Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

TransDigm Group Incorporated (NYSE:TDG) released its fiscal third-quarter 2025 earnings presentation on August 5, 2025, reporting solid financial results with revenue growth of 9.3% year-over-year. Despite the positive performance and raised guidance, the stock fell 7.33% in pre-market trading to $1,491, continuing a pattern of market skepticism that also followed the company’s Q2 results.

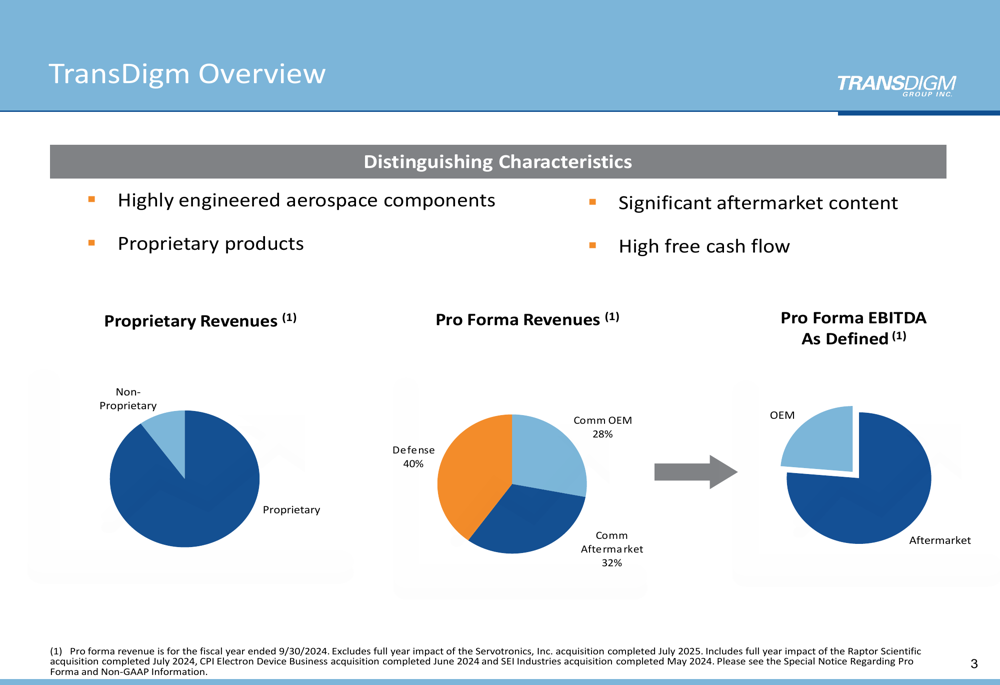

The aerospace components manufacturer, which specializes in proprietary products with significant aftermarket content, continues to benefit from a diversified revenue mix across defense (40%), commercial OEM (28%), and commercial aftermarket (32%) segments. This balanced approach has allowed TransDigm to offset weakness in commercial OEM with strength in defense and aftermarket businesses.

