Bank of America just raised its EUR/USD forecast

Introduction & Market Context

TrueBlue Inc (NYSE:TBI) presented its Q1 2025 earnings results on May 5, 2025, revealing ongoing challenges in the staffing industry. The company reported an 8% year-over-year revenue decline amid persistent market headwinds, though this represents an improvement from the 19% decline reported in Q3 2024. TrueBlue’s stock closed at $4.44, near its 52-week low of $3.95, reflecting investor concerns about the company’s performance.

The staffing services provider continues to navigate a difficult market environment characterized by reduced business spending and cautious hiring trends among clients. However, management highlighted several areas of resilience, particularly in its commercial driving services division.

Quarterly Performance Highlights

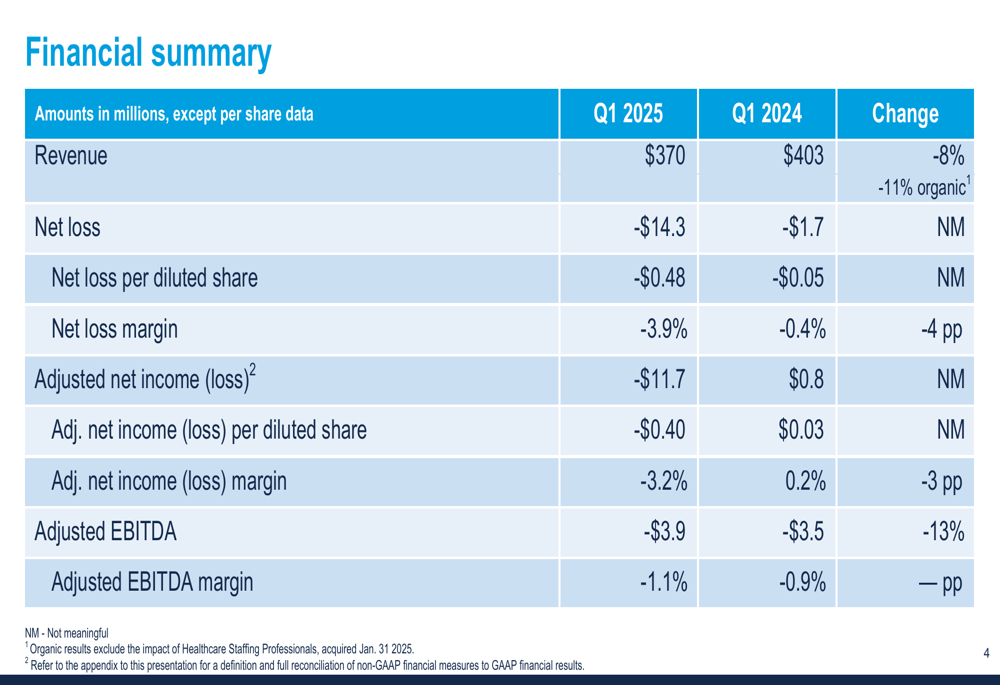

TrueBlue reported total revenue of $370 million for Q1 2025, down 8% from $403 million in the same period last year. Organic revenue, which excludes the impact of the Healthcare Staffing Professionals acquisition, declined by 11%.

As shown in the following financial summary, the company posted a net loss of $14.3 million, significantly wider than the $1.7 million loss recorded in Q1 2024. This translated to a loss of $0.48 per diluted share, compared to a $0.05 loss per share in the prior-year quarter.

Adjusted EBITDA was negative $3.9 million, slightly worse than the negative $3.5 million reported in Q1 2024. The adjusted EBITDA margin deteriorated marginally to -1.1% from -0.9% a year earlier.

Gross margin decreased by 1.4 percentage points to 23.3%, primarily due to changes in business mix. However, the company made progress on the cost front, with selling, general, and administrative (SG&A) expenses decreasing by 12% to $95 million, reflecting management’s focus on operational efficiency.

