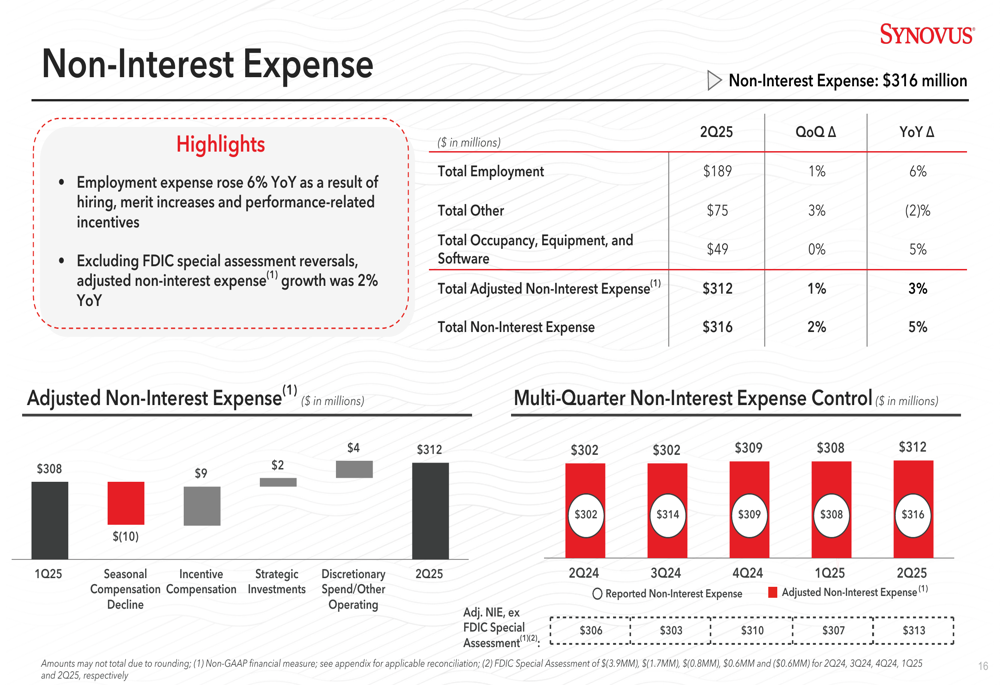

Non-interest expense was $316 million, up 2% quarter-over-quarter and 5% year-over-year. Employment expenses rose 6% year-over-year due to hiring, merit increases, and performance-related incentives.

Capital Position

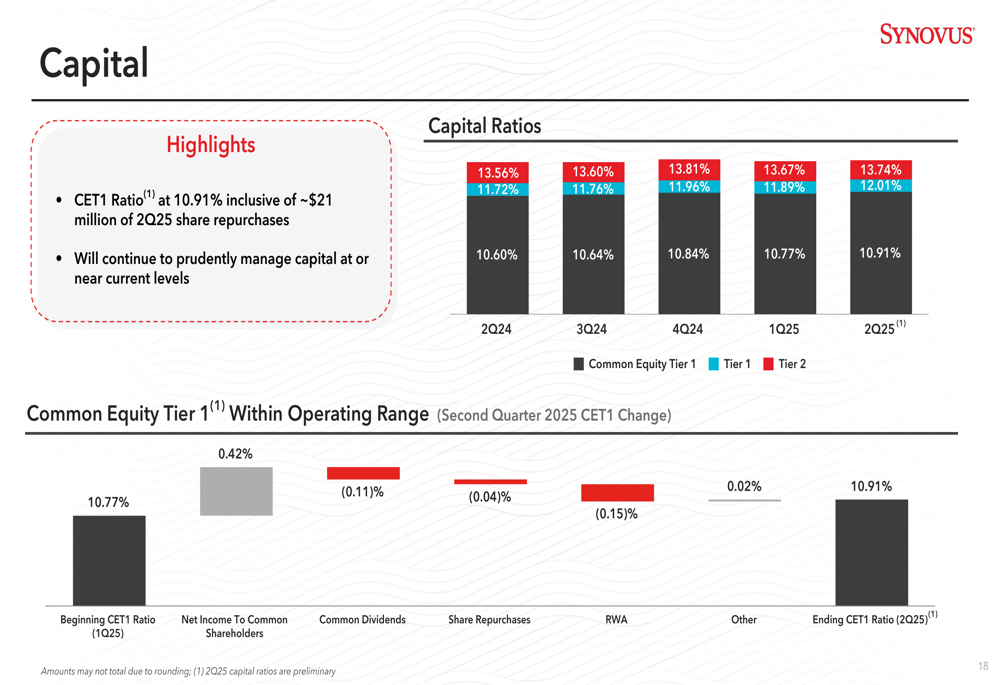

Synovus’ capital position strengthened further in Q2 2025, with the Common Equity Tier 1 (CET1) ratio reaching 10.91%, up from 10.77% in Q1 2025 and 10.60% in Q2 2024. This represents the highest CET1 ratio in the company’s history, providing additional flexibility for potential growth opportunities.