Quarterly Performance Highlights

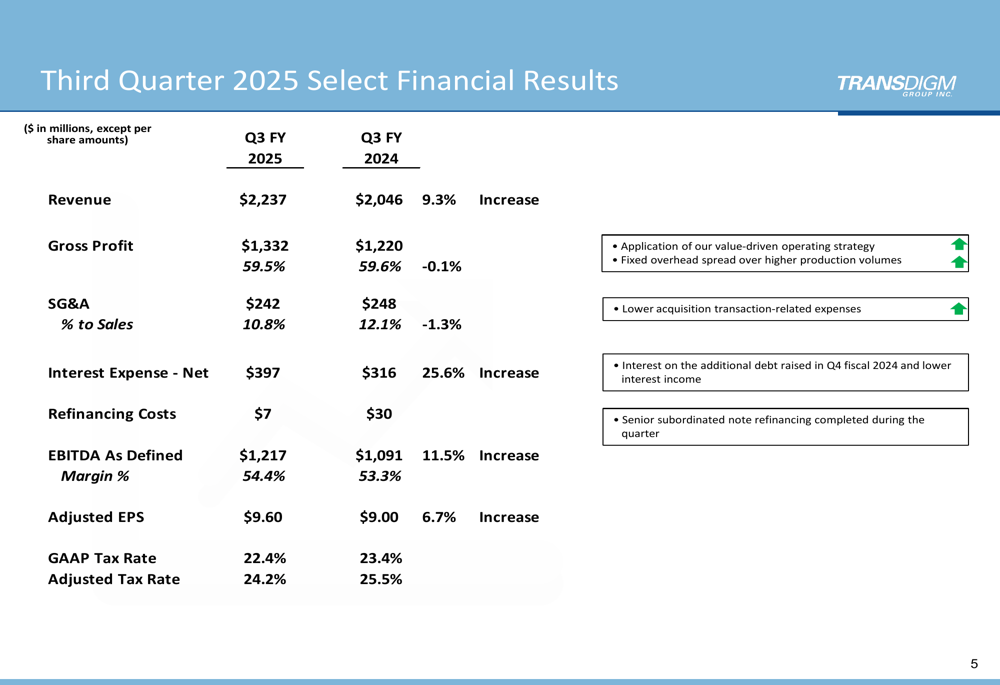

TransDigm reported Q3 FY2025 revenue of $2,237 million, representing a 9.3% increase from $2,046 million in the same quarter last year. The company’s EBITDA As Defined reached $1,217 million, up 11.5% year-over-year, with margins expanding to 54.4% from 53.3% in Q3 FY2024.

As shown in the following financial results summary:

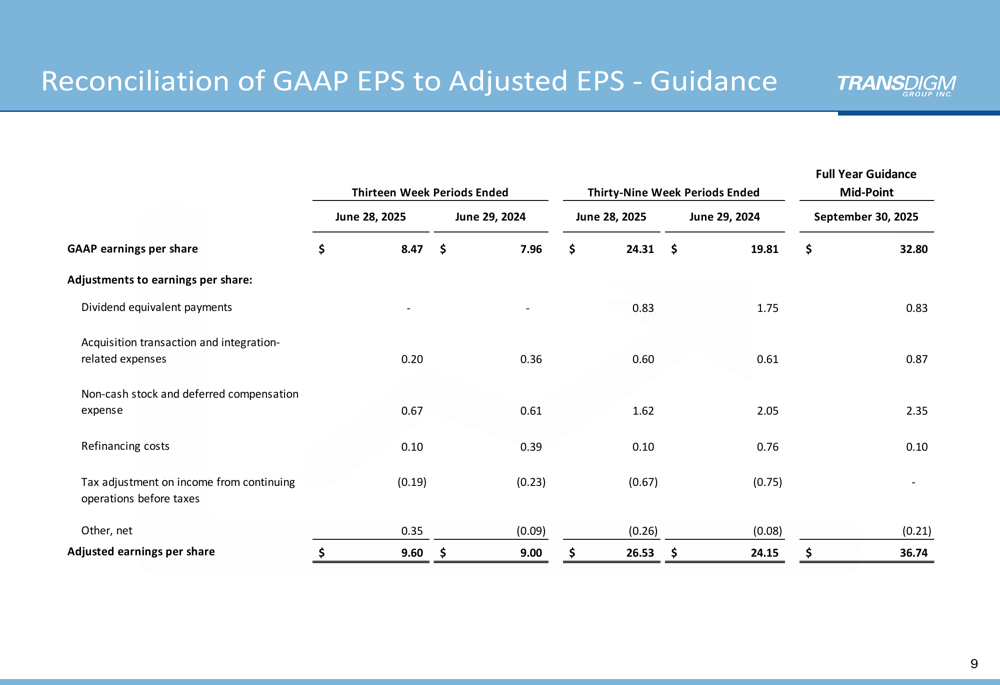

Adjusted earnings per share increased 6.7% to $9.60, compared to $9.00 in the prior year period. The company maintained strong gross profit margins at 59.5%, nearly unchanged from 59.6% a year ago, while reducing SG&A expenses as a percentage of sales to 10.8% from 12.1% in Q3 FY2024.

