Asia FX dithers as dollar steadies before Powell speech; yen muted after CPI data

Introduction & Market Context

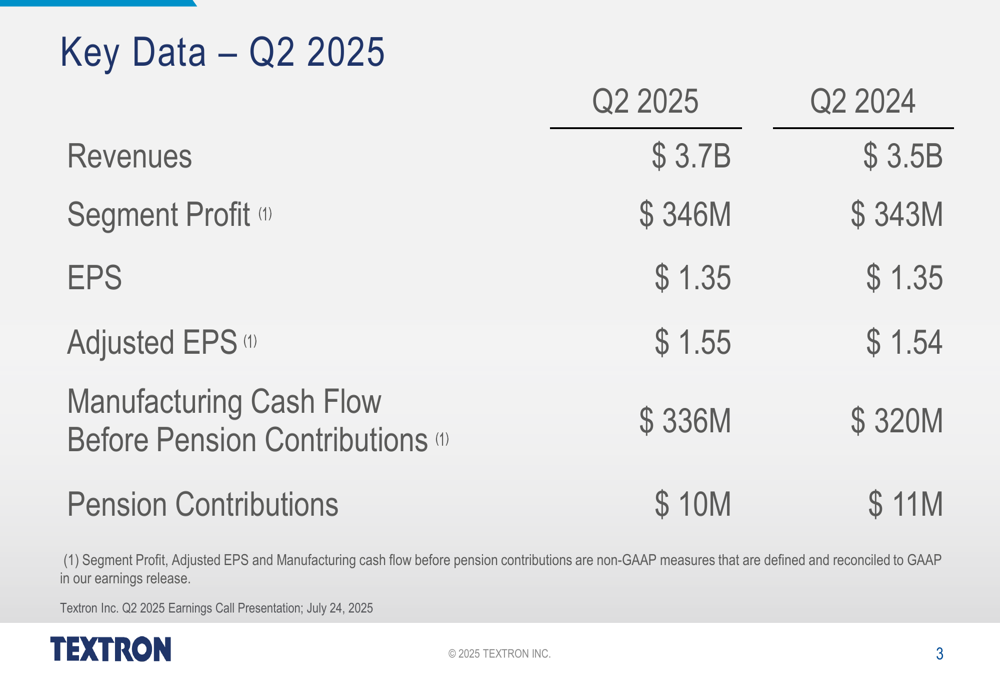

Textron Inc . (NYSE:TXT) released its second quarter 2025 earnings presentation on July 24, 2025, revealing a 5.7% year-over-year revenue increase to $3.7 billion, up from $3.5 billion in the same period last year. The industrial conglomerate’s stock closed at $87.21 prior to the presentation, showing minimal movement in premarket trading with shares down just 0.01% to $87.20.

The Q2 results come after a strong first quarter where Textron exceeded analyst expectations with adjusted earnings of $1.28 per share against forecasts of $1.16. The latest quarterly performance shows sequential improvement in earnings per share, rising from $1.28 in Q1 to $1.35 in Q2 2025.

Quarterly Performance Highlights

Textron’s Q2 2025 financial results showed modest growth across key metrics compared to the same period last year. Revenue increased to $3.7 billion, while segment profit edged up slightly to $346 million from $343 million. Earnings per share remained flat at $1.35, though adjusted EPS showed a marginal improvement to $1.55 from $1.54 in Q2 2024.

Manufacturing cash flow before pension contributions showed more substantial improvement, reaching $336 million compared to $320 million in the prior year period, representing a 5% increase. This marks a significant turnaround from the negative manufacturing cash flow of $158 million reported in Q1 2025.

Segment Performance Analysis

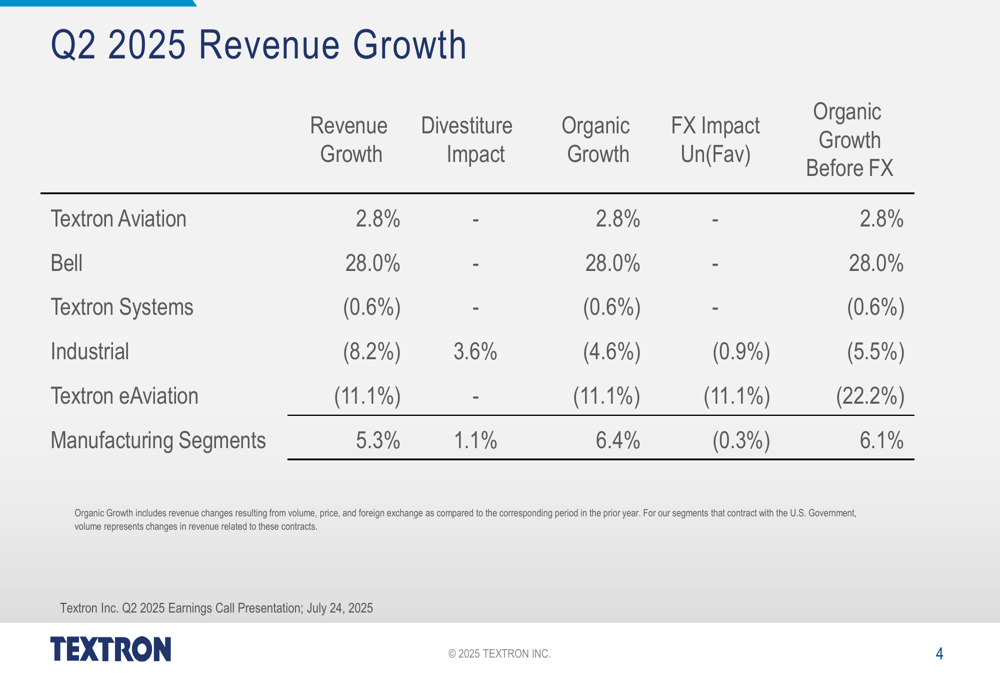

The company’s performance varied significantly across its business segments, with Bell emerging as the standout performer with 28% revenue growth year-over-year. This exceptional growth in the helicopter division contrasts sharply with declines in other segments.

