OpenAI seeks government backing for AI chip investments

Introduction & Market Context

Twilio Inc. (NYSE:TWLO) released its second-quarter 2025 earnings results on August 7, 2025, reporting accelerating revenue growth and improved profitability. Despite the seemingly strong performance, Twilio’s stock dropped 12.76% in premarket trading to $106.77, suggesting investors may have concerns about the company’s guidance or other forward-looking indicators.

The cloud communications platform provider reported total revenue of $1.228 billion, representing 13% year-over-year growth, with notable strength in its Communications segment while its Segment division showed stagnation.

Quarterly Performance Highlights

Twilio delivered solid financial results across key metrics for Q2 2025, continuing its trend of accelerating growth from previous quarters.

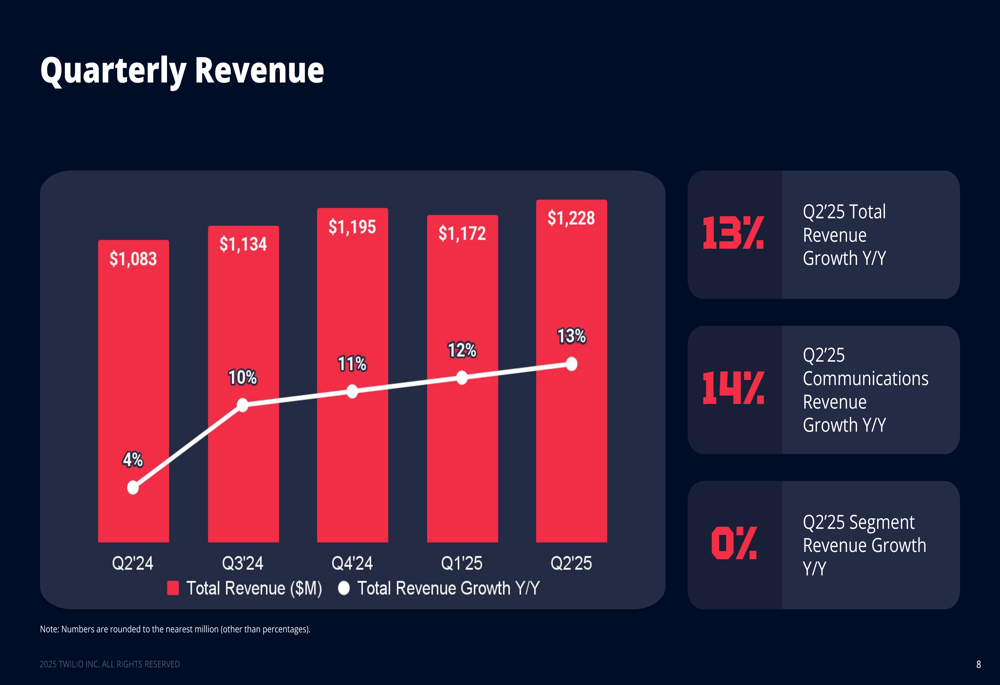

As shown in the following chart of quarterly revenue:

