Oil prices extend losses as traders downplay Russia sanction risks

Tyler Technologies, Inc. (NYSE:TYL) presented its second quarter 2025 earnings results on July 31, showcasing strong performance across key metrics with particular strength in recurring revenue streams. The company’s stock responded positively, rising 4.24% following the earnings release, as investors reacted to better-than-expected results and maintained full-year guidance.

Quarterly Performance Highlights

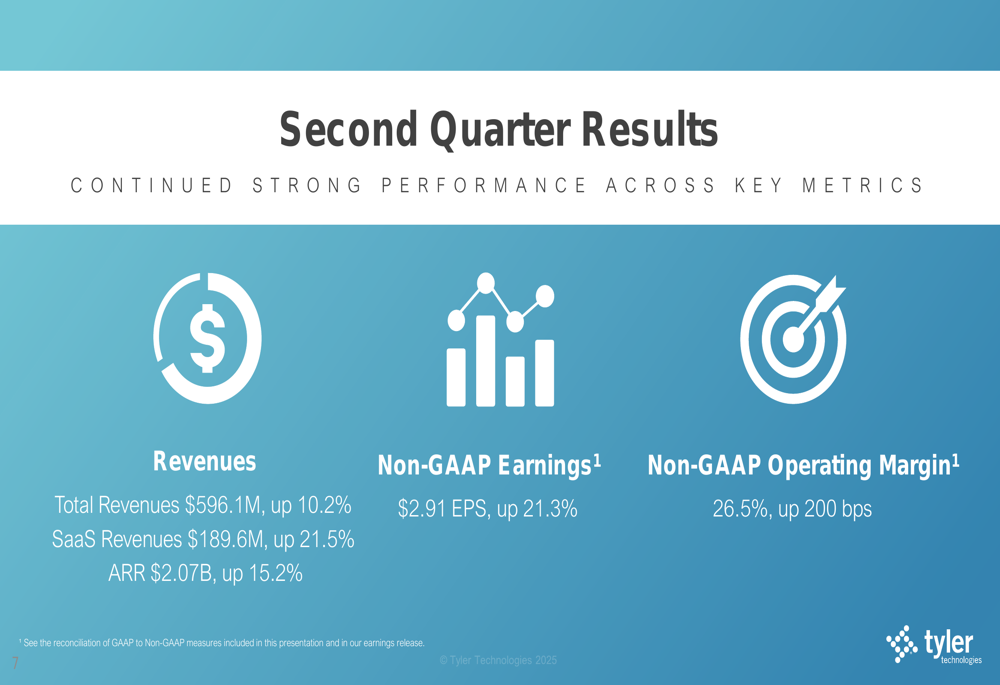

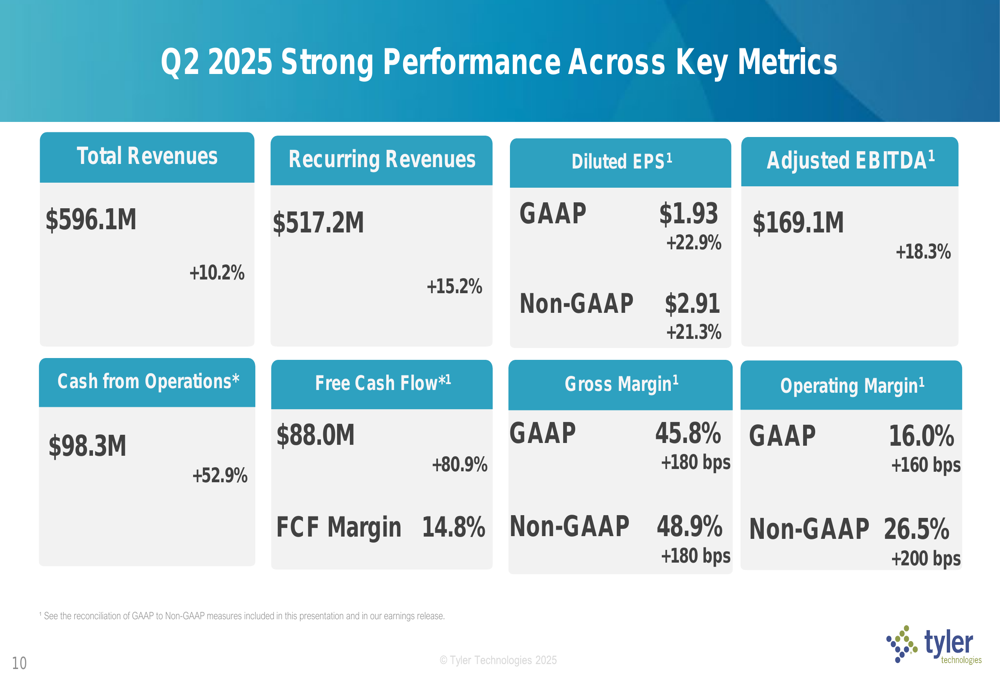

Tyler Technologies reported total revenues of $596.1 million for Q2 2025, representing a 10.2% year-over-year increase. The company significantly exceeded analyst expectations with non-GAAP earnings per share of $2.91, up 21.3% from the prior year and beating the forecast of $2.77 by 5.05%.

