Piper Sandler lowers Arbor Realty Trust stock price target on credit issues

Introduction & Market Context

Technip Energies (PARIS:TE) reported its third quarter and nine-month 2025 results on October 30, showing solid revenue growth but falling short of analysts’ expectations. The company’s stock dropped 7.04% following the release, closing at €37.22, as investors reacted to the earnings miss despite management’s positive outlook on long-term positioning.

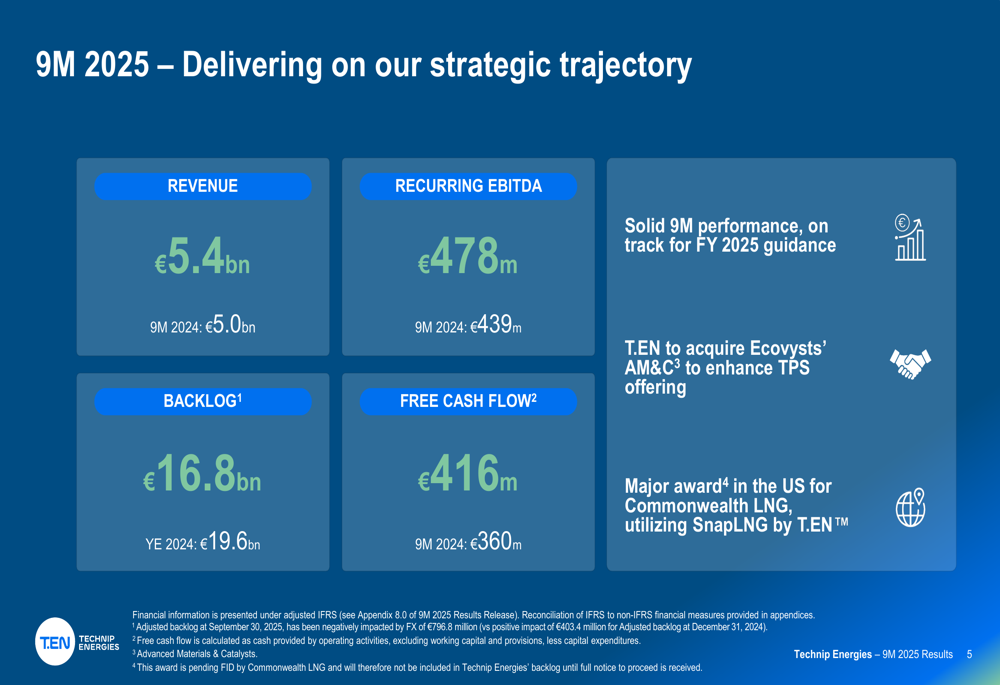

The engineering and technology company reported a 9% year-over-year increase in revenue for the first nine months of 2025, reaching €5.4 billion, while maintaining a stable EBITDA margin of 8.8%. However, Q3 earnings per share came in at €0.5981, missing the forecast of €0.6287 by 4.87%.

