Dubai Holding and Palantir create joint venture Aither for AI transformation

Introduction & Market Context

The Hartford Financial Services Group (NYSE:HIG) presented its third-quarter 2025 financial results on October 27, showcasing record core earnings despite a challenging market environment. The insurance giant reported core earnings of $1.1 billion, translating to earnings per share of $3.78, significantly outperforming analyst expectations of $3.09. Despite these strong results, Hartford’s stock dipped 2.29% in after-hours trading to $122.66, reflecting broader market volatility rather than company-specific concerns.

The company demonstrated robust performance across most business segments, with particularly strong results in its Property & Casualty operations, while maintaining disciplined underwriting and pricing strategies in a competitive insurance landscape.

Quarterly Performance Highlights

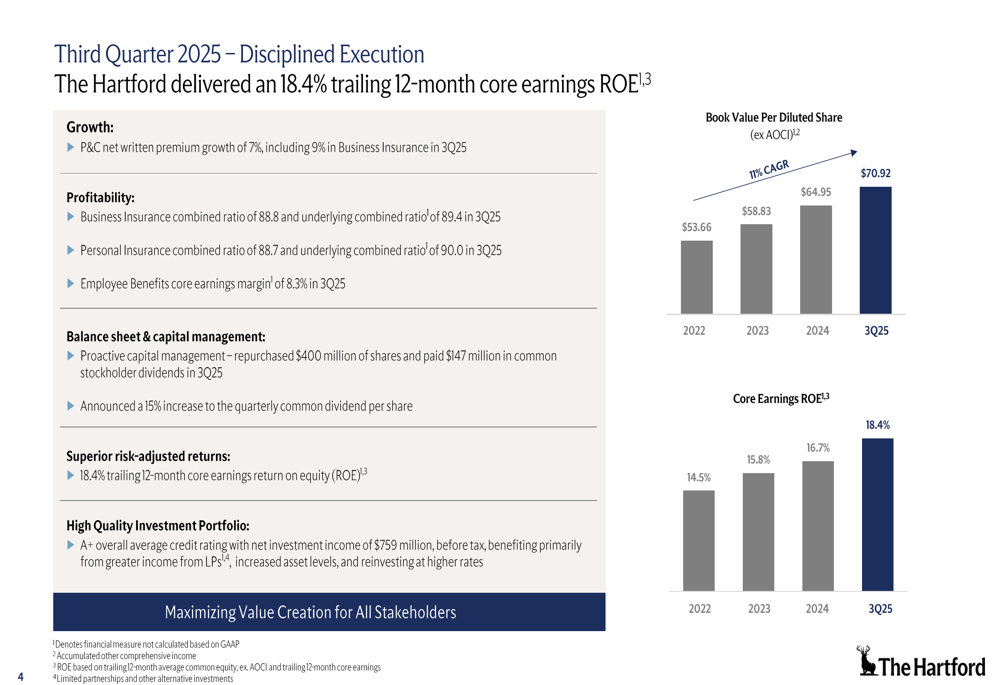

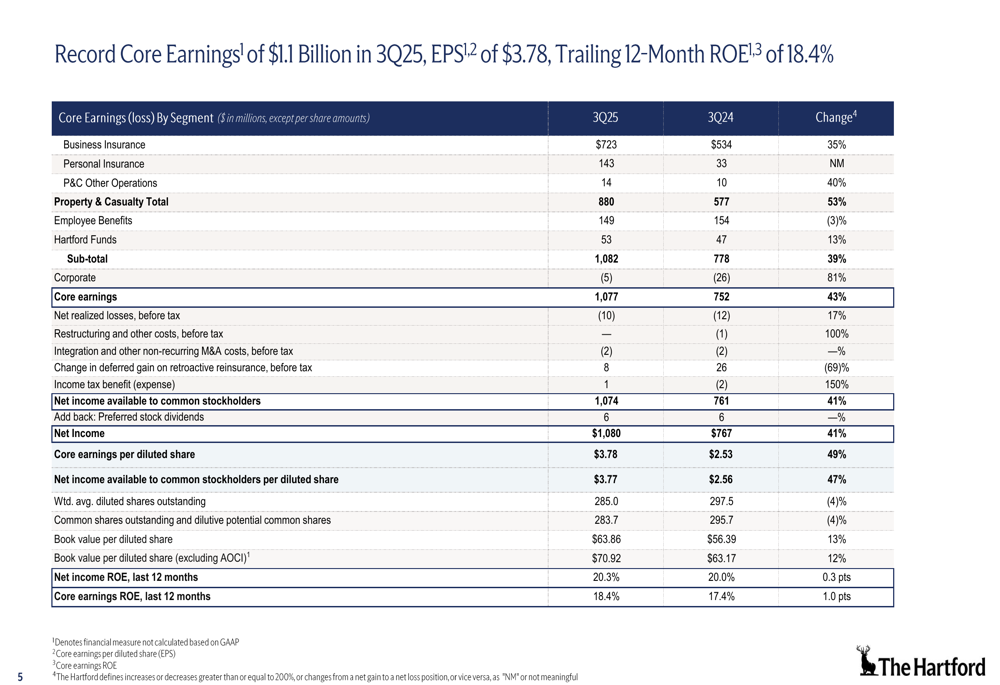

