Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Upwork Inc. (NASDAQ:UPWK) presented its Q2 2025 investor slides on August 6, highlighting record profitability metrics despite modest revenue growth. The freelance marketplace platform emphasized its strategic focus on artificial intelligence capabilities, enterprise expansion through acquisitions, and monetization improvements as key growth drivers.

Following the earnings release, Upwork’s stock saw a modest 0.59% increase in the regular trading session, closing at $11.95. However, the company’s shares surged 13.14% in premarket trading on August 7, reaching $13.52, as investors responded positively to the stronger-than-expected financial results and strategic initiatives.

Quarterly Performance Highlights

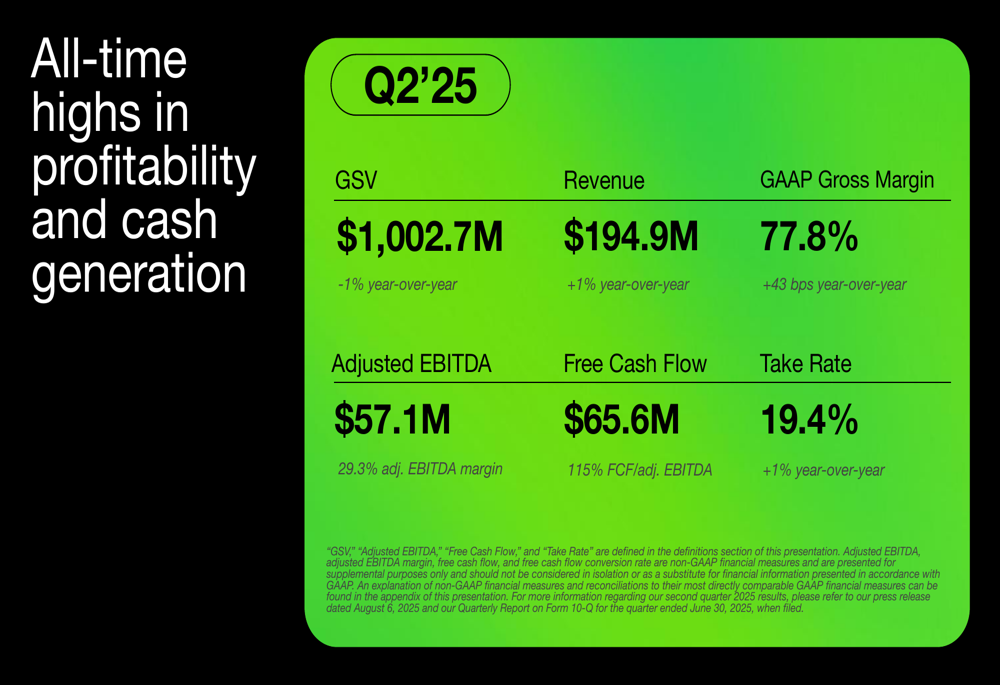

Upwork reported Q2 2025 revenue of $194.9 million, representing a 1% year-over-year increase, while achieving record profitability metrics. The company’s gross service value (GSV) reached $1.0 billion, showing a slight 1% year-over-year decline, but take rate improved to 19.4%, up 1% from the previous year.