Profitability metrics showed substantial improvement, with non-GAAP operating margin expanding to 26.5%, an increase of 200 basis points year-over-year. The company’s cash generation was particularly impressive, with cash from operations growing 52.9% to $98.3 million and free cash flow surging 80.9% to $88 million.

As shown in the following performance summary:

The company’s annual recurring revenue (ARR) reached $2.07 billion, up 15.2% compared to the same period last year, underscoring Tyler’s successful transition toward more predictable revenue streams.

Revenue Breakdown and Growth Drivers

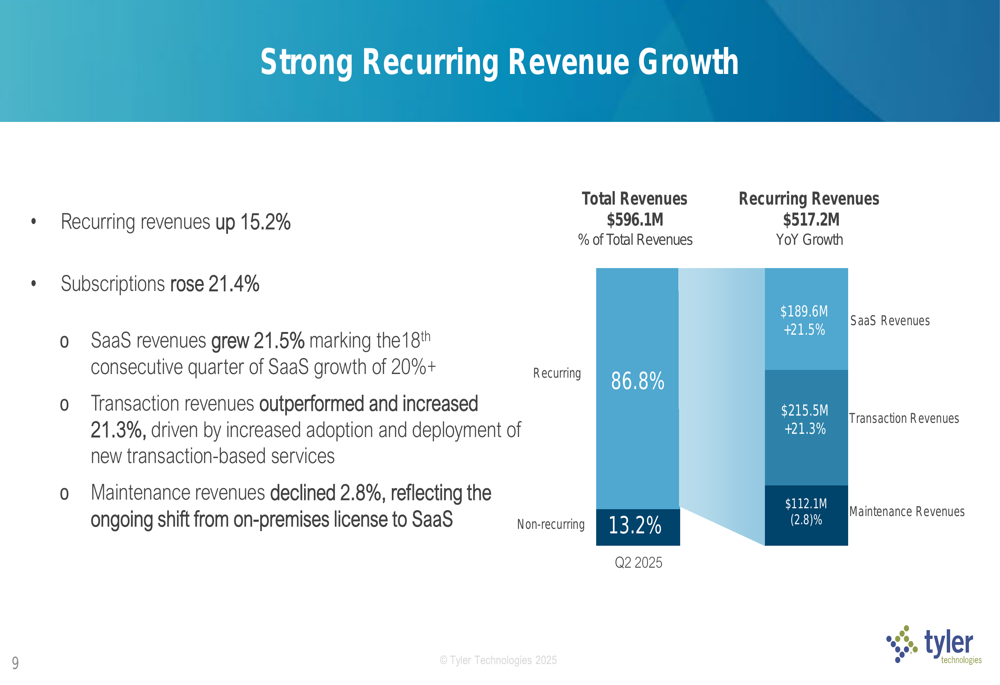

Recurring revenues, which now account for 87% of total revenues, grew 15.2% to $517.2 million. This growth was primarily driven by the continued strength in subscription-based offerings, with SaaS revenues increasing 21.5% to $189.6 million, marking the 18th consecutive quarter of SaaS growth exceeding 20%.

