Gold prices just lower; monthly gains on track

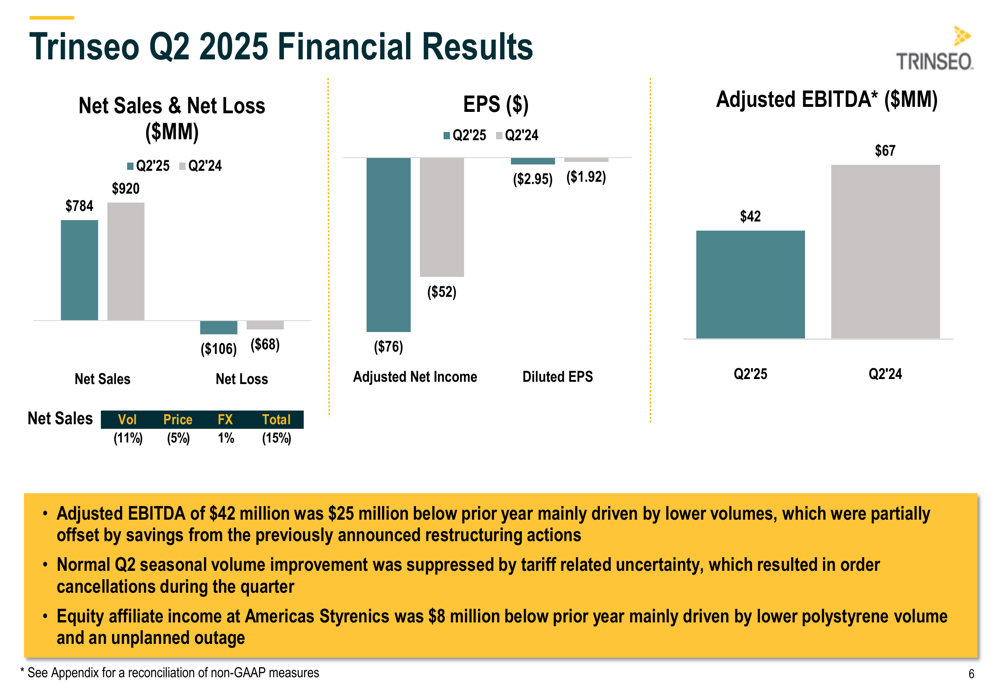

Trinseo SA (NYSE:TSE) released its second quarter 2025 financial results on August 6, revealing continued challenges across its core markets while highlighting progress in specialty segments and sustainability initiatives. The materials company reported a net loss of $106 million as volumes declined across all major business segments.

Quarterly Performance Highlights

Trinseo reported a net loss of $106 million for Q2 2025, translating to earnings per share of -$2.95, compared to a net loss of $68 million (-$1.92 per share) in the same period last year. The company generated $42 million in Adjusted EBITDA, down from $67 million in Q2 2024, primarily due to lower volumes and reduced equity income from its Americas Styrenics joint venture.

As shown in the following financial results summary:

Net sales declined 15% year-over-year to $784 million, driven by an 11% decrease in volume and a 5% reduction in price, partially offset by a 1% favorable currency impact. The company generated $7 million in cash from operations and spent $10 million on capital expenditures, resulting in negative free cash flow of $3 million for the quarter.

"Normal Q2 seasonal volume improvement was suppressed by tariff related uncertainty, which resulted in order cancellations during the quarter," the company noted in its presentation.

Segment Analysis

Trinseo’s performance varied across its three main business segments, with all experiencing year-over-year declines in volume and most showing reduced profitability.

