Fed Governor Adriana Kugler to resign

Introduction & Market Context

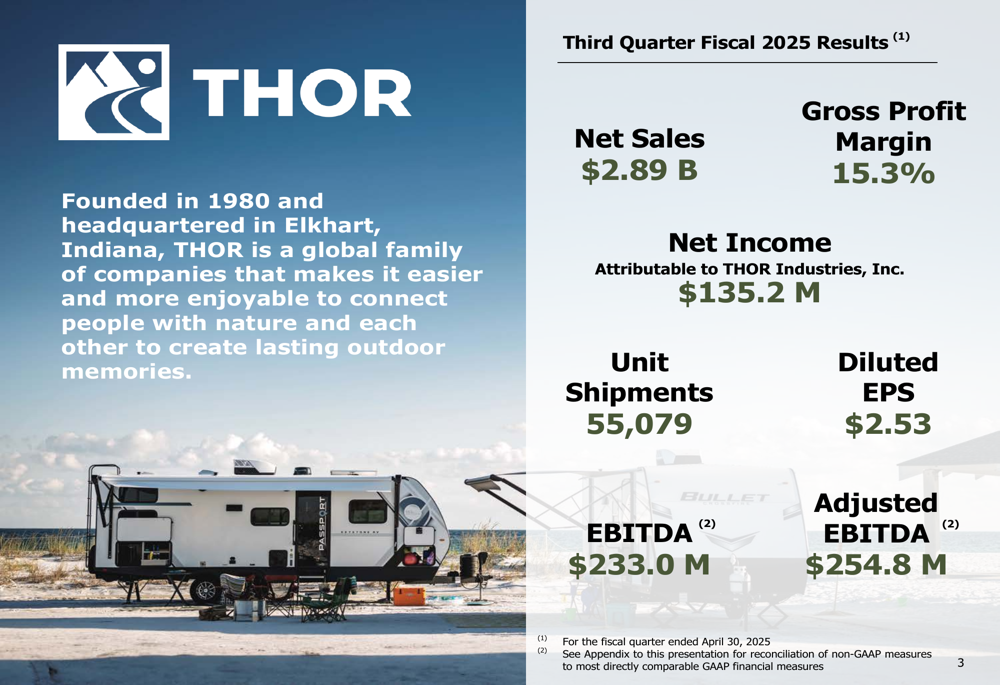

Thor Industries (NYSE:THO) reported third-quarter fiscal 2025 results on June 4, 2025, with net sales rising 3.3% year-over-year to $2.89 billion, exceeding market expectations. The company’s shares responded positively in premarket trading, jumping 8.53% to $89.44 following the announcement, as investors welcomed the better-than-anticipated performance amid challenging market conditions.

The global RV leader delivered these results against a backdrop of shifting market dynamics and macroeconomic conditions, with varied performance across its geographic segments. North American operations showed strength while European markets faced headwinds.

Quarterly Performance Highlights

Thor Industries reported net income of $135.2 million for Q3 FY2025, translating to diluted earnings per share of $2.53. The company maintained a solid gross profit margin of 15.3%, demonstrating resilience in its operational efficiency despite market pressures.

As shown in the following financial summary:

The company’s EBITDA reached $233.0 million, with adjusted EBITDA of $254.8 million. This performance came as Thor shipped 55,079 units during the quarter, with varying results across its three main business segments.

