Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

TriMas Corporation (NYSE:TRS) shares jumped over 10% in regular trading and nearly 14% in premarket following the release of its second quarter 2025 earnings presentation on July 29. The industrial manufacturer reported strong results across all segments and raised its full-year guidance, continuing the positive momentum seen in Q1 when the stock surged 12% after beating revenue expectations.

The company’s performance comes during a transitional period with new CEO Thomas Snyder at the helm, who delivered impressive results in his first earnings presentation since joining the company.

Executive Summary

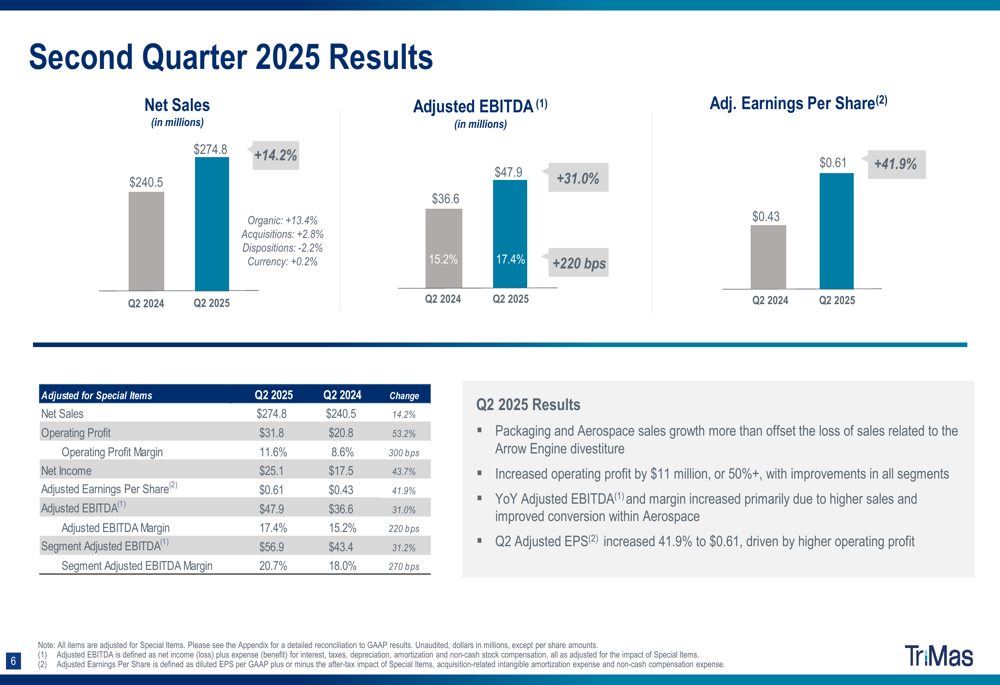

TriMas reported robust financial performance for Q2 2025, with net sales increasing 14.2% to $274.8 million, driven primarily by organic growth of 13.4% and acquisitions contributing 2.8%, partially offset by dispositions (-2.2%).

"All businesses showed year-over-year sales growth and margin expansion during Q2," noted the company in its presentation, with particularly strong performance in the Aerospace segment, which delivered record quarterly sales.

As shown in the following financial results summary:

Adjusted EBITDA grew by 31.0% to $47.9 million, representing a margin of 17.4% - a 220 basis point improvement year-over-year. Adjusted earnings per share increased by 41.9% to $0.61, significantly outpacing sales growth and reflecting improved operational efficiency.

