Here’s why Citi says crypto prices have been weak recently

Introduction & Market Context

TrueBlue Inc. (NYSE:TBI) released its third-quarter 2025 earnings presentation on November 3, showing improved revenue growth and profitability metrics despite ongoing margin challenges. The workforce solutions provider reported a 13% year-over-year revenue increase, exceeding analyst expectations, though investors responded cautiously as the stock declined 1.27% in after-hours trading to $4.74.

The company’s results reflect its continued focus on digital transformation and specialized workforce solutions in a labor market that remains complex. TrueBlue’s performance comes as its stock trades in the lower half of its 52-week range of $3.45 to $9.05, highlighting the ongoing challenges in the staffing sector despite operational improvements.

Quarterly Performance Highlights

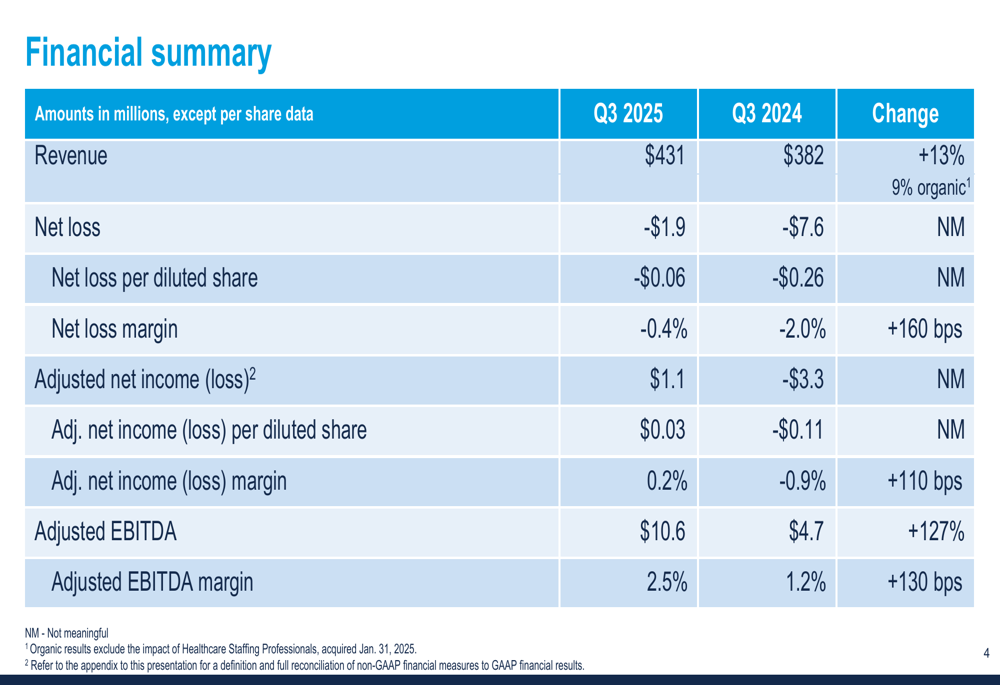

TrueBlue reported total revenue of $431 million for Q3 2025, representing a 13% increase compared to the same period last year, with organic growth contributing 9% of the increase. Despite this strong top-line performance, the company posted a net loss of $1.9 million, though this marked a substantial improvement from the $7.6 million loss recorded in Q3 2024.

As shown in the following financial summary, the company achieved significant improvements in adjusted metrics:

Adjusted EBITDA more than doubled to $10.6 million compared to $4.7 million in the prior year, with the adjusted EBITDA margin expanding by 130 basis points to 2.5%. The company also swung to an adjusted net income of $1.1 million ($0.03 per diluted share) from an adjusted net loss of $3.3 million (-$0.11 per diluted share) in Q3 2024.