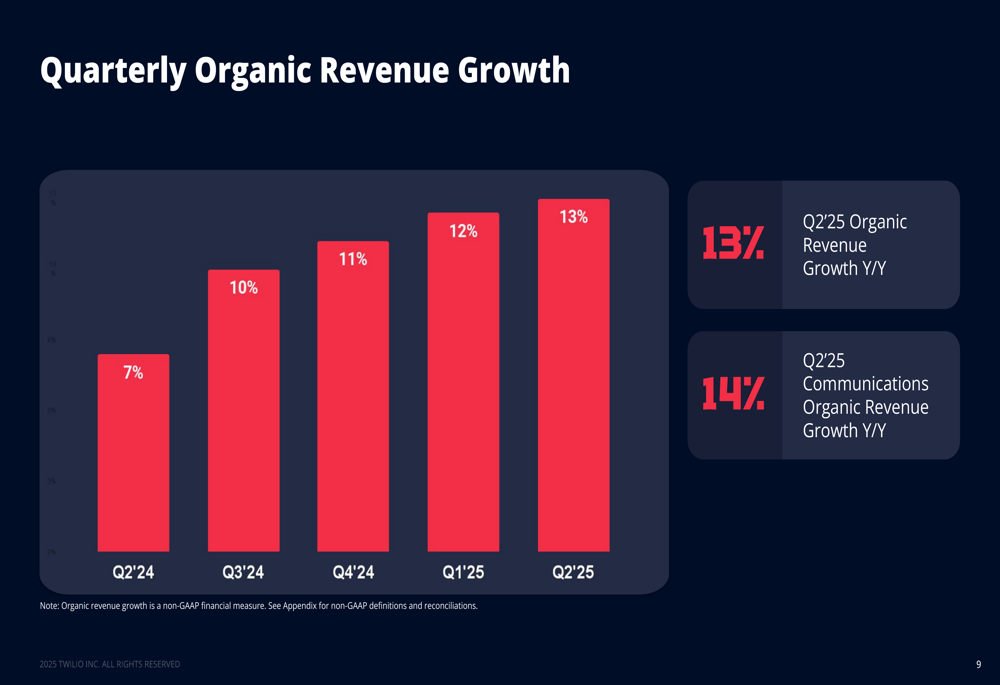

Total (EPA:TTEF) revenue reached $1.228 billion, up 13% year-over-year, marking the fifth consecutive quarter of accelerating growth from the 4% reported in Q2 2024. The company’s organic revenue growth, which excludes certain impacts, also showed consistent improvement:

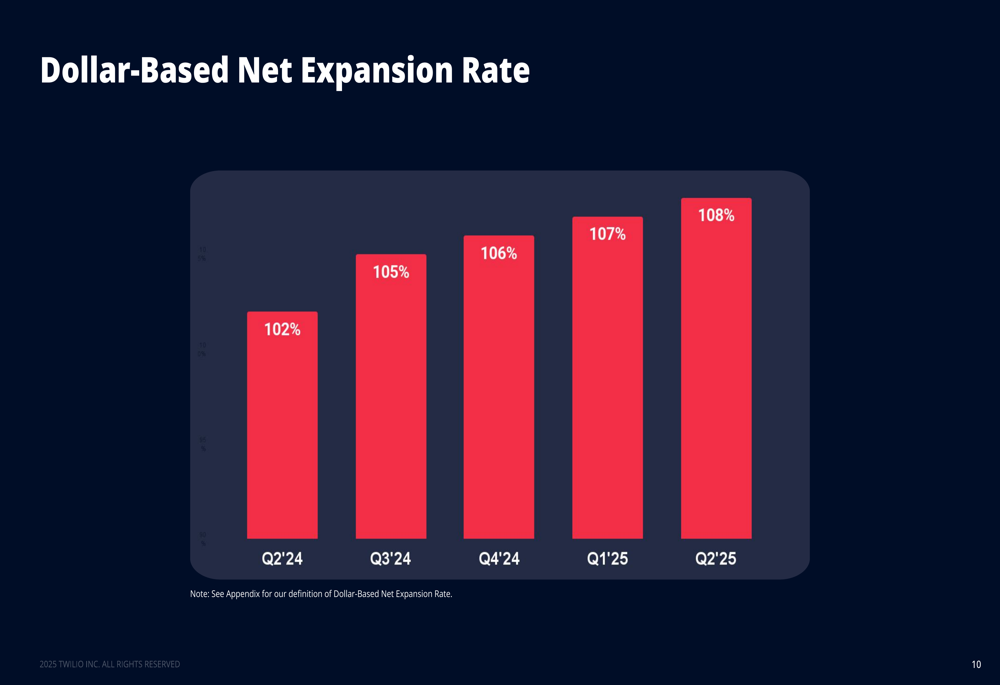

The company’s Dollar-Based Net Expansion Rate, a key indicator of customer spending growth, improved to 108% from 102% in the same quarter last year, reflecting Twilio’s success in expanding relationships with existing customers.

