US stock futures steady with China trade talks, Q3 earnings in focus

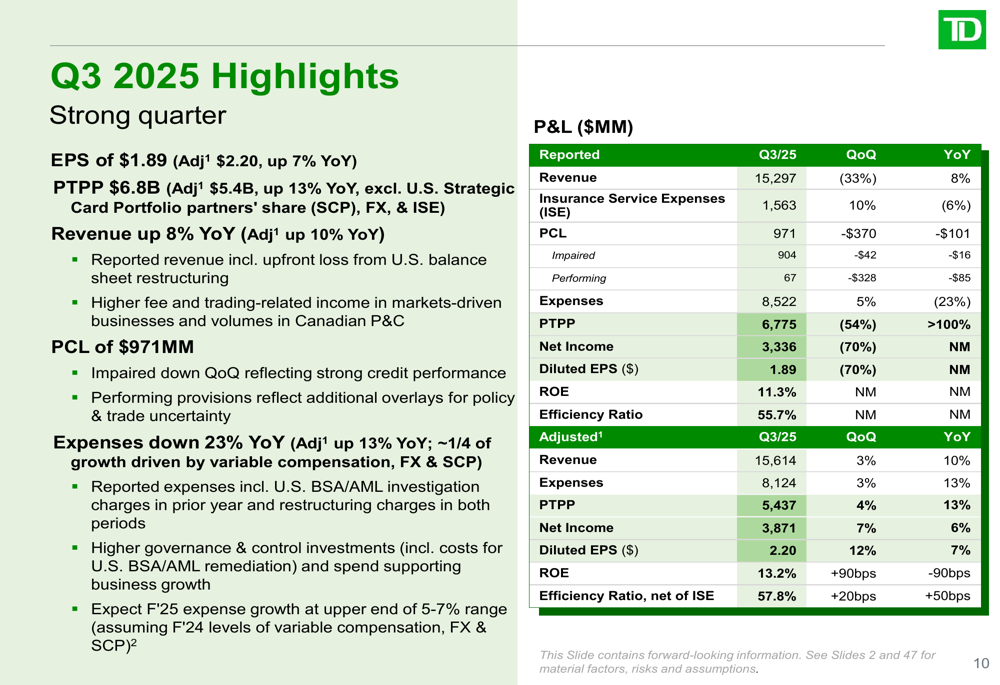

TD Bank Group (NYSE:TD) presented its third-quarter 2025 results on August 28, 2025, highlighting progress on strategic restructuring initiatives while delivering adjusted earnings growth. The bank reported adjusted net income of $3.9 billion and adjusted EPS of $2.20, representing a 7% year-over-year increase, despite ongoing challenges in its U.S. operations.

Quarterly Performance Highlights

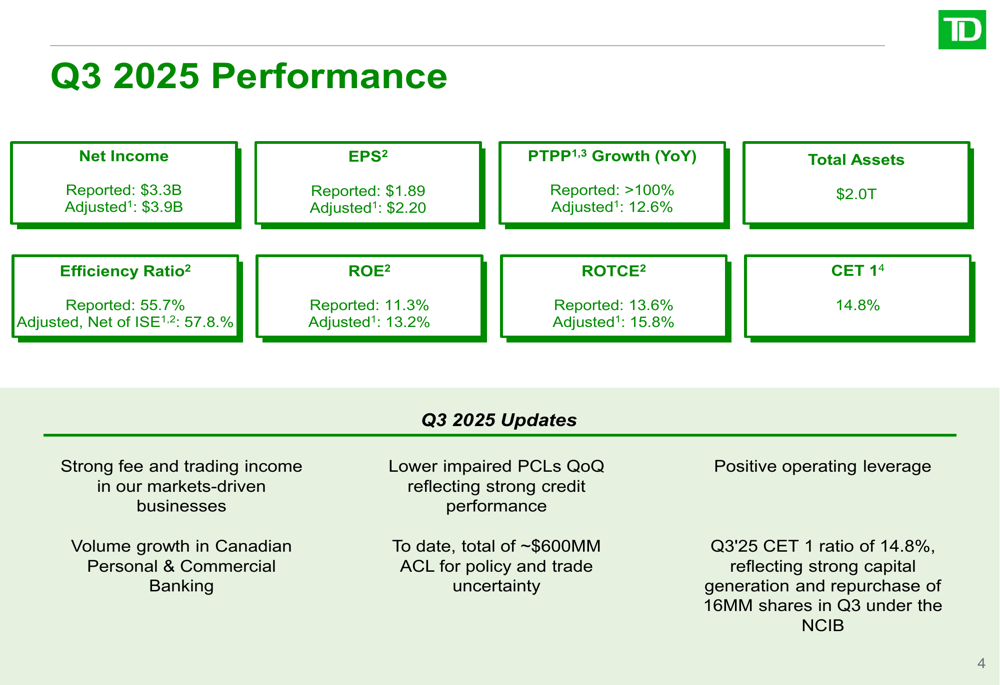

TD Bank reported Q3 2025 net income of $3.3 billion on a reported basis and $3.9 billion on an adjusted basis. Reported earnings per share came in at $1.89, while adjusted EPS reached $2.20. The bank maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 14.8%, down slightly from 14.9% in the previous quarter.