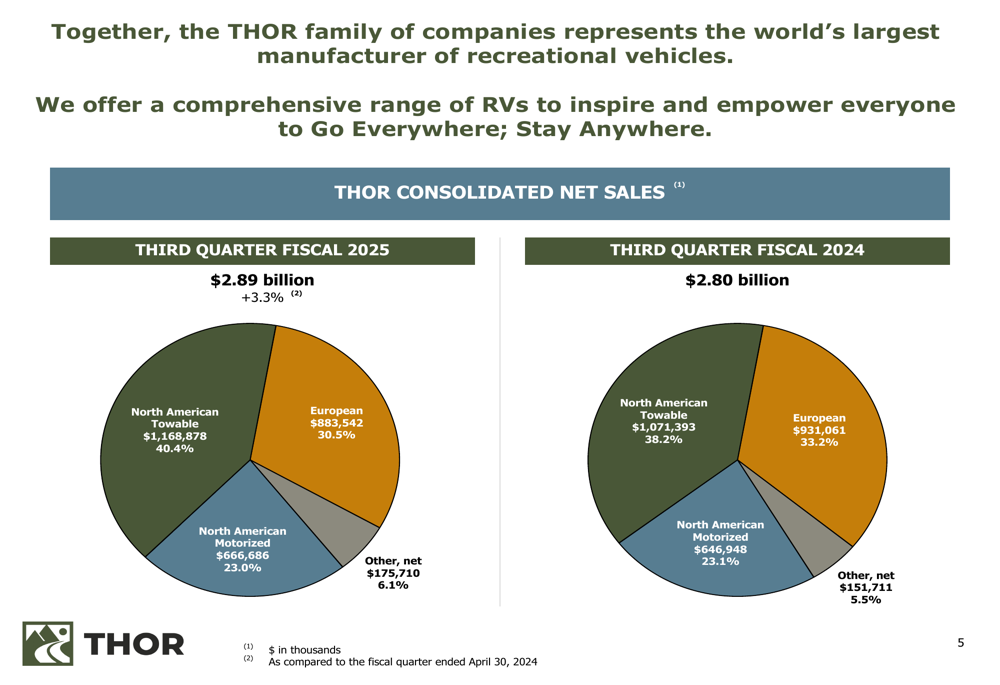

Breaking down the revenue by segment shows the shifting dynamics of Thor’s business mix:

North American Towable products represented the largest segment at 40.4% of total sales ($1.17 billion), followed by European operations at 30.5% ($883.5 million) and North American Motorized at 23.0% ($666.7 million). Notably, the North American Towable segment increased its share of total revenue compared to the same period last year, while the European segment’s contribution declined.

Segment Analysis

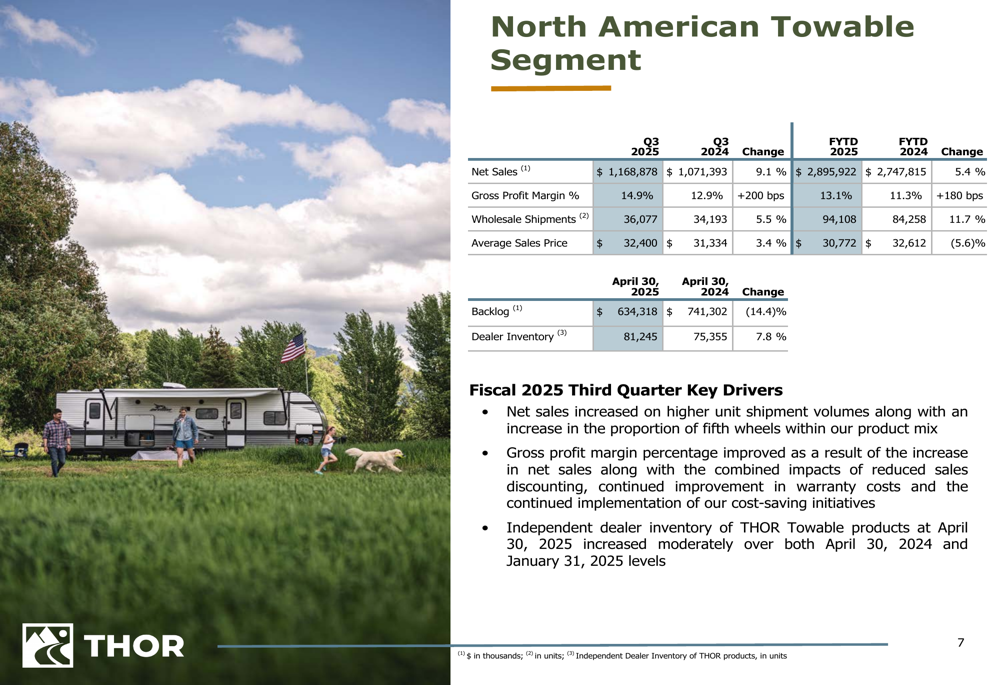

North American Towable Segment

The North American Towable segment delivered strong results with net sales increasing 9.1% to $1.17 billion. Unit shipments grew 5.5% to 36,077 units, though the average sales price decreased slightly to $32,400 per unit. The segment achieved a gross profit margin of 14.9%.

