United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

Verizon Communications Inc (NYSE:VZ) released its first quarter 2025 earnings presentation on April 22, showing record quarterly adjusted EBITDA and solid wireless service revenue growth. Despite these positive results, Verizon’s stock was down 3.19% in premarket trading to $41.56, suggesting investors may have had higher expectations or are responding to other market factors.

The telecommunications giant reported a 2.7% year-over-year increase in wireless service revenue and a significant 34.3% jump in free cash flow, continuing the momentum from its strong fourth quarter 2024 performance when it exceeded analyst expectations.

Quarterly Performance Highlights

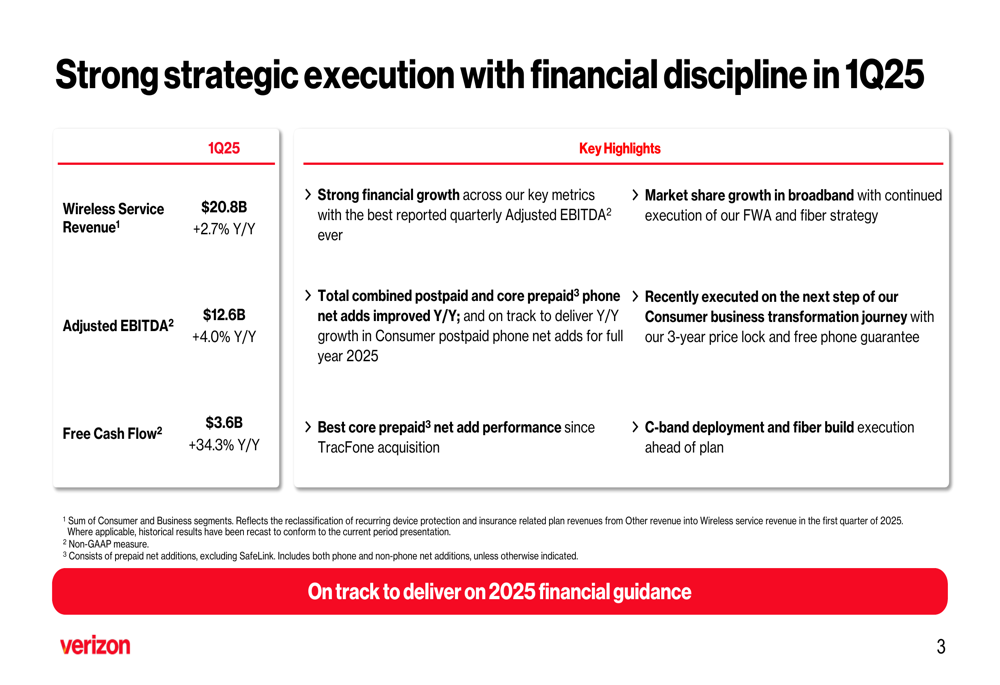

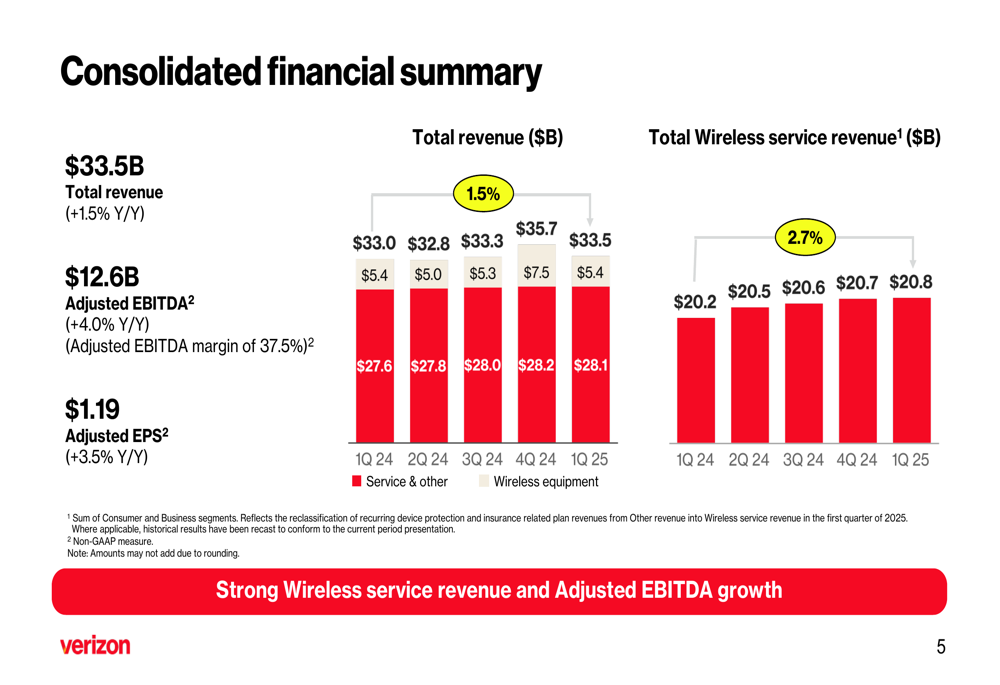

Verizon achieved its highest-ever quarterly adjusted EBITDA of $12.6 billion, representing a 4.0% increase compared to the same period last year. This record performance underscores the company’s focus on operational efficiency and strategic execution.