As shown in the following comprehensive financial overview, TD achieved strong pre-tax, pre-provision (PTPP) earnings growth of 12.6% year-over-year on an adjusted basis:

Revenue increased by 8% year-over-year on a reported basis and 10% on an adjusted basis, driven by strong fee and trading income. The bank’s provision for credit losses (PCL) decreased to $971 million from $1,341 million in the previous quarter, reflecting improvements across consumer and business portfolios.

The detailed financial performance shows positive operating leverage and strong capital generation, with the bank repurchasing 16 million shares during the quarter:

Strategic Initiatives

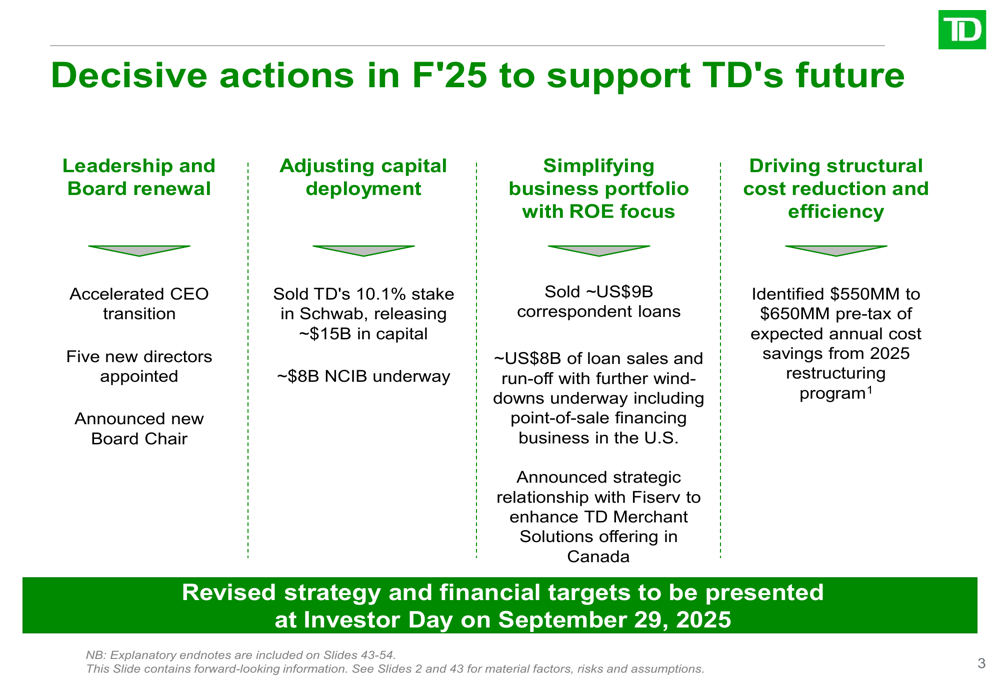

TD Bank outlined several decisive actions taken in fiscal year 2025 to support its future growth and profitability. These initiatives include leadership renewal, capital redeployment, business portfolio simplification, and cost reduction efforts:

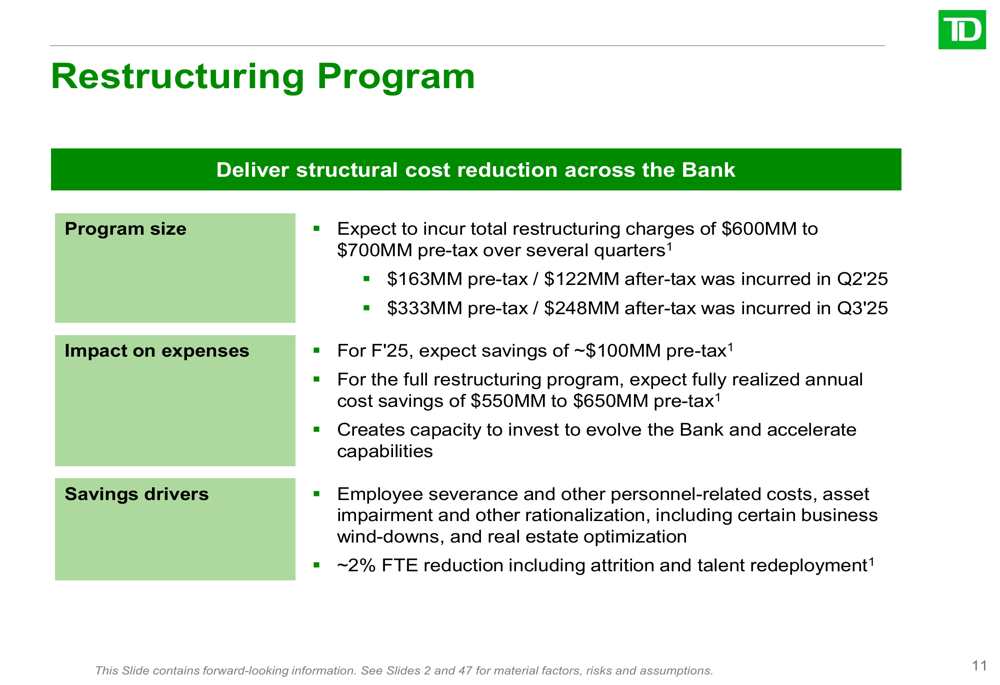

A key component of TD’s strategy is its comprehensive restructuring program, which is expected to deliver annual cost savings of $550 million to $650 million pre-tax. The bank has already incurred restructuring charges of $163 million pre-tax in Q2 2025 and $333 million pre-tax in Q3 2025, with more expected in coming quarters.

"We are making significant progress on our strategic initiatives while maintaining strong capital and liquidity positions," said Raymond Chun, CEO of TD Bank, according to the previous earnings call. "Our focus remains on identifying growth opportunities and executing against our strategic pillars."

The restructuring program includes employee severance, asset impairment, business wind-downs, and real estate optimization, with approximately 2% FTE reduction including attrition and talent redeployment:

Segment Performance

TD’s Canadian Personal & Commercial Banking segment delivered record revenue, earnings, and volume growth. The segment reported net income of $1,953 million, up 4% year-over-year, with revenue increasing by 5%. Loan growth was particularly strong in residential secured lending, card loans (up 7%), and business loans (up 6%).

The Wealth Management & Insurance segment showed impressive performance with earnings up 63% year-over-year and PTPP up 66%. TD Asset Management reinforced its position as the #1 institutional asset manager in Canada with $2.5 billion in new mandates.

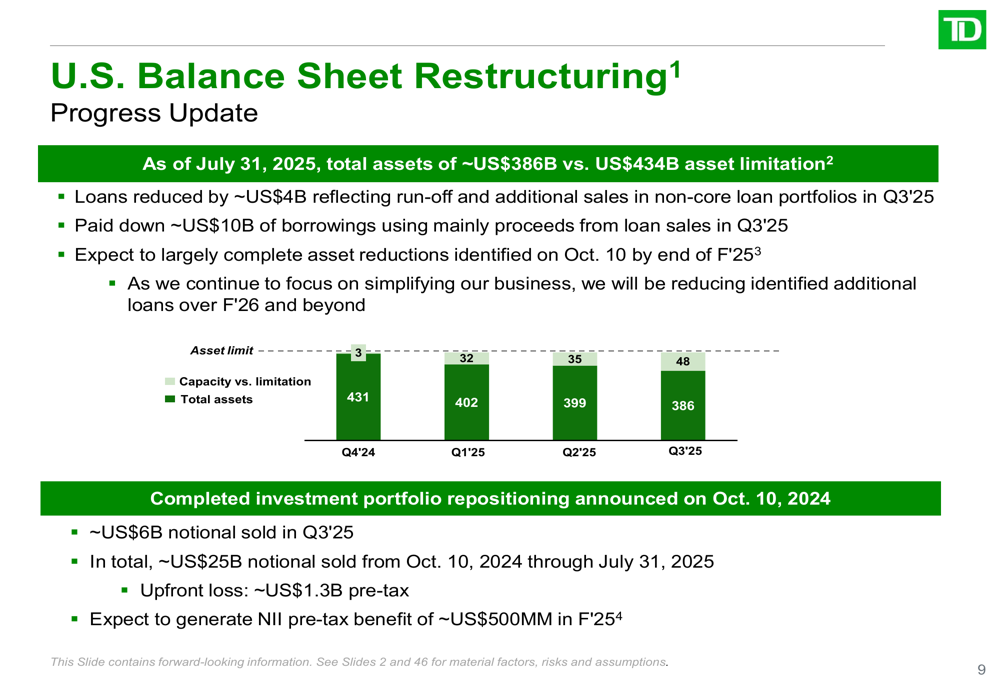

U.S. Retail performance reflected the ongoing focus on BSA/AML remediation, with adjusted net income of US$695 million. The segment achieved its ~10% asset reduction target as part of the balance sheet restructuring initiative:

Wholesale Banking delivered strong results with revenue exceeding $2 billion for the third consecutive quarter. Net income increased by 26% year-over-year on a reported basis and 12% on an adjusted basis.