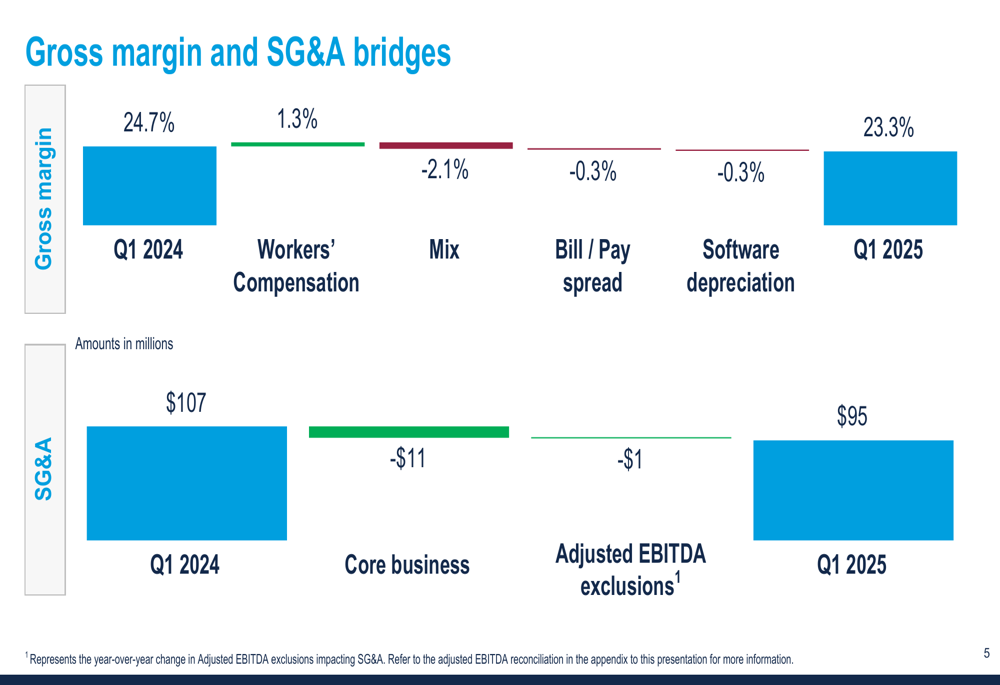

The following chart breaks down the key factors affecting gross margin and SG&A expenses:

While business mix had a negative 2.1 percentage point impact on gross margin, this was partially offset by a 1.3 percentage point benefit from workers’ compensation adjustments. On the SG&A side, the company achieved an $11 million reduction in core business expenses.

