Gold prices just lower; monthly gains on track

Introduction & Market Context

TrueBlue Inc (NYSE:TBI) released its Q2 2025 earnings presentation on August 4, 2025, revealing flat year-over-year revenue but significantly improved profitability metrics compared to the prior year. The staffing company, which faced challenges in Q1 with an EPS miss, showed signs of stabilization in Q2 despite continued organic revenue decline of 4%. The market responded negatively to the results, with TrueBlue’s stock declining 4.66% to close at $6.65 on the day of the announcement.

The presentation highlighted the company’s focus on cost discipline and growth in skilled businesses, which helped offset weakness in its traditional staffing segments. This quarter marks a continuation of TrueBlue’s efforts to navigate a challenging labor market while positioning itself for future growth.

Quarterly Performance Highlights

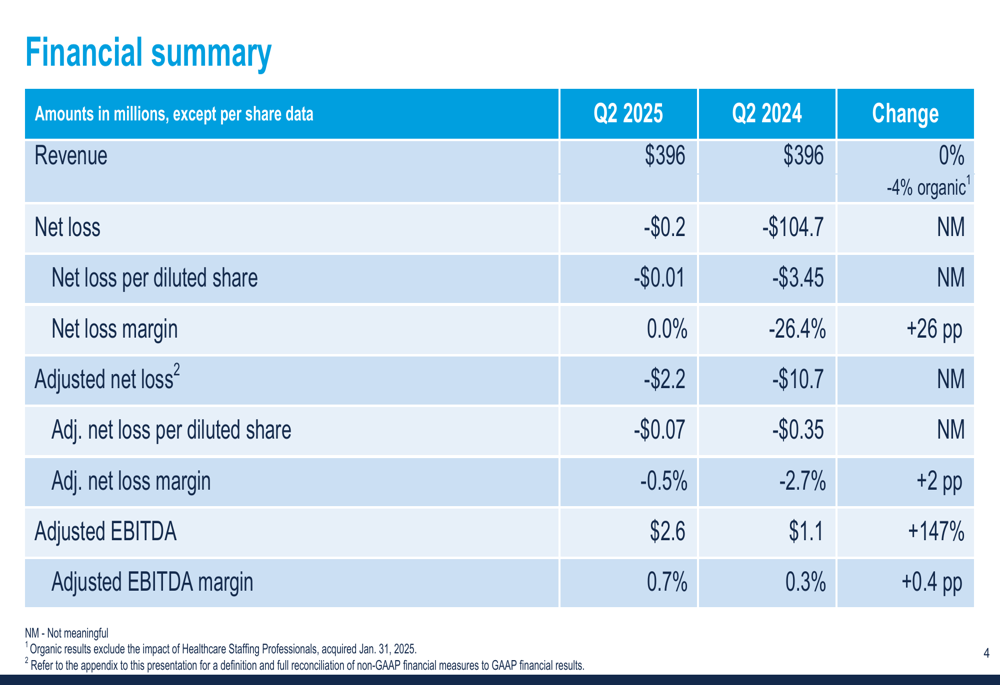

TrueBlue reported total revenue of $396 million for Q2 2025, unchanged from the same period last year, though organic revenue declined by 4%. The company posted a minimal net loss of $0.2 million, a substantial improvement from the $104.7 million loss in Q2 2024, which had included $100 million in non-cash impairment and tax valuation charges.