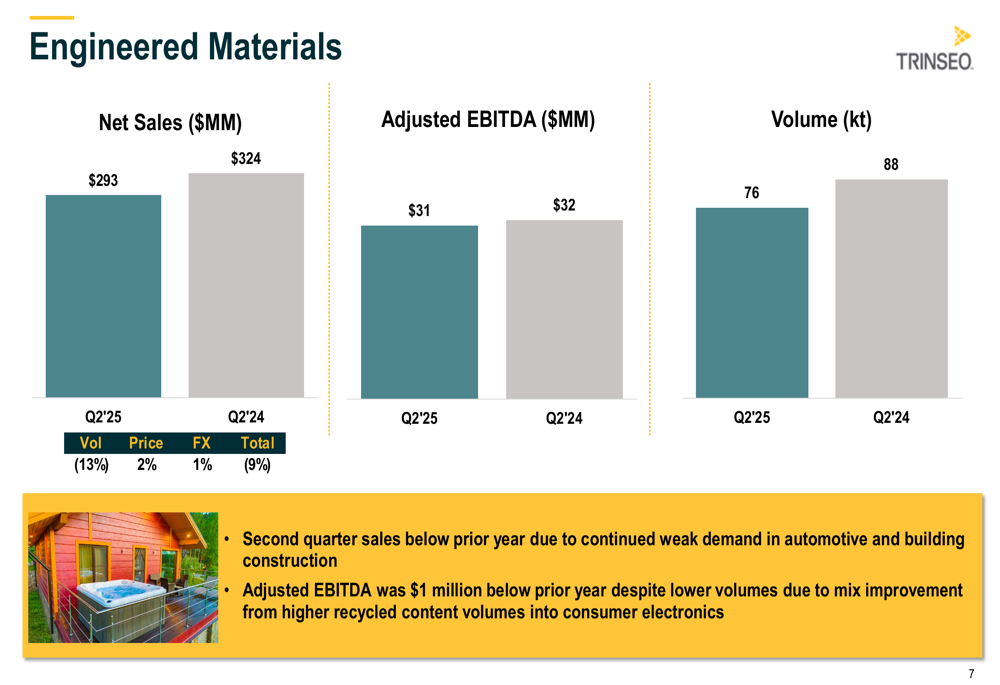

The Engineered Materials segment saw net sales decrease by 9% to $293 million, with volumes down 13% year-over-year:

Despite the volume decline, Adjusted EBITDA for the segment remained relatively stable at $31 million, just $1 million below the prior year. The company attributed this resilience to "mix improvement from higher recycled content volumes into consumer electronics."

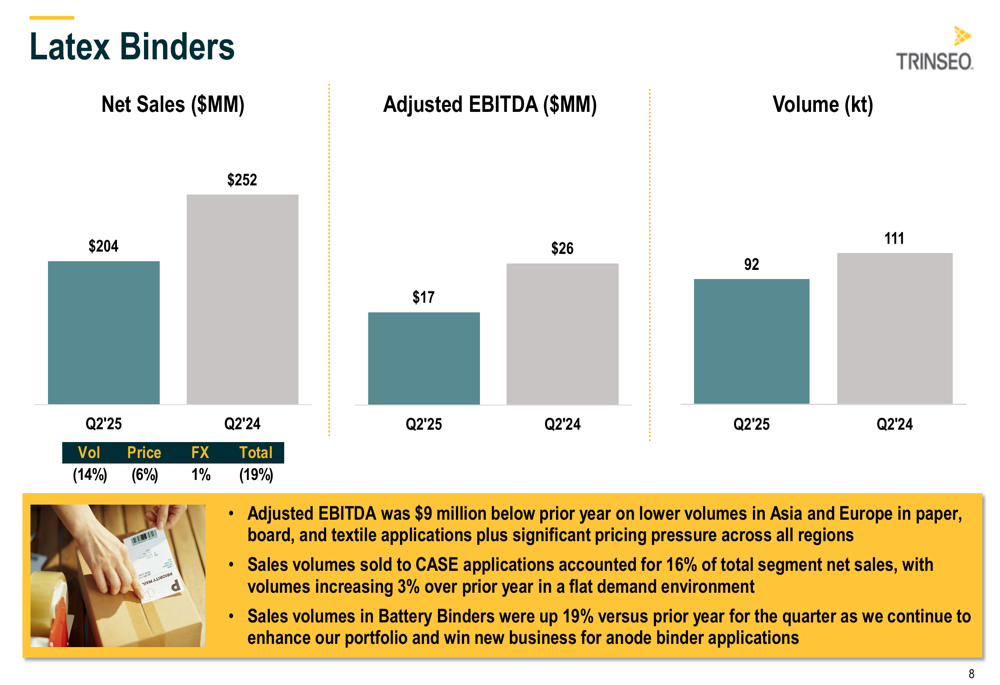

The Latex Binders segment experienced more significant challenges, with net sales falling 19% to $204 million and Adjusted EBITDA declining from $26 million to $17 million:

While overall Latex Binders volumes declined 14%, the company highlighted growth in specialty applications, with Battery Binders volumes increasing 19% year-over-year. The company is positioning this as a strategic growth area, noting a five-year volume CAGR (2020-2025) of 63% in its battery materials business.

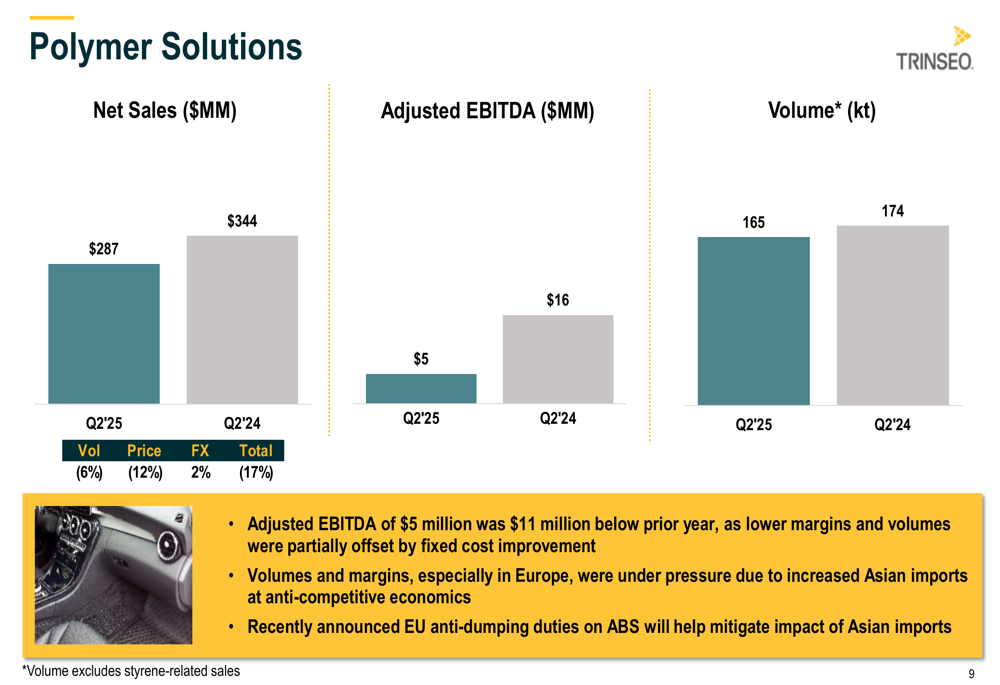

The Polymer Solutions segment showed the most pronounced profitability decline, with Adjusted EBITDA falling to $5 million from $16 million in the prior year:

The company cited "increased Asian imports at anti-competitive economics" as a key challenge for this segment, particularly in Europe, but noted that "recently announced EU anti-dumping duties on ABS will help mitigate impact of Asian imports."