Total (EPA:TTEF) revenue reached $33.5 billion, up 1.5% year-over-year, while adjusted earnings per share rose to $1.19, a 3.5% improvement from Q1 2024. The company’s free cash flow saw a substantial increase of 34.3% to $3.6 billion, demonstrating strong underlying cash generation capabilities.

As shown in the following financial and strategic highlights from Verizon’s presentation:

Operational Metrics

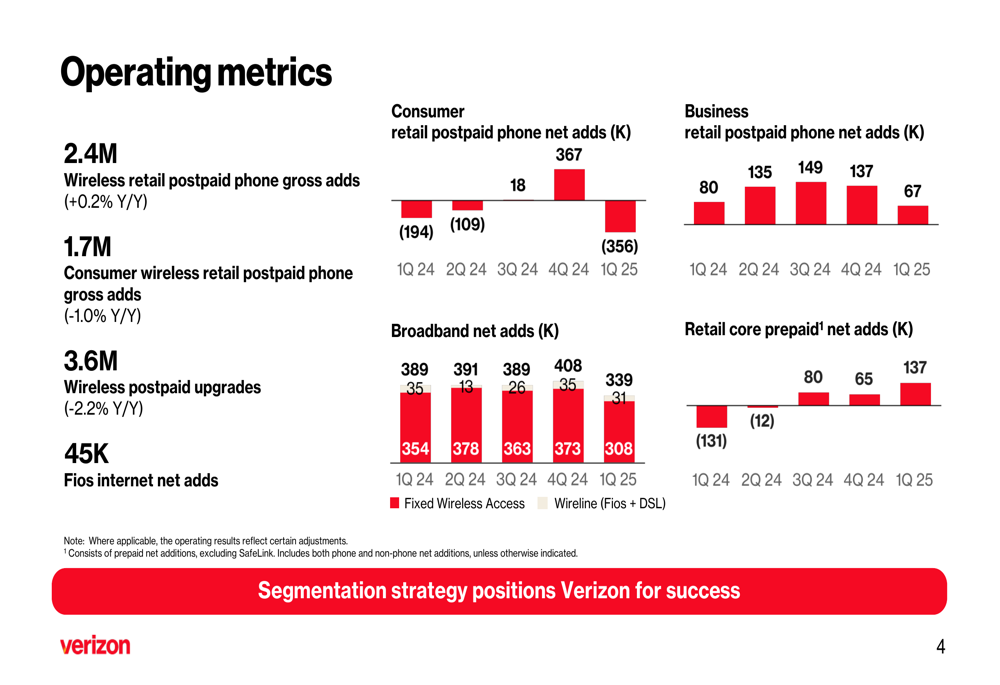

Verizon reported significant improvements in its customer metrics, particularly in the consumer segment. Consumer retail postpaid phone net adds reached 356,000 in Q1 2025, compared to 194,000 in the same period last year, reflecting strengthened customer acquisition and retention strategies.

The business segment contributed 67,000 retail postpaid phone net adds, slightly down from 80,000 in Q1 2024 but still representing solid performance. Overall wireless retail postpaid phone gross adds increased marginally by 0.2% year-over-year to 2.4 million.

One of the most notable improvements came in the prepaid segment, where Verizon achieved 137,000 retail core prepaid net adds, a dramatic turnaround from the 131,000 net losses in Q1 2024. The company described this as its "best core prepaid net add performance since TracFone acquisition."

The following operating metrics slide illustrates these trends:

Broadband performance remained strong with 339,000 net adds in Q1 2025, though slightly below the 389,000 reported in Q1 2024. This includes continued growth in both Fios internet and fixed wireless access services, with Fios internet contributing 45,000 net adds for the quarter.

Detailed Financial Analysis

Verizon’s consolidated financial results show consistent growth across key metrics. Wireless service revenue, a critical indicator of the company’s core business health, increased to $20.8 billion, up 2.7% year-over-year. This growth has been steady over the past five quarters, as illustrated in the company’s financial summary:

The adjusted EBITDA margin stood at 37.5%, reflecting the company’s ability to maintain profitability while investing in network expansion and customer acquisition. This margin strength, combined with the record EBITDA figure of $12.6 billion, indicates effective cost management alongside revenue growth.