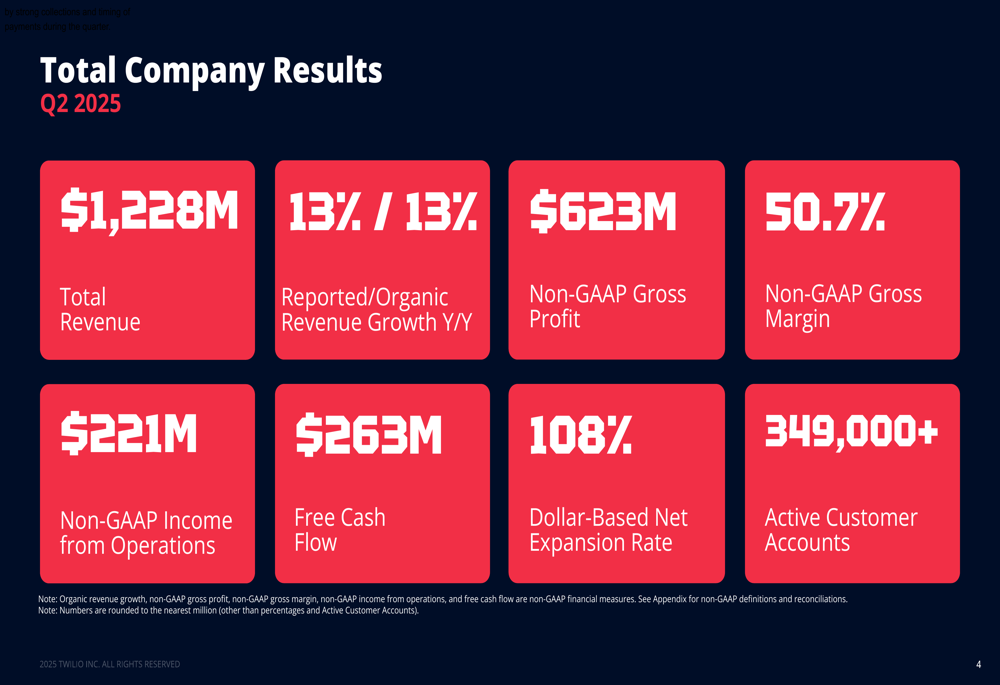

The overall quarterly performance showed strength across multiple financial metrics:

Segment Performance Analysis

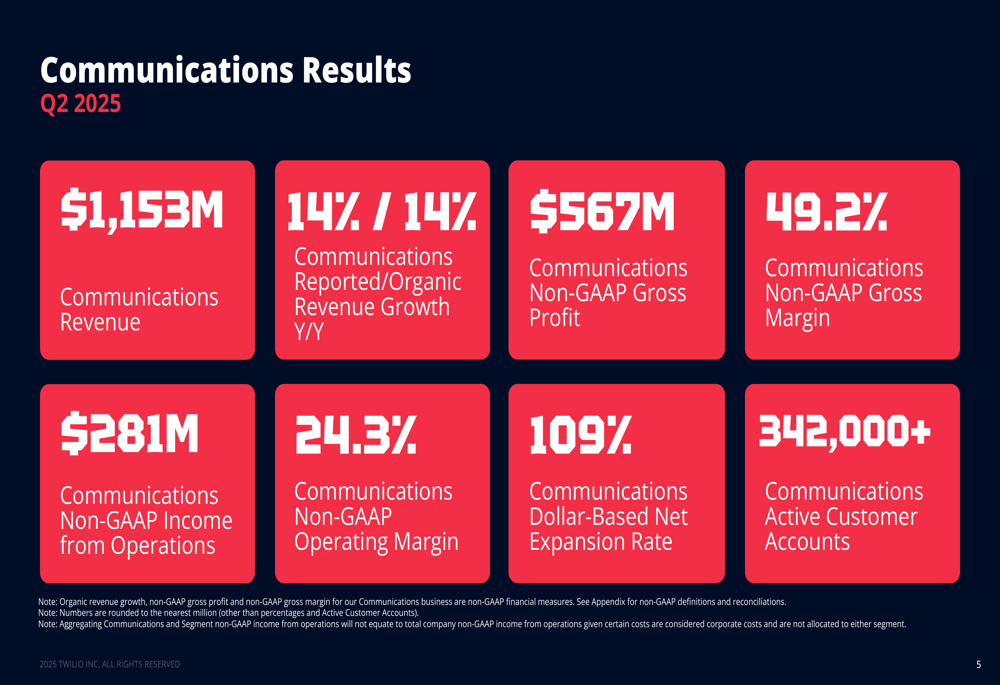

Twilio’s business performance showed a clear divergence between its two main segments. The Communications segment, which represents the bulk of the company’s revenue, delivered strong results with 14% year-over-year growth:

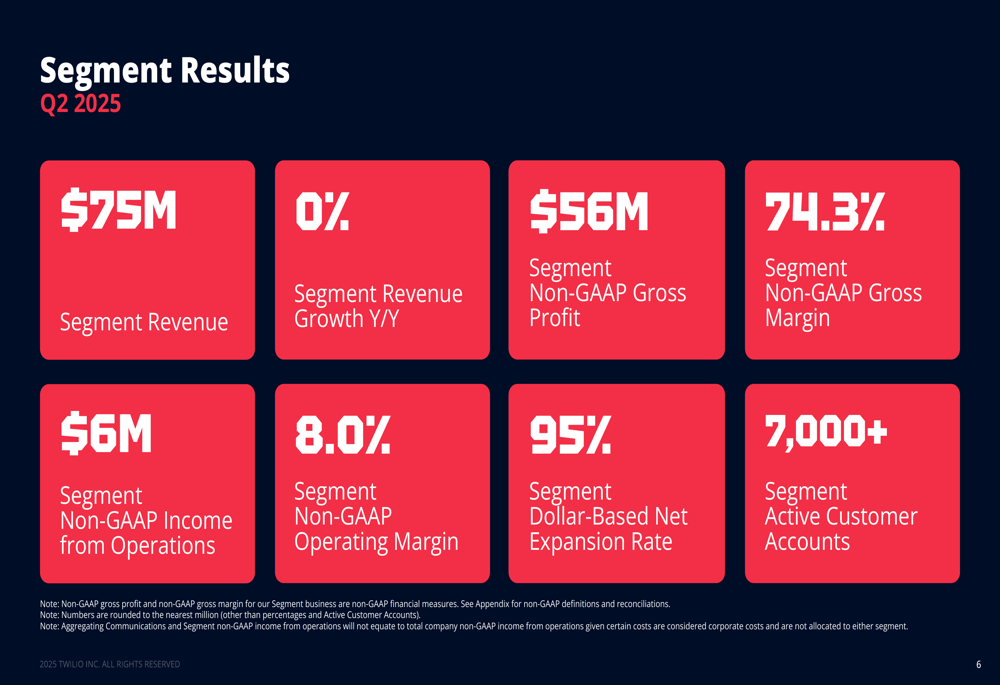

In contrast, the Segment business unit, which focuses on customer data platforms, reported flat revenue growth at 0% year-over-year, though it maintained higher gross margins at 74.3%:

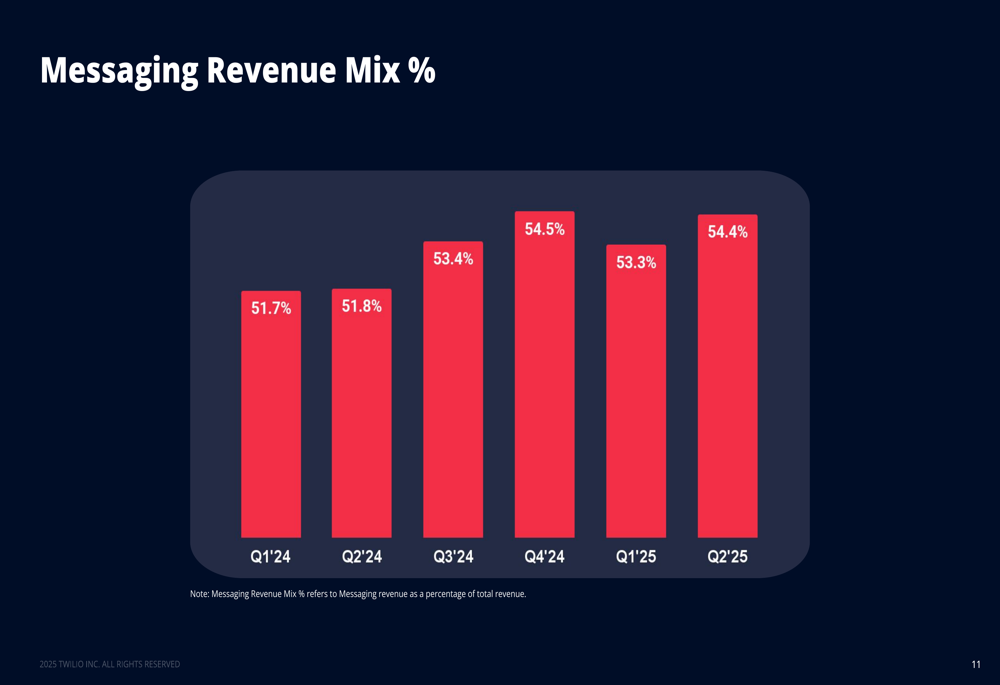

The disparity between segment performances highlights Twilio’s ongoing challenge in driving growth across all parts of its business. Messaging continues to be the dominant revenue driver, accounting for 54.4% of total revenue in Q2 2025, up from 51.8% in Q2 2024:

Operational Efficiency & Profitability

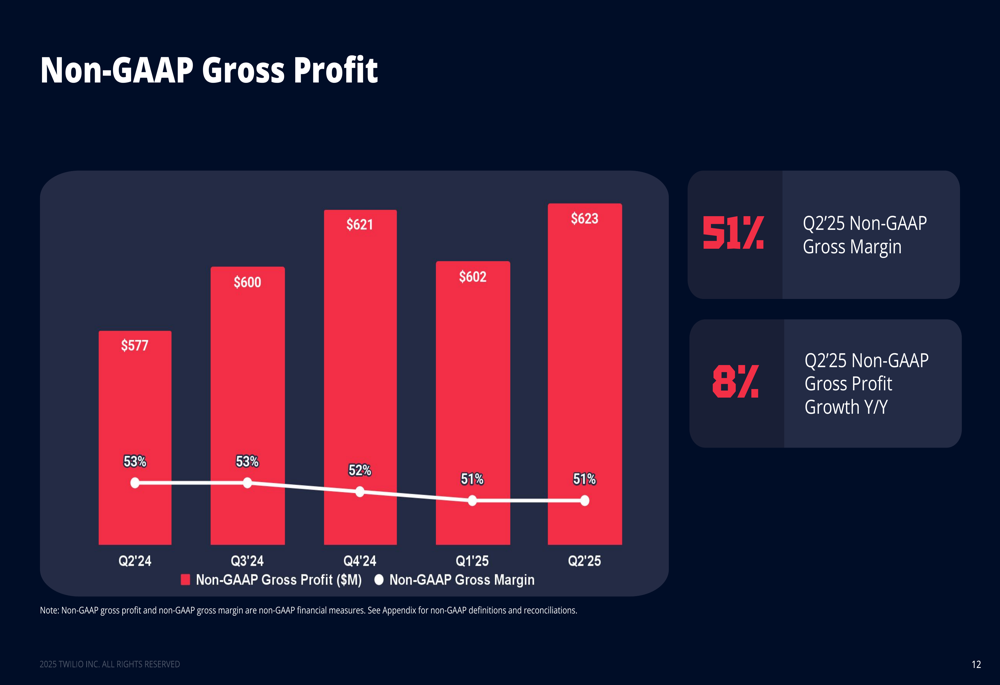

Twilio demonstrated improved operational efficiency and profitability metrics during the quarter. Non-GAAP gross profit reached $623 million, though gross margins slightly declined to 51% from 53% a year ago:

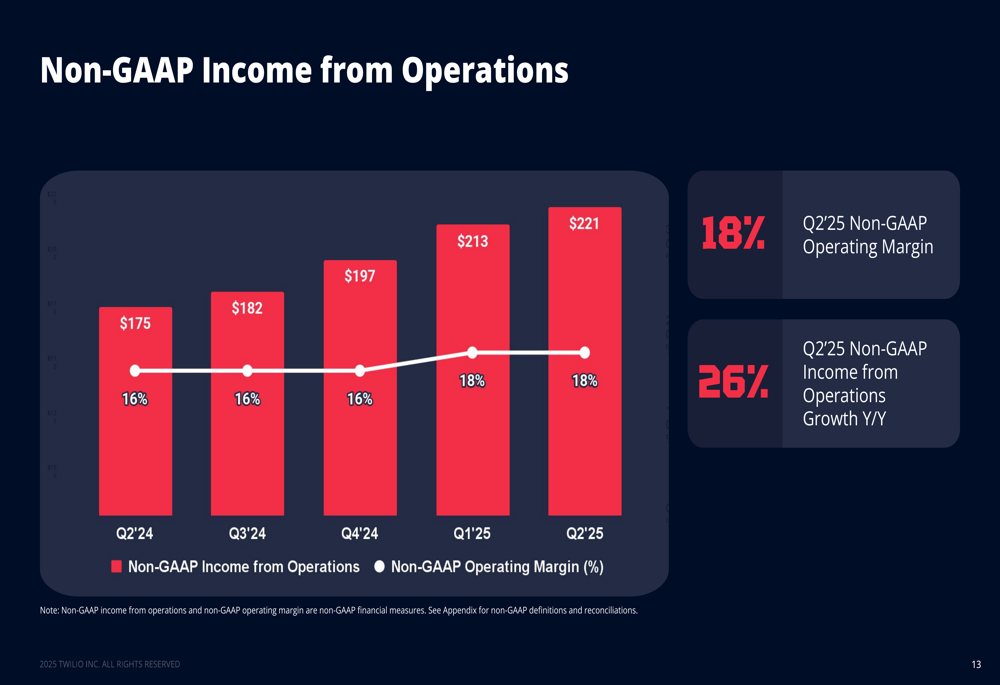

The company showed more significant improvement in operational profitability, with Non-GAAP income from operations increasing 26% year-over-year to $221 million, maintaining an 18% operating margin:

Notably, Twilio achieved GAAP profitability with $37 million in income from operations, representing a 3% margin compared to a -2% margin in Q2 2024. This marks a significant improvement in the company’s path to sustainable GAAP profitability.

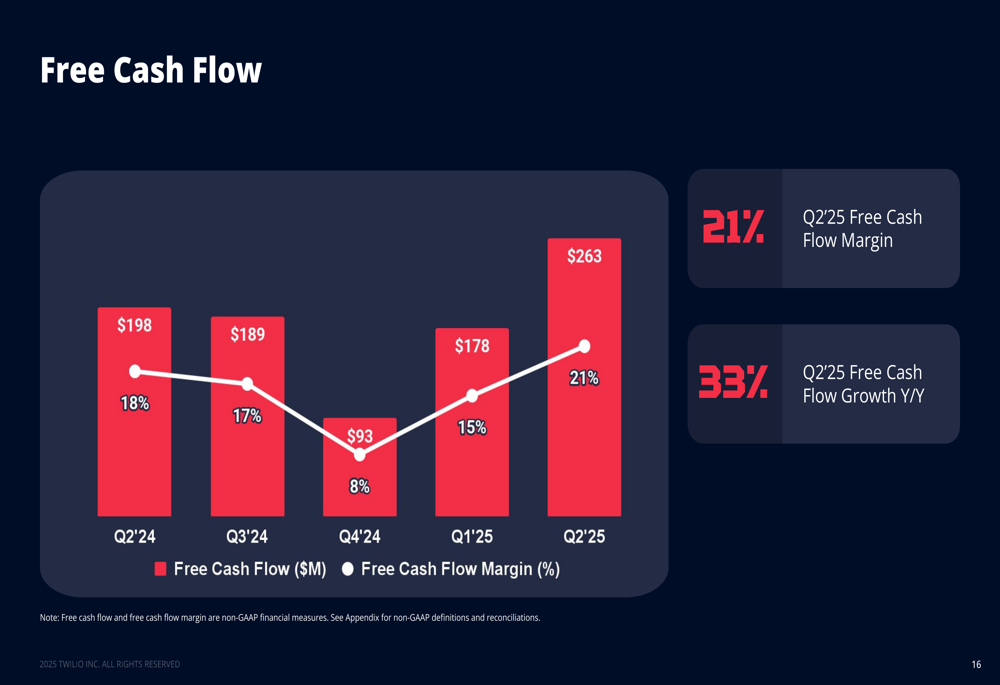

Free cash flow showed particularly strong performance, growing 33% year-over-year to $263 million with a 21% margin:

Customer Wins & Strategic Initiatives

Twilio highlighted several significant customer wins during the quarter, demonstrating its ability to attract new clients and expand relationships with existing ones. In the Communications segment, the company secured deals with companies across various industries including fintech, marketing automation, and AI.