Key drivers for this segment included higher unit volumes and an improved product mix with more fifth wheels, as well as reduced sales discounting and improved warranty costs:

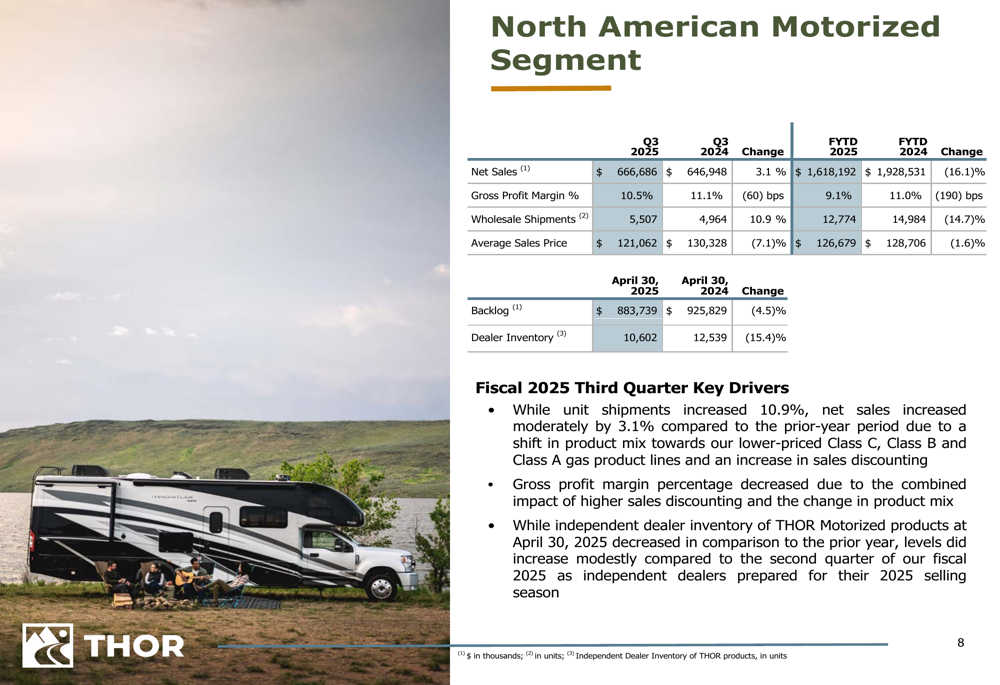

North American Motorized Segment

The North American Motorized segment saw net sales increase by 3.1% to $666.7 million, with unit shipments up 10.9% to 5,507 units. However, the average sales price decreased to $121,062 per unit due to a shift toward lower-priced product lines and increased sales discounting. This product mix shift contributed to a lower gross profit margin of 10.5%.