Segment Analysis

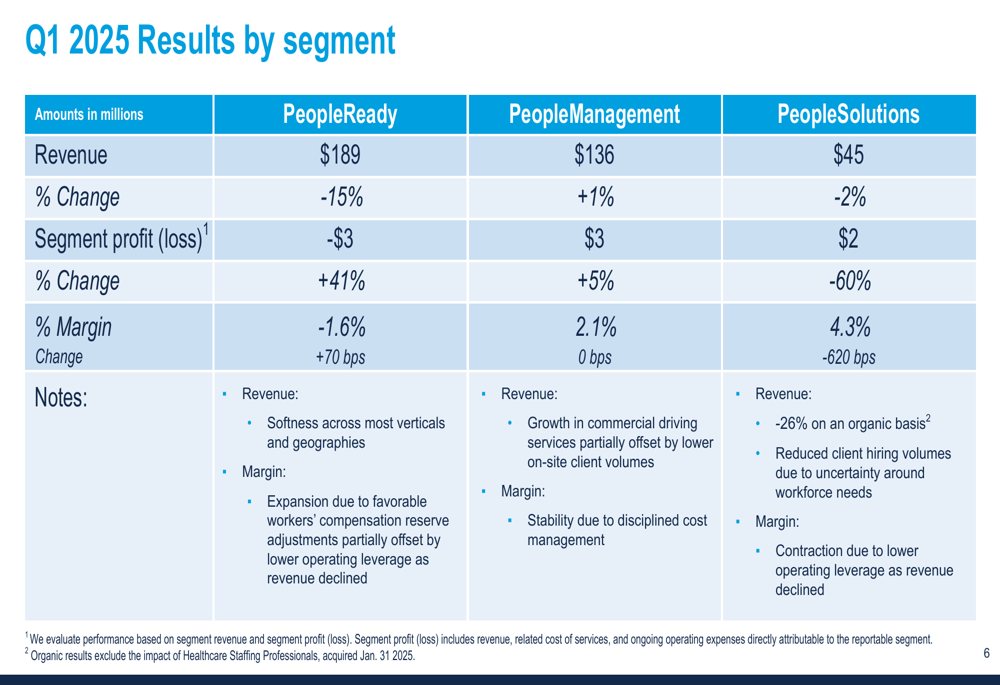

TrueBlue’s performance varied significantly across its three business segments, with PeopleManagement showing modest growth while the other divisions faced challenges.

The PeopleReady segment, which provides on-demand labor for industrial and service sectors, saw revenue decline by 15% to $189 million. Despite this, the segment’s loss narrowed by 41% to $3 million, with margin improving by 70 basis points to -1.6%. Management attributed this improvement to favorable workers’ compensation reserve adjustments.

PeopleManagement, which offers workforce management solutions, was the only segment to report revenue growth, with a 1% increase to $136 million. Segment profit rose 5% to $3 million, maintaining a margin of 2.1%. The company highlighted that commercial driving services achieved double-digit growth for the third consecutive quarter, offsetting lower on-site client volumes in other areas.

The PeopleSolutions segment, which includes recruitment process outsourcing and professional staffing services, reported a 2% revenue decline to $45 million. On an organic basis, excluding the Healthcare Staffing Professionals acquisition, revenue fell by 26%. Segment profit decreased by 60% to $2 million, with margin contracting by 620 basis points to 4.3%, primarily due to reduced client hiring volumes and lower operating leverage.

Financial Position & Outlook

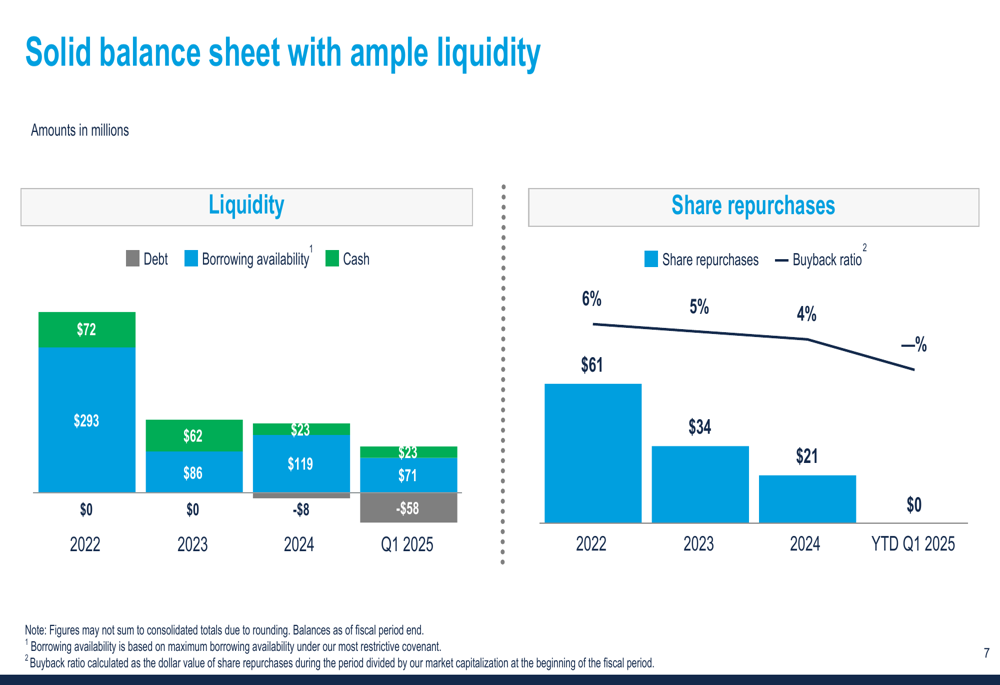

Despite the challenging operating environment, TrueBlue maintained a solid liquidity position with $23 million in cash, $58 million in debt, and $71 million in borrowing availability, totaling $94 million in liquidity.