Quarterly Performance Highlights

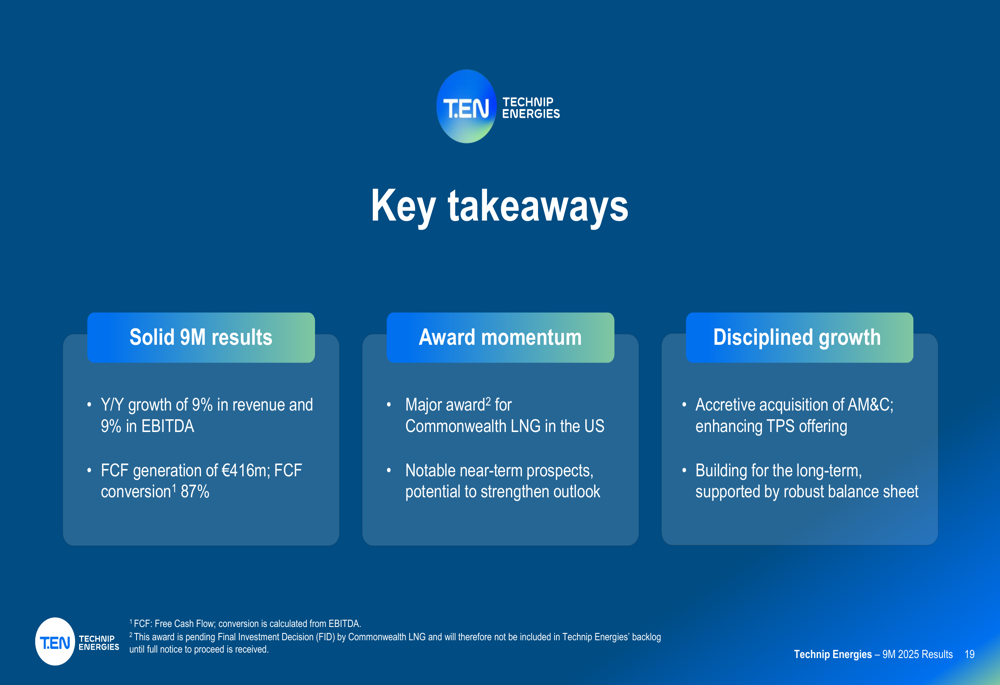

Technip Energies delivered mixed results across its business segments for the first nine months of 2025. The company reported recurring EBITDA of €478 million, representing a 9% increase from the same period in 2024, while diluted earnings per share rose slightly to €1.58 from €1.55.

As shown in the following financial summary:

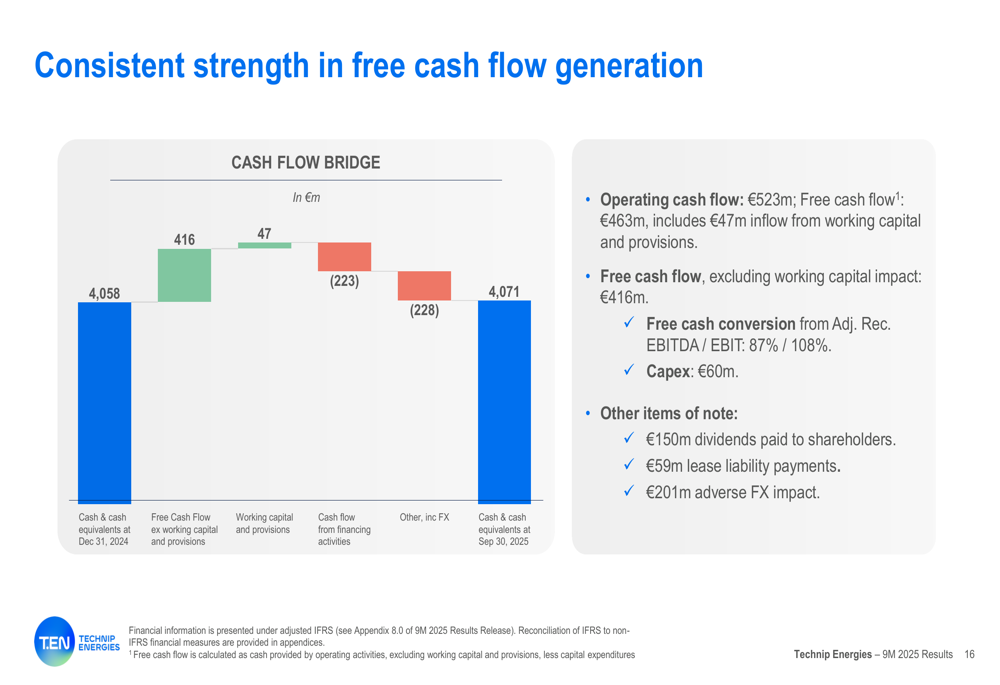

Free cash flow generation remained strong at €416 million, with an impressive conversion rate of 87%, up from 82% in the comparable period. The company’s backlog stood at €16.8 billion, down from €19.6 billion at year-end 2024, but still representing over three times the annual segment revenue.