Textron Aviation, the company’s aircraft manufacturing division, posted modest growth of 2.8%, while Textron Systems experienced a slight decline of 0.6%. More concerning was the performance of the Industrial segment, which saw an 8.2% revenue decline, including a 3.6% impact from divestitures. Even excluding this divestiture impact, the segment’s organic growth before foreign exchange effects was negative at 5.5%.

The company’s newest division, Textron eAviation, which focuses on electric aircraft development, also struggled with an 11.1% revenue decline. Despite these mixed results, Textron’s manufacturing segments collectively achieved 5.3% growth, or 6.1% organic growth when excluding divestiture impacts and foreign exchange effects.

Financial Metrics Deep Dive

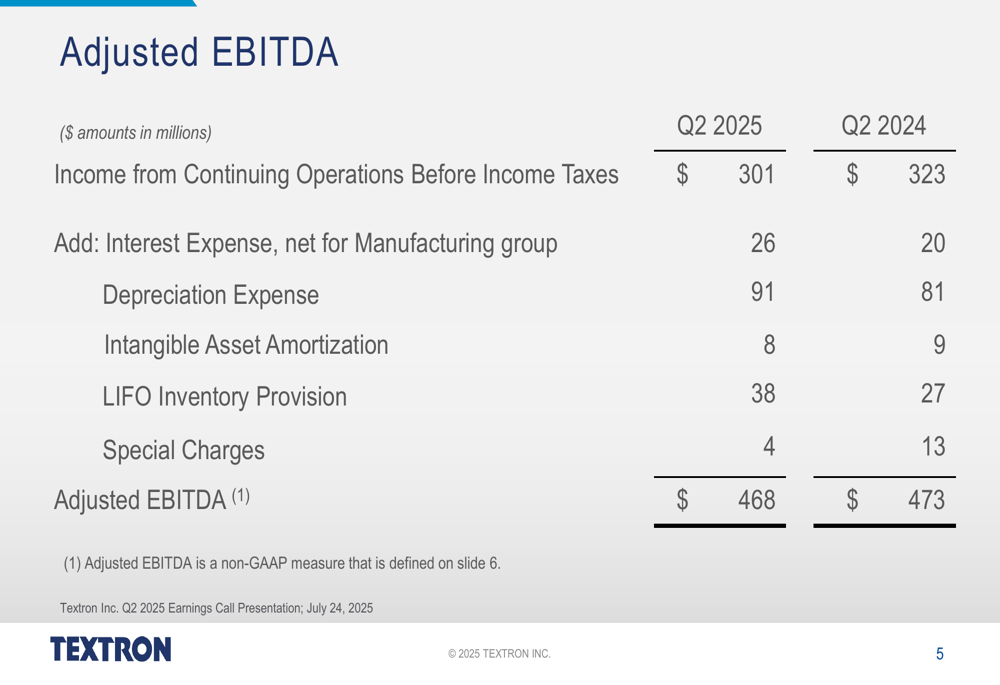

Textron’s adjusted EBITDA for Q2 2025 was $468 million, slightly down from $473 million in Q2 2024, suggesting some margin pressure despite the revenue growth. The company’s income from continuing operations before income taxes decreased to $301 million from $323 million in the prior year period.

The slight decline in adjusted EBITDA despite revenue growth indicates potential challenges in cost management or shifts in business mix toward lower-margin segments. Notable increases in certain expense categories include interest expense (up to $26 million from $20 million), depreciation expense (up to $91 million from $81 million), and LIFO inventory provisions (up to $38 million from $27 million).

These increases were partially offset by a reduction in special charges, which fell to $4 million from $13 million in the prior year period. The company’s presentation included detailed explanations of its non-GAAP financial measures, emphasizing their use in evaluating operating performance.

Forward-Looking Statements

While the presentation included standard forward-looking statements disclaimers, it did not provide specific guidance updates for the remainder of fiscal year 2025. In its previous quarter’s earnings call, Textron maintained its full-year adjusted EPS guidance between $6.00 and $6.20, with expectations for improved margins in the latter half of the year.

The company’s diverse brand portfolio positions it across multiple industries, from aviation and defense to specialized vehicles and industrial products. This diversification strategy continues to provide some insulation against weakness in individual segments, as evidenced by the overall growth despite challenges in certain divisions.

Textron’s performance in the second quarter demonstrates the company’s resilience amid varying market conditions across its business segments. The exceptional growth in the Bell segment has helped offset weaknesses elsewhere, particularly in the Industrial and eAviation divisions. While overall revenue growth is positive, the flat year-over-year EPS performance suggests ongoing challenges in translating top-line growth to bottom-line improvements. Investors will likely be watching closely for signs of margin expansion and continued cash flow generation in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.