Fed Governor Adriana Kugler to resign

Introduction & Market Context

Truist Financial Corp (NYSE:TFC) reported its first quarter 2025 results on April 17, with shares jumping 13.86% in premarket trading to $40.99, despite mixed financial performance. The bank posted net income available to common shareholders of $1.2 billion, or $0.87 per diluted share, showing resilience in a challenging rate environment while highlighting its digital transformation progress and capital strength.

The results come after Truist’s stock had declined to $36.00 at the previous close, significantly below its 52-week high of $49.06. The positive market reaction suggests investors are focusing on the bank’s forward guidance and capital return plans rather than the quarter-over-quarter earnings decline from Q4 2024’s $0.91 per share.

Quarterly Performance Highlights

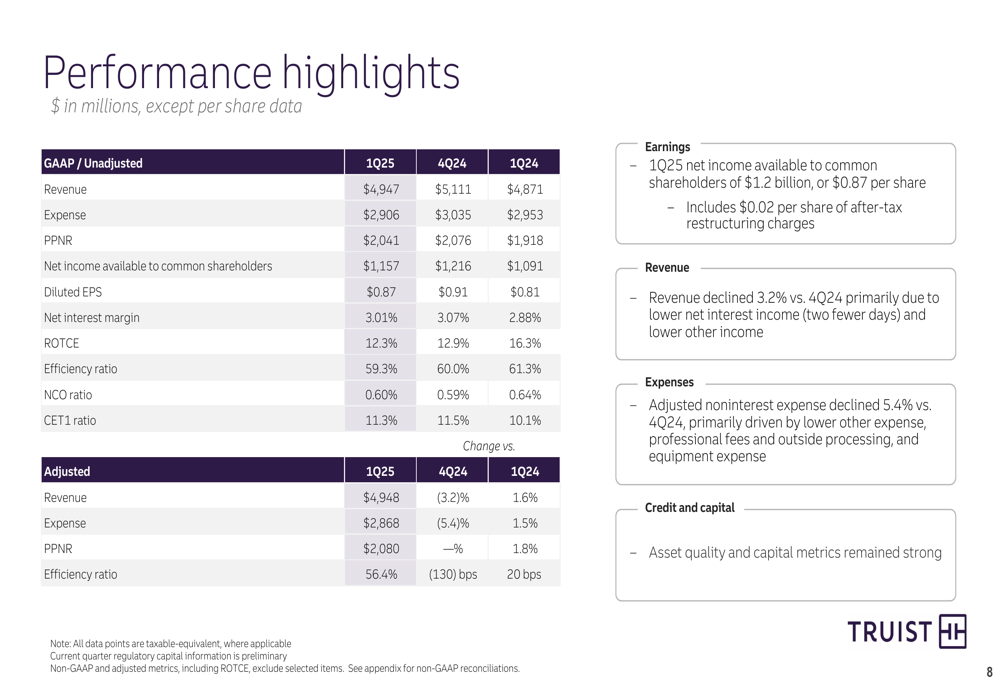

Truist’s Q1 2025 financial results showed mixed performance compared to the previous quarter. The bank reported $4.947 billion in revenue, down from $5.111 billion in Q4 2024, primarily due to lower net interest income affected by fewer days in the quarter.

As shown in the following performance highlights slide, the bank maintained expense discipline with an efficiency ratio of 59.3%, improving from 60.0% in the previous quarter:

Net interest margin decreased to 3.01% from 3.07% in the previous quarter but remained above the 2.88% reported in Q1 2024. Return on tangible common equity (ROTCE) declined to 12.3% from 12.9% in Q4 2024 and 16.3% in Q1 2024, reflecting the impact of higher capital levels following previous strategic initiatives.