The following chart illustrates the company’s liquidity position and share repurchase activity:

Unlike previous years, TrueBlue did not repurchase any shares in Q1 2025, likely reflecting a more conservative approach to capital allocation given the current market conditions.

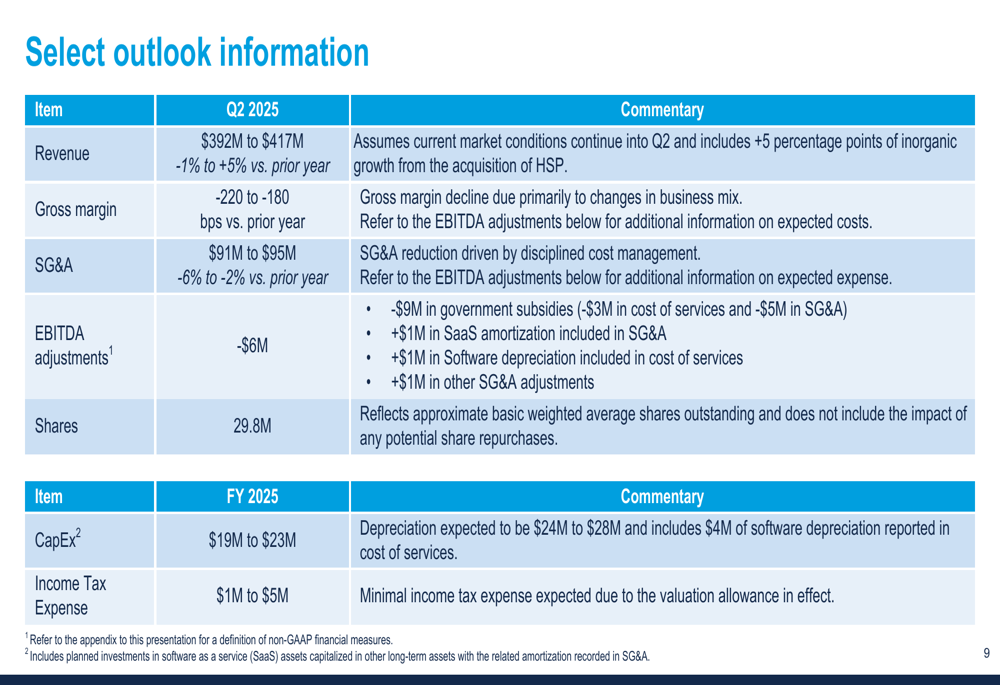

Looking ahead, the company provided the following outlook for Q2 2025 and the full fiscal year:

For Q2 2025, TrueBlue expects revenue between $392 million and $417 million, representing a range of -1% to +5% compared to the prior year. Gross margin is projected to decline by 180 to 220 basis points year-over-year, while SG&A expenses are expected to decrease by 2% to 6%.

For the full fiscal year 2025, the company forecasts capital expenditures of $19 million to $23 million and income tax expense of $1 million to $5 million.

Forward-Looking Statements

TrueBlue’s management expressed cautious optimism about the company’s strategic initiatives, including the integration of Healthcare Staffing Professionals, which remains on track. The continued growth in commercial driving services represents a bright spot amid broader industry challenges.

The company’s focus on cost management has yielded significant SG&A reductions, which could position TrueBlue for improved profitability if and when market conditions stabilize. However, the persistent revenue declines and widening losses underscore the difficult operating environment facing the staffing industry.

As TrueBlue navigates these challenges, investors will be watching closely for signs of stabilization in the company’s core businesses and the potential for a return to profitability in the coming quarters. The Q2 2025 outlook, which suggests the possibility of modest revenue growth, may indicate that the worst of the downturn could be nearing its end, though significant headwinds clearly remain.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.