ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Tallink Grupp AS (TAL1T) presented its Q3 2025 results on October 23, showing resilience in a challenging Baltic Sea market environment. The Estonian shipping and travel company reported a modest 0.5% revenue increase year-over-year, while achieving a more substantial 10.8% growth in net profit, suggesting improved operational efficiency.

The company currently trades near €0.60 per share, close to its 52-week low of €0.564, with a market capitalization of approximately €535 million. With a beta of 0.37, Tallink’s stock has demonstrated relatively low volatility compared to the broader market.

Tallink maintains a significant market position, accounting for 48% of passenger traffic between Estonia and Finland, and 36% between Finland and Sweden, operating in a competitive environment where discretionary consumer spending remains under pressure.

Quarterly Performance Highlights

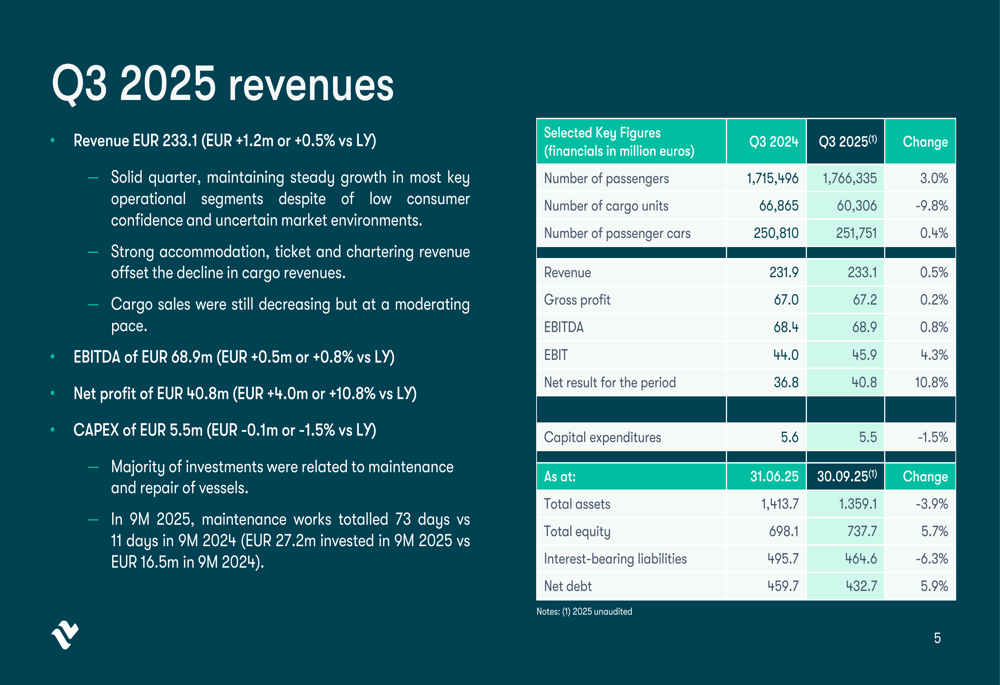

Tallink’s Q3 2025 financial results showed mixed performance across key metrics. Revenue reached €233.1 million, representing a slight 0.5% increase compared to Q3 2024. More impressively, net profit grew to €40.8 million, a 10.8% improvement year-over-year.

The company transported 1,766,335 passengers during the quarter, a 3.0% increase from the previous year, while passenger car volume rose marginally by 0.4% to 251,751 vehicles. However, cargo units declined significantly by 9.8% to 60,306 units, reflecting ongoing challenges in the Baltic freight market.

As shown in the following financial summary:

EBITDA increased slightly by 0.8% to €68.9 million, while capital expenditures decreased by 1.5% to €5.5 million. The company’s asset base contracted to €1,359.1 million, while total equity increased to €737.7 million. Net debt rose to €432.7 million during the period.

Margus Schults, Member of the Management Board, noted during the presentation that "We compete with home sofa and all other alternatives to spend free time," acknowledging the broader competitive landscape for consumer discretionary spending.

