Starbucks union plans Red Cup Day strike in 25+ cities - Bloomberg

Tamboran Resources Corp (NYSE:TBN, ASX:TBN) presented its fourth quarter fiscal year 2025 results on September 25, highlighting record gas flow rates from its Beetaloo Basin operations and confirming it remains on schedule for first gas production by mid-2026. The company’s shares closed at $21.50 on September 25, down 4.65% from the previous session, but still above its 52-week low of $15.75.

Quarterly Performance Highlights

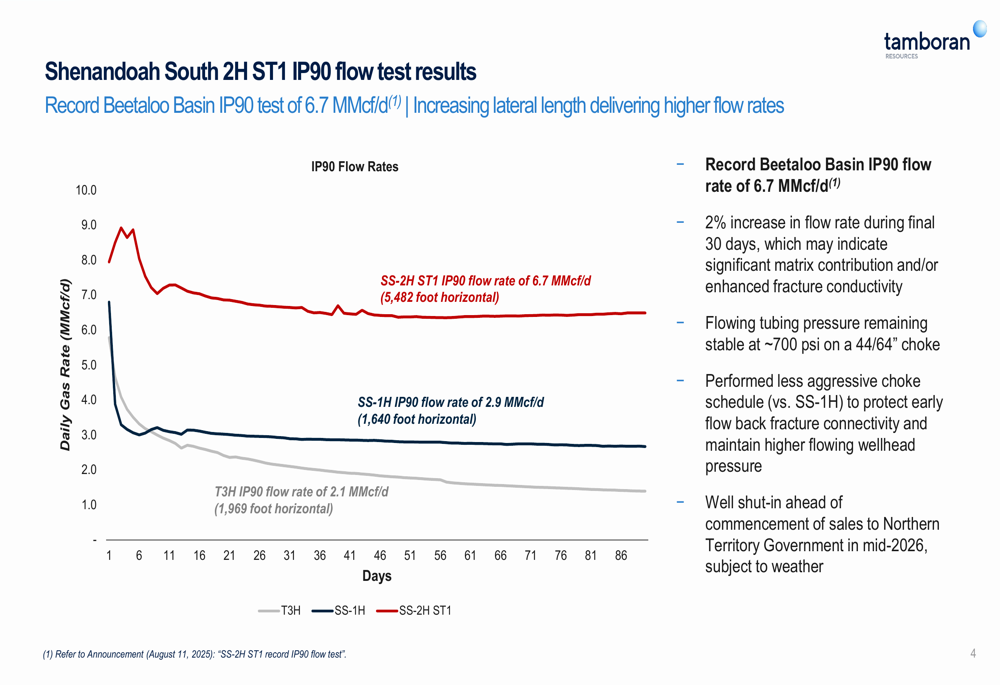

Tamboran reported significant operational achievements during the quarter, most notably delivering record Beetaloo Basin IP90 (initial production over 90 days) flow rates of 6.7 MMcf/d from its Shenandoah South 2H ST1 well. This represents substantial improvement over previous wells, demonstrating the company’s advancing technical capabilities in the region.

"We’ve successfully commenced our first batch drilling program in the Beetaloo Basin with the SS-4H and -5H wells," noted Dick Stoneburner, Chairman and Interim CEO, according to the presentation. The company also received historic approval from Native Title Holders and the Northern Land Council for the sale of appraisal gas, a critical regulatory milestone.

The presentation highlighted strengthened corporate governance with the appointments of industry veterans Scott Sheffield and Phillip Pace as Non-Executive Directors, bringing additional expertise to the board.

As shown in the following chart of flow test results, the SS-2H ST1 well significantly outperformed previous wells in the basin:

Operational Progress

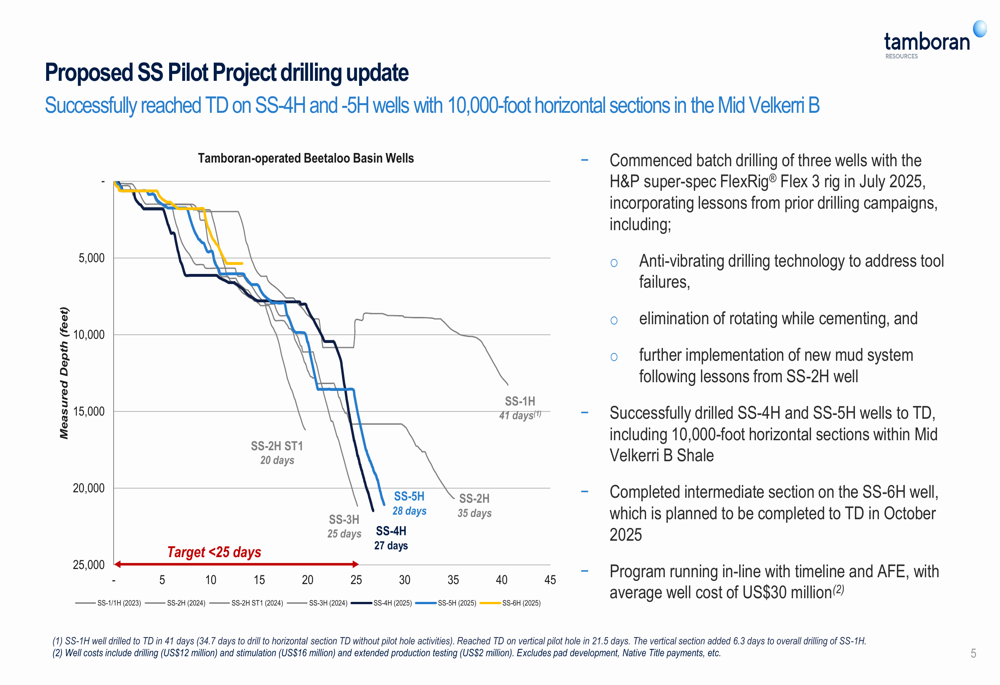

Tamboran’s drilling operations continue to advance, with the company successfully reaching target depth on SS-4H and -5H wells, both featuring 10,000-foot horizontal sections in the Mid Velkerri B formation. The presentation noted that the drilling program is running in line with timeline and budget, with an average well cost of US$30 million.

The drilling progress chart demonstrates improving efficiency compared to previous wells:

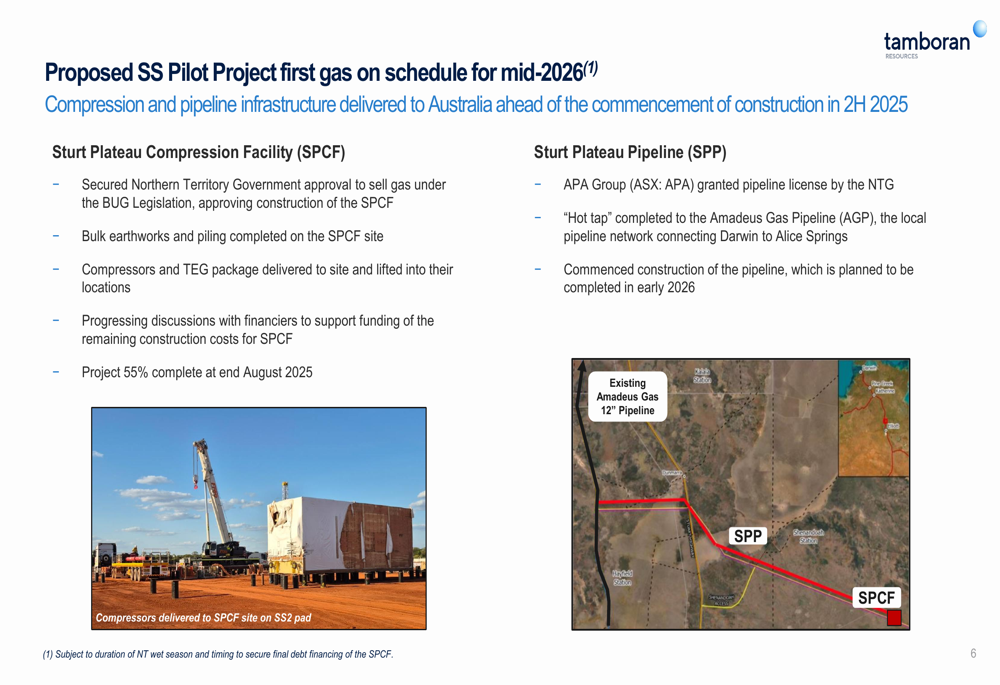

Infrastructure development for the SS Pilot Project is progressing on schedule toward first gas by mid-2026. The Sturt Plateau Compression Facility (SPCF) is now 55% complete, with Northern Territory Government approval secured, bulk earthworks and piling completed, and compressors delivered. Meanwhile, the APA Group has been granted a pipeline license for the Sturt Plateau Pipeline (SPP), with construction already underway.

The following image illustrates the pipeline infrastructure development:

Financial Position

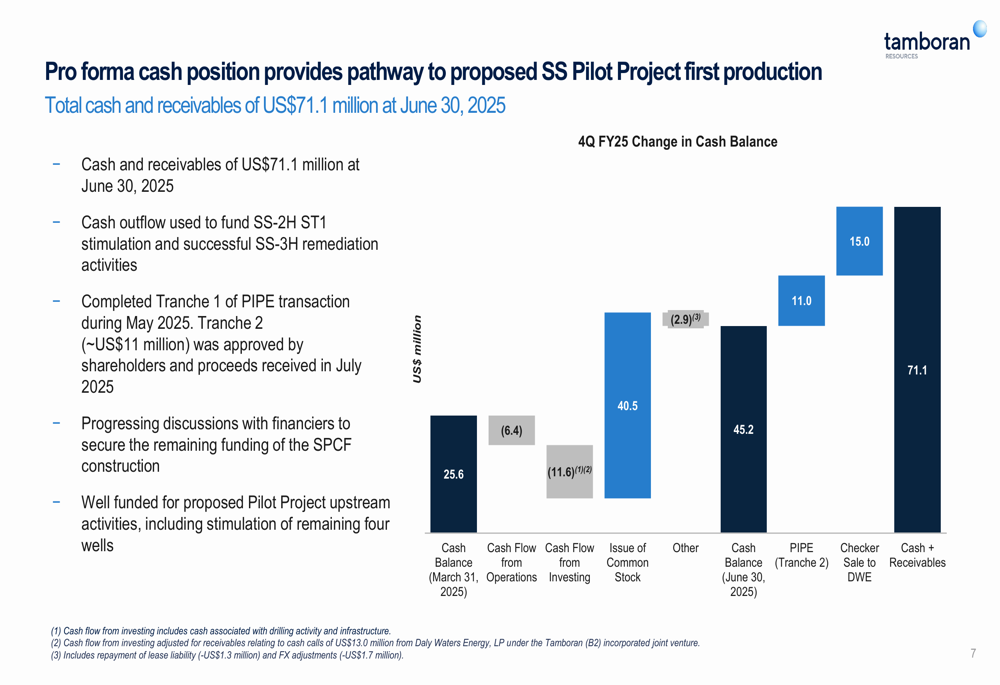

Tamboran reported a pro forma cash and receivables position of US$71.1 million as of June 30, 2025. This includes US$45.2 million in cash, US$11 million expected from Tranche 2 of a PIPE transaction, and US$15 million from an acreage sale to DWE.

The financial waterfall chart shows the company’s cash flow during the quarter:

This represents a significant improvement from the US$25.6 million reported in the previous quarter. However, the presentation also revealed ongoing cash outflows, with US$6.4 million used for operations and US$11.6 million for investing activities during the quarter.

According to recent InvestingPro data, while Tamboran holds more cash than debt on its balance sheet, analysts have expressed concern about its cash burn rate. The company’s stock has traded between $15.75 and $34.50 over the past 52 weeks, suggesting significant volatility as it progresses toward production.

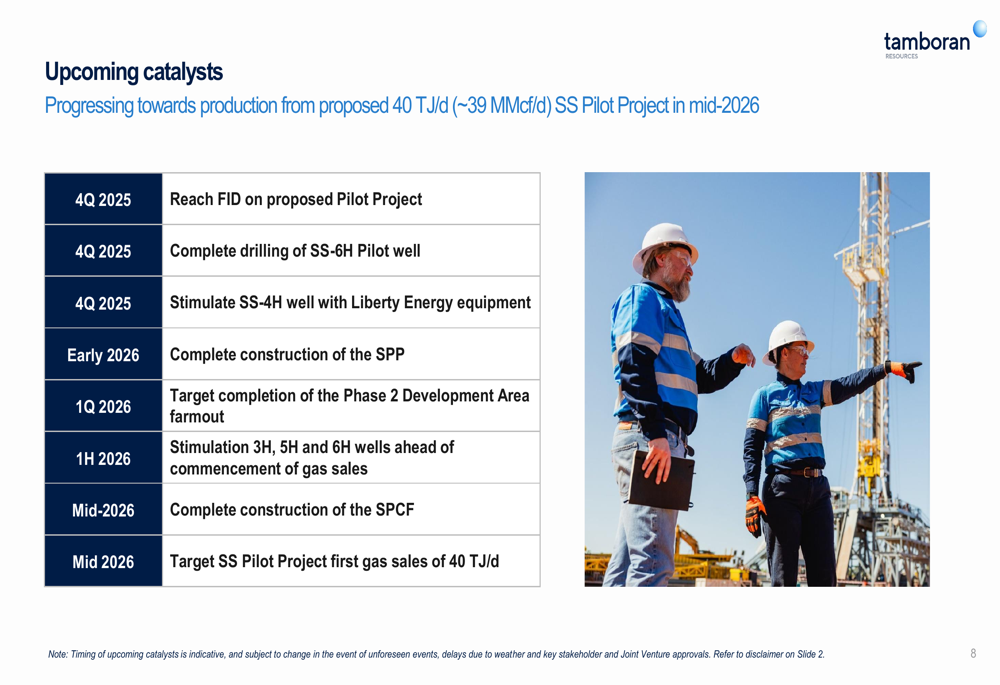

Forward-Looking Statements

Tamboran outlined several upcoming catalysts as it progresses toward production from the proposed 40 TJ/d (~39 MMcf/d) SS Pilot Project in mid-2026:

Key milestones include reaching Final Investment Decision (FID) on the proposed Pilot Project in Q4 2025, completing construction of the SPP in early 2026, and targeting completion of the Phase 2 Development Area farmout in Q1 2026.

The company’s presentation emphasized its pathway to first gas sales, though investors should note that Tamboran faces challenges in cost management and operational efficiency. In a previous earnings call, CEO Joel Riddle highlighted the company’s substantial resource potential, stating, "20 Tcf is enough reserves that we could develop two Bcf a day for twenty years."

With its strengthened cash position and operational progress, Tamboran appears positioned to advance toward its production goals, though execution risks remain as the company works to complete its infrastructure projects and drilling program on schedule and within budget.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.