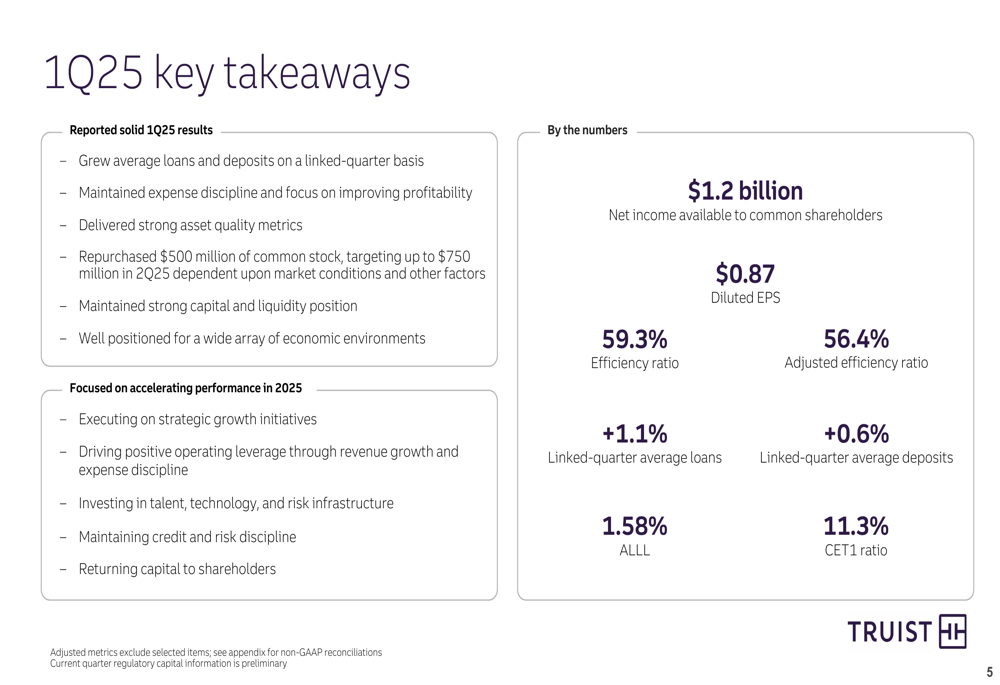

The bank’s key takeaways emphasized modest growth in average loans (1.1%) and deposits (0.6%) on a linked-quarter basis, while maintaining strong asset quality metrics and capital position:

Digital Transformation Progress

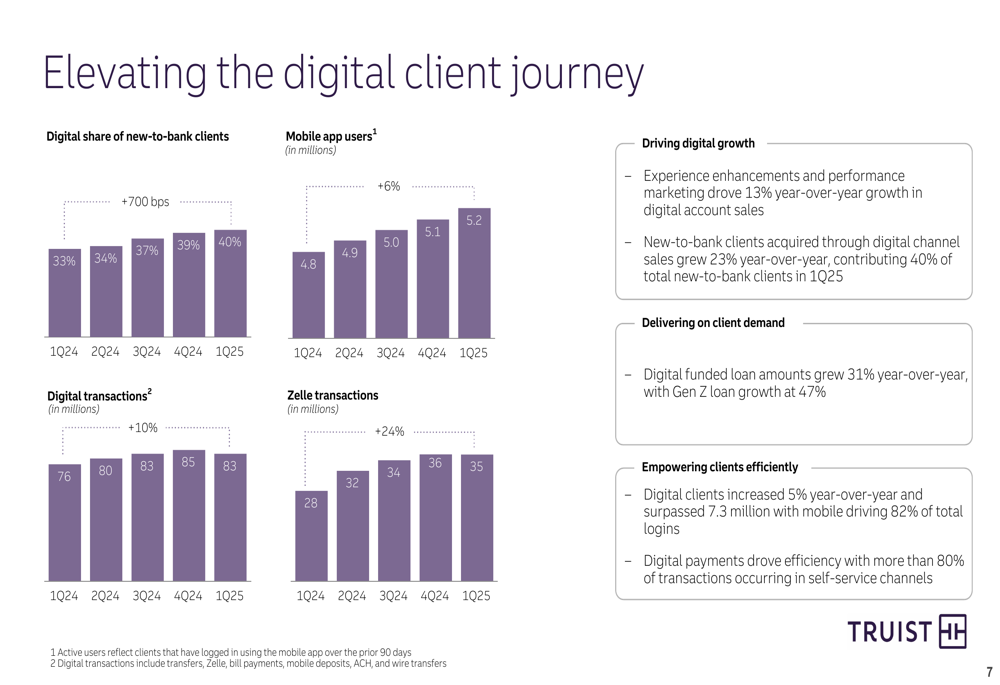

A standout aspect of Truist’s presentation was the continued momentum in its digital banking initiatives. The bank reported significant growth in digital engagement metrics, with mobile app users increasing from 4.8 million in Q1 2024 to 5.2 million in Q1 2025, representing an 8.3% year-over-year increase.