Interest expense rose significantly by 25.6% to $397 million, reflecting the company’s highly leveraged capital structure. However, refinancing costs decreased to $7 million from $30 million in the prior year period.

Segment Analysis

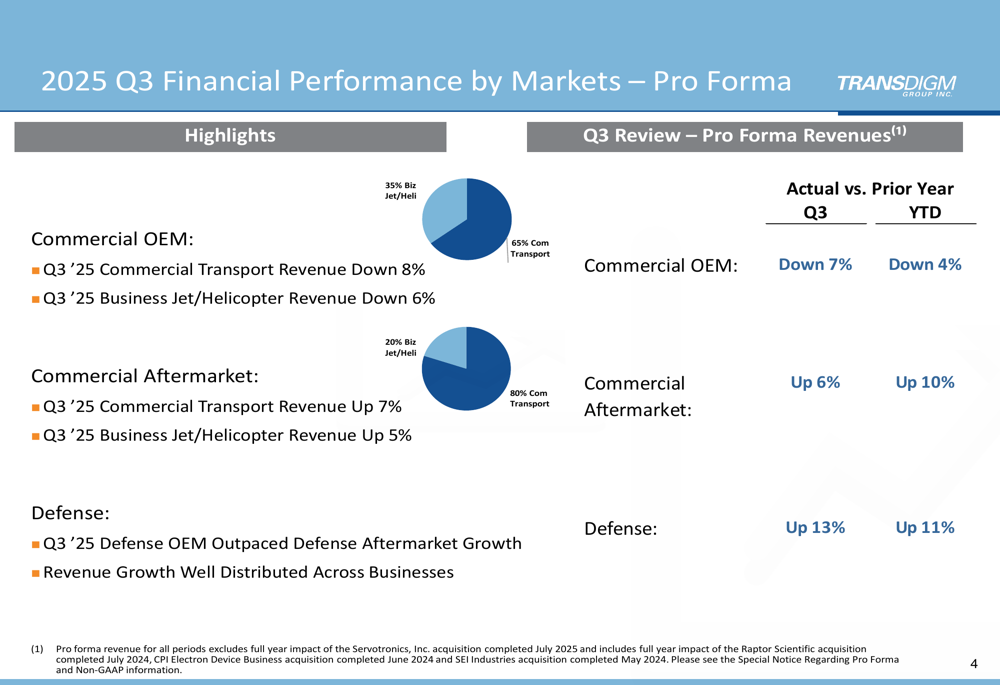

TransDigm’s performance varied significantly across its three main market segments. Defense revenue showed the strongest growth at 13% for the quarter and 11% year-to-date, while commercial aftermarket revenue increased by 6% for the quarter and 10% year-to-date. In contrast, commercial OEM revenue declined by 7% for the quarter and 4% year-to-date.

The following chart illustrates the company’s Q3 2025 performance by market segment:

Within the commercial segments, transport revenue outperformed business jet and helicopter revenue in both OEM and aftermarket categories. Commercial transport OEM revenue was down 8%, while business jet/helicopter OEM revenue declined 6%. In the aftermarket segment, commercial transport revenue grew 7%, while business jet/helicopter aftermarket revenue increased 5%.

The company’s business model continues to be anchored by its focus on proprietary products, which represent approximately 90% of total revenue, providing strong pricing power and competitive advantages.