Financial Position

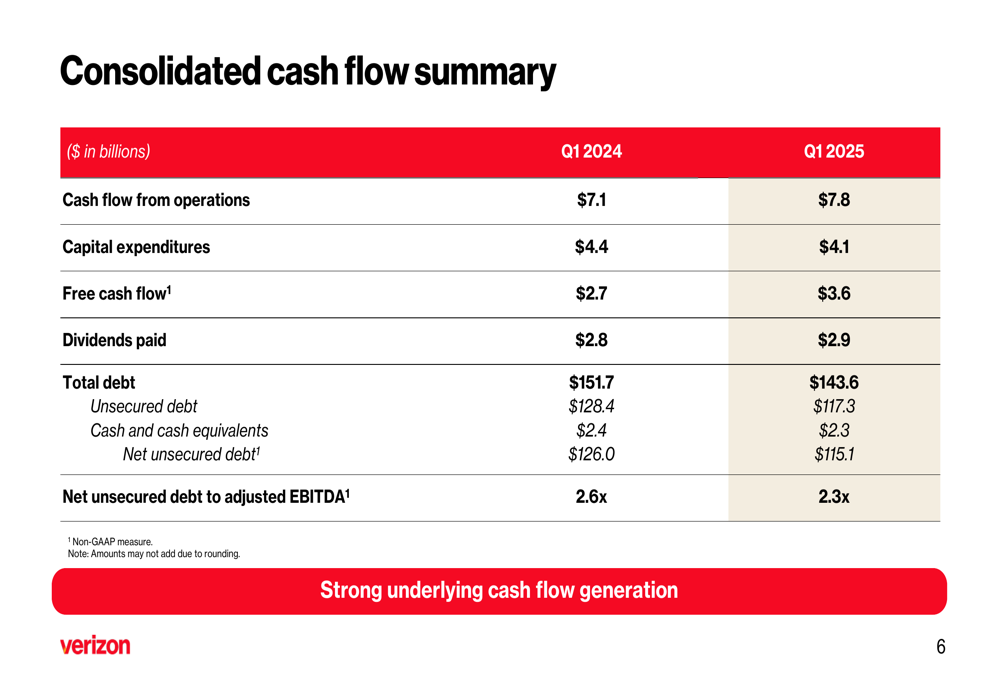

Verizon continues to strengthen its balance sheet, reducing total debt to $143.6 billion in Q1 2025 from $151.7 billion a year earlier. This $8.1 billion debt reduction has improved the company’s net unsecured debt to adjusted EBITDA ratio to 2.3x, down from 2.6x in Q1 2024.

Cash flow from operations increased to $7.8 billion in Q1 2025, up from $7.1 billion in Q1 2024, while capital expenditures decreased slightly to $4.1 billion from $4.4 billion. The combination of higher operating cash flow and lower capital spending contributed to the significant improvement in free cash flow.

The consolidated cash flow summary provides a clear picture of these improvements:

Dividend payments increased slightly to $2.9 billion in Q1 2025 from $2.8 billion in Q1 2024, reflecting Verizon’s commitment to returning value to shareholders while managing its debt reduction efforts.

Strategic Initiatives

Verizon highlighted several strategic achievements in its Q1 2025 presentation, including market share growth in broadband and progress in its C-band deployment and fiber build initiatives. The company emphasized its strong financial growth alongside operational improvements across multiple segments.

The presentation noted that Verizon is on track to deliver on its 2025 financial guidance, suggesting management confidence in the company’s strategic direction and execution capabilities. This follows the positive momentum established in Q4 2024, when the company provided optimistic guidance for 2025 with projected capital expenditure between $17.5 billion and $18.5 billion.

Forward Outlook

While specific forward guidance details were limited in the presentation materials, Verizon indicated it is "on track to deliver on 2025 financial guidance." This suggests the company remains confident in its ability to maintain service revenue growth and continue expanding EBITDA despite competitive pressures in the telecommunications industry.

The company’s focus on broadband expansion, including both fiber and fixed wireless access services, positions it to capitalize on growing demand for high-speed connectivity. Additionally, the improvement in prepaid performance indicates successful execution in a segment that had previously been challenging.

Verizon’s stock performance, however, suggests investors may be looking for more aggressive growth or clearer indications of how the company plans to differentiate itself in an increasingly competitive market. The premarket decline of 3.19% contrasts with the positive market reaction to Q4 2024 results, when the stock rose by 0.56% following the earnings announcement.

As Verizon continues to execute its strategy throughout 2025, investors will likely focus on whether the company can maintain its momentum in wireless service revenue growth while further improving its debt metrics and free cash flow generation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.