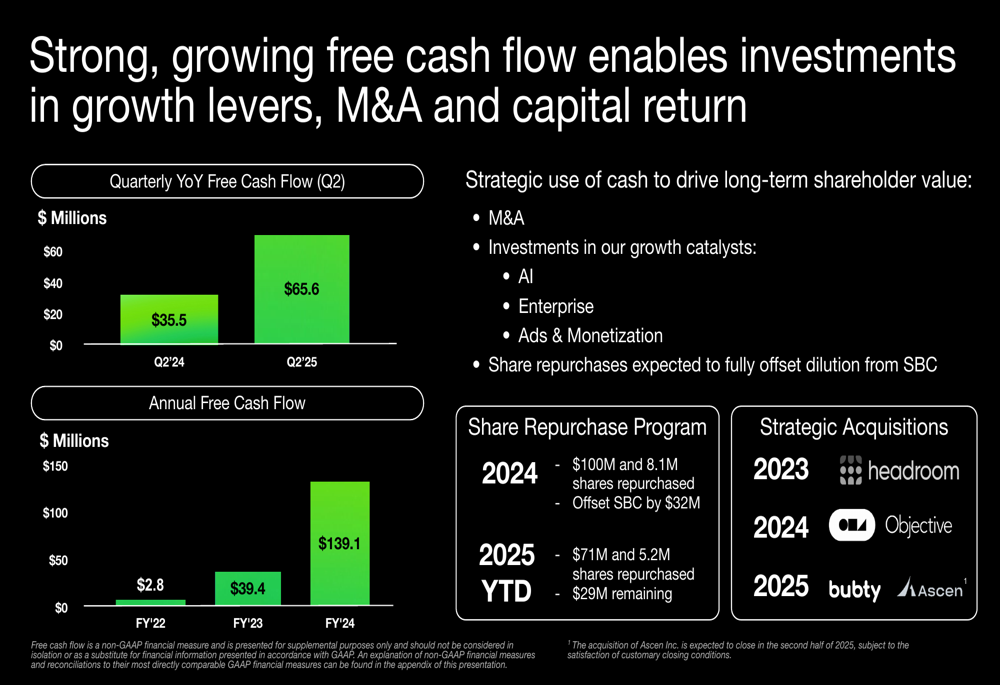

The company highlighted its exceptional profitability metrics, with adjusted EBITDA reaching $57.1 million, a 40% year-over-year increase, and representing a record 29.3% margin. Free cash flow generation was strong at $65.6 million.

As shown in the following comprehensive financial summary:

Upwork’s gross margin reached a record 77.8% in Q2, improving 43 basis points year-over-year. The company reported net income of $32.7 million, representing a 47% increase from the same period last year, though there appears to be a discrepancy between the reported EPS of $0.35 in earnings coverage and the $0.24 diluted EPS shown in the presentation.

AI Growth Strategy

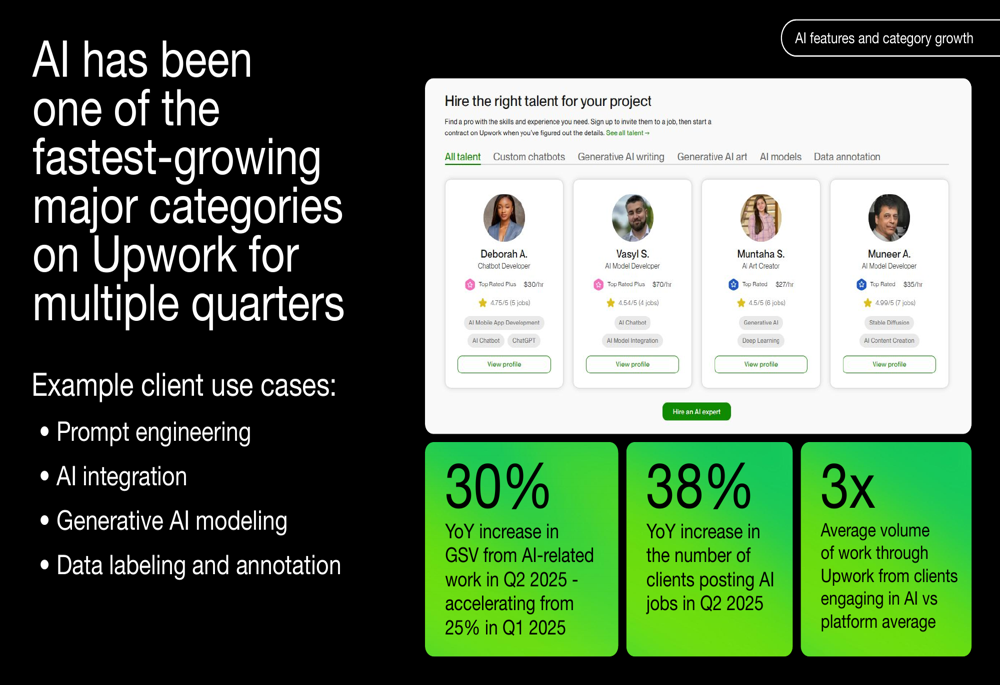

A central theme of Upwork’s presentation was the accelerating growth in AI-related work on its platform. The company reported that GSV from AI-related work grew 30% year-over-year in Q2 2025, accelerating from 25% growth in Q1, while the number of clients posting AI jobs increased 38% year-over-year.