The Hartford delivered record core earnings of $1.1 billion in the third quarter, representing a 43% increase from the $752 million reported in Q3 2024. This performance translated to core earnings per diluted share of $3.78, up from $2.53 in the same period last year.

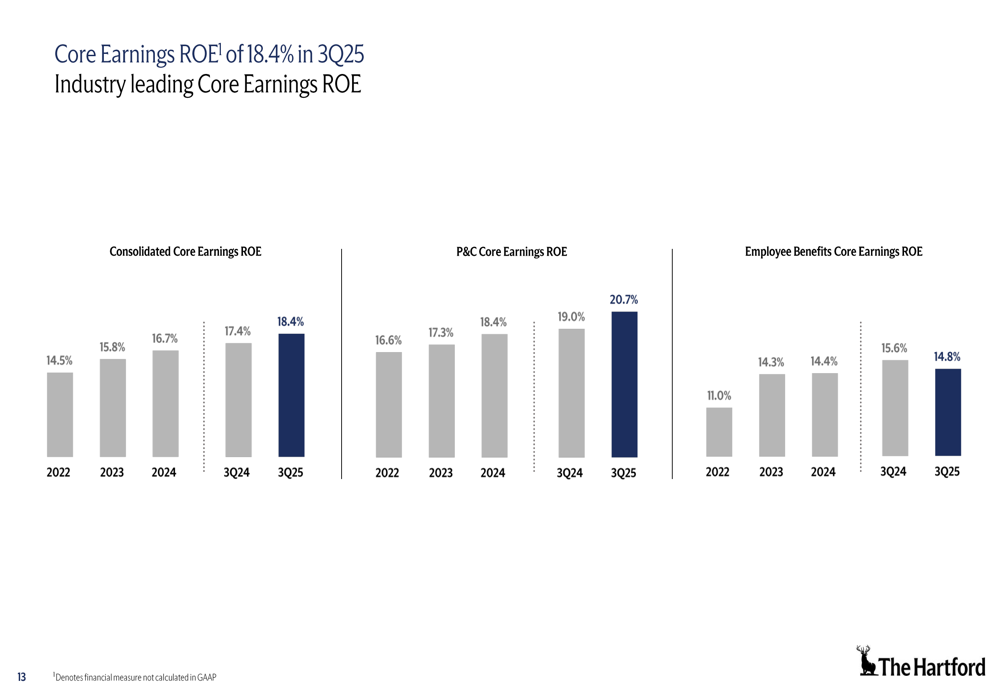

The company’s trailing 12-month core earnings return on equity (ROE) reached 18.4%, continuing an upward trajectory from 14.5% in 2022 and 16.7% in 2024. Book value per diluted share (excluding AOCI) grew to $70.92, representing an 11% compound annual growth rate since 2022.

As shown in the following chart of quarterly performance metrics:

Property & Casualty written premiums grew by 7% year-over-year, with Business Insurance leading the way with 9% growth. The combined ratios showed significant improvement, with Business Insurance at 88.8 (down 3.4 points) and Personal Insurance at 88.7 (down 13.8 points), reflecting enhanced underwriting discipline and favorable pricing trends.