The digital transformation is showing tangible results in client acquisition and transaction volumes, as illustrated in this comprehensive digital metrics slide:

Digital share of new-to-bank clients increased from 33% in Q1 2024 to 40% in Q1 2025, while digital transactions grew from 76 million to 83 million over the same period. Particularly notable was the 25% year-over-year growth in Zelle transactions, increasing from 28 million to 35 million, demonstrating strong adoption of digital payment solutions.

The bank highlighted that digital payments now drive efficiency for over 80% of transactions, contributing to operational efficiency while enhancing the customer experience.

Balance Sheet and Credit Quality

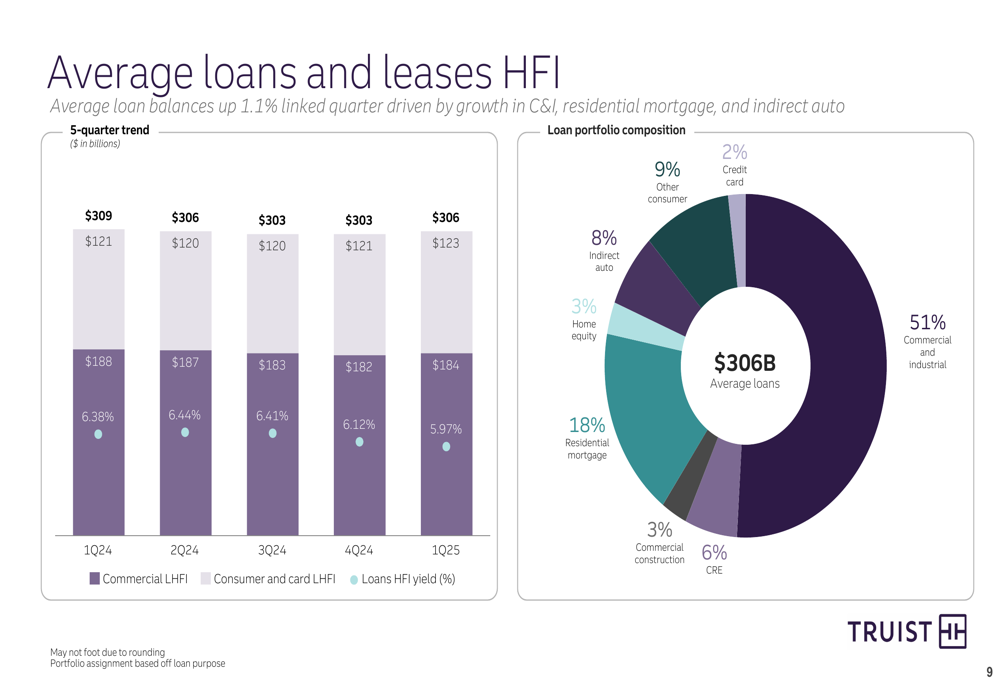

Truist’s loan portfolio showed modest growth, with average loans increasing 1.1% linked quarter, primarily driven by growth in commercial and industrial (C&I), residential mortgage, and indirect auto segments. The loan portfolio remains well-diversified, with C&I loans representing the largest component at 51% of total loans.

The following slide details the composition and yield trends of the loan portfolio:

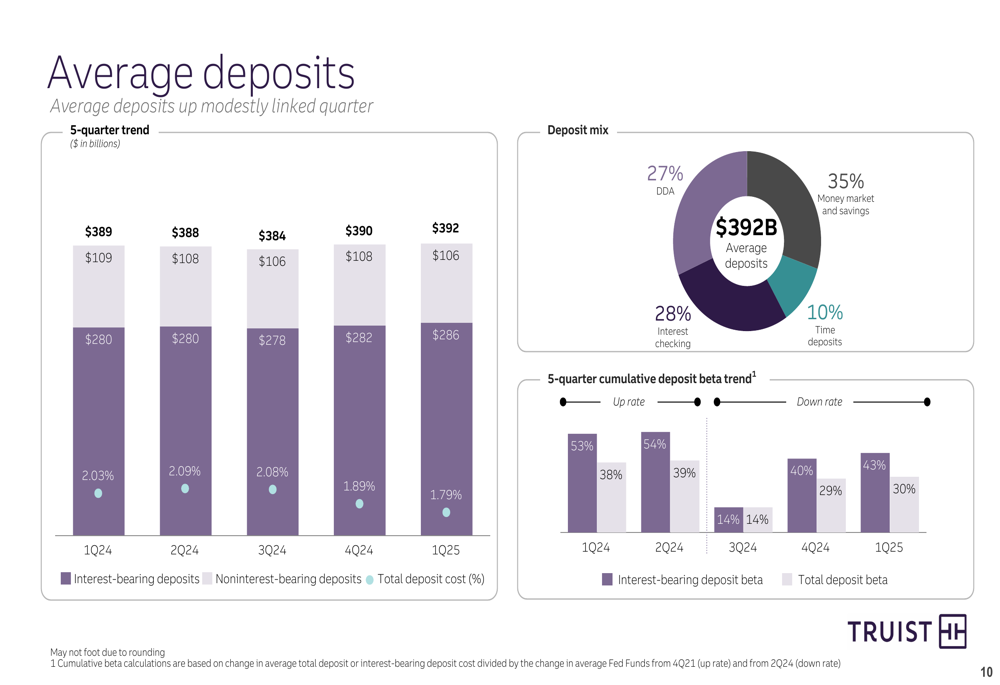

On the deposit side, average deposits increased by 0.6% linked quarter to $392 billion. The deposit mix remained relatively stable with 27% in demand deposits, 28% in interest checking, 35% in money market and savings, and 10% in time deposits.

Asset quality metrics remained strong, with the net charge-off ratio at 0.60%, slightly up from 0.59% in Q4 2024 but improved from 0.64% in Q1 2024. The allowance for loan and lease losses (ALLL) ratio stood at 1.58%, reflecting the bank’s conservative approach to credit risk management.

