Gold prices snap 4-day losing streak after Fed rate cut, Trump-Xi meeting

Introduction & Market Context

TreeHouse Foods Inc (NYSE:THS) released its second quarter 2025 results on July 31, exceeding guidance for both sales and EBITDA despite ongoing market challenges. The private label food manufacturer continues to benefit from the long-term growth trend in private brands, which has increased from 16% market share in 2006 to 25% in 2025 year-to-date.

The company’s stock has faced significant pressure in recent months, with fundamentals data showing a 3.15% decline to $20.57 in the most recent trading session. This continues a downward trend that has seen THS reach a 52-week low of $19.11, well below its 52-week high of $43.84.

As shown in the following chart illustrating the long-term growth of private brands in North America, TreeHouse Foods operates in a sector with favorable structural trends:

Quarterly Performance Highlights

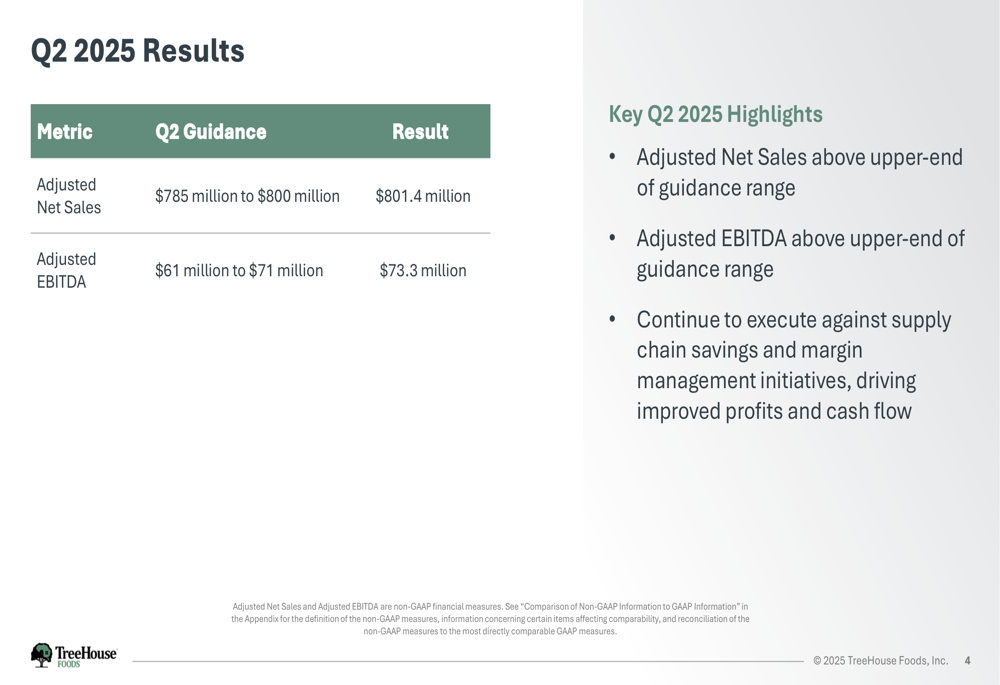

TreeHouse Foods reported Q2 2025 adjusted net sales of $801.4 million, exceeding the upper end of its guidance range of $785-800 million. Adjusted EBITDA came in at $73.3 million, also surpassing the guidance range of $61-71 million. The company’s adjusted EBITDA margin improved by 20 basis points year-over-year to 9.1%.

The following slide summarizes the company’s Q2 2025 results compared to guidance:

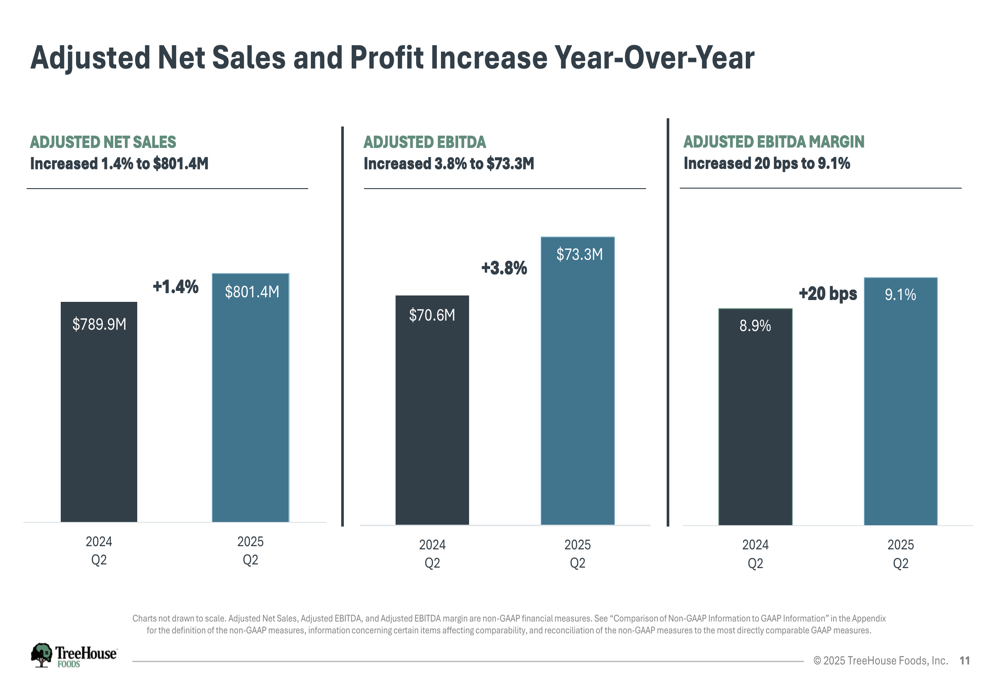

Year-over-year, adjusted net sales increased 1.4% from $789.9 million in Q2 2024, while adjusted EBITDA grew 3.8% from $70.6 million. This growth was achieved despite several headwinds, including negative impacts from margin management decisions and volume/mix challenges.

As illustrated in the chart below, both adjusted net sales and adjusted EBITDA showed positive year-over-year growth:

The primary drivers of adjusted net sales performance included positive contributions from acquisitions (+4.5%) and pricing (+4.2%), offset by negative impacts from margin management (-2.6%), consumption/other (-2.4%), Griddle recall service impacts (-1.2%), and volume/mix (-6.2%).

Private Brand Market Positioning

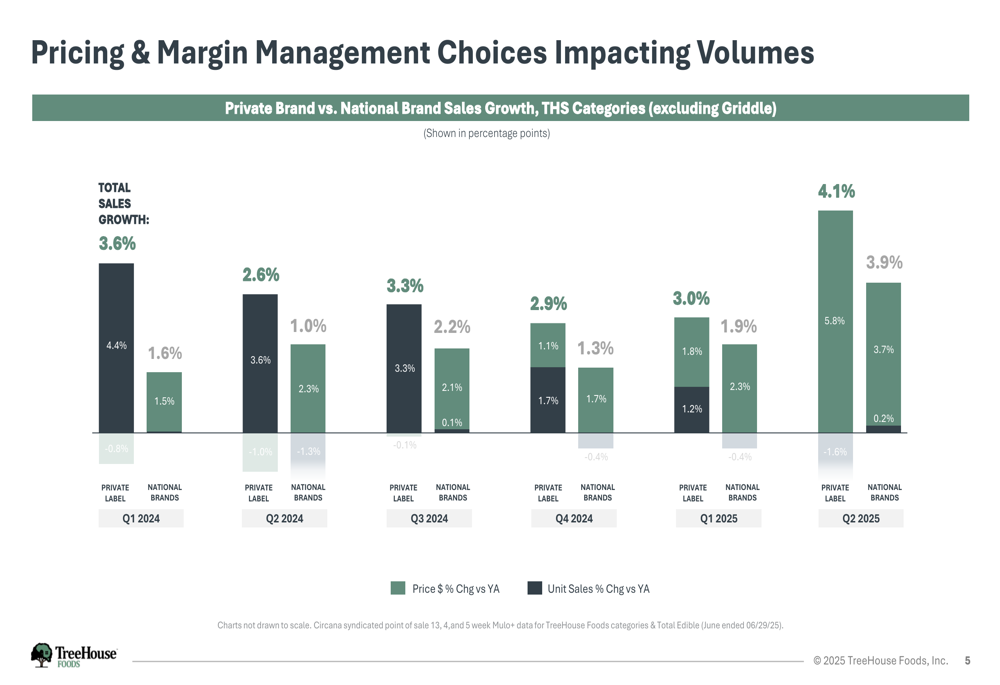

TreeHouse Foods highlighted the resilience of private brands in its presentation, noting that private brand dollar share in its categories has remained flat year-over-year. The company also emphasized that the price gap between private brands and national brands remains above historical levels, providing value to consumers in an inflationary environment.