The detailed breakdown of core earnings by segment reveals the strength of the company’s diversified business model:

Detailed Financial Analysis

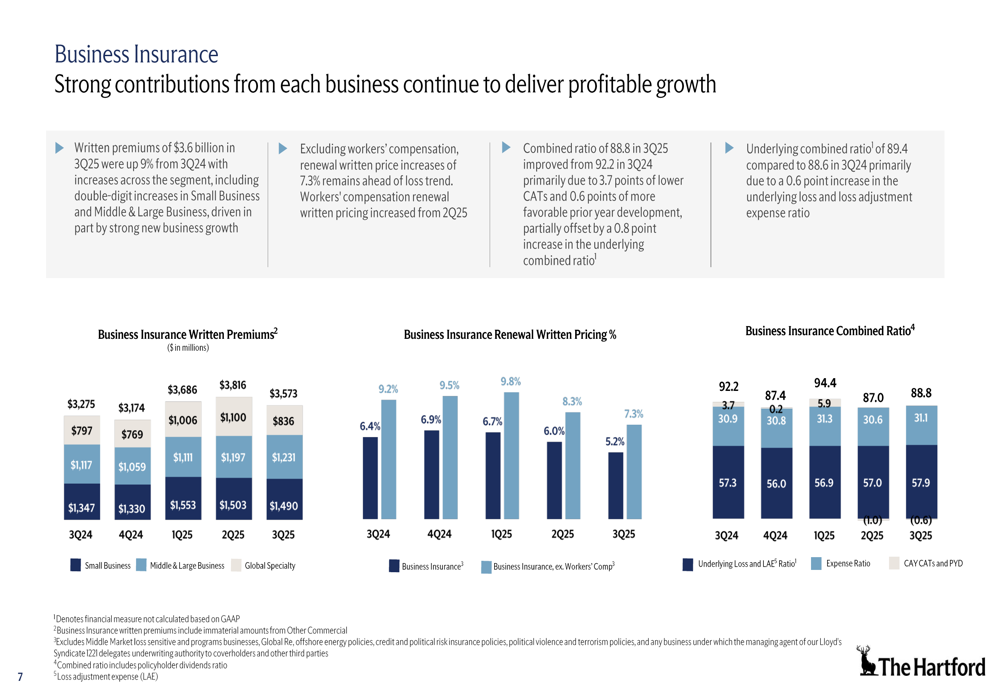

Business Insurance Performance

The Business Insurance segment, which contributes 55% of The Hartford’s revenue, delivered particularly strong results with written premiums of $3.6 billion, up 9% year-over-year. The segment’s combined ratio improved to 88.8% from 92.2% in Q3 2024, while maintaining disciplined pricing with renewal written price increases of 7.3% (excluding workers’ compensation), which the company noted remains ahead of loss trends.

The following chart illustrates Business Insurance performance metrics:

Personal Insurance Performance

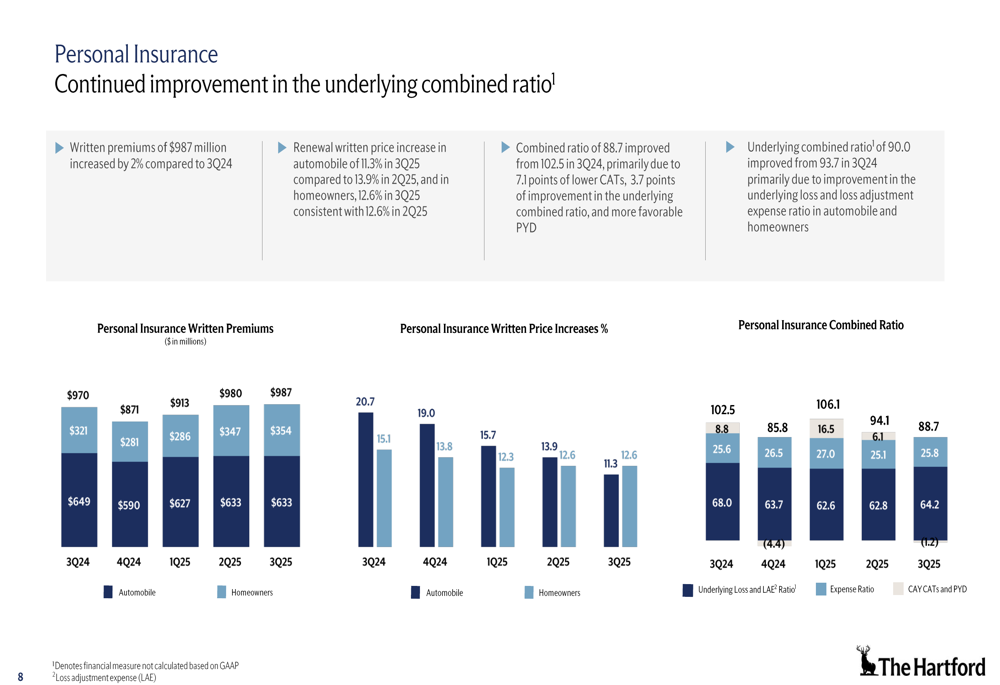

The Personal Insurance segment showed remarkable improvement with a combined ratio of 88.7, a dramatic 13.8-point enhancement from 102.5 in Q3 2024. Written premiums grew 2% to $987 million, supported by strong renewal pricing in both automobile (11.3%) and homeowners (12.6%) lines.

The underlying combined ratio improved to 90.0 from 93.7 in the prior year, demonstrating the effectiveness of The Hartford’s pricing and underwriting actions in this previously challenged segment.

As shown in the following chart of Personal Insurance metrics:

Employee Benefits and Hartford Funds

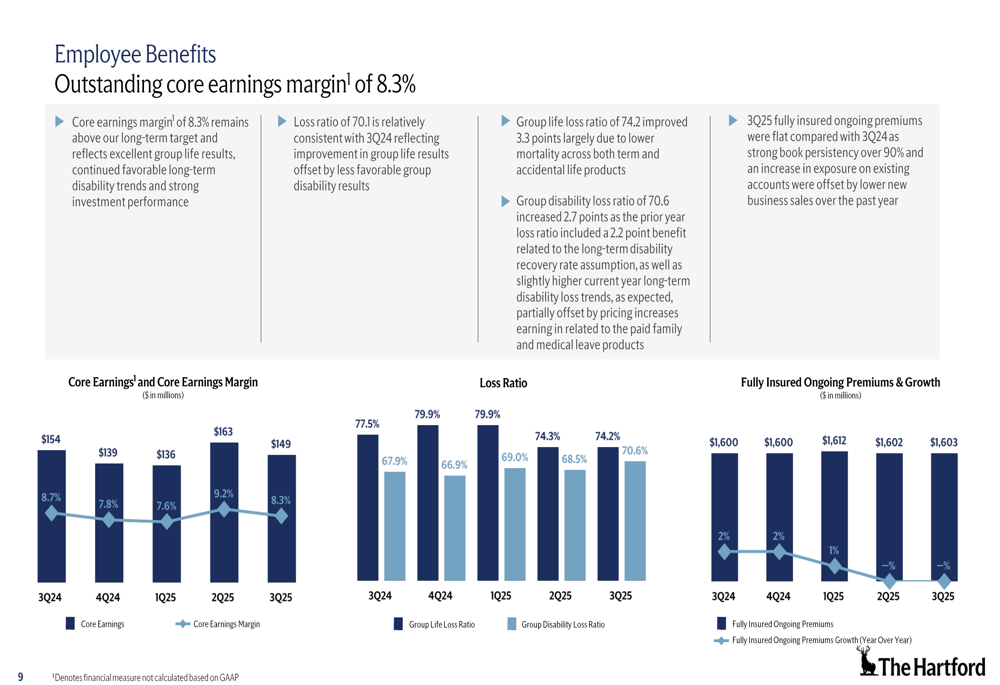

The Employee Benefits segment reported core earnings of $149 million, slightly down 3% from $154 million in Q3 2024, but maintained a strong core earnings margin of 8.3%. This performance reflects excellent group life results, favorable long-term disability trends, and strong investment performance.

The segment’s loss ratios showed improvement, with the life loss ratio decreasing 3.3 points to 74.2% and the disability loss ratio improving 2.7 points to 70.6%.