Upwork emphasized that clients engaging in AI work generate approximately three times the average volume compared to the platform average, highlighting the strategic importance of this category.

The following slide illustrates the growth of AI as a fast-growing category on the platform:

The company also highlighted its own AI capabilities, including the expansion of Uma (Upwork’s Mindful AI) as an autonomous work agent. Upwork positioned this development as transformative for its platform, allowing it to better connect businesses with its pool of approximately 250,000 AI experts globally.

Enterprise Expansion

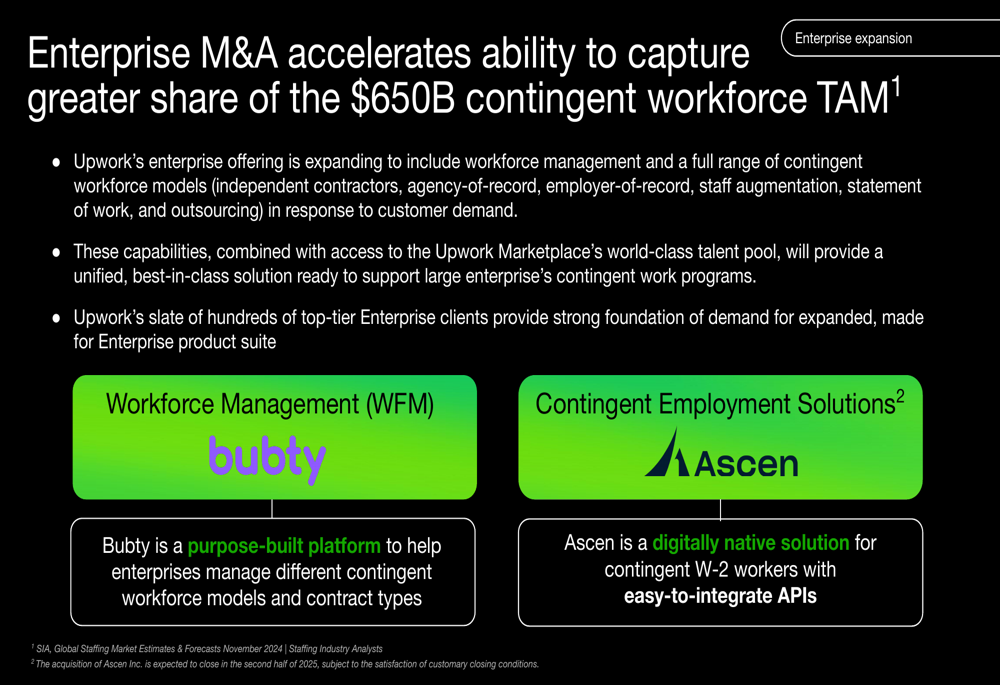

Upwork detailed its strategy to capture a larger share of the $650 billion contingent workforce market through enterprise-focused acquisitions and product development. The company has made strategic acquisitions including Bubty and Ascen to enhance its enterprise workforce management capabilities.

These acquisitions are designed to create what Upwork describes as a "singular, differentiated solution" for enterprise clients seeking contingent workforce solutions. The company highlighted that its enterprise offering is expanding beyond talent sourcing to include comprehensive workforce management.

As illustrated in the following slide, Upwork is positioning itself to accelerate market share capture in the enterprise segment:

The company’s enterprise strategy aims to provide a unified solution for all contingent work needs, with capabilities that are country and contract agnostic, addressing a key pain point for multinational corporations.

Strategic Initiatives

Upwork identified three primary growth catalysts for 2026: AI features and category growth, enterprise expansion, and enhanced monetization through ads and value-added services.

