WATCH LIVE: Investing.com reveals the top 10 stock picks for 2026

Introduction & Market Context

TGS NOPEC Geophysical Company ASA (OB:TGS) reported its second quarter 2025 results on July 17, 2025, revealing a year-over-year revenue decline but improved profit margins as the company implements strategic cost-cutting measures and vessel capacity adjustments. The geophysical services provider, which completed its merger with PGS in July 2024, faces challenging market conditions in both its multi-client and contract segments.

Total (EPA:TTEF) revenues for Q2 2025 reached $308 million, down from $381 million in the same quarter last year, while EBITDA declined to $153 million from $175 million. Despite these decreases, the company improved its EBITDA margin to 50% from 46% in Q2 2024, reflecting successful cost optimization efforts.

Quarterly Performance Highlights

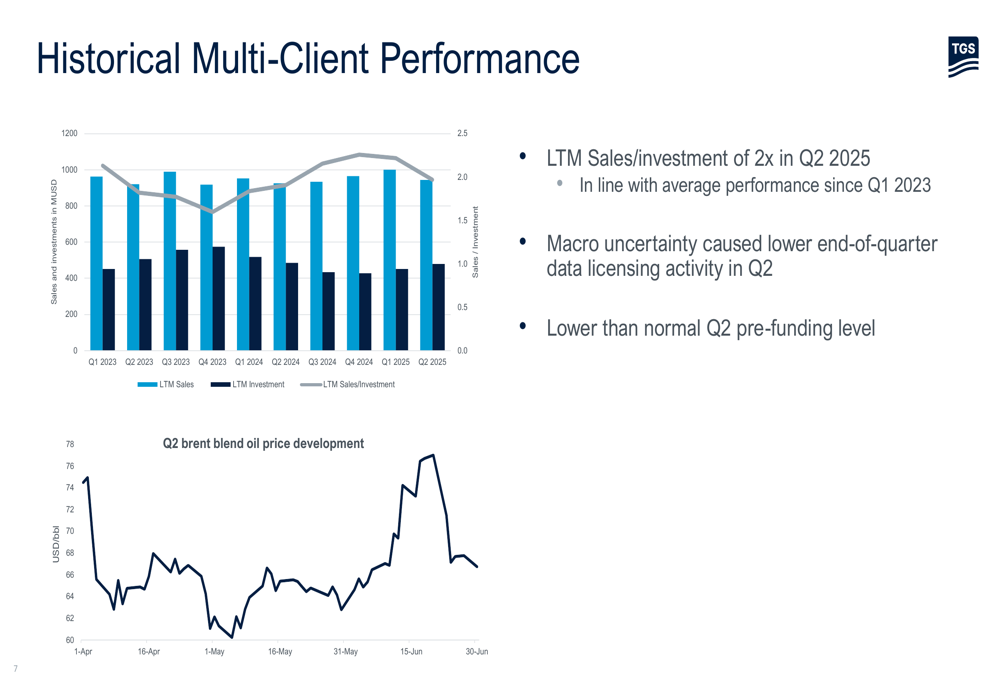

TGS reported multi-client revenues below expectations due to low library sales, with Q2 2025 multi-client sales reaching $137 million compared to $191 million in Q2 2024. The company attributed this underperformance partly to macro uncertainty causing lower end-of-quarter data licensing activity.

As shown in the following chart detailing multi-client performance, TGS maintained a last-twelve-months (LTM) sales-to-investment ratio of 2.0x, in line with average performance since Q1 2023:

Contract revenues were also negatively affected by operational challenges and lower contribution from partners. The contract segment, which includes both Ocean Bottom Node (OBN) and streamer operations, reported total gross revenues of $203 million in Q2 2025, down from $221 million in Q2 2024. However, the segment’s EBITDA margin improved to 25% from 22% in the comparable period.