Strategic Initiatives

Synovus outlined three main strategic initiatives for 2025 that remain on track:

1. Winning in the Southeast: The bank continues to focus on relationship manager hiring in middle market, commercial, and wealth services, while expanding structured lending teams and deepening corporate and investment banking offerings.

2. Maintaining Top Quartile Profitability: Through disciplined expense management, conservative balance sheet management, and leveraging a more robust product set including treasury and payment solutions and capital markets.

3. Targeting Sustainable Returns: By maintaining strong credit metrics, exercising prudent interest rate risk management, enhancing risk frameworks, and continuing key technology investments.

The company’s client-focused approach appears to be yielding results, as evidenced by its strong performance in the J.D. Power 2025 U.S. Retail Banking Satisfaction Study, where Synovus ranked #6 in Net Promoter Score among the top 50 asset banks.

Forward-Looking Statements

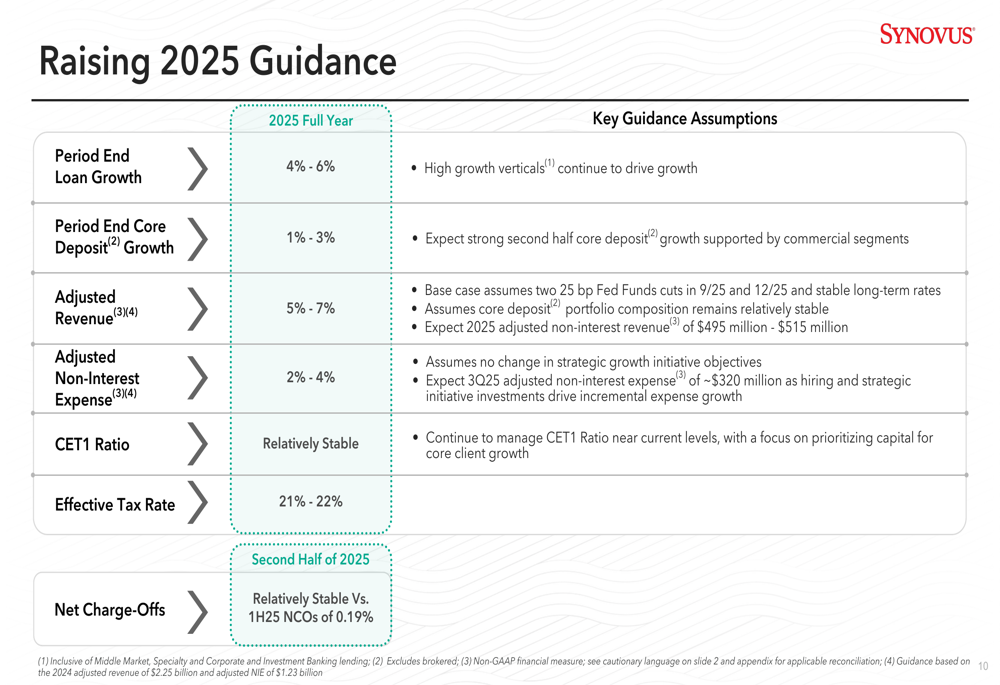

Based on its strong first-half performance, Synovus has raised its full-year 2025 guidance:

The bank now expects:

- Period-end loan growth of 4-6%

- Period-end core deposit growth of 1-3%

- Adjusted revenue growth of 5-7%

- Adjusted non-interest expense growth of 2-4%

- Relatively stable CET1 ratio

- Net charge-offs in the second half of 2025 to remain relatively stable compared to the first half’s 0.19%

This improved outlook builds on the momentum seen in Q1 2025, when Synovus beat analyst expectations with EPS of $1.30 against a forecast of $1.12. The Q2 results continue this positive trajectory, with EPS improving to $1.48, a 14% increase quarter-over-quarter.

With its strengthened capital position, improving credit metrics, and accelerating loan growth in high-growth verticals, Synovus appears well-positioned to deliver on its raised guidance for the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.