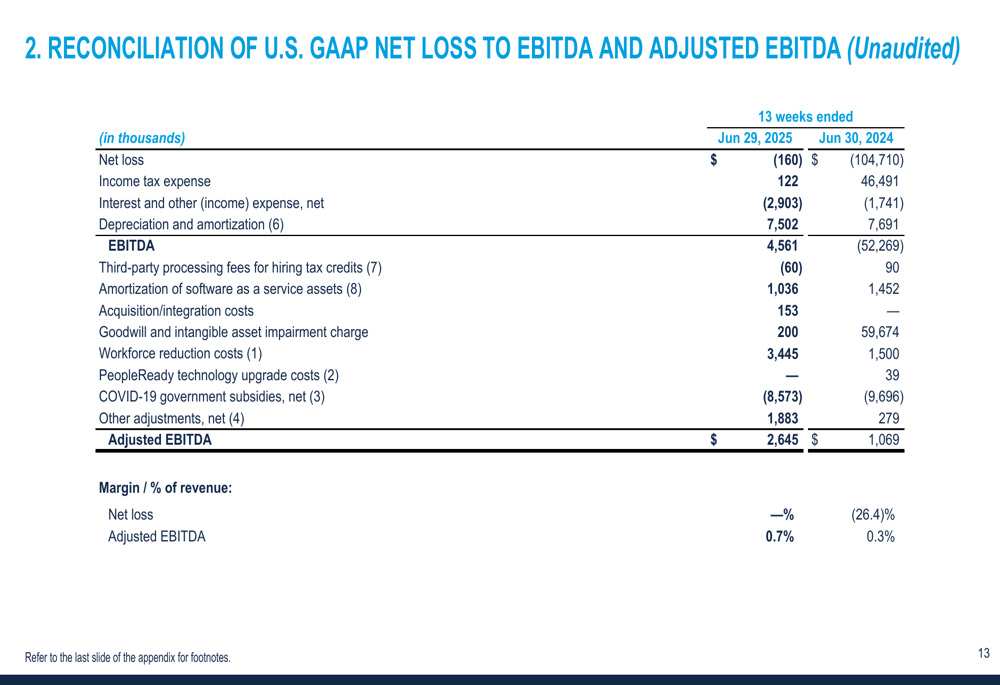

As shown in the following financial summary, adjusted EBITDA increased 147% to $2.6 million, with the adjusted EBITDA margin improving to 0.7% from 0.3% in the prior year:

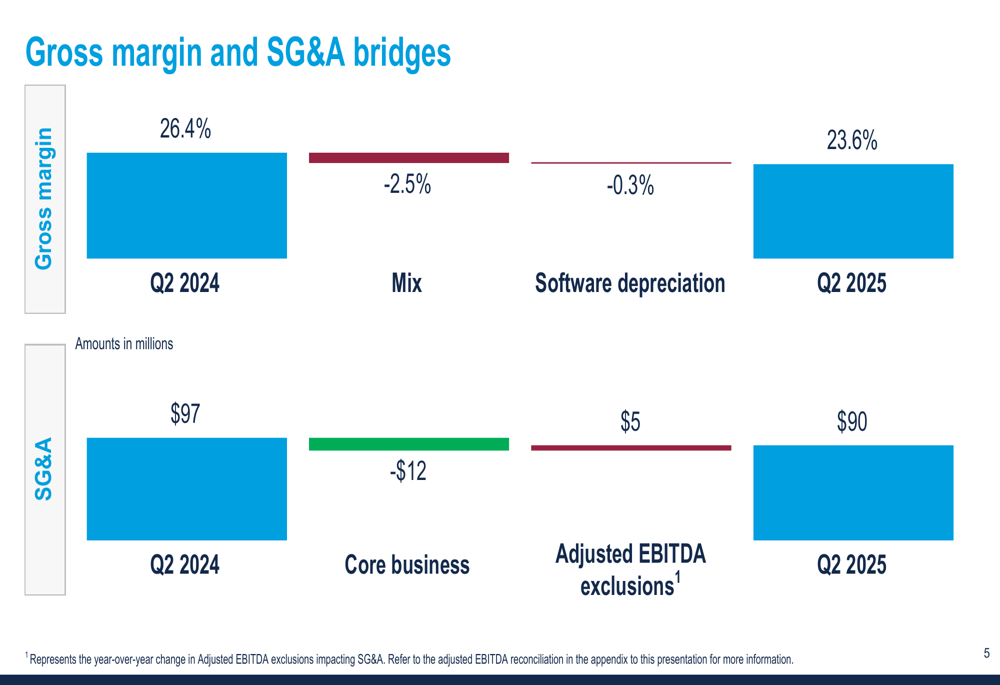

Gross margin decreased by 3 percentage points to 23.6%, primarily due to changes in business mix. However, the company’s disciplined approach to expenses resulted in a 7% reduction in SG&A costs, helping to offset the margin pressure.