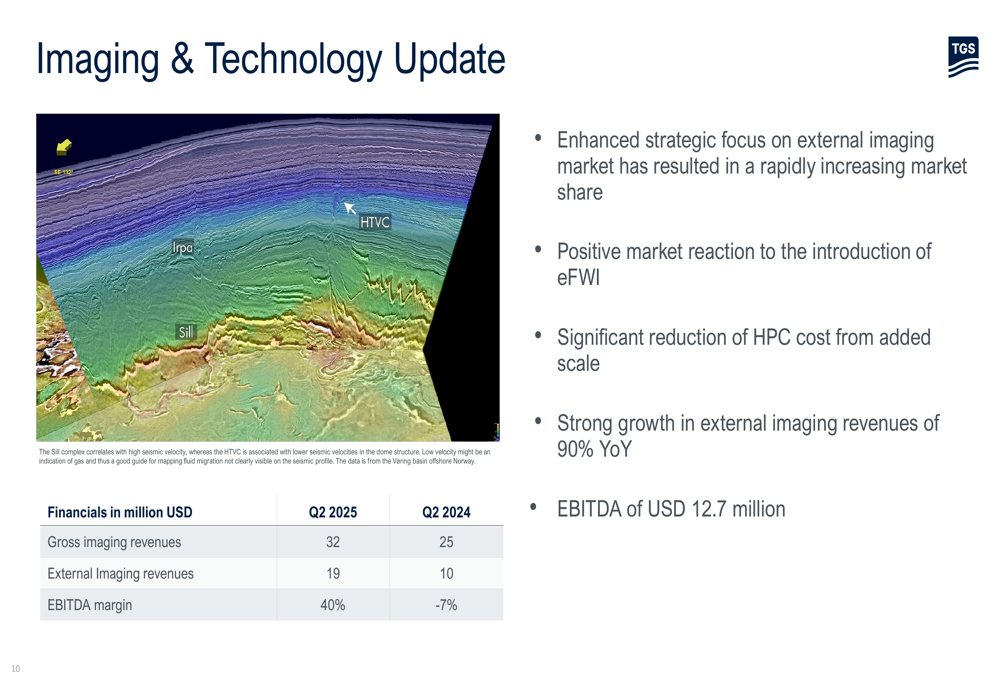

The company’s Imaging & Technology segment showed remarkable improvement, with external imaging revenues growing 90% year-over-year to $19 million in Q2 2025. The segment achieved an EBITDA margin of 40%, a dramatic turnaround from -7% in Q2 2024, driven by enhanced strategic focus on the external imaging market and significant reduction in High-Performance Computing (HPC) costs.

As shown in the following chart, the Imaging & Technology segment has made substantial progress:

The New Energy Solutions (NES) segment maintained stable revenues of $18 million, matching Q2 2024 performance, while improving its EBITDA margin to 31% from 20%. This segment continues to develop with recent achievements including a new Ultra-High Resolution 3D (UHR-3D) contract offshore Norway and a collaboration with Equinor to drive digital transformation in Carbon Capture and Storage (CCS) operations.

Strategic Initiatives

A key focus of TGS’s presentation was its strategic vessel capacity reduction to address current market conditions. The company has agreements to sell two vessels—Ramform Explorer and Ramform Valiant—with sales contracts prohibiting their use as seismic/source vessels. Additionally, TGS is stacking the Ramform Vanguard and a multi-purpose vessel used for seismic and offshore wind acquisition projects.

As illustrated in the following slide, TGS is taking decisive action to adjust its fleet capacity:

The company is also reviewing its OBN vessel strategy, noting that all OBN vessels are chartered with staggered expiry dates allowing for gradual release. Management indicated that 2026 outlook may warrant new charters during the year, showing a flexible approach to capacity management.

TGS continues to optimize its business operations, reducing its gross operating cost target to approximately $950 million for 2025, down from the previous target of approximately $1,000 million. This cost reduction, combined with the vessel capacity adjustments, demonstrates management’s proactive approach to navigating challenging market conditions.

Market Context and Outlook

TGS provided valuable industry context, highlighting that several International Oil Companies (IOCs) have reserve life oil of approximately 7 years and an average 3-year rolling reserve replacement ratio of about 40%. This suggests that exploration activities will need to increase to secure sufficient energy reserves, potentially benefiting TGS’s services in the medium to long term.