Financial Position and Capital Structure

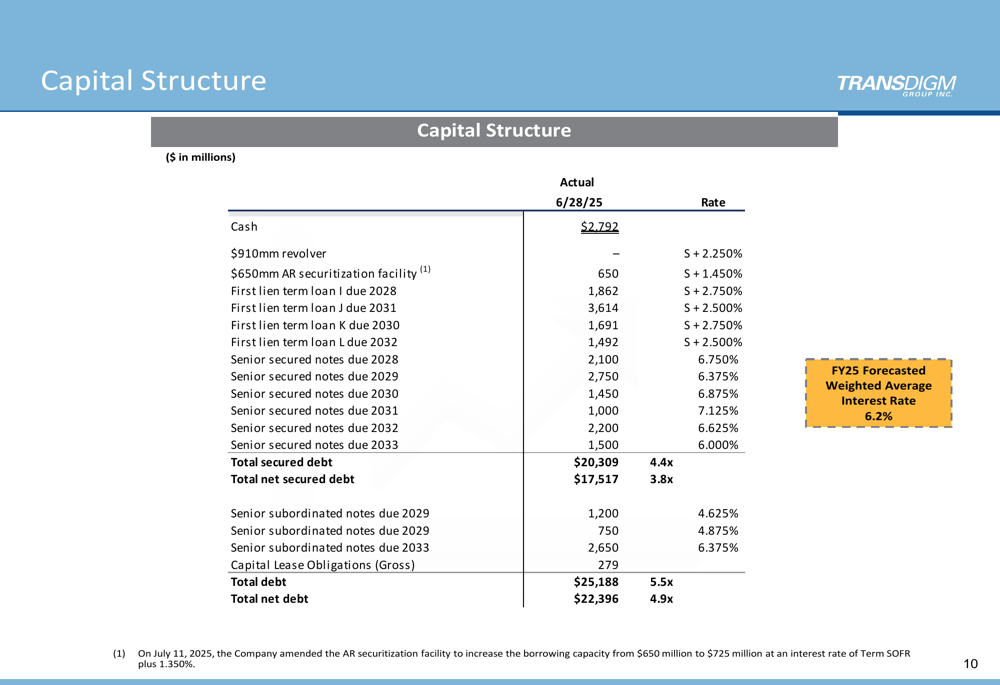

TransDigm maintained a highly leveraged but stable capital structure, with total debt of $25,188 million representing 5.5x leverage. The company reported a cash balance of $2,792 million, resulting in net debt of $22,396 million or 4.9x leverage.

The following slide details the company’s capital structure as of June 28, 2025:

To mitigate interest rate risk, TransDigm has hedged or fixed approximately 75% of its $25 billion gross debt through fiscal year 2027 using a combination of interest rate caps, swaps, and collars. This strategy significantly reduces the company’s near-term exposure to variable rate increases.

The company’s interest rate sensitivity analysis shows that a 100 basis point increase in average variable rates would increase annual interest expense by approximately $65 million:

Outlook and Guidance

TransDigm slightly lowered its fiscal 2025 revenue guidance to $8,790 million from the previous $8,850 million, a $60 million reduction. However, the company raised its EBITDA As Defined guidance to $4,725 million from $4,685 million, a $40 million increase, and increased its adjusted EPS guidance to $36.74 from $36.47.

The following slide summarizes the company’s updated guidance and market growth assumptions:

For fiscal 2025, TransDigm expects commercial OEM markets to be flat to low single-digit growth, commercial aftermarket to grow in the high single-digit to low double-digit range, and defense markets to grow in the high single-digit to low double-digit range.

The company also updated several financial assumptions, including a slight increase in full-year net interest expense to approximately $1.56 billion (from $1.54 billion) and a change in other EBITDA As Defined add-backs from ($15) to ($25) million to $25 to $35 million.

Market Reaction

Despite the positive results and raised EBITDA and EPS guidance, TransDigm’s stock fell 7.33% in pre-market trading to $1,491. This continues a pattern seen after the Q2 2025 results, when the stock declined 5.61% despite beating earnings expectations.

The market’s negative reaction may reflect concerns about the slight reduction in revenue guidance, the company’s high leverage in a rising interest rate environment, or broader market apprehensions about the commercial aerospace sector. TransDigm’s stock had been trading near its 52-week high of $1,623.83 prior to the earnings release, suggesting high investor expectations that may have been difficult to surpass despite solid results.

The company’s P/E ratio of 49x, as mentioned in previous earnings coverage, also indicates a premium valuation that leaves little room for disappointment, even as TransDigm continues to deliver strong operational performance and margin expansion.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.