The following chart shows the comparison between private brand and national brand sales growth in TreeHouse Foods categories:

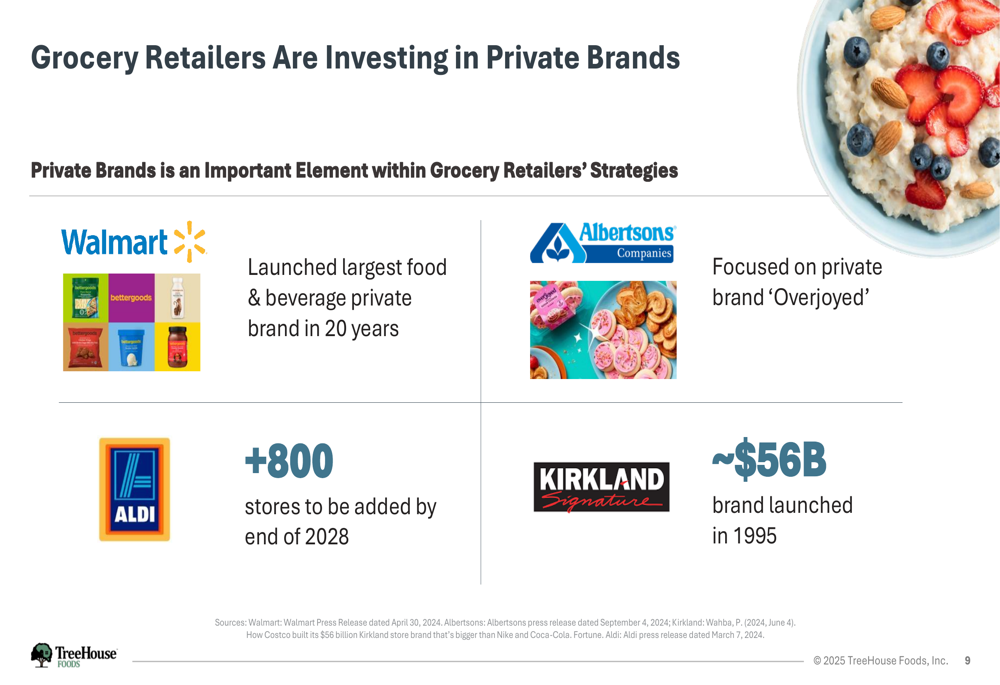

Major retailers continue to invest in private brands, with examples including Walmart (NYSE:WMT)’s launch of its largest food & beverage private brand in 20 years ("bettergoods"), Albertsons (NYSE:ACI)’ focus on its "Overjoyed" brand, ALDI’s expansion plans to add 800 stores by 2028, and Kirkland Signature’s growth to approximately $56 billion in sales since its 1995 launch.

As illustrated in the slide below, major retailers are making significant investments in private brands:

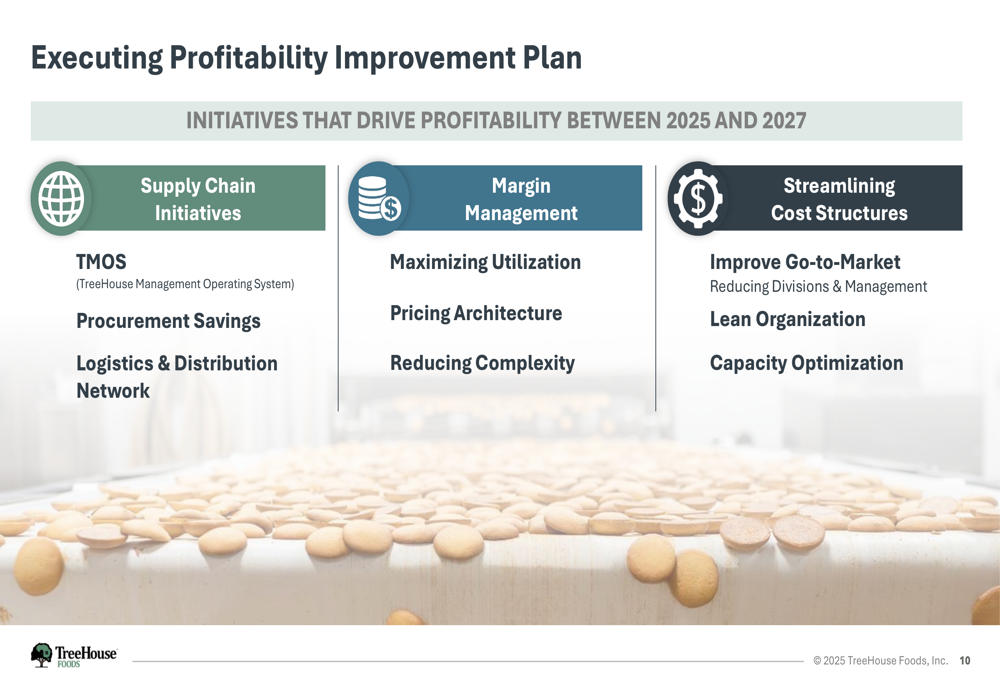

Profitability Improvement Initiatives

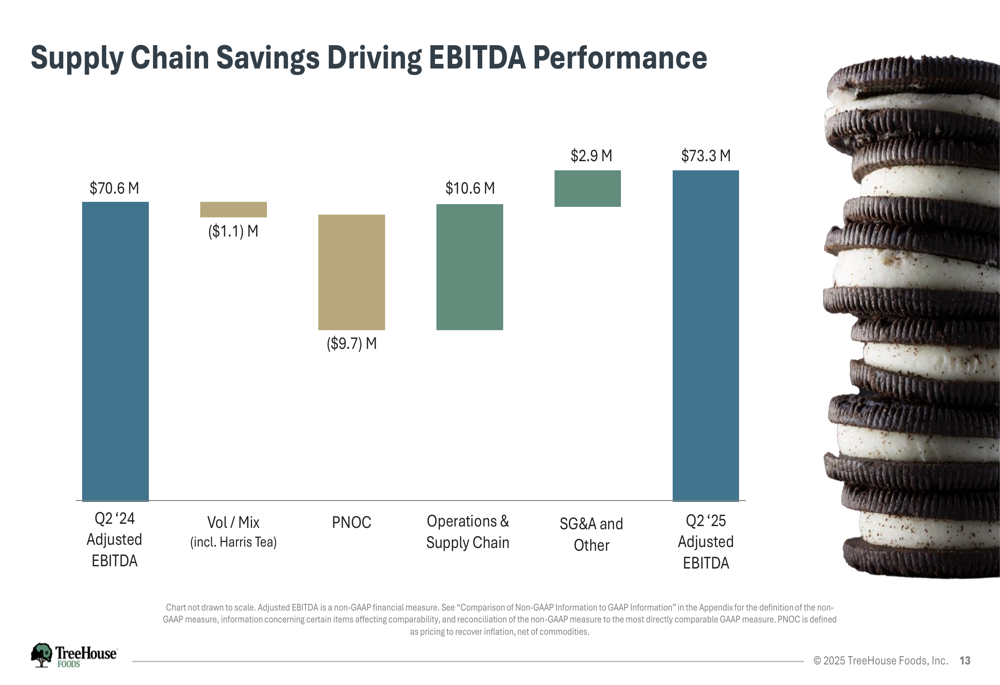

A key focus for TreeHouse Foods is its profitability improvement plan, which centers on three main areas: supply chain initiatives, margin management, and streamlining cost structures. The company reported that supply chain savings of $10.6 million were a major driver of EBITDA performance in Q2 2025.

The following slide outlines the company’s profitability improvement initiatives:

Breaking down the changes in adjusted EBITDA from Q2 2024 to Q2 2025, operations and supply chain improvements contributed $10.6 million, while SG&A and other factors added $2.9 million. These positive factors were partially offset by negative impacts from volume/mix including Harris Tea (-$1.1 million) and PNOC (-$9.7 million).

The waterfall chart below illustrates how supply chain savings drove EBITDA performance:

TreeHouse Foods also highlighted its balanced capital allocation approach, with $1.6 billion deployed between 2022-2024 across debt paydown (33%), capital expenditures and growth (31%), acquisitions (20%), and share buybacks (16%).