Risk Management & Credit Quality

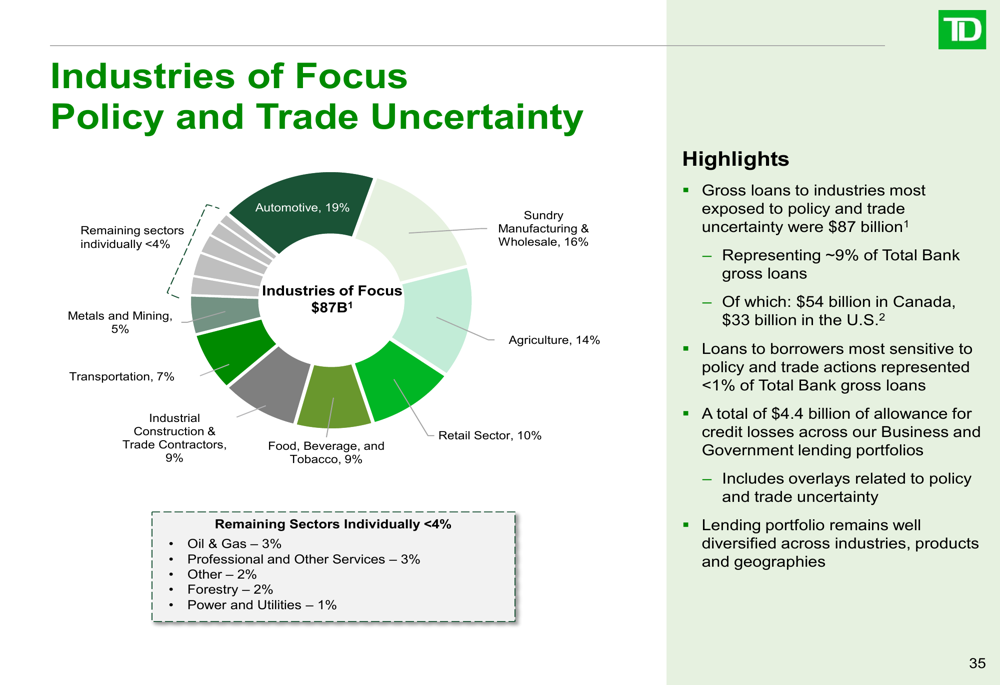

TD Bank is closely monitoring industries most sensitive to policy and trade uncertainty, which represent approximately 9% of the bank’s total gross loans. The following chart illustrates the breakdown of these industries:

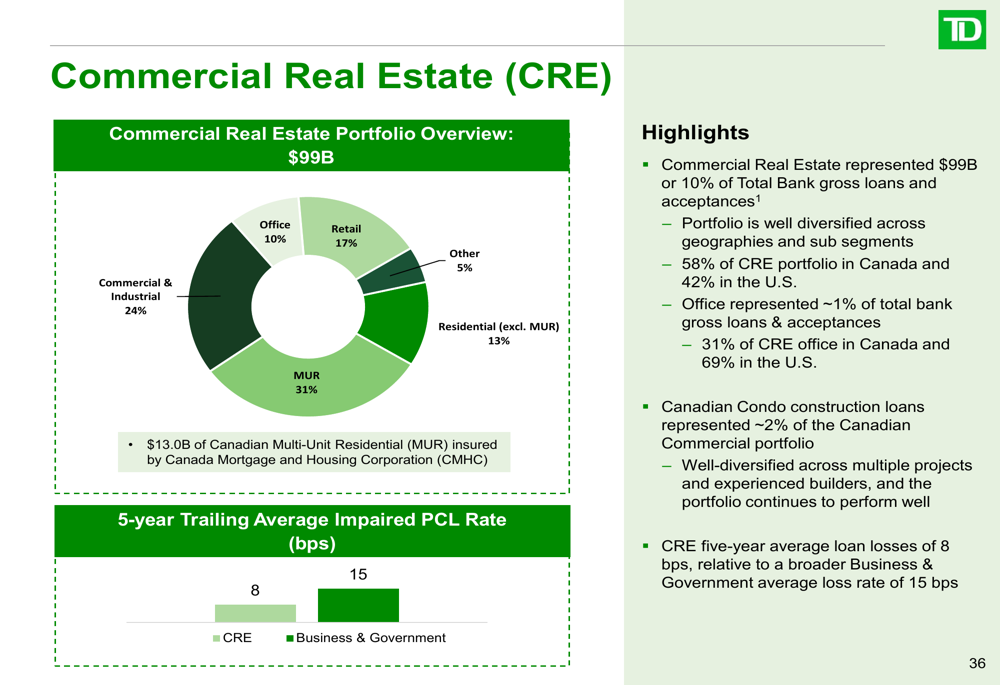

The bank’s commercial real estate portfolio, representing 10% of total gross loans and acceptances, has maintained strong credit performance with a five-year average loan loss rate of 8 basis points, significantly below the broader business and government average loss rate of 15 basis points:

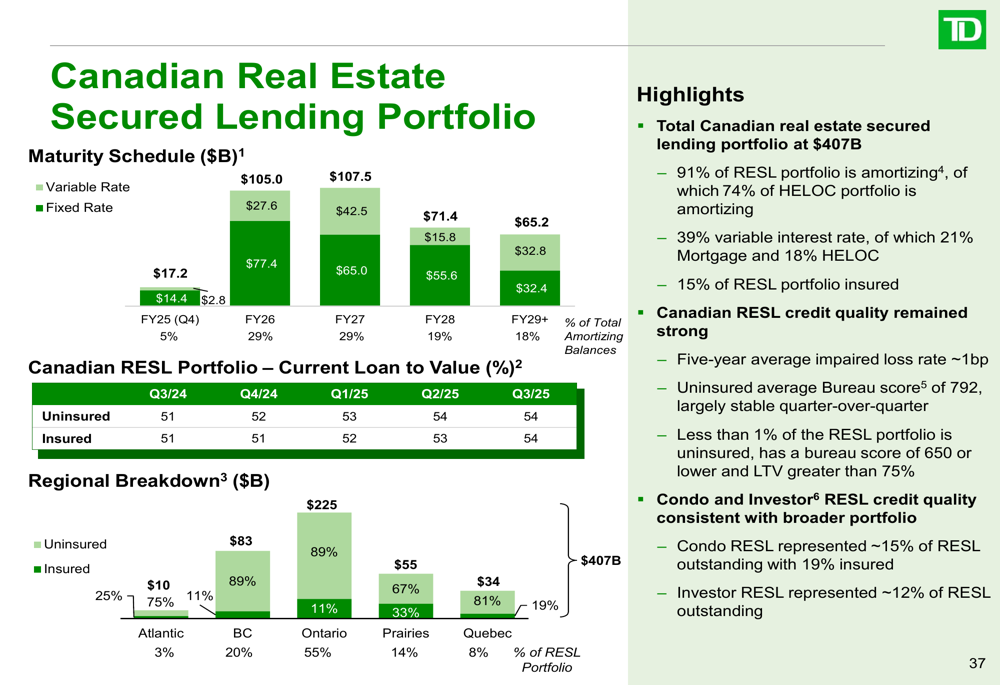

TD’s Canadian real estate secured lending portfolio remains robust at $407 billion, with 91% of the portfolio being amortizing loans. The geographic distribution shows diversification across Canadian regions:

Provision for credit losses decreased quarter-over-quarter, with the bank expecting fiscal 2025 PCLs to be in the range of 45 to 55 basis points. Gross impaired loans increased quarter-over-quarter, largely in the Wholesale Banking and U.S. Commercial lending portfolios.

Forward-Looking Statements

TD Bank is scheduled to present its revised strategy and financial targets at an Investor Day on September 29, 2025. The bank continues to focus on completing its U.S. BSA/AML remediation, with the majority of Management Remediation Actions expected to be completed in 2025, though significant work will remain in 2026 and 2027.

The bank’s digital transformation continues to show progress, with increased adoption across all segments. Canadian Personal & Commercial Banking saw digital adoption increase by 140 basis points year-over-year, while mobile users increased by 5.9%.

TD’s shares were trading up 2.53% in premarket trading at $78.07 following the earnings presentation, reflecting investor optimism about the bank’s strategic direction and adjusted earnings growth despite ongoing challenges.

The bank maintains a strong capital position that will allow it to navigate economic uncertainties while continuing to execute on its strategic initiatives. Management expects to largely complete the identified asset reductions by the end of fiscal 2025, with additional loan reductions continuing over fiscal 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.