Janux stock plunges after hours following mCRPC trial data

Introduction & Market Context

Syrah Resources (ASX:SYR) released its Q3 2025 quarterly activities report on October 28, 2025, revealing operational improvements amid persistent challenges in the global graphite market. The company's stock fell 4.67% following the release, reflecting investor concerns despite several positive developments.

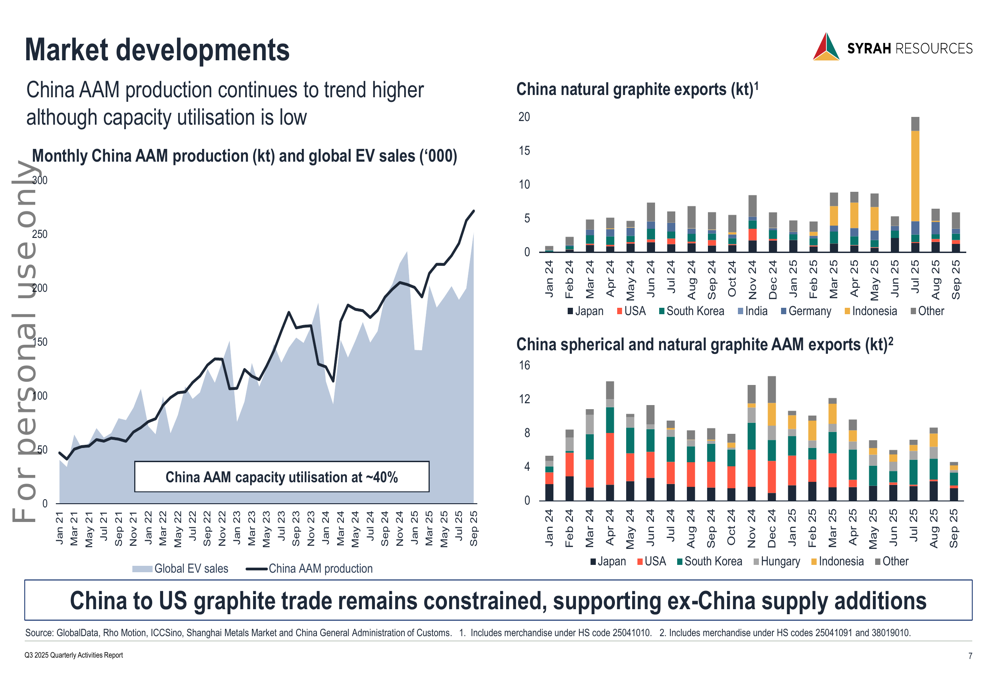

The graphite market continues to face significant headwinds, with China's active anode material (AAM) production capacity utilization hovering around 40%, indicating substantial overcapacity. This market dynamic has placed downward pressure on prices, with Syrah reporting a 9% year-over-year decline in average sales prices.

As shown in the following chart illustrating market developments, China's AAM production correlates with global EV sales, while trade restrictions between China and the US create opportunities for alternative suppliers:

Quarterly Performance Highlights

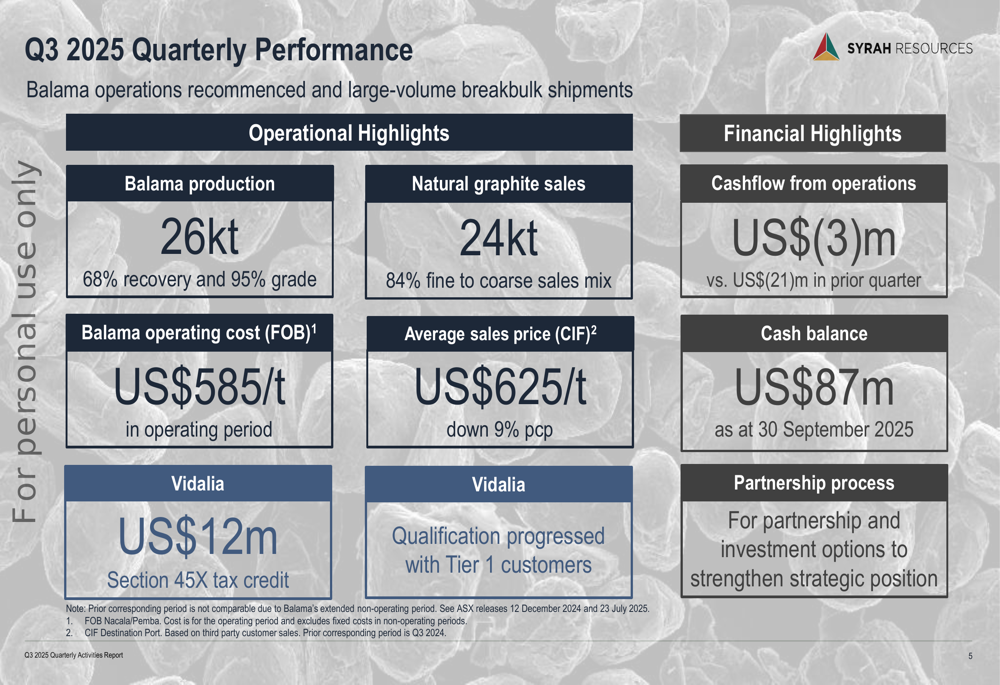

Syrah's Balama operation in Mozambique produced 26,000 tonnes of natural graphite during Q3 2025, achieving a 68% recovery rate and 95% grade. The company sold 24,000 tonnes of natural graphite with an improved 84% fine to coarse sales mix, reflecting its strategic shift toward higher-value products.

The company maintained a competitive operating cost structure with Balama's FOB operating costs at US$585 per tonne during the operating period. However, the average sales price of US$625 per tonne (CIF) represents a 9% decline compared to the previous corresponding period, highlighting the challenging pricing environment.

The following slide summarizes Syrah's key operational and financial metrics for Q3 2025:

Financial Position and Cash Flow

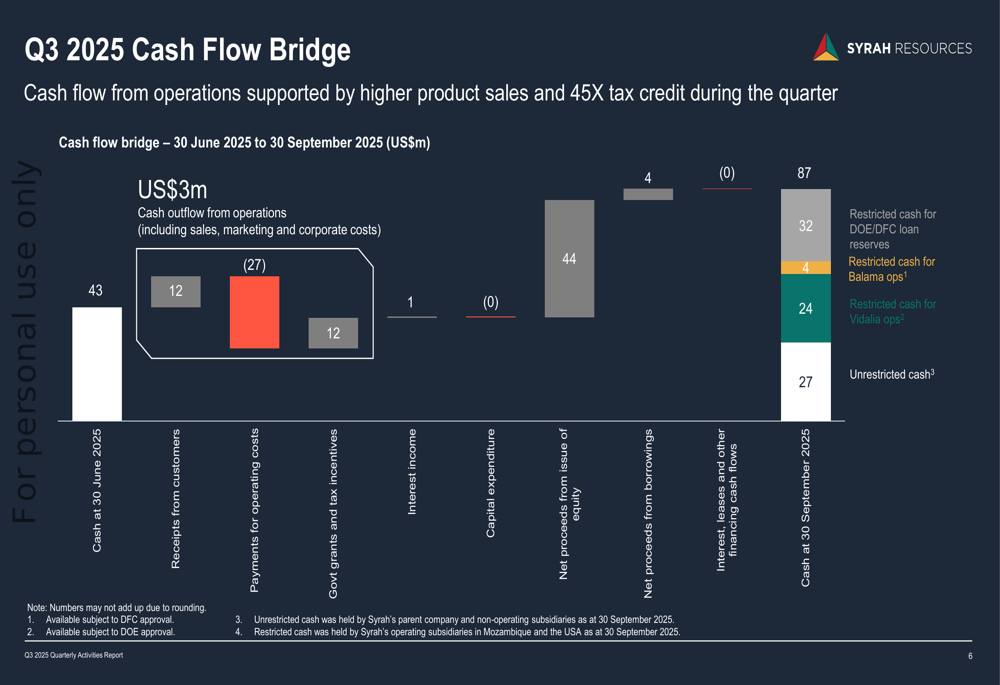

Syrah significantly strengthened its financial position during the quarter, with cash holdings increasing from US$43 million to US$87 million as of September 30, 2025. This improvement was primarily driven by a US$44 million equity issuance and a US$12 million Section 45X tax credit for its Vidalia facility.

The company also demonstrated progress in operational cash flow, which improved to negative US$3 million compared to negative US$21 million in the previous quarter. This improvement suggests Syrah is moving closer to its stated goal of achieving operational cash flow breakeven at Balama.

The detailed cash flow bridge below illustrates the company's financial movements during the quarter:

Of the US$87 million cash balance, US$60 million is restricted (US$32 million for DOE/DFC loan, US$4 million for Balama operations, and US$24 million for Vidalia operations), leaving US$27 million as unrestricted cash for general corporate purposes.

Strategic Positioning and Trade Policy Impact

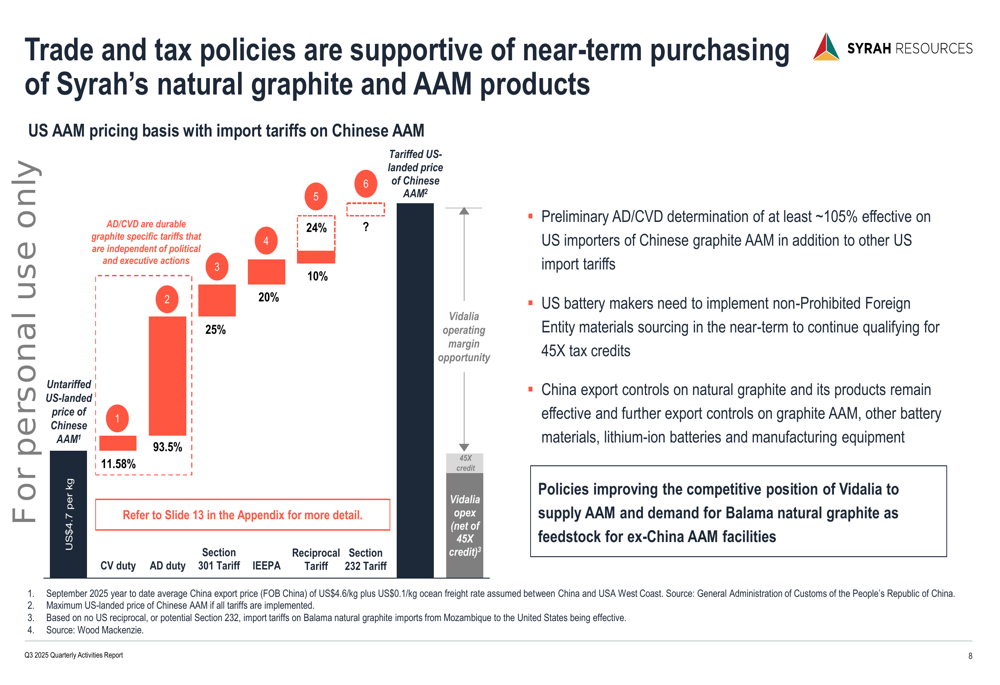

Syrah continues to position itself as the leading natural graphite and active anode material producer outside China, a strategic advantage in the current geopolitical environment. The company is capitalizing on trade tensions between the US and China, which have resulted in substantial tariffs on Chinese graphite imports to the US.