Strategic Initiatives & Self-Help Actions

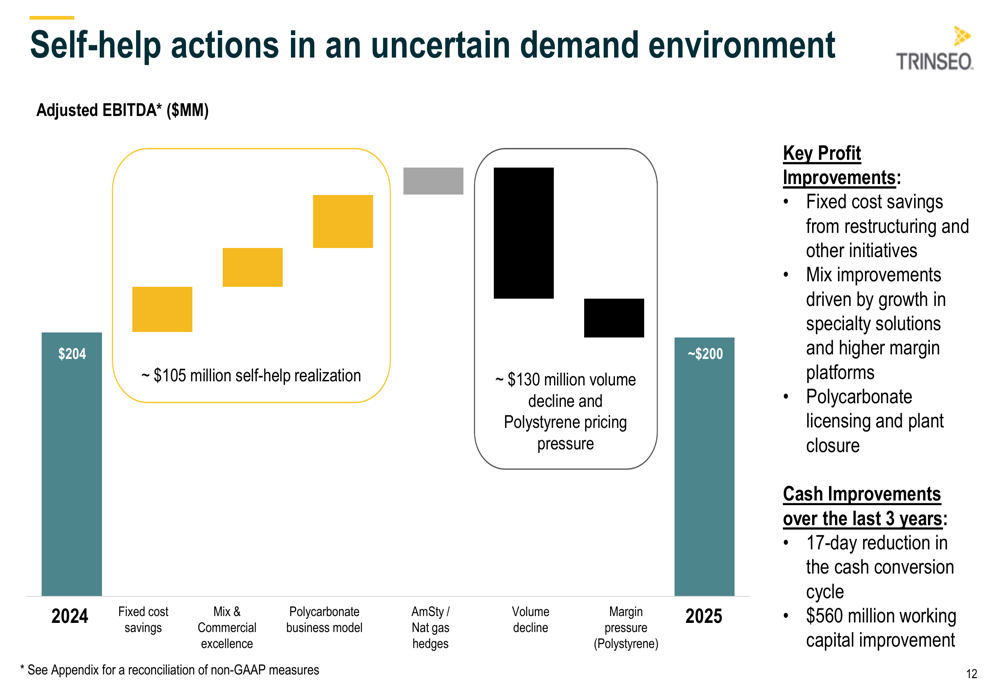

Trinseo highlighted its ongoing efforts to offset market challenges through self-help initiatives, which are expected to deliver approximately $105 million in Adjusted EBITDA improvements. However, these gains are being largely offset by volume declines and pricing pressure, estimated at approximately $130 million.

The following chart illustrates this dynamic:

Key profit improvement areas include fixed cost savings from restructuring, mix improvements driven by growth in specialty solutions, and changes to the Polycarbonate business model. The company also noted significant cash improvements over the past three years, including a 17-day reduction in the cash conversion cycle and $560 million in working capital improvements.

In the sustainability arena, Trinseo reported achieving five key goals, including:

- Establishing Scope 3 base year data and management system

- Increasing electricity from non-fossil sources from 5% to 30%

- Reducing Scope 1 & 2 GHG emissions intensity by 35%

- Reducing freshwater intake by 20%

- Reducing overall waste generation by 15%

Outlook & Guidance

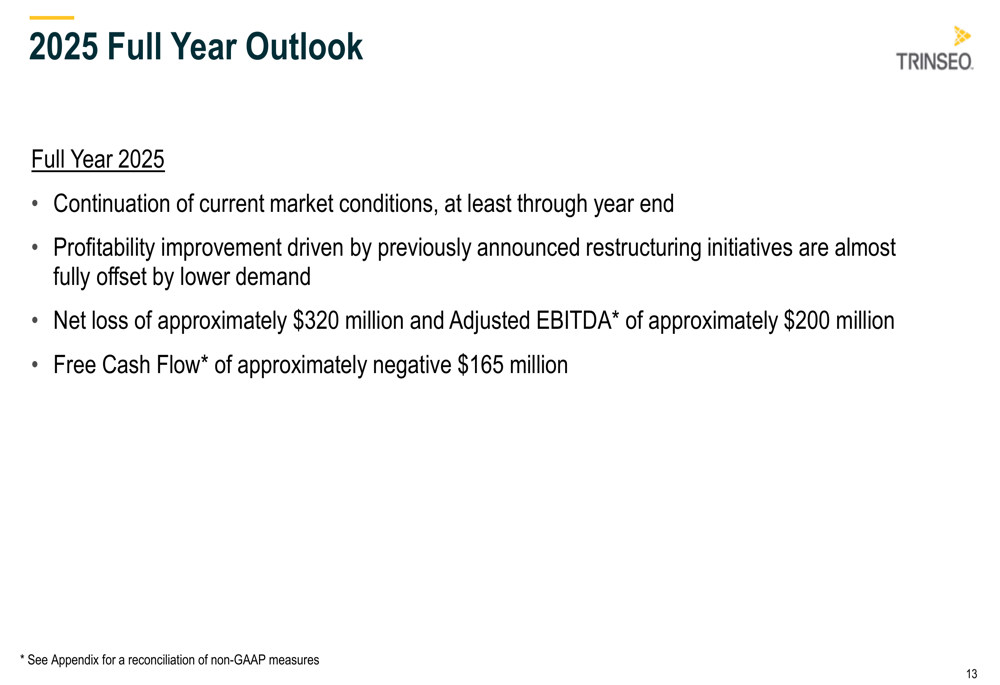

Trinseo provided a cautious outlook for the remainder of 2025, assuming "continuation of current market conditions, at least through year end." The company expects profitability improvements from restructuring initiatives to be almost fully offset by lower demand.

For the full year 2025, Trinseo forecasts:

The company expects a net loss of approximately $320 million, Adjusted EBITDA of approximately $200 million, and negative free cash flow of approximately $165 million. This outlook represents a significant deterioration from Q1 2025, when the company reported an EPS of -$1.37 and Adjusted EBITDA of $65 million.

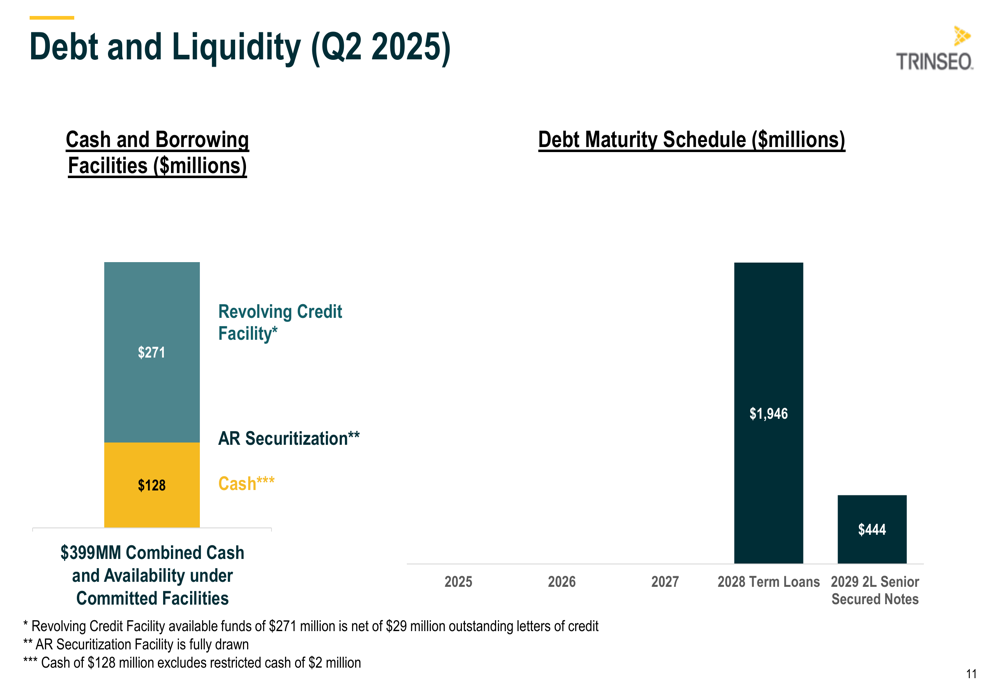

Trinseo’s debt and liquidity position remains a concern, with $1.95 billion in term loans due in 2028 and $444 million in senior secured notes due in 2029:

As of Q2 2025, the company reported total liquidity of $399 million, including $128 million in cash and availability under its revolving credit facility and accounts receivable securitization.

The market has responded negatively to Trinseo’s continued challenges, with the stock closing at $2.55 on August 6, down 5.9% for the day and approaching its 52-week low of $2.16. The shares have fallen significantly from their 52-week high of $7.05, reflecting ongoing investor concerns about the company’s path to profitability in a challenging market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.