The company’s monetization efforts showed promising results, with ads and monetization revenues growing 17% year-over-year in Q2. Freelancer Plus subscription revenue increased 13% year-over-year, while Connects revenue grew 19%. Business Plus, a newer offering, saw its GSV increase 190% quarter-over-quarter.

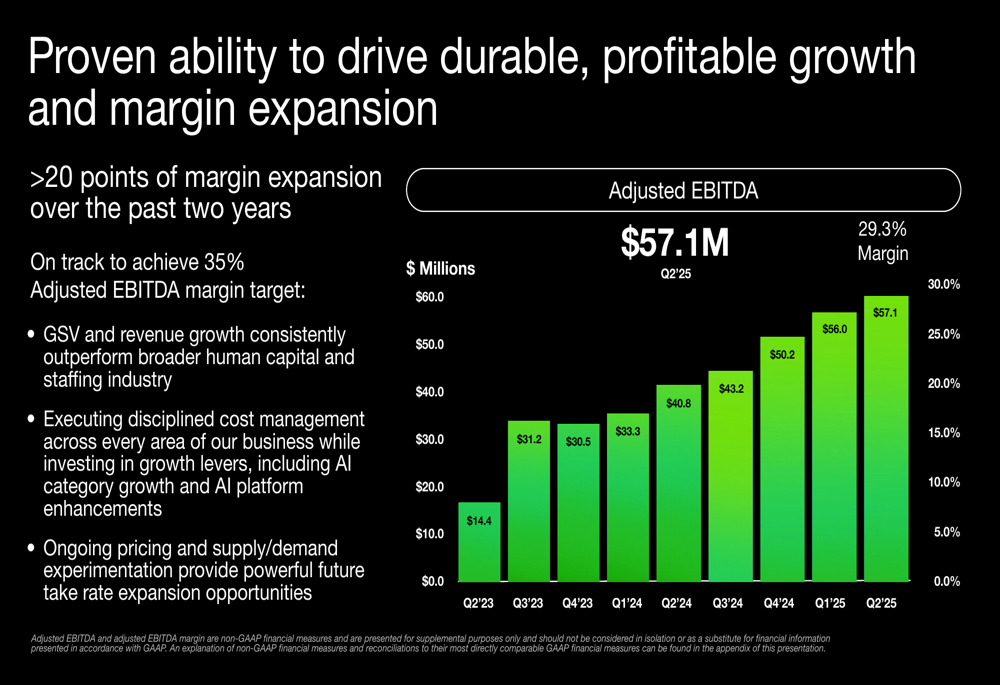

The following slide demonstrates Upwork’s proven ability to drive profitable growth, showing the substantial margin expansion achieved over the past two years:

The company’s strong free cash flow generation has enabled strategic acquisitions while maintaining a robust balance sheet with approximately $635 million in cash, cash equivalents, and marketable securities at the end of Q2 2025.

Forward-Looking Statements

Upwork raised its full-year 2025 revenue guidance to a range of $765-$775 million, reflecting confidence in its growth trajectory. The company also projects adjusted EBITDA for the year to be between $206 million and $214 million, with a long-term target of achieving a 35% adjusted EBITDA margin.

Management expressed confidence in the company’s strategic direction, with CEO Hayden Brown noting that "Our platform is more powerful. Our customers are more engaged." CFO Erica Gesser added, "We are building the foundation for accelerated multi-year growth."

Market Reaction

The market responded positively to Upwork’s presentation and Q2 results. After closing at $11.95 on August 6 (up 0.59% from the previous session), the stock surged 13.14% in premarket trading on August 7, reaching $13.52.

This significant premarket movement suggests investors are encouraged by Upwork’s record profitability metrics, strategic acquisitions, and growth in high-value categories like AI. Analyst targets for the stock range from $15 to $25, with five analysts recently revising their earnings expectations upward.

Despite these positive developments, Upwork faces ongoing challenges including macroeconomic uncertainties that could impact client spending, potential integration challenges with recent acquisitions, competitive pressures in the AI and freelancing markets, and possible regulatory changes affecting the gig economy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.