Transaction-based revenues were another highlight, growing 21.3% to $215.5 million and surpassing the $200 million quarterly threshold for the first time. Meanwhile, maintenance revenues declined by 2.8% to $112.1 million, reflecting the ongoing shift from on-premises solutions to cloud-based offerings.

The following chart illustrates the company’s recurring revenue growth and breakdown:

Tyler Technologies’ comprehensive performance across all key financial metrics demonstrates the company’s operational efficiency and successful execution of its strategic initiatives:

Strategic Initiatives and Notable Wins

The company reported stable public sector market conditions with healthy budgets, primarily funded by property taxes. Tyler’s strategic focus on accelerating SaaS adoption showed results, with total SaaS bookings increasing 47.7% sequentially from Q1 2025 and 8.2% year-over-year.

The quarter featured several significant client wins across various segments. Notable new SaaS deals included an $11 million total contract value (TCV) agreement with the Arizona Supreme Court for Enterprise Supervision and multiple Enterprise Public Safety contracts. The company also secured several large SaaS conversions from existing on-premises customers, including a $1.2 million annual recurring revenue (ARR) deal with the Superior Court of California, County of Santa Clara.

As shown in the following highlights summary:

Tyler Technologies continues to expand its AI-driven solutions, with new deployments of its Resident Assistant for the State of Alabama Department of Revenue and Priority-Based Budgeting implementations for the City of Dallas, TX and City of Eugene, OR.

The company’s strategic focus remains aligned with its "Tyler 2030" growth pillars, which emphasize leveraging its strong client base, expanding into new markets, completing its cloud transition, and growing its payments business:

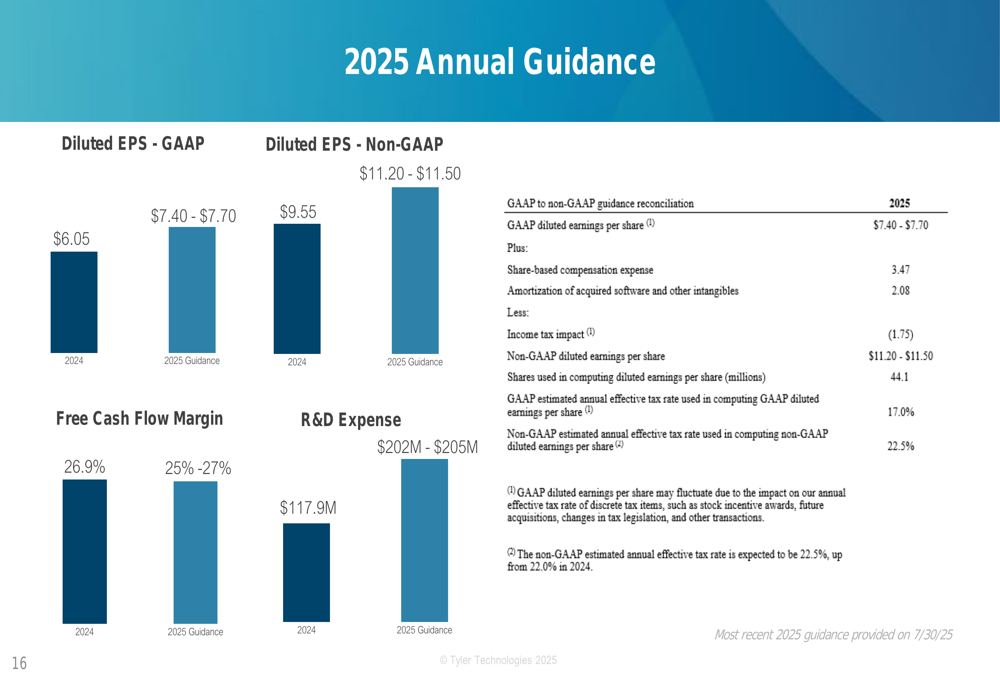

2025 Outlook and Guidance

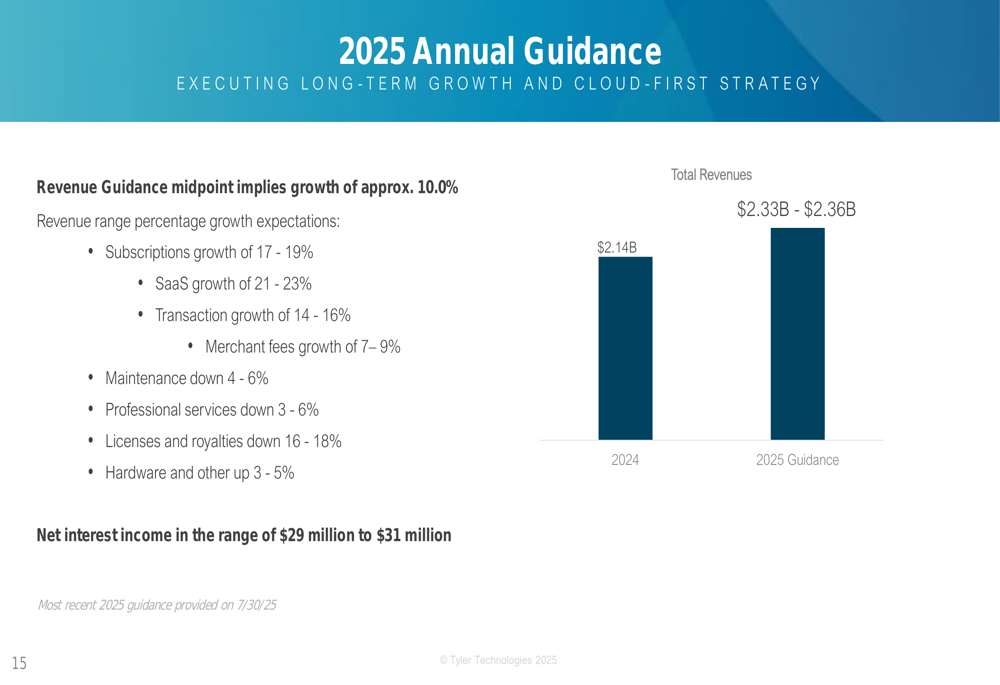

Tyler Technologies maintained its full-year 2025 revenue guidance of $2.33 billion to $2.36 billion, representing approximately 10% growth at the midpoint compared to 2024. The company expects subscription revenues to grow 17-19%, with SaaS revenues increasing 21-23% and transaction revenues growing 14-16%.

The following chart details the company’s revenue guidance for 2025:

For earnings, Tyler Technologies expects GAAP diluted EPS of $7.40-$7.70 and non-GAAP diluted EPS of $11.20-$11.50, compared to $6.05 and $9.55 respectively in 2024. The company anticipates a free cash flow margin between 25-27%, consistent with its 2024 performance of 26.9%.

The company also plans to significantly increase its R&D investments, with expected expenses of $202-205 million in 2025, up from $117.9 million in 2024, reflecting its commitment to innovation and product development:

Tyler Technologies’ Q2 2025 results demonstrate the company’s continued success in executing its cloud-first strategy while maintaining its leadership position in the public sector software market. With recurring revenues now comprising 87% of total revenues and strong growth in high-margin SaaS and transaction-based offerings, the company appears well-positioned to deliver on its full-year guidance and long-term strategic objectives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.