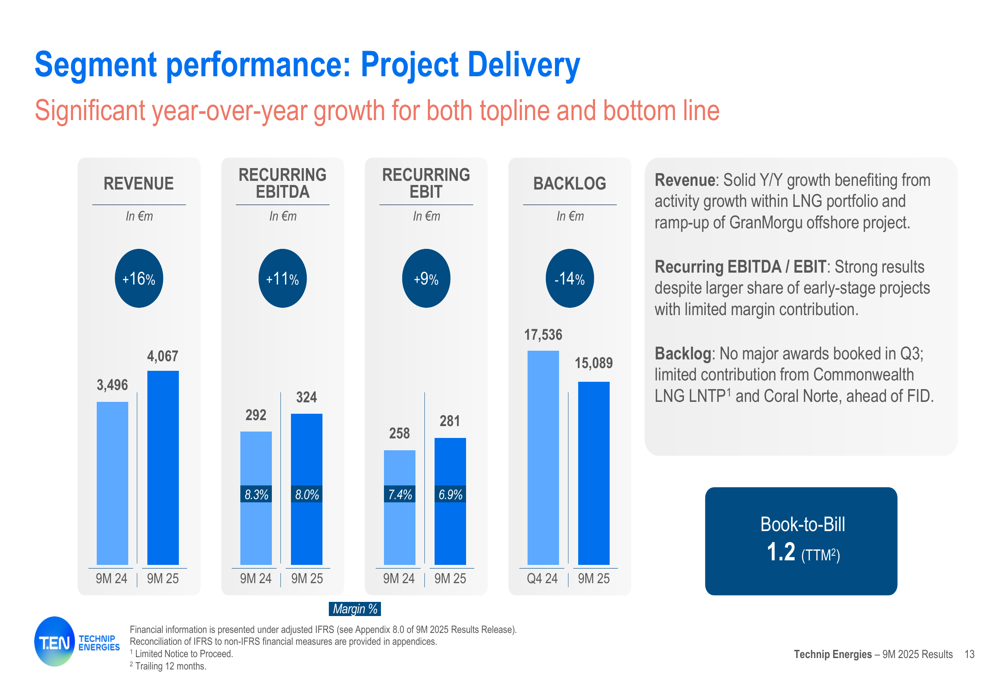

The Project Delivery segment, which handles major EPC contracts, showed robust performance with 16% revenue growth:

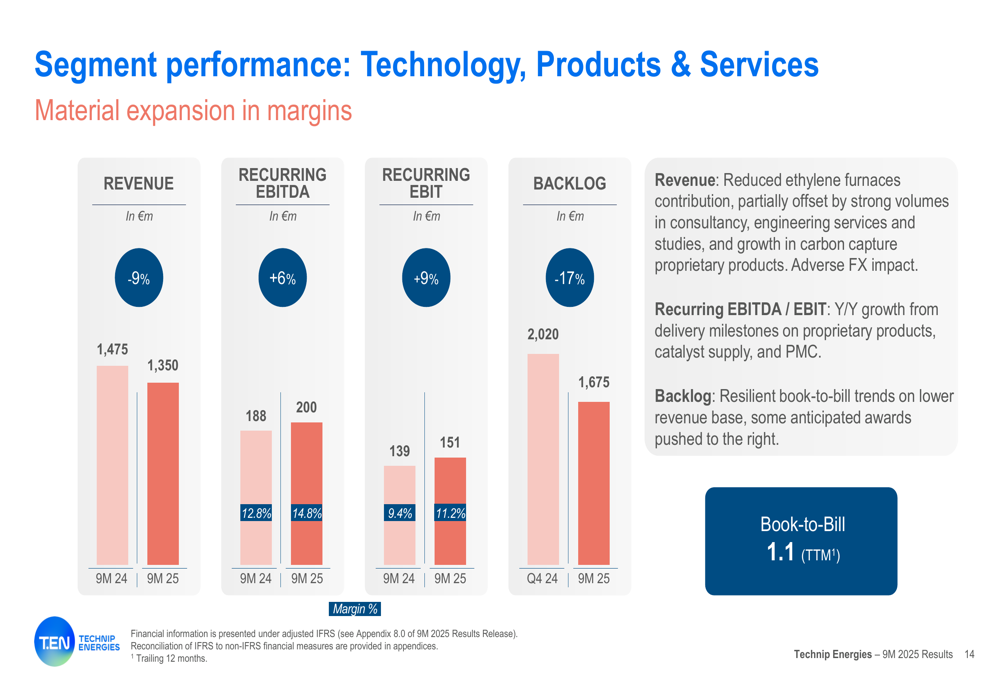

Meanwhile, the Technology, Products & Services (TPS) segment experienced a 9% revenue decline but improved profitability with a 6% increase in EBITDA:

The company’s cash flow generation remained strong, as illustrated in the following bridge chart:

Strategic Initiatives

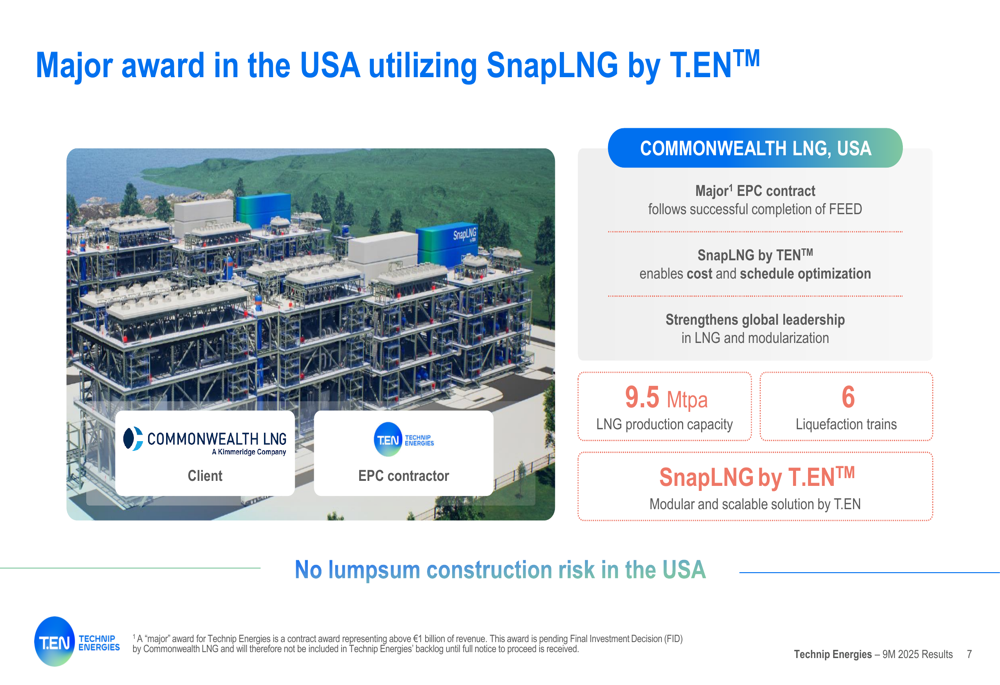

During the quarter, Technip Energies announced a major EPC contract for Commonwealth LNG in the United States, utilizing its proprietary SnapLNG technology. This award, pending final investment decision, represents a significant expansion of the company’s LNG portfolio and strengthens its position in the U.S. market.

As detailed in the presentation:

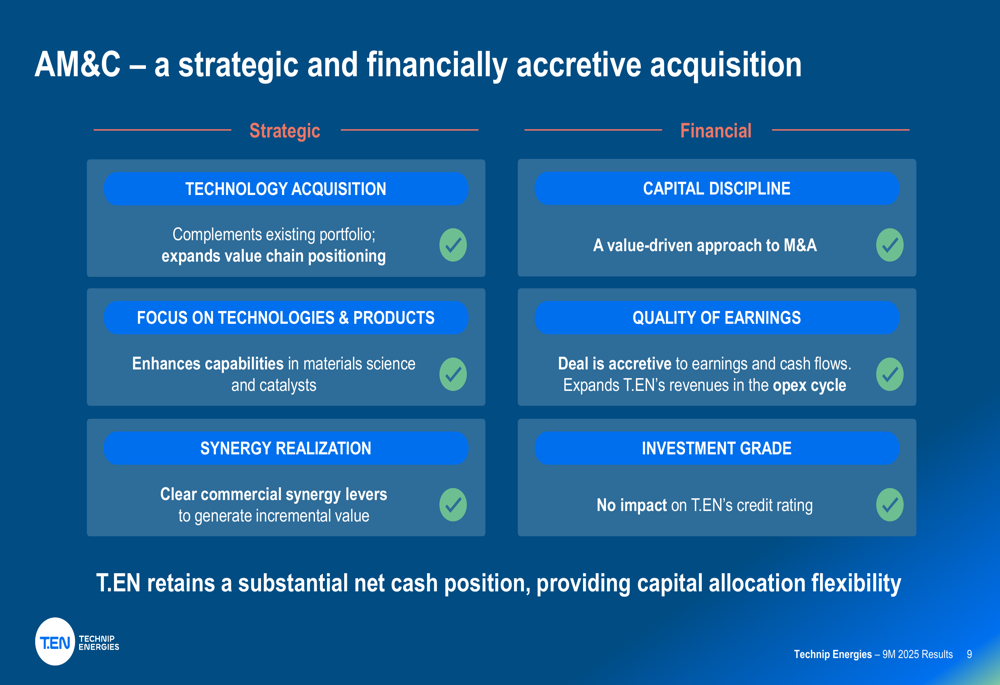

The company also completed the acquisition of Ecovysts’ Advanced Materials & Catalysts (AM&C) business, a strategic move to enhance its technology portfolio and expand its presence in the materials science and catalysts sector.

The acquisition is expected to be immediately accretive to earnings while maintaining the company’s investment grade credit rating:

The AM&C acquisition will enhance the company’s Technology, Products & Services segment by increasing the proportion of technology and products in the revenue mix from approximately 40% to 45%, while boosting the segment’s EBITDA margin from 12.9% to 14.1%.

Operational Progress

Technip Energies highlighted several operational achievements during Q3 2025, including progress on major LNG projects and energy derivative projects, as well as advancements in decarbonization initiatives:

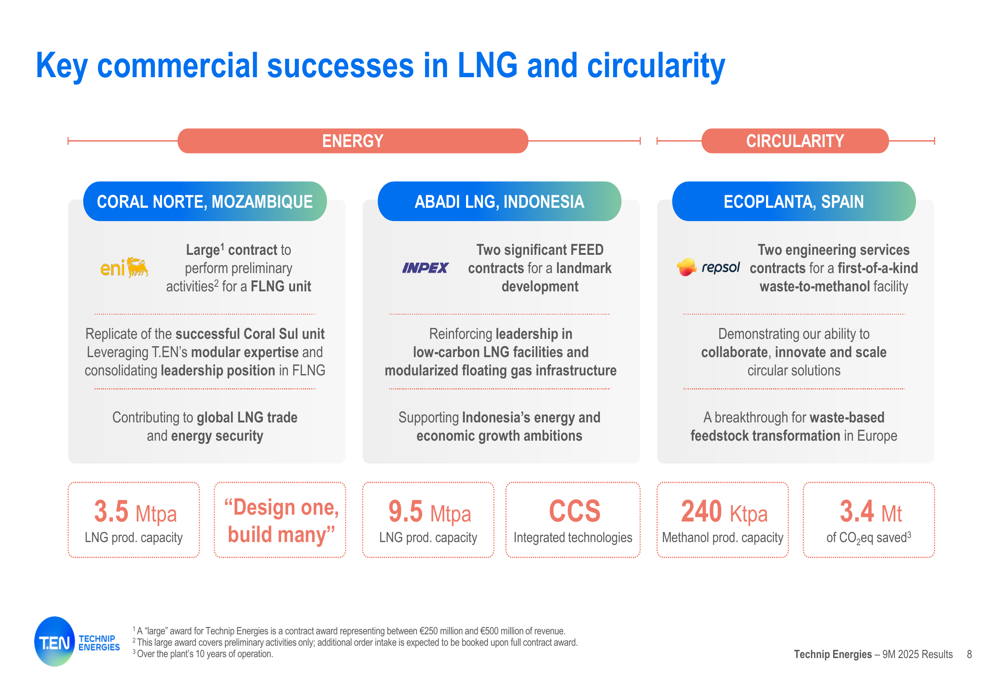

The company also secured commercial successes in both traditional energy and circularity projects, demonstrating its balanced approach to energy transition:

Forward-Looking Statements

Despite the Q3 earnings miss, Technip Energies confirmed its full-year 2025 guidance, though it noted that TPS segment revenues are expected to come in at the lower end of the previously provided range of €1.8-2.2 billion.

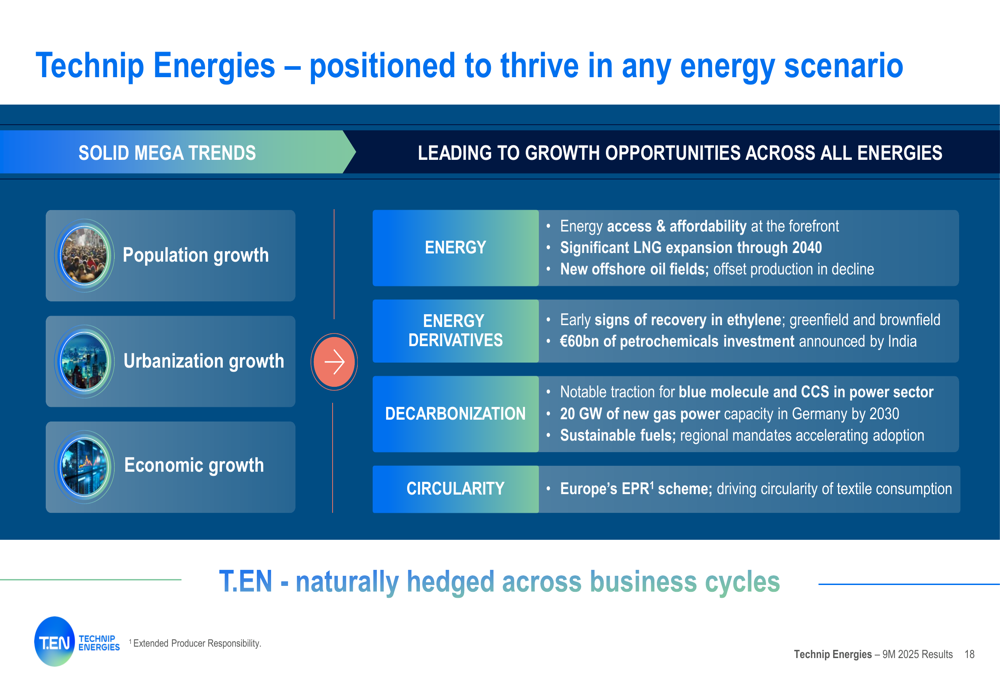

The company emphasized its positioning to benefit from various energy scenarios, highlighting opportunities across traditional energy, energy derivatives, decarbonization, and circularity:

CEO Arnaud Pieton emphasized the company’s strategic positioning, stating, "We are naturally hedged and positioned to thrive in any energy scenario." He also highlighted the ongoing trend towards decarbonization, describing it as "a game of resilience."

Conclusion

Technip Energies’ Q3 2025 presentation paints a picture of a company navigating a complex energy landscape with a diversified approach. While the quarterly results fell short of market expectations, leading to a significant stock price decline, the company’s overall nine-month performance showed solid growth in key financial metrics.

The key takeaways from the presentation highlight both the company’s current performance and strategic direction:

Investors will be watching closely to see if the company can maintain its guidance and capitalize on its project pipeline, particularly given concerns about delayed LNG final investment decisions that could impact future growth. The integration of the AM&C acquisition and execution of the Commonwealth LNG project (pending FID) will be critical factors in determining the company’s performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.