The Employee Benefits performance is illustrated in this chart:

Hartford Funds contributed $53 million to core earnings, up 13% from the prior year, despite experiencing net outflows of $25 million. The company noted that 57% of overall funds are outperforming peers on a 1-year basis.

Capital Management & Investment Portfolio

The Hartford maintained a strong focus on capital management during the quarter, repurchasing $400 million of shares and paying $147 million in common stock dividends. The company also announced a 15% increase to the quarterly common dividend per share, demonstrating confidence in its financial position and future prospects.

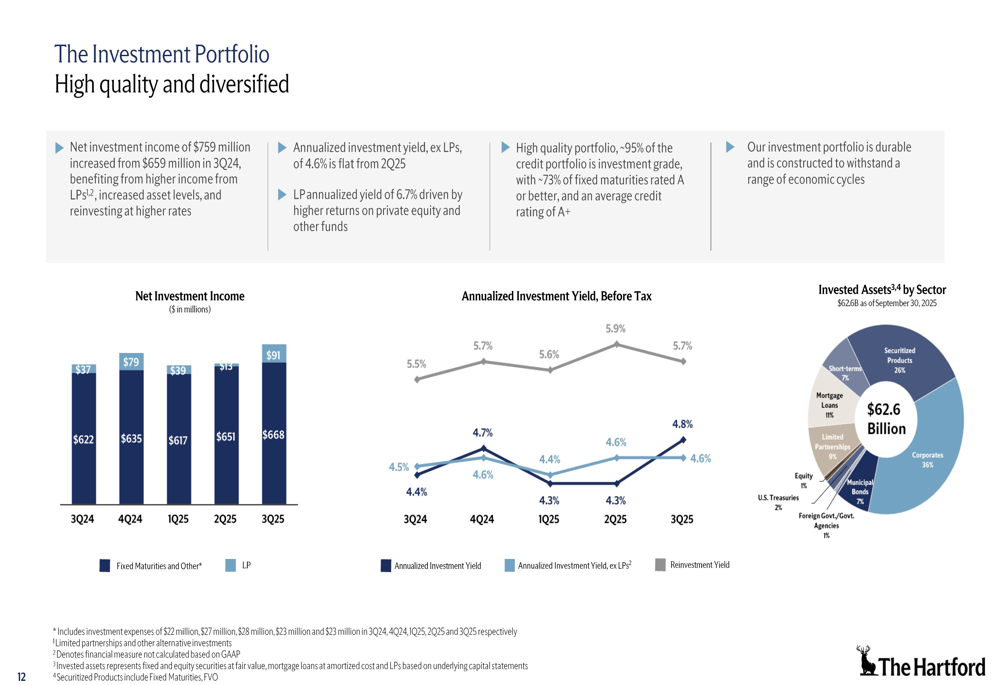

Net investment income rose to $759 million, up from $659 million in Q3 2024, benefiting primarily from greater income from limited partnerships, increased asset levels, and reinvestment at higher rates. The annualized investment yield, excluding limited partnerships, held steady at 4.6% quarter-over-quarter.

The investment portfolio and income trends are illustrated in the following chart:

The company maintains a high-quality investment portfolio with an A+ overall average credit rating, providing stability in uncertain economic conditions.

Forward-Looking Statements

Looking ahead, The Hartford remains positioned for continued strong performance, building on its market leadership in desirable segments and leveraging core underwriting strengths. The company’s focus on disciplined execution has driven consistent improvement in key metrics, with book value per diluted share growing at an 11% compound annual growth rate since 2022.

The following chart illustrates the consistent improvement in core earnings ROE across segments:

Despite the positive earnings report, investors should note that Hartford’s stock declined in after-hours trading, possibly reflecting broader market concerns rather than company-specific issues. According to the earnings call, the company plans to continue its investments in digital capabilities and AI-driven underwriting, with an IT budget of $1.3 billion, including over $500 million for investment projects.

CEO Christopher Swift emphasized during the earnings call that technology investments are intended to "augment our human talent, not necessarily to replace it," highlighting the company’s balanced approach to innovation while maintaining its people-focused culture.

With strong pricing trends, disciplined underwriting, and a robust capital position, The Hartford appears well-positioned to navigate market challenges while delivering sustainable shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.