Notable wins included a multi-year email deal with a SaaS marketing automation platform, a seven-figure competitive takeout deal for U.S. Messaging, and a verification solutions deal with Manus AI. The company also began piloting RCS (Rich Communication Services) with Postscript, a leading SMS marketing platform, indicating Twilio’s focus on next-generation messaging technologies.

In the Segment division, despite flat revenue growth, the company secured new deals with JustFab (an online fashion retailer), Centerfield (a performance marketing company), and expanded relationships with several existing customers including Metcash, a leading Australian wholesale distribution company.

Forward-Looking Statements

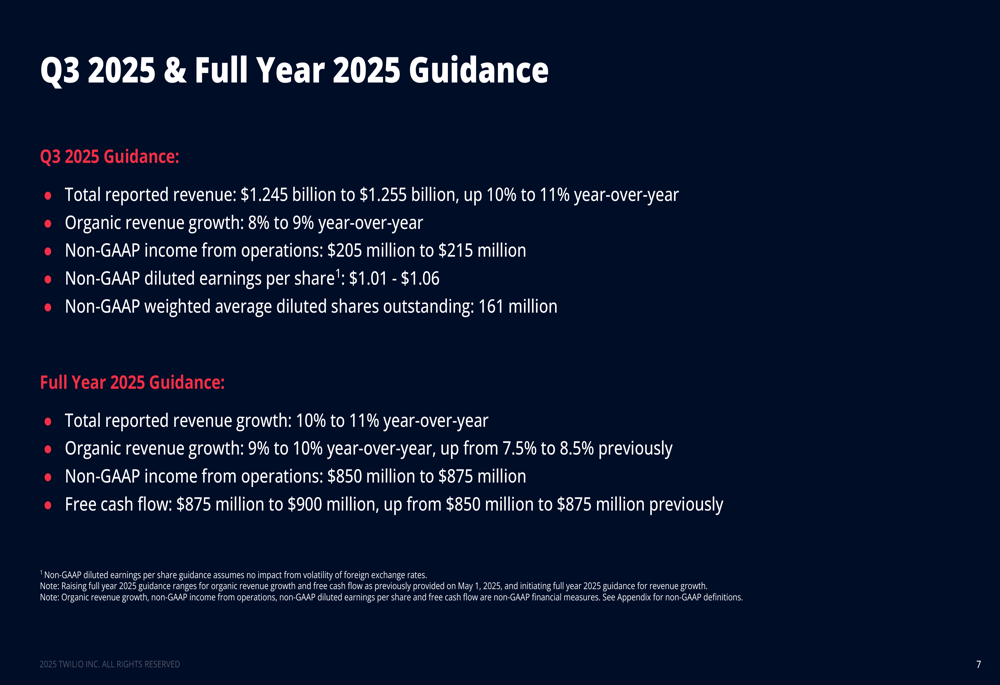

For Q3 2025, Twilio provided revenue guidance of $1.245-1.255 billion, representing 10-11% year-over-year growth, with organic revenue growth of 8-9%. The company expects Non-GAAP income from operations of $205-215 million and Non-GAAP diluted earnings per share of $1.01-1.06.

For the full year 2025, Twilio raised its organic revenue growth guidance to 9-10% (up from 7.5-8.5% previously) and expects Non-GAAP income from operations of $850-875 million. The company also increased its free cash flow guidance to $875-900 million (up from $850-875 million):

Despite the raised guidance for organic revenue growth and free cash flow, the projected deceleration in growth from Q2’s 13% to Q3’s projected 8-9% may be contributing to the negative market reaction following the earnings release.

Conclusion

Twilio’s Q2 2025 results demonstrate the company’s ability to accelerate revenue growth and improve profitability metrics, particularly in its core Communications segment. However, the stagnation in its Segment division and the projected growth deceleration for Q3 appear to be weighing on investor sentiment.

The company’s focus on operational efficiency has yielded positive results in terms of free cash flow generation and margin improvement, but the market seems to be looking for more balanced growth across all business segments. As Twilio continues to navigate the competitive cloud communications landscape, its ability to revitalize growth in the Segment division while maintaining momentum in Communications will be crucial for future performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.