Quarterly Performance Highlights

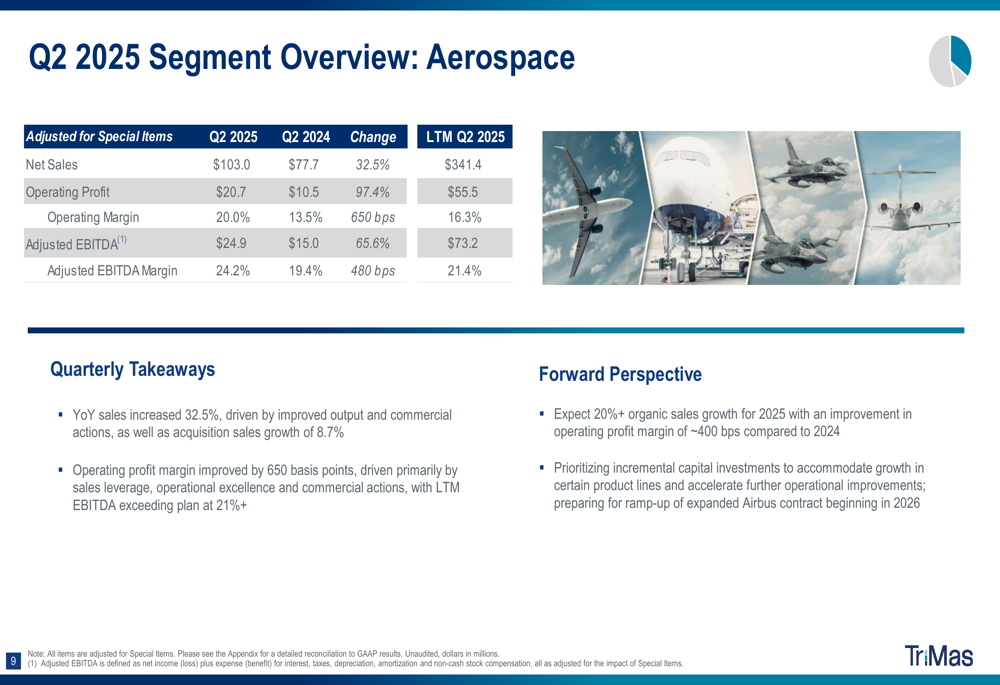

The Aerospace segment was the standout performer, achieving record quarterly sales of $103.0 million, a 32.5% increase from Q2 2024. Operating profit margins in this segment improved by 650 basis points, demonstrating strong operational leverage as volumes increased.

The segment’s impressive performance is detailed in the following overview:

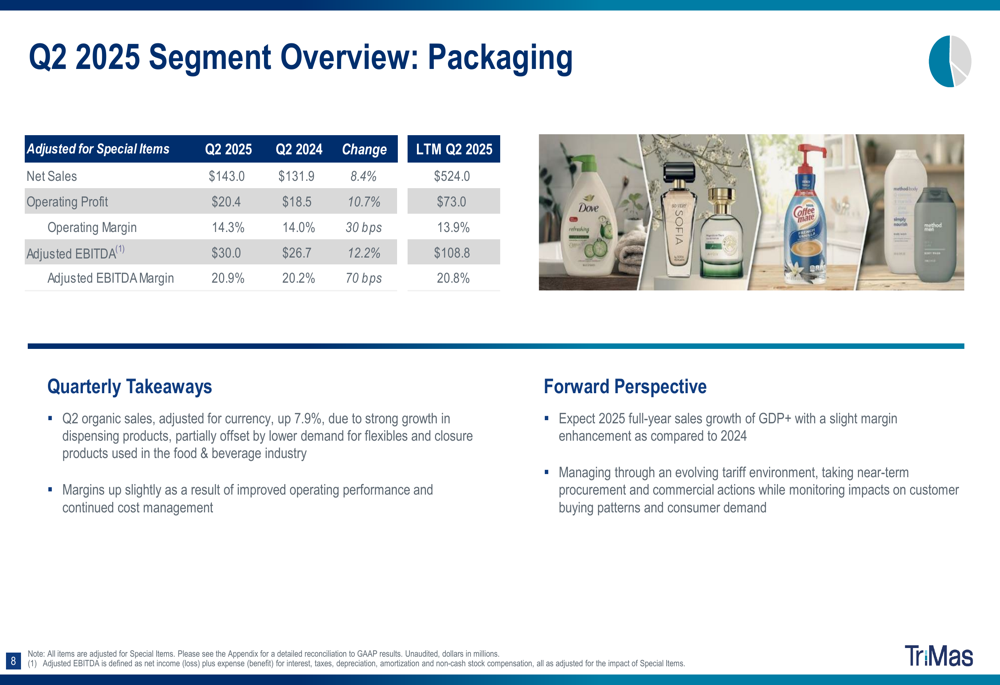

The Packaging (NYSE:PKG) segment, which remains TriMas’ largest business unit, delivered sales of $143.0 million, up 8.4% year-over-year. Growth was primarily driven by dispensing products, though partially offset by lower demand for flexibles and closure products.

The Specialty Products segment showed mixed results, with 13% sales growth in the Norris Cylinder business more than offset by lower sales related to the divestiture of Arrow Engine. Despite this, operating profit improved due to higher absorption of fixed costs.

New Leadership & Strategic Direction

The Q2 results mark the first full quarter under new CEO Thomas Snyder, who brings over 30 years of experience in the global packaging industry, including 17 years as President of Silgan Containers.

During his first 30+ days at TriMas, Snyder visited 10 manufacturing sites, engaged with business leadership teams, and began a strategic business review. His initial observations highlighted "talented teams, innovative products, a diverse manufacturing platform, strategic customer relationships, and significant opportunities for growth and cost reduction."

Snyder’s experience in operational excellence and strategy development appears well-aligned with TriMas’ focus on performance enhancement and growth opportunities, potentially setting the stage for continued improvement in the coming quarters.