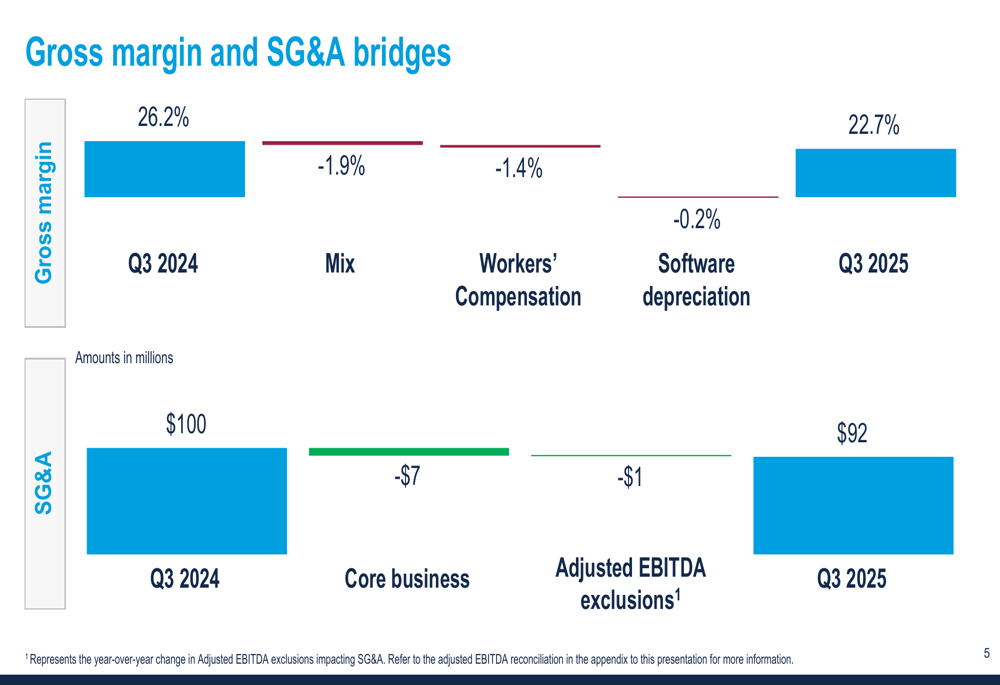

However, gross margin declined significantly, dropping to 22.7% from 26.2% in the prior year. The following chart breaks down the factors contributing to this decline:

The gross margin contraction was primarily driven by changes in business mix (-1.9%), lower workers’ compensation benefits (-1.4%), and increased software depreciation (-0.2%). Despite these headwinds, TrueBlue effectively managed its SG&A expenses, which decreased by 8% year-over-year, helping to offset the margin pressure.

Segment Analysis

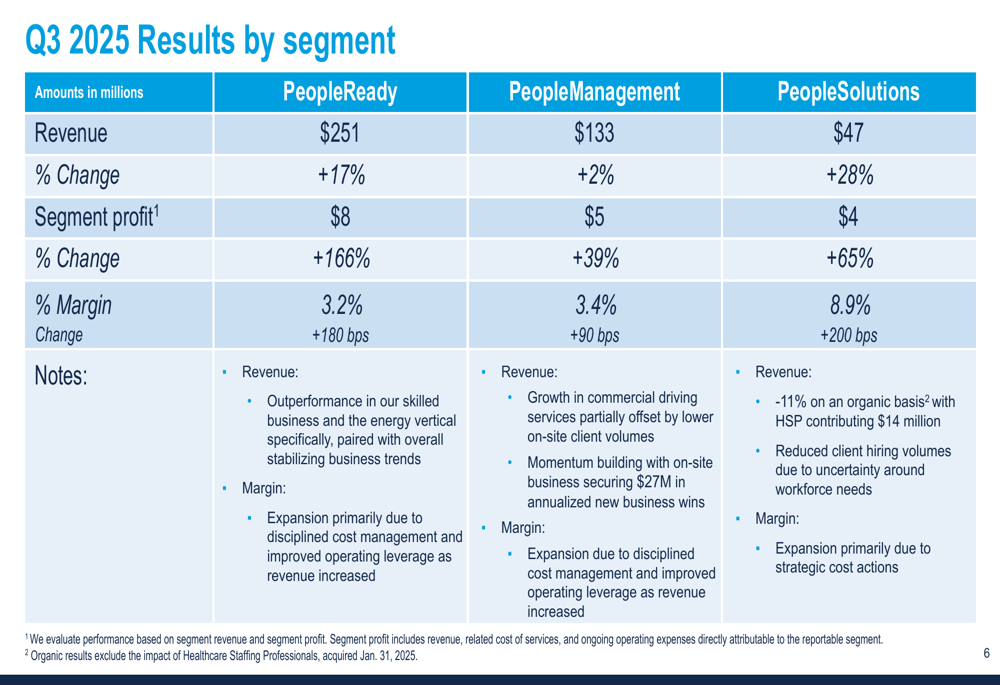

TrueBlue’s performance varied across its three business segments, with each showing revenue growth but at different rates:

PeopleReady, the company’s largest segment providing on-demand labor, delivered the strongest performance with a 17% revenue increase to $251 million. Segment profit surged 166% to $8 million, with margin expanding 180 basis points to 3.2%. Management attributed this growth to outperformance in the skilled business and continued recovery in the core blue-collar business.

PeopleManagement, which offers on-site workforce management solutions, saw more modest growth of 2% to $133 million in revenue. Despite the slower top-line growth, segment profit increased 39% to $5 million, with margin improving by 90 basis points to 3.4%. The company noted that growth in commercial driving services helped offset ongoing challenges in the transportation market.