Capital Management and Outlook

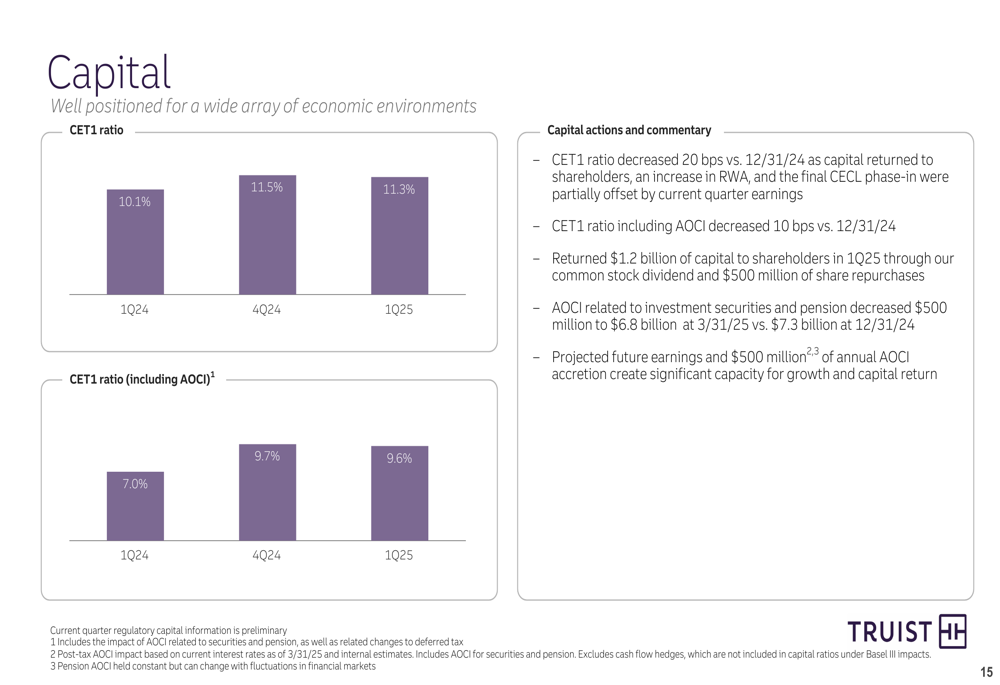

Truist maintained a strong capital position with a Common Equity Tier 1 (CET1) ratio of 11.3%, slightly down from 11.5% in Q4 2024 but significantly improved from 10.1% in Q1 2024. This capital strength enabled the bank to repurchase $500 million of common stock during the quarter, with plans to increase buybacks to up to $750 million in Q2 2025.

The bank’s capital position and actions are illustrated in the following slide:

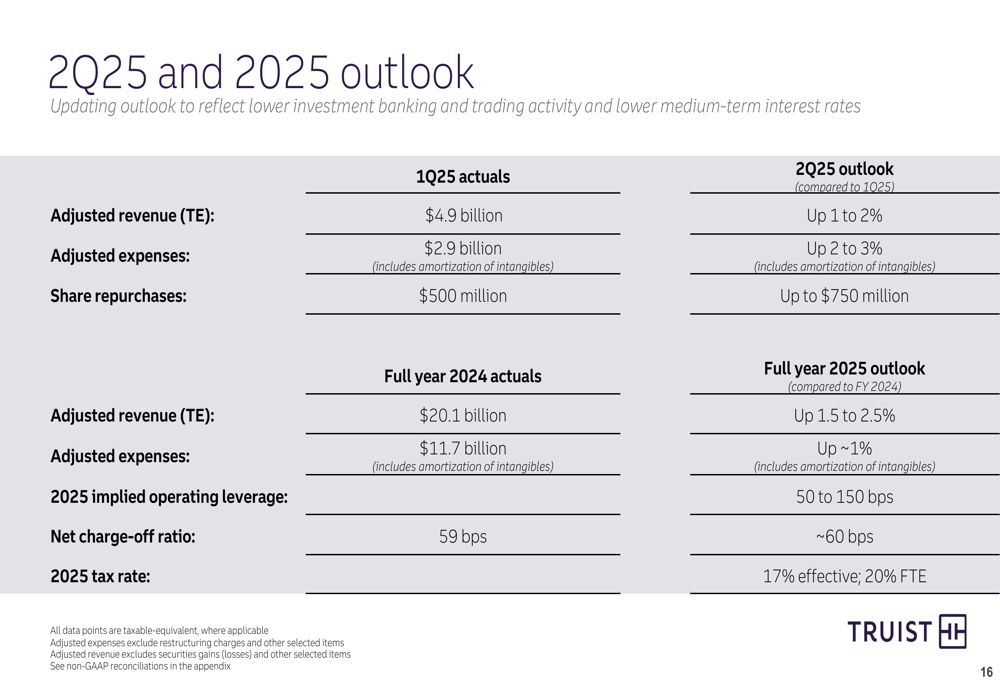

Looking ahead, Truist provided guidance for Q2 2025 and the full year 2025, expecting modest pressure on revenue in the near term but maintaining its commitment to positive operating leverage for the full year 2025:

The bank’s strategic priorities for 2025 include executing on growth initiatives, driving positive operating leverage through revenue growth and expense discipline, investing in talent and technology, maintaining credit discipline, and returning capital to shareholders.

Forward-Looking Statements

Truist’s management emphasized its focus on expanding relationships with existing clients and growing market share in key segments. The bank highlighted its Consumer & Small Business Banking segment, where consumer loan production increased to $3.7 billion, and its Wholesale Banking segment, where average wholesale loans increased by $2.3 billion.

The bank’s net interest income outlook assumes continued pressure in Q2 2025, with a 1.5% expected decline from Q1 levels. However, management expressed confidence that deposit beta acceleration would catch up to asset repricing by early 2025, potentially stabilizing and then improving margins as the year progresses.

Truist remains committed to its medium-term target of achieving mid-teens ROTCE, supported by its capital deployment strategy and focus on operational efficiency. The bank’s strong capital position provides flexibility to pursue growth opportunities while continuing to return significant capital to shareholders through dividends and share repurchases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.