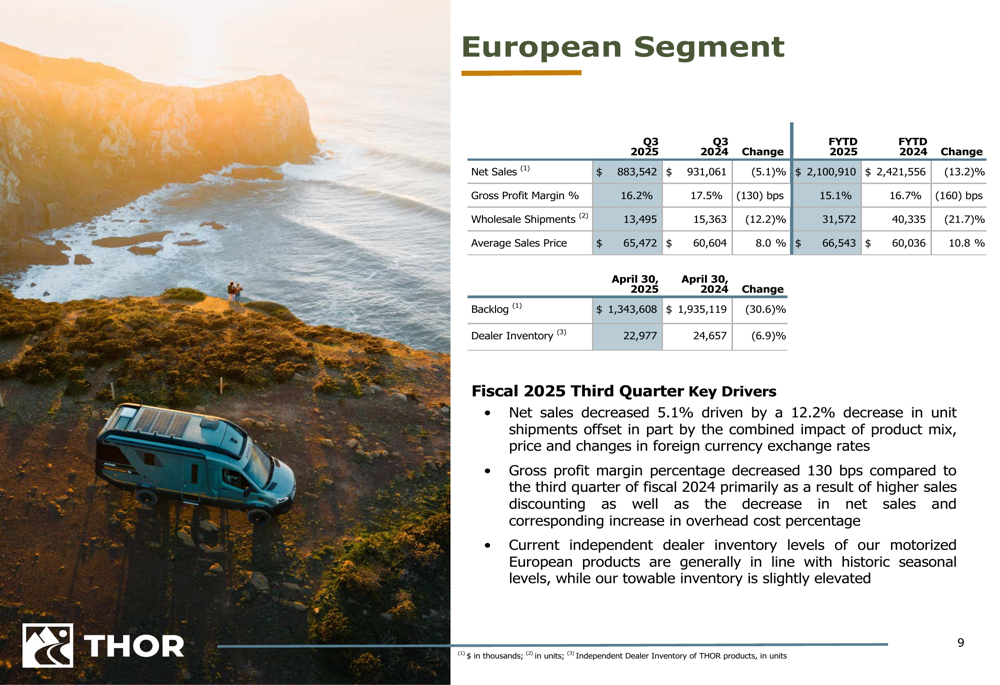

European Segment

Thor’s European operations faced the most significant challenges during the quarter, with net sales decreasing 5.1% to $883.5 million. Unit shipments declined 12.2% to 13,495 units, though the average sales price increased by 8.0% to $65,472 per unit. The gross profit margin decreased to 16.2%, down 130 basis points from the prior year.

Management attributed the European performance to higher sales discounting and decreased net sales leading to increased overhead cost percentages. The company noted that motorized European product inventory is in line with historic seasonal levels, while towable inventory remains slightly elevated.

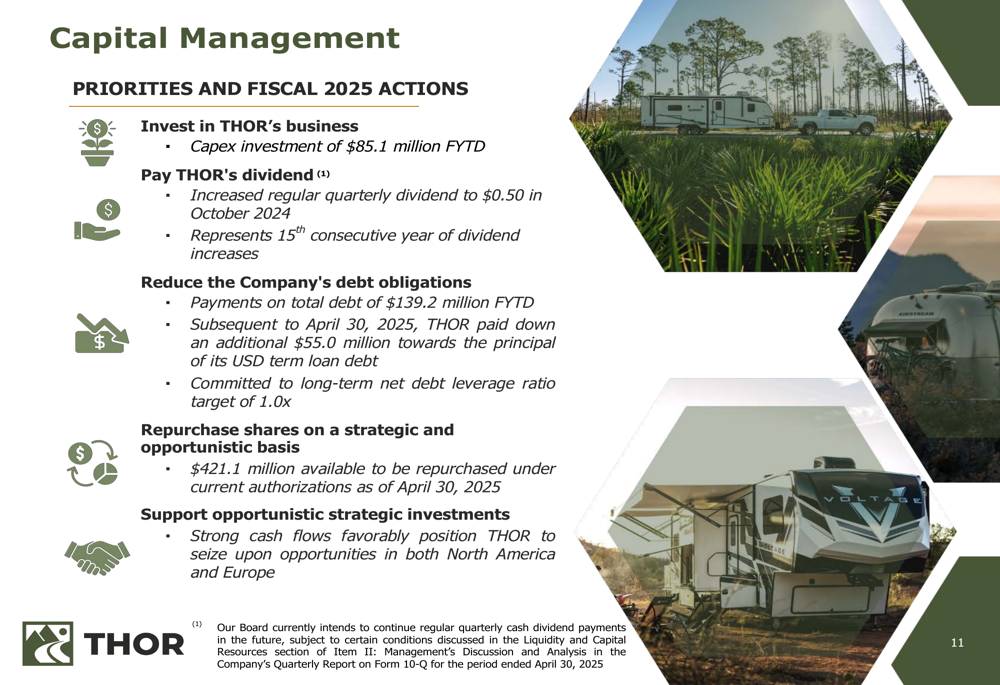

Financial Position & Capital Management

Thor Industries maintained a strong financial position with total liquidity of $1.49 billion as of April 30, 2025, including $508.3 million in cash and cash equivalents and $985.0 million available under its revolving credit facility. The company’s outstanding debt stood at $1.03 billion, resulting in a net debt to trailing twelve-month adjusted EBITDA ratio of 0.8x.

Cash flow from operating activities for the fiscal year to date reached $319.2 million, representing an improvement of over $100 million compared to the same period last year.

The company’s capital management priorities demonstrate a balanced approach to shareholder returns and financial strength:

Thor has invested $85.1 million in capital expenditures fiscal year to date while increasing its quarterly dividend to $0.50 in October 2024, marking the 15th consecutive year of dividend increases. The company has also reduced its debt obligations by $139.2 million fiscal year to date, with an additional $55.0 million paid down after the quarter ended.

