Street Calls of the Week

Introduction & Market Context

Transcat Inc. (NASDAQ:TRNS), a provider of calibration services and test equipment distribution, presented its fourth quarter and full-year fiscal 2025 financial results on May 20, 2025, showcasing solid revenue growth despite macroeconomic headwinds. The company’s stock surged 17.09% following the announcement, reflecting investor confidence in its long-term strategy despite some quarterly earnings pressure.

The Rochester, NY-based company reported consolidated revenue growth of 9% for the quarter and 7% for the full year, with particularly strong performance in its Service segment, which continues to be the centerpiece of Transcat’s growth strategy.

Quarterly Performance Highlights

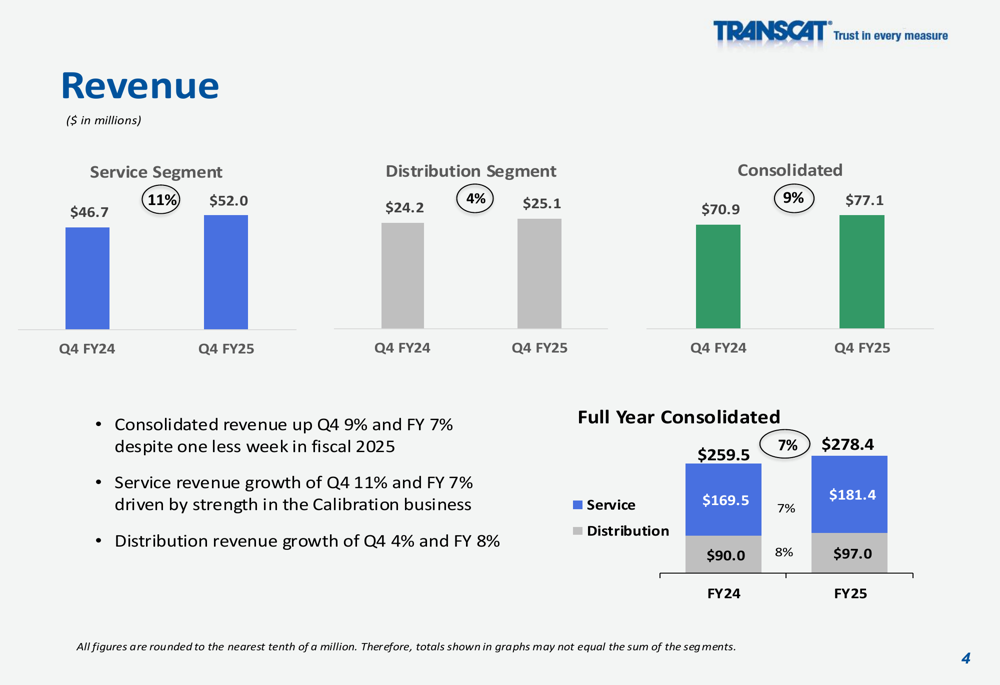

Transcat delivered Q4 FY25 revenue of $77.1 million, representing a 9% increase year-over-year and slightly exceeding analyst expectations of $76.67 million. The Service segment led this growth with an 11% revenue increase to $52.0 million, while the Distribution segment contributed a 4% increase to $25.1 million.

As shown in the following revenue performance breakdown:

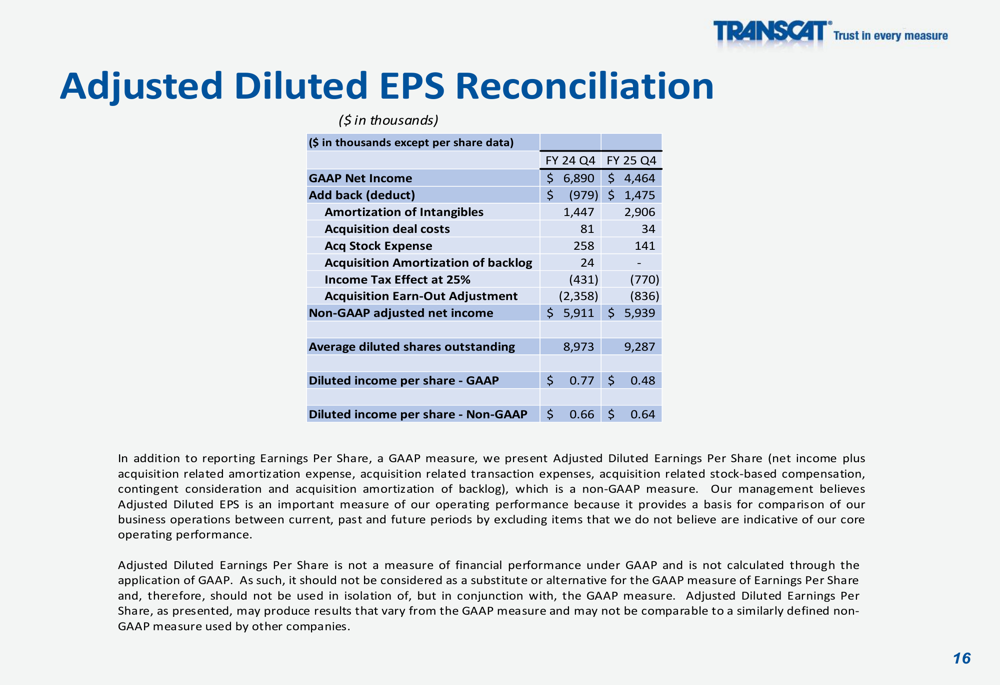

Despite the revenue growth, Q4 net income decreased to $4.5 million from $6.9 million in the prior year, with diluted earnings per share declining from $0.77 to $0.48. However, on an adjusted basis, EPS was $0.64, only slightly below the prior year’s $0.66 and consistent with the company’s expectations.

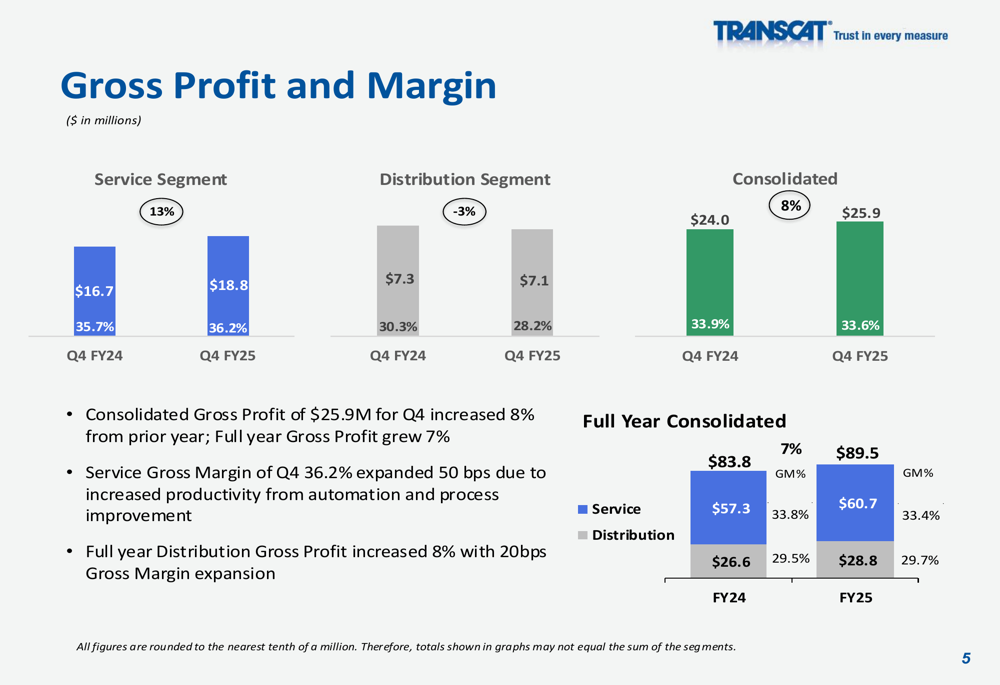

The company’s gross profit performance showed strength, particularly in the Service segment where gross margin expanded by 50 basis points to 36.2%, driven by increased productivity from automation and process improvements:

Detailed Financial Analysis

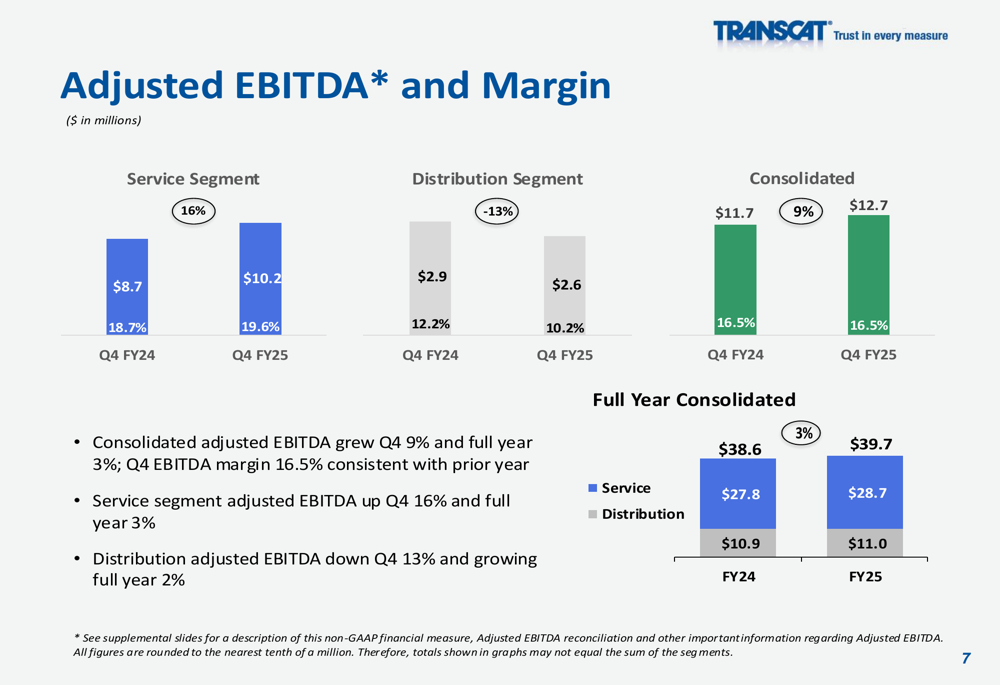

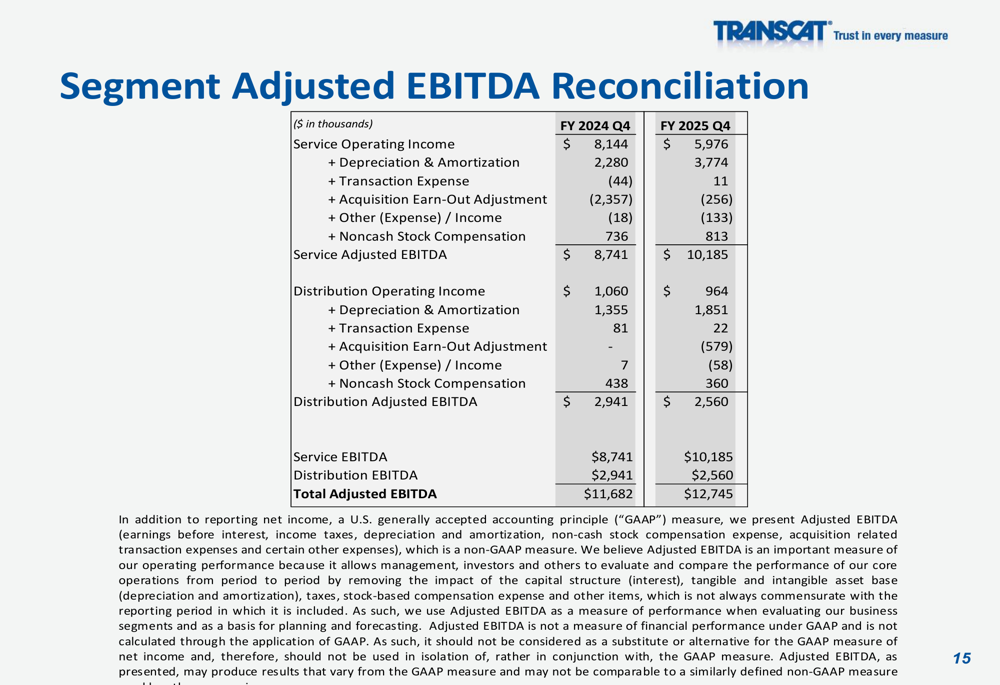

Transcat’s adjusted EBITDA for Q4 increased 9% year-over-year to $12.7 million, maintaining a consistent margin of 16.5%. The Service segment showed particularly strong adjusted EBITDA growth of 16% to $10.2 million, while the Distribution segment saw a 13% decrease to $2.6 million.