Detailed Financial Analysis

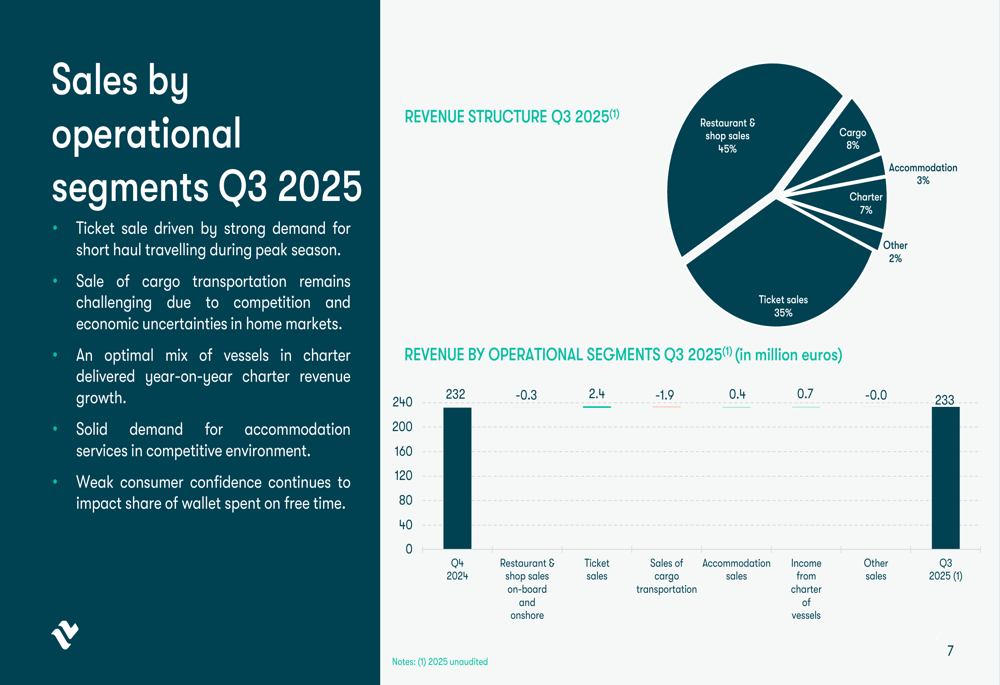

Tallink’s revenue structure reveals the diversified nature of its business model. Restaurant and shop sales constituted the largest portion at 45% of total revenue, followed by ticket sales at 35%. The remaining revenue streams included charter services (7%), cargo (8%), accommodation (3%), and other sources (2%).

The revenue breakdown by operational segments illustrates this distribution:

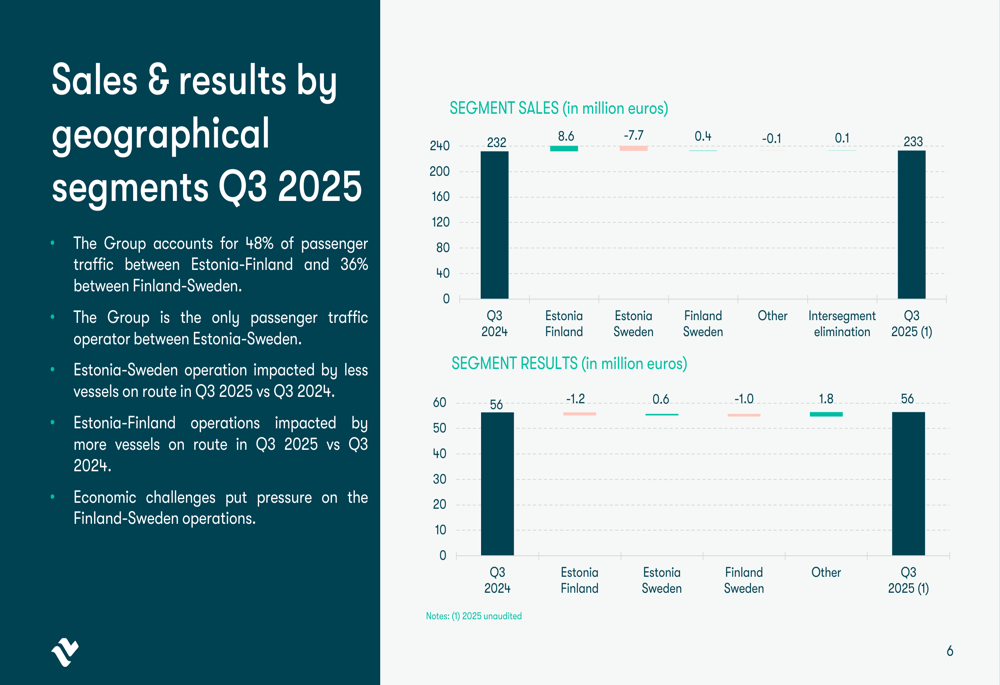

Geographically, Tallink’s operations across different Baltic Sea routes showed varying performance. The Estonia-Finland route was impacted by having more vessels in operation compared to Q3 2024, while the Estonia-Sweden route saw reduced capacity with fewer vessels. Economic challenges continued to pressure the Finland-Sweden operations.

The following chart shows sales and results by geographical segment:

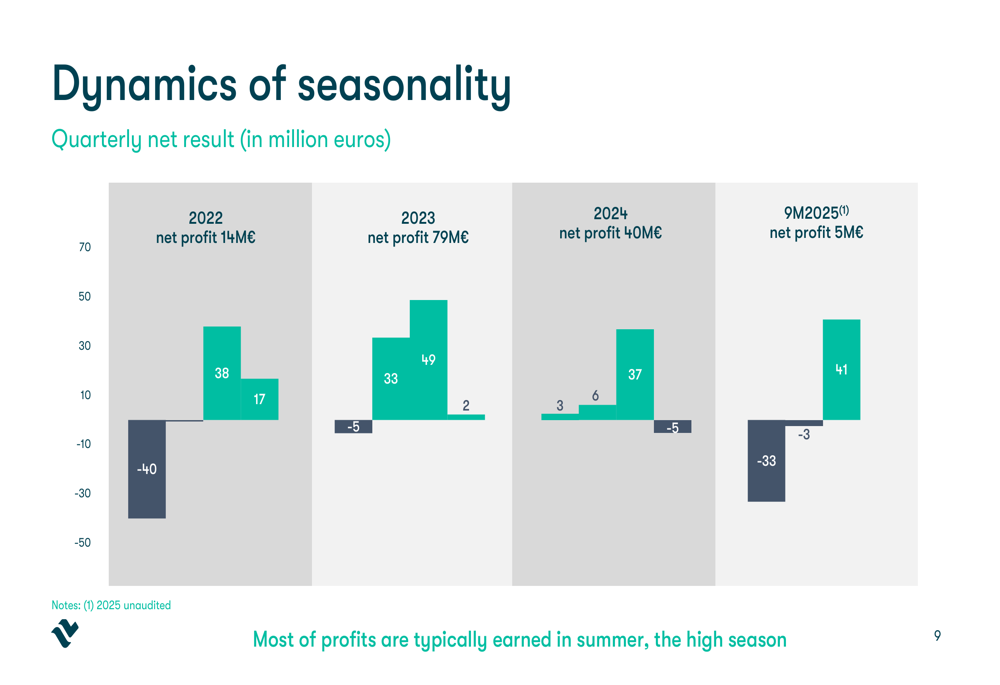

Tallink’s business demonstrates strong seasonality, with the company typically earning most of its profits during the summer high season. This pattern is evident in the quarterly net result dynamics:

While Q3 2025 showed strong profitability with a €40.8 million net profit, the company’s performance for the first nine months of 2025 reveals a more challenging picture. The 9M 2025 net profit was just €5 million, significantly lower than the €50 million reported for the same period in 2024.