The following chart demonstrates how these tariffs significantly impact the landed price of Chinese AAM in the US market, creating a competitive advantage for Syrah's Vidalia facility:

The preliminary anti-dumping and countervailing duties totaling approximately 105% on Chinese AAM imports, combined with Section 301 tariffs (25%) and IEEPA tariffs (20%), have dramatically altered the competitive landscape. These trade policies support Syrah's strategy to supply US battery manufacturers seeking to qualify for tax credits under the Inflation Reduction Act, which requires non-Prohibited Foreign Entity materials.

Forward-Looking Strategy

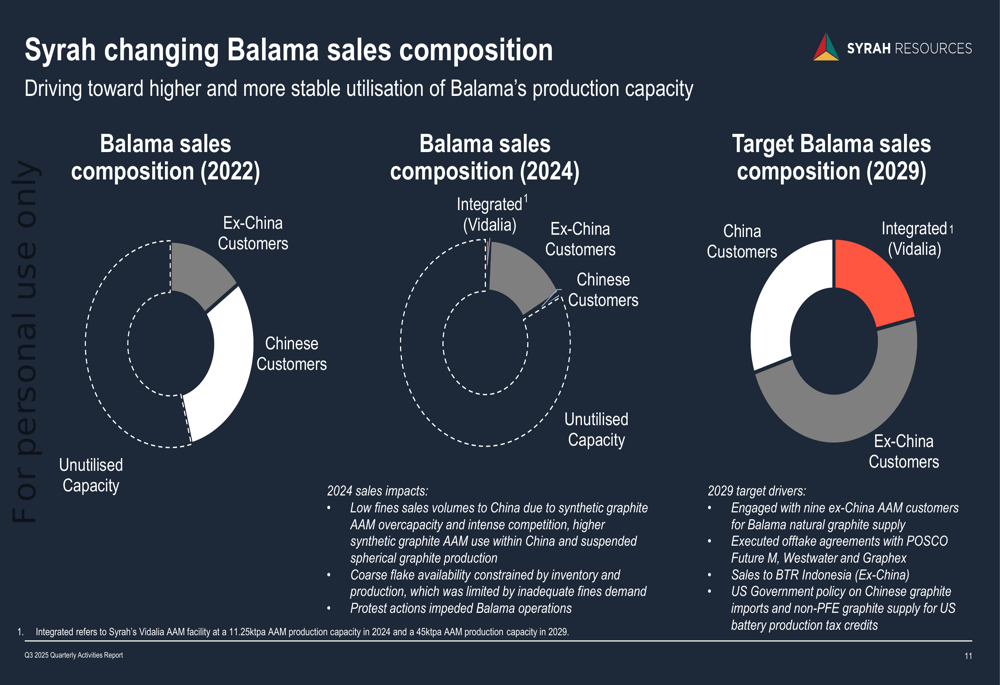

Syrah is actively working to reshape its sales composition, reducing reliance on the Chinese market and focusing on higher-value customers in ex-China markets and vertical integration through its Vidalia facility. The company has engaged with nine ex-China AAM customers for Balama natural graphite supply and has executed offtake agreements with POSCO Future M, Westwater, and Graphex.

The company's strategic roadmap is illustrated in the following value drivers and milestones:

Syrah is also transforming its Balama sales composition, as shown in the following chart, moving from a heavy reliance on Chinese customers toward greater integration with Vidalia and expanded ex-China customer relationships:

Looking ahead, Syrah faces both challenges and opportunities. The synthetic graphite market's overcapacity continues to pressure natural graphite demand, particularly in China. However, US battery manufacturers' need to implement non-Prohibited Foreign Entity materials sourcing to qualify for Section 45X tax credits creates a favorable environment for Syrah's US-based Vidalia facility.

CEO Shaun Verner emphasized the company's focus on achieving operational cash flow breakeven at Balama while expressing optimism about improving market and policy fundamentals. With potential Vidalia expansion decisions expected in 2026 and commercial sales anticipated to begin that same year, Syrah is positioning itself for growth despite current market headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.