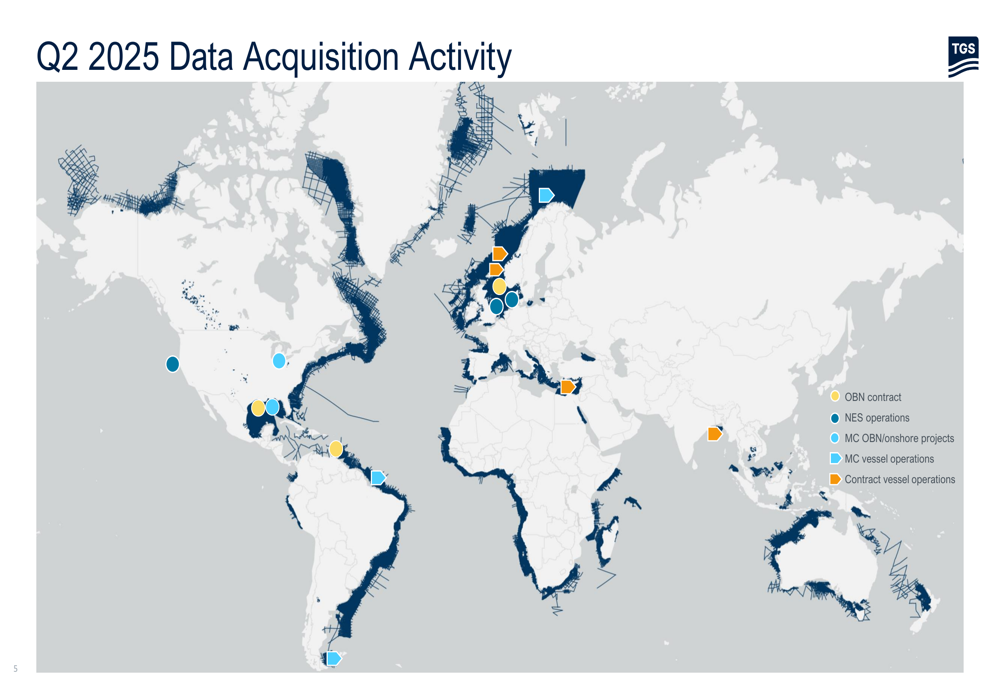

The company’s global data acquisition activity in Q2 2025 spanned multiple regions, with notable concentration in the North Sea, Gulf of Mexico, and off the coasts of Brazil and India:

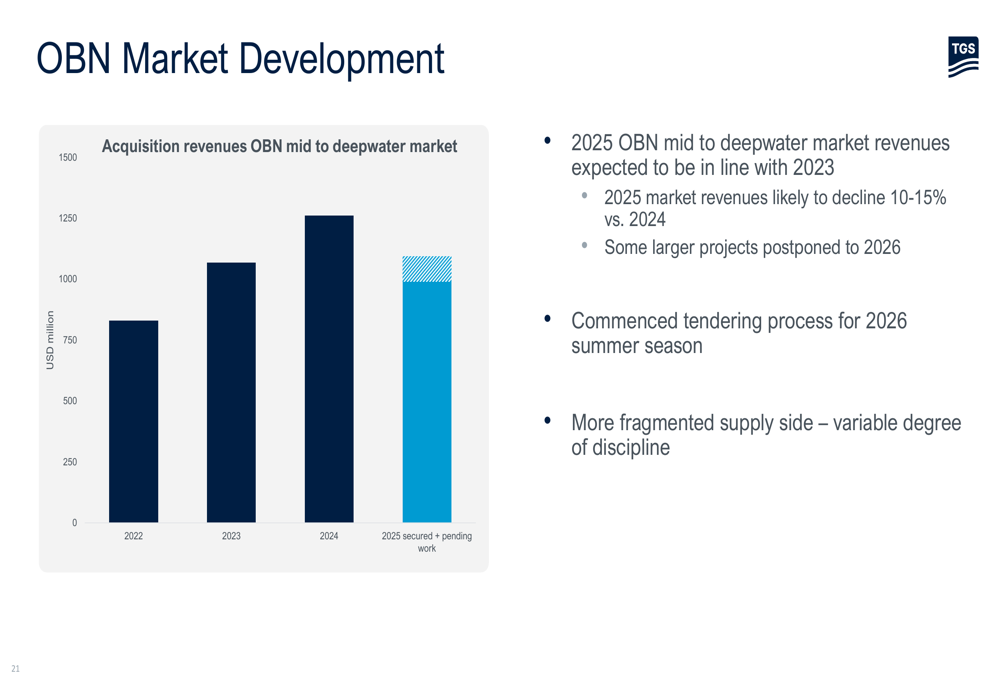

For the OBN market specifically, TGS expects 2025 mid to deepwater market revenues to be in line with 2023 but likely to decline 10-15% versus 2024, with some larger projects postponed to 2026. The company has commenced tendering for the 2026 summer season and noted a more fragmented supply side with variable degrees of discipline.