The following chart illustrates the adjusted EBITDA performance across segments:

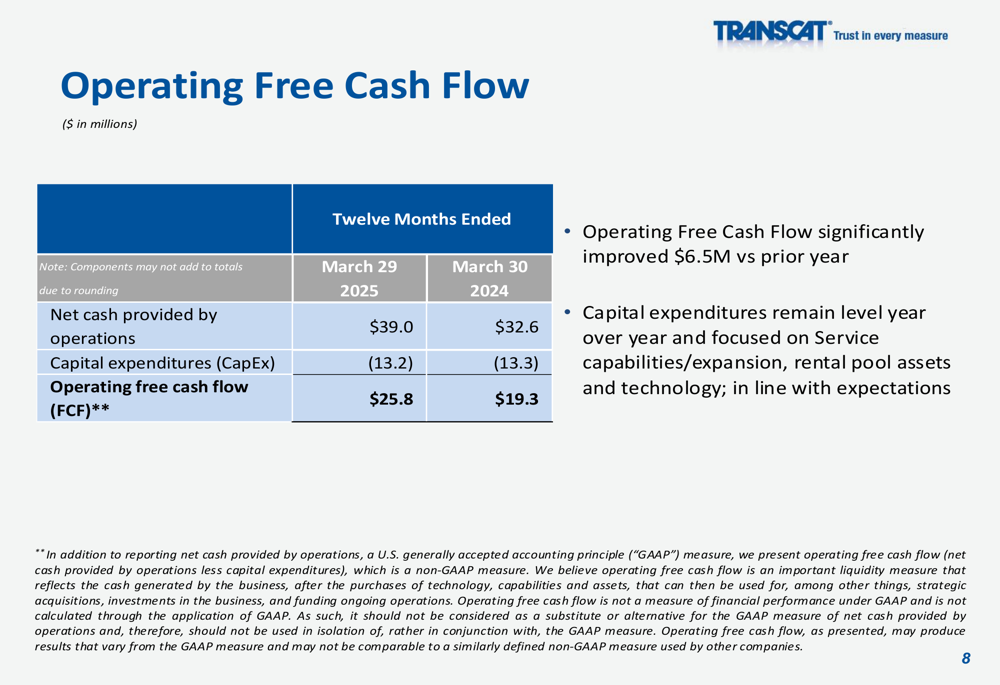

One of the most significant improvements came in operating free cash flow, which increased substantially to $25.8 million for the full year compared to $19.3 million in the prior year. This improvement came despite consistent capital expenditure levels, reflecting enhanced operational efficiency:

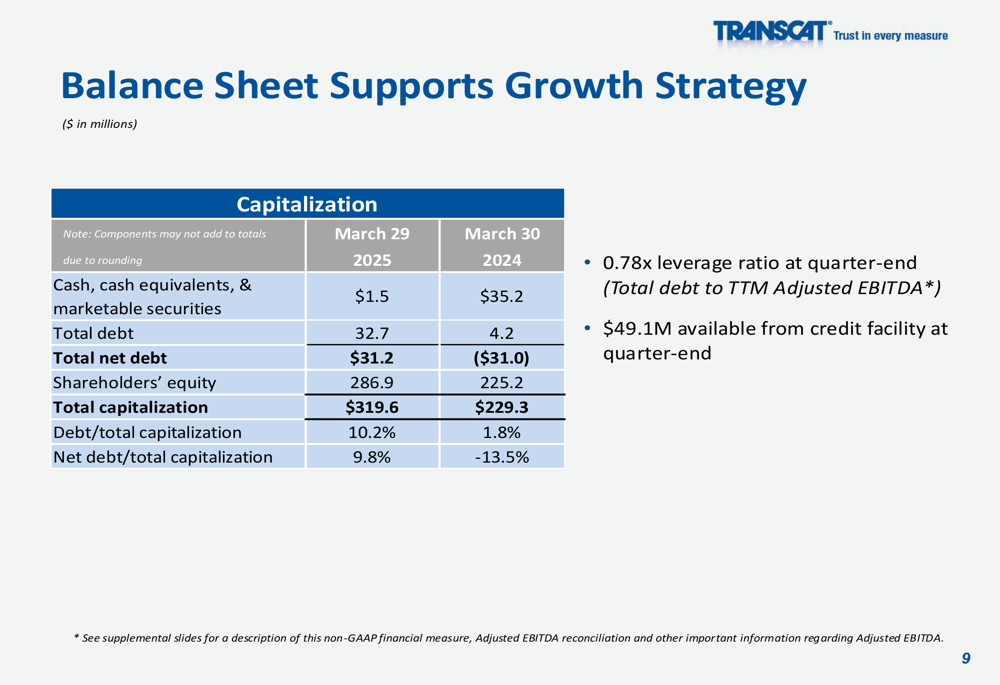

The company’s balance sheet showed a shift in capital structure, with total debt increasing to $32.7 million from $4.2 million in the prior year, while cash and equivalents decreased to $1.5 million from $35.2 million. This change reflects Transcat’s strategic investments, including the acquisition of Martin Calibration for $25 million mentioned in the earnings call:

Strategic Initiatives & Outlook

Transcat’s management emphasized that strong organic growth in the Service segment remains the centerpiece of their strategy. The company continues to benefit from its focus on the life science market, which provides recurring revenue streams driven by regulatory requirements.