PeopleSolutions, focused on recruitment process outsourcing and managed service provider offerings, recorded the highest percentage growth with revenue increasing 28% to $47 million. This growth was partially driven by the acquisition of Healthcare Staffing Professionals (HSP). Segment profit rose 65% to $4 million, with margin expanding 200 basis points to 8.9%.

Financial Position and Outlook

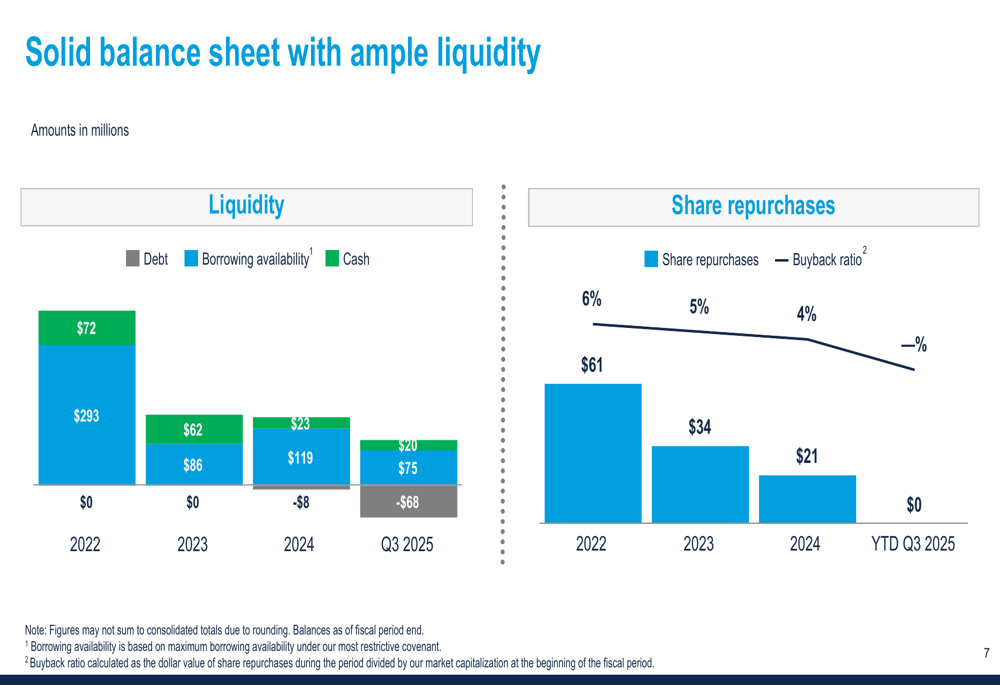

TrueBlue maintained a solid balance sheet with $20 million in cash and $68 million in debt at the end of Q3 2025. Total liquidity stood at $95 million, including $75 million in borrowing availability.

As illustrated in the following chart, the company has maintained financial flexibility while reducing debt:

Looking ahead to Q4 2025, TrueBlue provided the following guidance:

The company expects Q4 2025 revenue to range between $399 million and $424 million, representing growth of 4% to 10% compared to the prior year. This outlook includes approximately 4% inorganic growth from the HSP acquisition. However, gross margin is projected to decline by 370 to 410 basis points year-over-year, primarily due to prior year workers’ compensation adjustments.

SG&A expenses are expected to decrease by 11% to 15% compared to Q4 2024, reflecting continued cost discipline. The company anticipates capital expenditures of $17 million to $19 million for the full fiscal year 2025.

Strategic Initiatives

Throughout the earnings presentation, TrueBlue emphasized its strategic focus on digital transformation and specialized workforce solutions. CEO Taryn Owen highlighted that the company’s "digitally-enabled specialized workforce solutions are uniquely positioned to help businesses solve complex talent challenges with precision, scale, and agility."

The acquisition of Healthcare Staffing Professionals represents part of TrueBlue’s strategy to expand into higher-margin, specialized staffing segments. This acquisition has already contributed to the strong performance of the PeopleSolutions segment.

CFO Carl Schweihs expressed confidence in the company’s positioning, stating, "We feel like with our optimized fixed cost base, we’re poised for significant incremental margins and expanding our profitability as demand rebounds."

Despite these positive developments, TrueBlue continues to face challenges, including gross margin pressure, cautious client sentiment, and ongoing market uncertainties. Management acknowledged during the earnings call that the transportation market remains challenging, and that mixed impacts from immigration reforms could create uncertainties going forward.

Nevertheless, the company’s improved financial performance and disciplined cost management suggest that TrueBlue is making progress in navigating these challenges while positioning itself for future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.