As shown in the following chart of OBN market development:

Despite near-term challenges, TGS maintained its 2025 guidance for multi-client investment at $425-475 million and capital expenditures at approximately $135 million (excluding approximately $10 million of integration-related capex). The company expects improved utilization of its 3D streamer fleet in the remainder of 2025, though with lower OBN acquisition activity compared to 2024.

Forward-Looking Statements

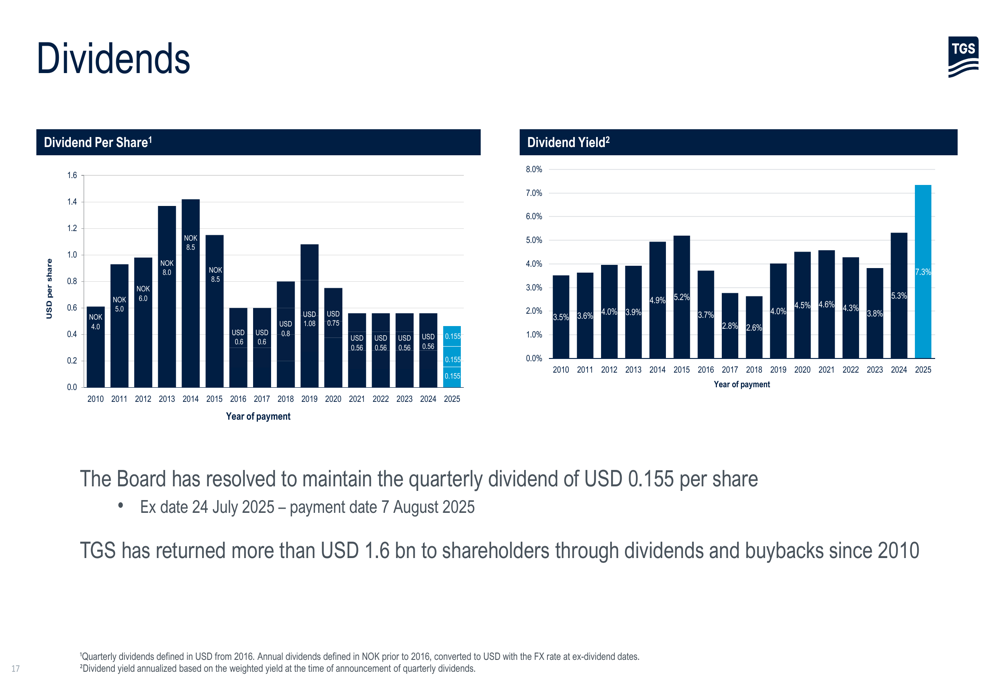

TGS maintained its quarterly dividend of $0.155 per share, with an ex-date of July 24, 2025, and payment date of August 7, 2025. The company highlighted that it has returned more than $1.6 billion to shareholders through dividends and buybacks since 2010, with the current dividend yield at 7.3%.

The following chart illustrates TGS’s consistent dividend history:

For Q3 2025, TGS expects multi-client investment of approximately $90 million, vessel utilization of approximately 65%, and a normalized OBN crew count of about 2.5. The company’s total order backlog stood at $425 million at the end of Q2 2025.

CEO Kristian Johansen and CFO Sven Børre Larsen emphasized that while short-term market development remains sensitive to oil price fluctuations, the long-term market outlook remains positive. The company’s strategy of business optimization through cost reduction and vessel capacity adjustment positions TGS to navigate current market headwinds while maintaining operational flexibility for future opportunities.

In contrast to the Q1 2025 results, which showed revenue growth to $451 million and EBITDA of $258 million, the Q2 2025 performance reflects a more challenging market environment. However, TGS’s improved margins and strategic adjustments demonstrate management’s ability to adapt to changing conditions while maintaining shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.