For fiscal 2026, Transcat expects continued organic revenue growth in the Service segment, with an anticipated acceleration to high single-digit growth once the macroeconomic environment normalizes. The company also projects a fiscal 2026 income tax rate in the range of 27% to 29%.

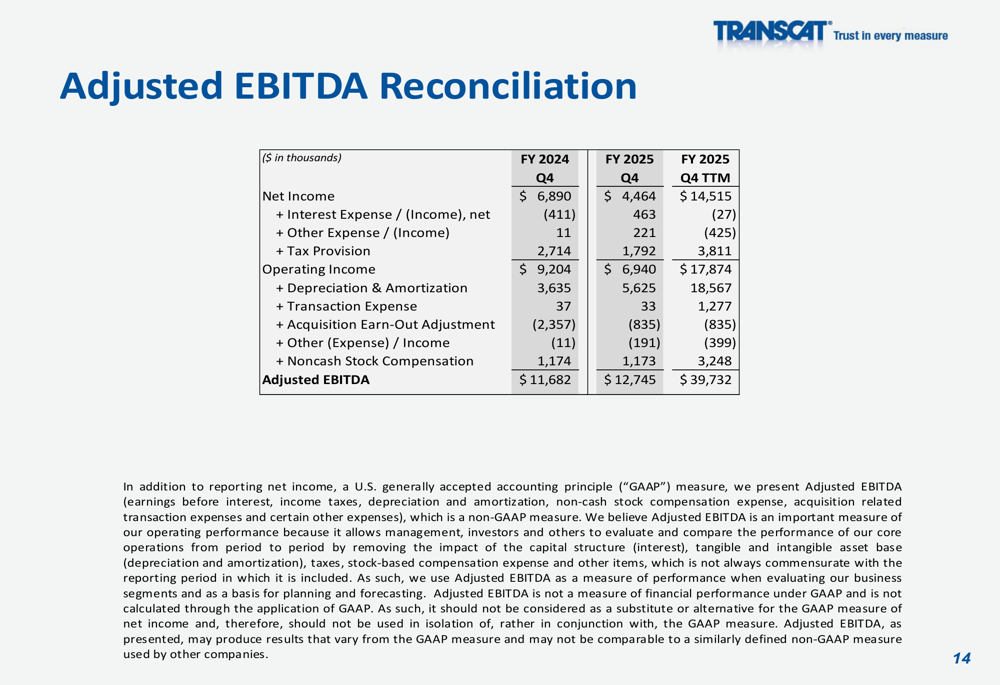

The company’s adjusted EBITDA reconciliation provides insight into the non-GAAP metrics that management uses to evaluate performance:

Further segment-specific performance can be seen in the detailed reconciliation:

Market Reaction & Analyst Perspectives

The market responded positively to Transcat’s results, with the stock price rising 17.09% following the announcement. This strong reaction suggests investors are focusing on the company’s revenue growth, cash flow generation, and long-term strategic positioning rather than the quarterly earnings decline.

According to the earnings call transcript, analysts inquired about the impact of tariffs on the distribution business and the potential of automation initiatives. Management addressed these concerns while emphasizing their disciplined approach to capital allocation and commitment to delivering profitable growth.

CEO Lee Rudow expressed optimism about the company’s future during the call, stating, "We have a proven track record of delivering profitable growth and being disciplined capital allocators," and noting, "We see a bright future that could get better."

The adjusted diluted earnings per share reconciliation helps explain the difference between GAAP and non-GAAP earnings figures:

While Transcat faces challenges including macroeconomic uncertainties and potential tariff impacts, its strong service segment performance, improved cash flow generation, and strategic focus on high-margin regulated industries position the company well for continued growth. The market’s positive reaction suggests investors share management’s confidence in the company’s long-term prospects despite some quarterly volatility.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.