The following chart breaks down the changes in gross margin and SG&A between Q2 2024 and Q2 2025:

Segment Analysis

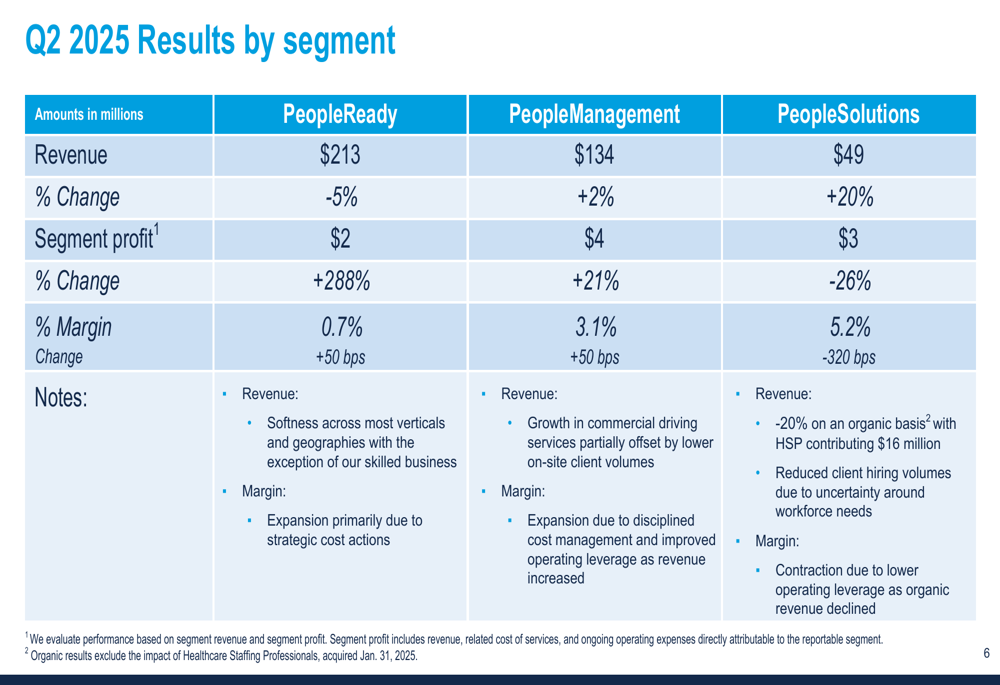

TrueBlue’s performance varied significantly across its three business segments. The PeopleReady segment, which provides on-demand labor for industrial and service sectors, saw a 5% revenue decline to $213 million. Despite this, segment profit increased by 288% to $2 million, with margin expanding by 50 basis points to 0.7%.

The PeopleManagement segment, which offers contingent workforce management solutions, grew revenue by 2% to $134 million. Segment profit increased 21% to $4 million, with margin improving by 50 basis points to 3.1%.

The PeopleSolutions segment, which includes the recently acquired HSP, delivered the strongest revenue growth at 20%, reaching $49 million. However, segment profit declined 26% to $3 million, with margin contracting 320 basis points to 5.2%.

The detailed segment breakdown is illustrated in the following chart:

Financial Position

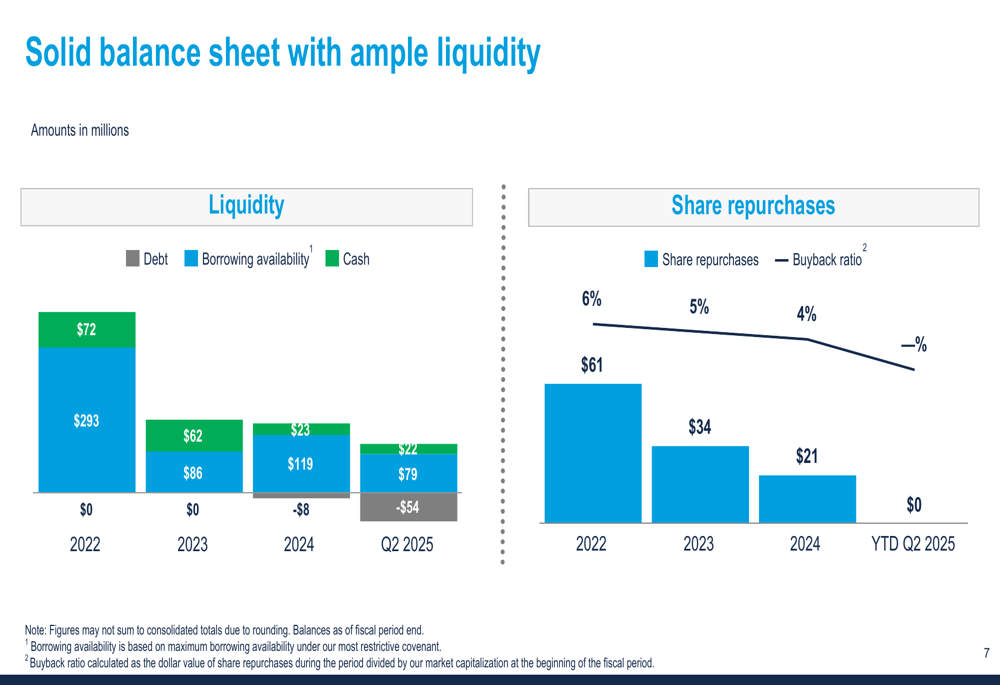

TrueBlue maintained a solid balance sheet with ample liquidity at the end of Q2 2025. The company reported cash of $22 million and debt of $54 million, resulting in total liquidity of $101 million when including borrowing availability of $79 million. During the quarter, TrueBlue reduced its debt by $4 million and increased working capital by $14 million.

The following chart illustrates TrueBlue’s liquidity position and share repurchase activity over time:

Notably, the company has not conducted any share repurchases year-to-date in 2025, a departure from previous years when buybacks ranged from 4-6% of market capitalization. This suggests management may be prioritizing debt reduction and operational investments over returning capital to shareholders in the current environment.

Forward Outlook

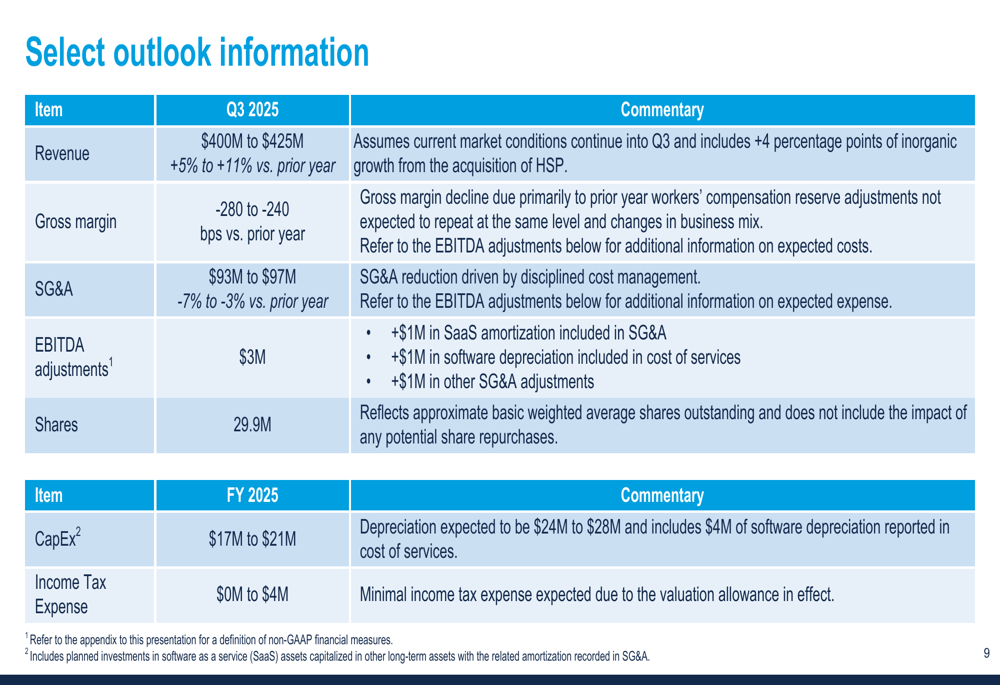

Looking ahead to Q3 2025, TrueBlue provided an optimistic outlook, projecting revenue between $400 million and $425 million, representing growth of 5% to 11% compared to the prior year. However, the company expects continued pressure on gross margins, forecasting a decline of 240 to 280 basis points year-over-year.