Strategic Initiatives

Tallink continues to optimize its fleet and route network to improve operational efficiency. As of Q3 2025, the company operated 12 vessels, including 11 passenger vessels and 1 cargo vessel, following the sale of cargo vessel Sailor in October 2025.

The company maintains 5 regular routes on the Baltic Sea and has 3 vessels under charter agreements - 2 in the Netherlands and 1 in Algeria. Its broader business portfolio includes 4 hotels (3 in Tallinn, 1 in Riga), 20 Burger King restaurants across the Baltic states, and approximately 4,700 employees.

The following slide provides an overview of Tallink’s key operational facts:

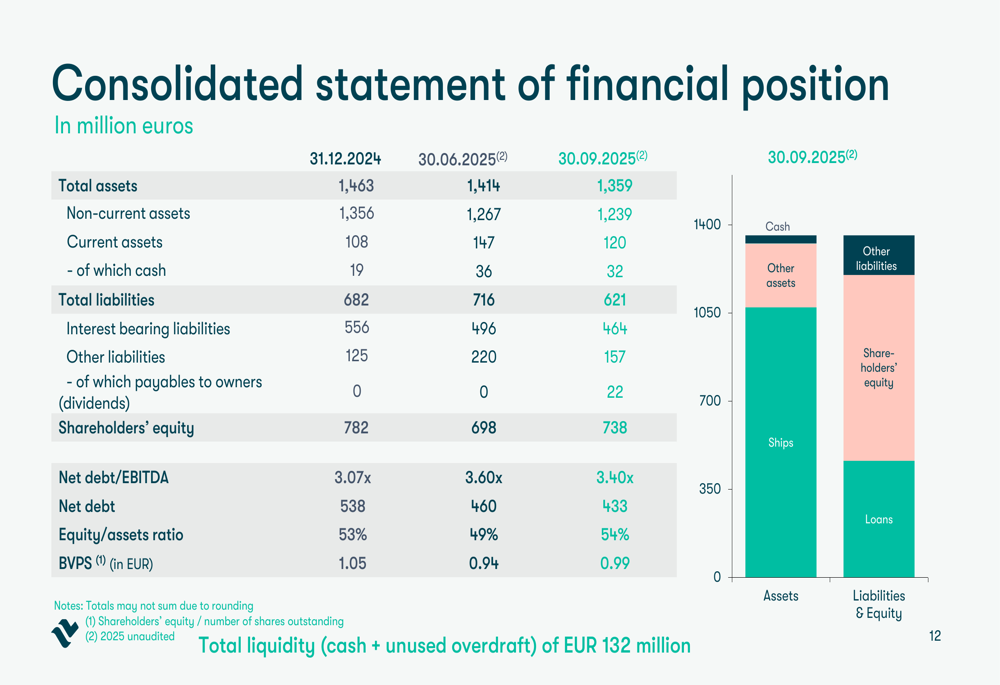

Tallink’s financial position remains stable with a total liquidity (cash plus unused overdraft) of €132 million as of September 30, 2025. The company’s loan portfolio consists primarily of long-term bank loans totaling €389 million, with maturities ranging from 3 to 9 years. The net debt to EBITDA ratio stood at 3.40x, showing some improvement from 3.60x reported on June 30, 2025.

The consolidated statement of financial position shows the company’s asset and liability structure:

Forward-Looking Statements

Tallink faces several challenges and opportunities in the coming quarters. The company’s management expressed cautious optimism, with Schults stating, "We hope that the worst is over," while acknowledging that "We are not assuming that capacity will return to pre-COVID levels."

The company has established a dividend policy of at least €0.05 per share and aims to reduce CO2 emissions by 2% annually. Rather than pursuing major new investments, Tallink is focusing on internal optimizations, targeting modest increases in passenger and cargo volumes.

Key risks include ongoing geopolitical developments affecting core markets, fragile economic conditions impacting travel demand, competition from alternative leisure activities, and potential challenges from environmental regulations.

The company’s strategic focus remains on route optimization and maintaining competitive pricing strategies to enhance passenger experience and comfort, positioning Tallink for steady, if modest, growth in the coming quarters despite the challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.