Financial Position & Outlook

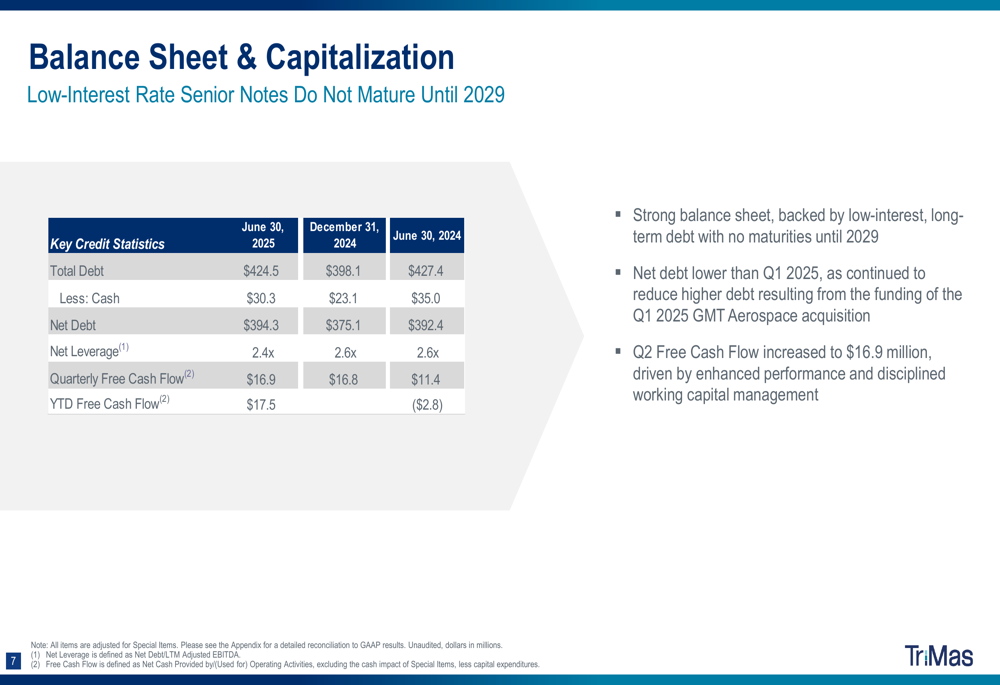

TriMas maintains a solid balance sheet with total debt of $424.5 million, cash of $30.3 million, and net debt of $394.3 million as of June 30, 2025. This results in a net leverage ratio of 2.4x, with the company noting that its debt is low-interest and long-term with no maturities until 2029.

Free cash flow increased to $16.9 million in Q2, driven by enhanced performance and improved working capital management. This financial flexibility supports the company’s ability to pursue strategic growth initiatives while maintaining balance sheet strength.

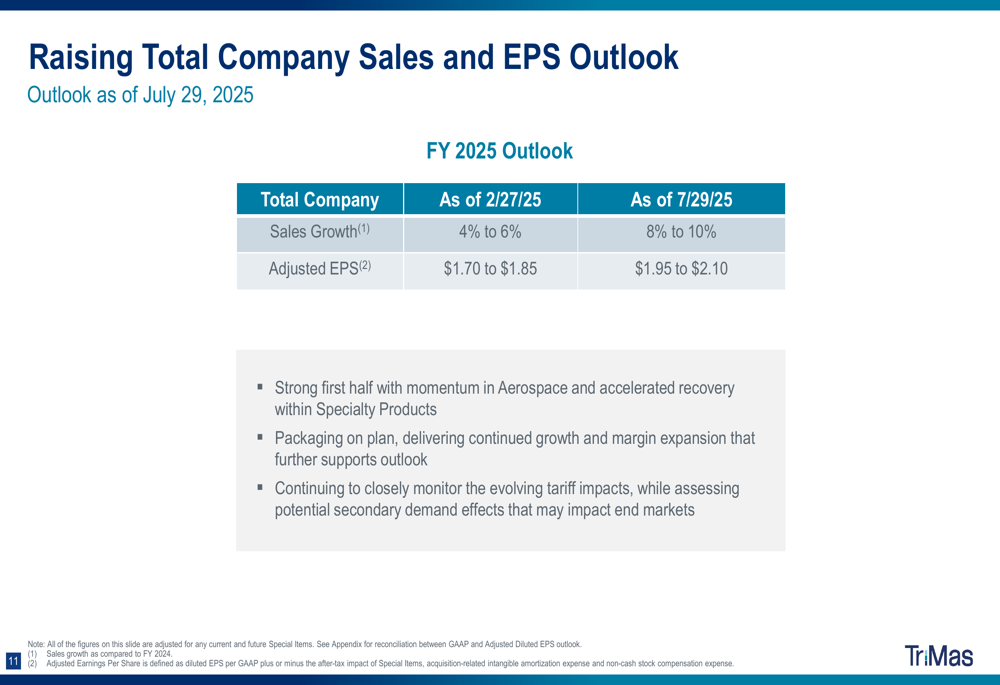

In a significant vote of confidence in future performance, TriMas raised its full-year 2025 outlook, as shown in the following guidance update:

Sales growth is now projected at 8% to 10%, up from the previous estimate of 4% to 6%. Similarly, adjusted EPS guidance was increased to a range of $1.95 to $2.10, from the previous $1.70 to $1.85. This upward revision reflects strong first-half performance, continued momentum in Aerospace, and recovery in Specialty Products.

The company did note that it continues to monitor "evolving tariff impacts," which was also mentioned as a concern during the Q1 earnings call when then-CEO Thomas Amato stated, "If it wasn’t for the uncertainty in tariffs, we’d probably be guiding on an overall annual basis to the higher end of our range or beyond."

Despite these uncertainties, TriMas’ raised guidance and strong Q2 performance demonstrate management’s confidence in the company’s ability to navigate challenges while capitalizing on growth opportunities across its diverse business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.