Guidance & Outlook

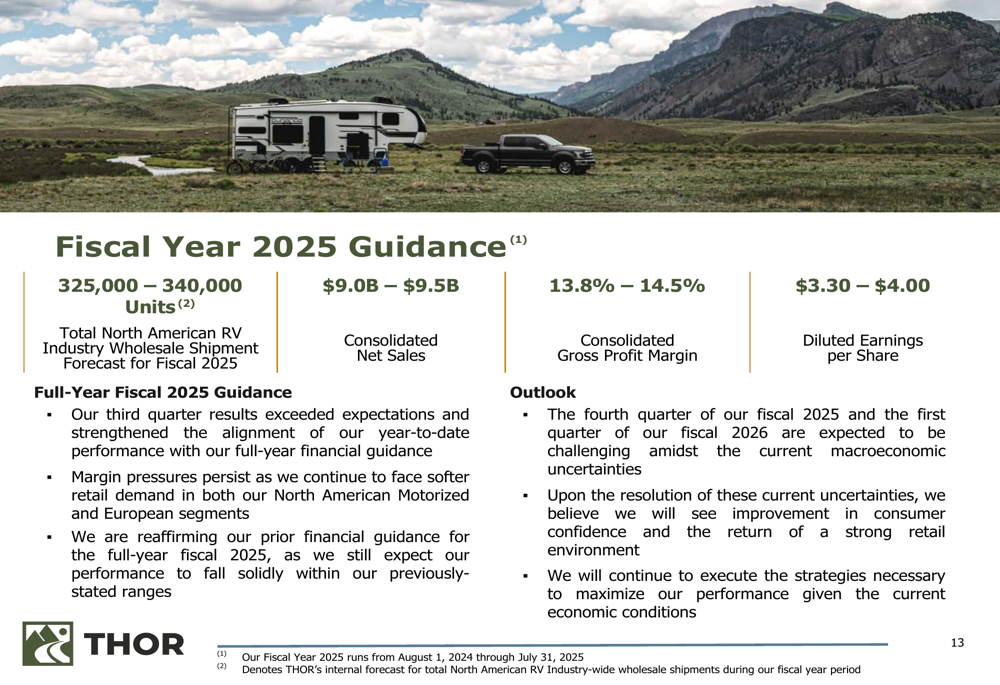

Looking ahead, Thor Industries provided guidance for fiscal year 2025, projecting consolidated net sales between $9.0 billion and $9.5 billion, with a consolidated gross profit margin of 13.8% to 14.5%. The company expects diluted earnings per share to range from $3.30 to $4.00.

The company forecasts North American RV industry wholesale shipments between 325,000 and 340,000 units for fiscal year 2025. Management noted expectations for challenges in the fourth quarter of fiscal 2025 and the first quarter of fiscal 2026.

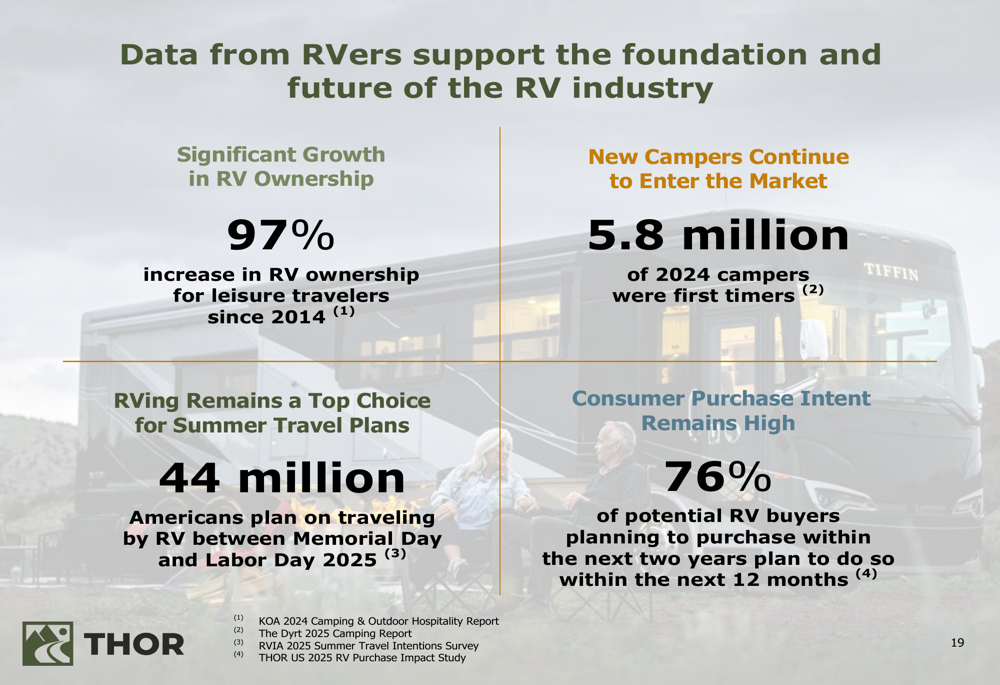

Despite these near-term challenges, Thor highlighted several positive industry trends supporting the long-term outlook for the RV market:

These trends include a 97% increase in RV ownership among leisure travelers since 2014, 5.8 million first-time campers in 2024, and 44 million Americans planning to travel by RV between Memorial Day and Labor Day 2025. Additionally, 76% of potential RV buyers planning to purchase within the next two years intend to do so within the next 12 months.

Strategic Initiatives

During the quarter, Thor announced a strategic organizational restructuring to align operations with current market conditions. While specific details of the restructuring were not extensively covered in the presentation, management emphasized that this initiative, along with ongoing cost-saving measures, contributed to the company’s ability to deliver resilient margins despite market challenges.

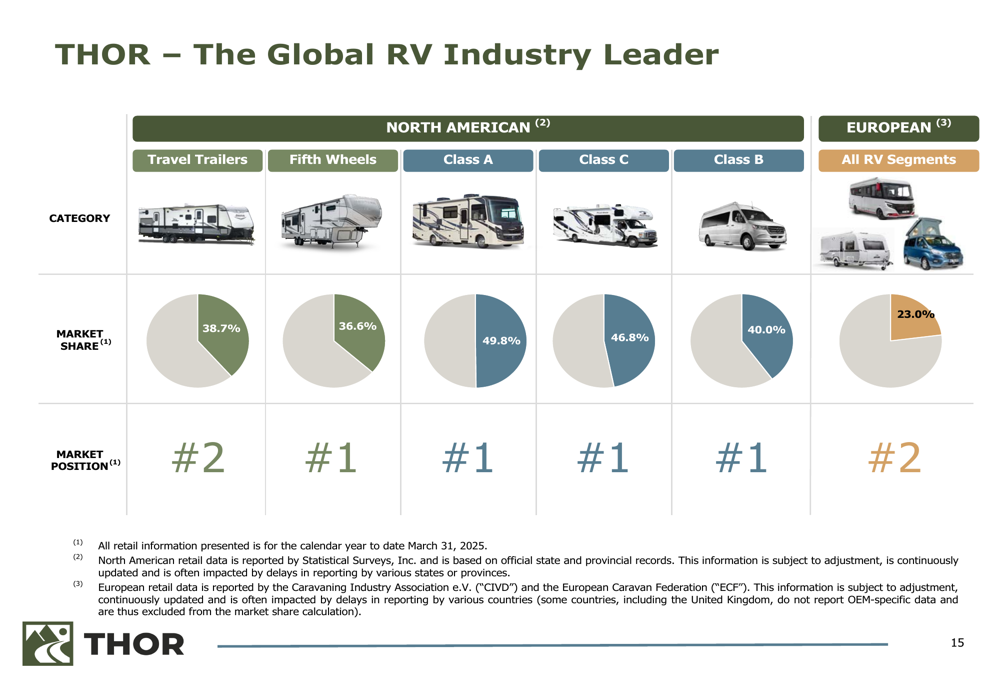

Thor continues to maintain its position as the global RV industry leader, with significant market share across multiple product categories:

The company holds the number one market position in North America for Fifth Wheels (36.6%), Class A RVs (49.8%), Class C RVs (46.8%), and Class B RVs (40.0%), while maintaining the number two position in North American Travel Trailers (38.7%) and European RV segments (23.0%).

Conclusion

Thor Industries’ third quarter fiscal 2025 results demonstrated the company’s ability to navigate varying market conditions across its global operations. Strong performance in North American segments offset weakness in European markets, resulting in overall sales growth and financial results that exceeded expectations.

The company’s focus on debt reduction, cost management, and strategic restructuring positions it to weather potential near-term challenges while maintaining the financial flexibility to capitalize on long-term growth opportunities in the RV industry. With a strong balance sheet, diverse brand portfolio, and leading market positions, Thor appears well-positioned despite its cautious outlook for the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.