Management anticipates SG&A expenses of $93 million to $97 million in Q3, representing a 3% to 7% reduction from the prior year, as cost discipline remains a priority. For the full year 2025, capital expenditures are expected to range from $17 million to $21 million, with minimal income tax expense of $0 million to $4 million.

The detailed outlook is presented in the following chart:

Reconciliation of Non-GAAP Measures

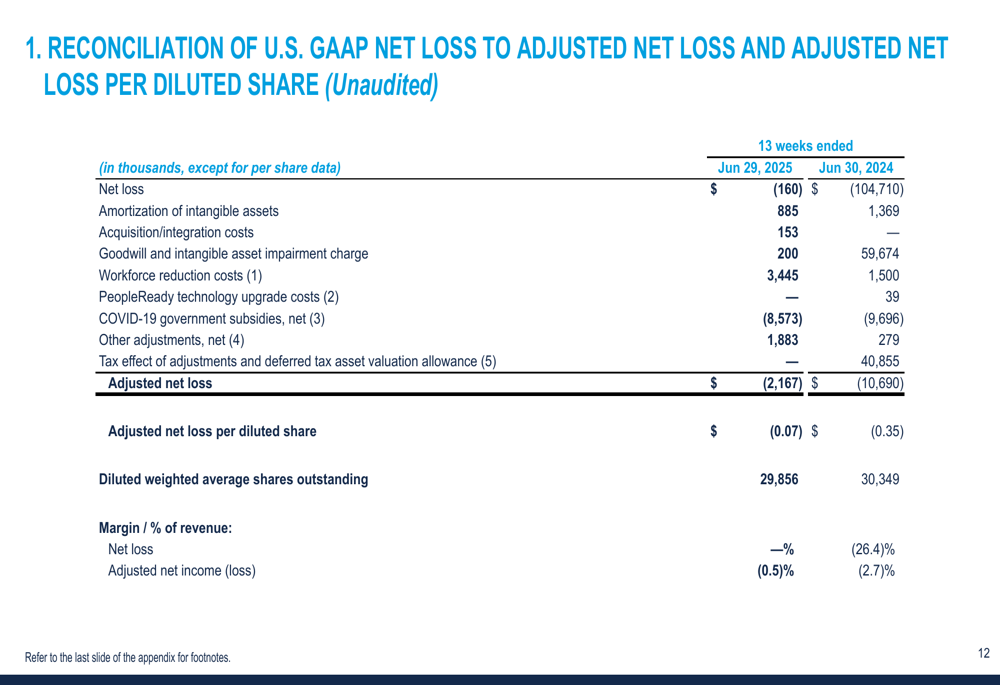

To provide a clearer picture of its underlying performance, TrueBlue presented reconciliations of GAAP to non-GAAP financial measures. The company’s adjusted net loss of $2.2 million for Q2 2025 represented a significant improvement from the $10.7 million adjusted net loss in Q2 2024.

The reconciliation highlights several notable adjustments, including a $0.2 million goodwill and intangible asset impairment charge in Q2 2025 compared to $59.7 million in Q2 2024, as well as $3.4 million in workforce reduction costs in the current quarter versus $1.5 million in the prior year.

The detailed reconciliation of GAAP net loss to adjusted net loss is shown below:

Similarly, the reconciliation to adjusted EBITDA reveals how the company achieved its 147% improvement in this key metric:

Conclusion

TrueBlue’s Q2 2025 results demonstrate the company’s ability to improve profitability despite challenging market conditions and flat revenue. The significant reduction in net loss and growth in adjusted EBITDA highlight the effectiveness of management’s cost discipline and strategic focus on higher-margin skilled businesses.

However, the company continues to face headwinds, including organic revenue decline and gross margin pressure due to business mix changes. The market’s negative reaction to the results suggests investors may have expected stronger performance or were concerned about the continued organic revenue decline despite the improved profitability metrics.

As TrueBlue looks toward Q3 2025 with projected revenue growth of 5% to 11%, the company’s ability to maintain cost discipline while driving growth in its skilled businesses will be crucial for sustaining the positive momentum in profitability and eventually returning to organic growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.