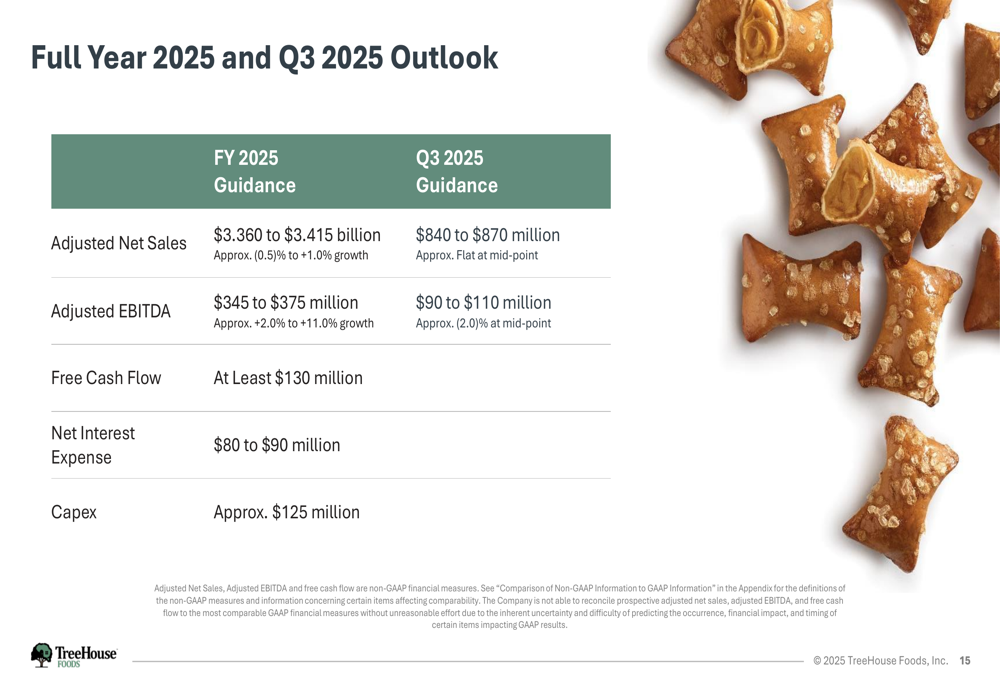

Forward Outlook and Guidance

Looking ahead, TreeHouse Foods maintained its full-year 2025 adjusted EBITDA guidance of $345-375 million (representing approximately 2-11% growth) and free cash flow of at least $130 million. However, the company slightly revised its adjusted net sales growth outlook to -0.5% to 1.0%, suggesting caution about volume trends.

For Q3 2025, TreeHouse Foods expects adjusted net sales of $840-870 million (approximately flat at the midpoint) and adjusted EBITDA of $90-110 million (approximately -2.0% at the midpoint).

The following slide details the company’s full-year 2025 and Q3 2025 outlook:

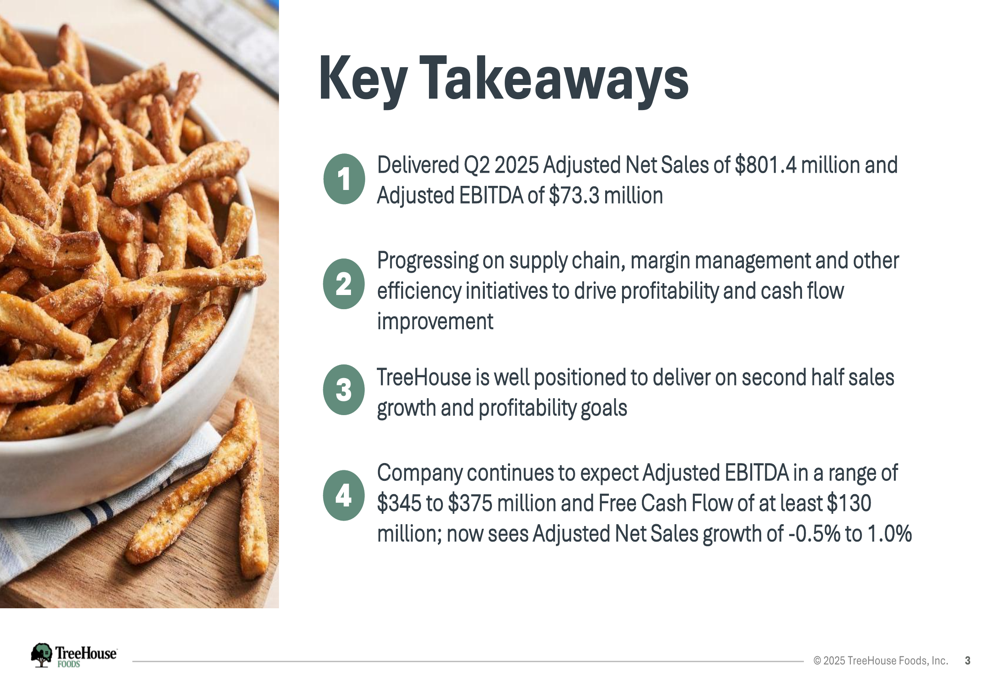

TreeHouse Foods emphasized that it is well-positioned to deliver on second-half sales growth and profitability goals, continuing to progress on supply chain, margin management, and other efficiency initiatives to drive profitability and cash flow improvement.

As summarized in the key takeaways slide, the company remains focused on executing its strategy despite market challenges:

While TreeHouse Foods exceeded its Q2 2025 guidance, the cautious outlook for the remainder of the year reflects ongoing challenges in the consumer packaged goods sector. The company’s focus on margin management and operational efficiency will be crucial as it navigates a competitive landscape where private brands continue to gain importance with both retailers and consumers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.