US stock futures flat after Wall St drops on Trump tariffs, soft jobs data

Verra Mobility Corp (NASDAQ:VRRM) presented its first quarter 2025 earnings results on May 7, highlighting solid revenue growth and exceptional free cash flow performance despite lingering travel demand uncertainties. The mobility technology company maintained its full-year guidance while announcing strategic contract wins that could drive future growth.

Quarterly Performance Highlights

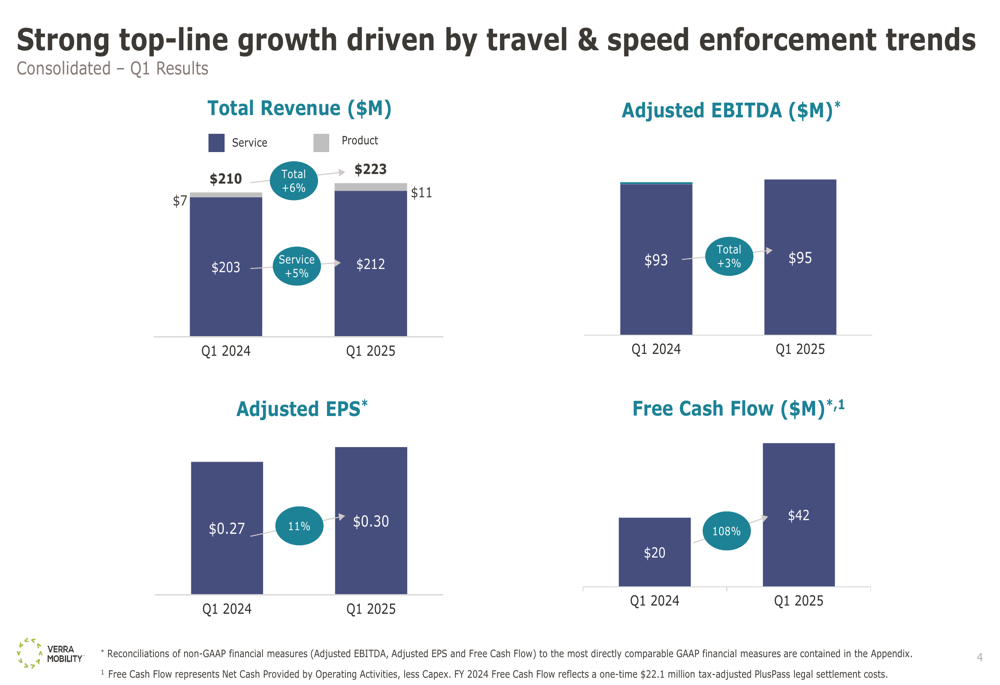

Verra Mobility reported total revenue of $223 million for Q1 2025, representing a 6% year-over-year increase from $210 million in Q1 2024. The company’s adjusted EBITDA grew 3% to $95 million, while adjusted earnings per share increased 11% to $0.30.

The most impressive metric was free cash flow, which more than doubled to $42 million, representing a 108% year-over-year increase from $20 million in the same period last year.

As shown in the following chart of quarterly financial performance:

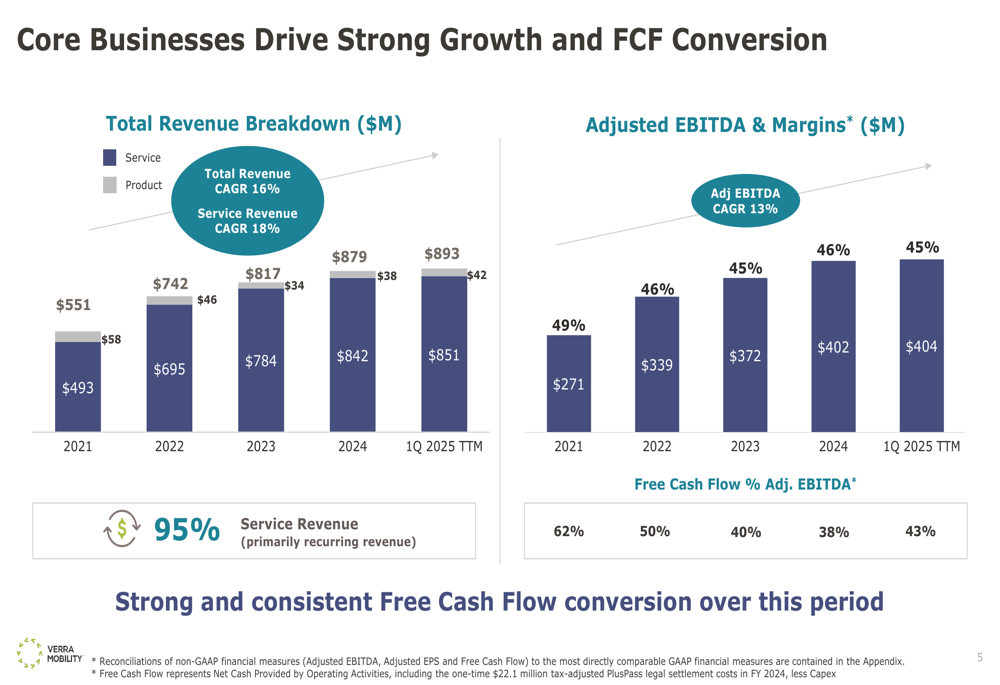

"Our business fundamentals remain strong and intact," said David Roberts, CEO of Verra Mobility, during the earnings presentation. The company highlighted that service revenue, which represents approximately 95% of total revenue, continues to provide a stable, recurring revenue base.

Segment Analysis

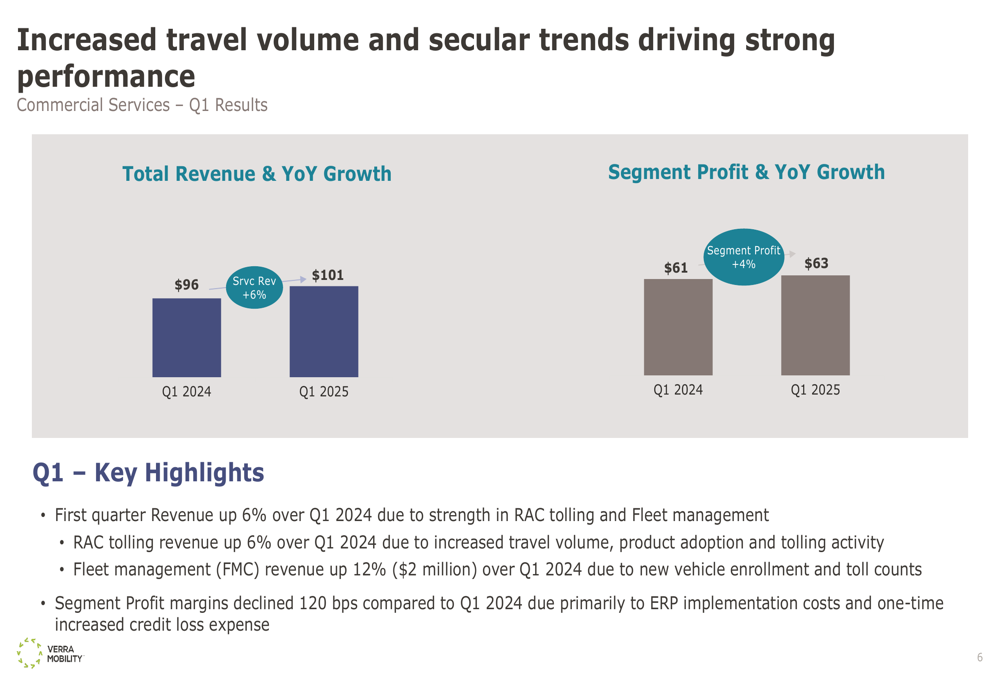

Verra Mobility’s performance was driven by growth in two of its three business segments. The Commercial Services segment, which primarily includes rental car tolling and fleet management services, posted revenue of $101 million, up 6% year-over-year, with segment profit increasing 4% to $63 million.

The company noted that rental car tolling revenue increased 6% due to increased travel volume, product adoption, and tolling activity. Meanwhile, fleet management revenue grew an impressive 12% ($2 million) due to new vehicle enrollment and increased toll counts.

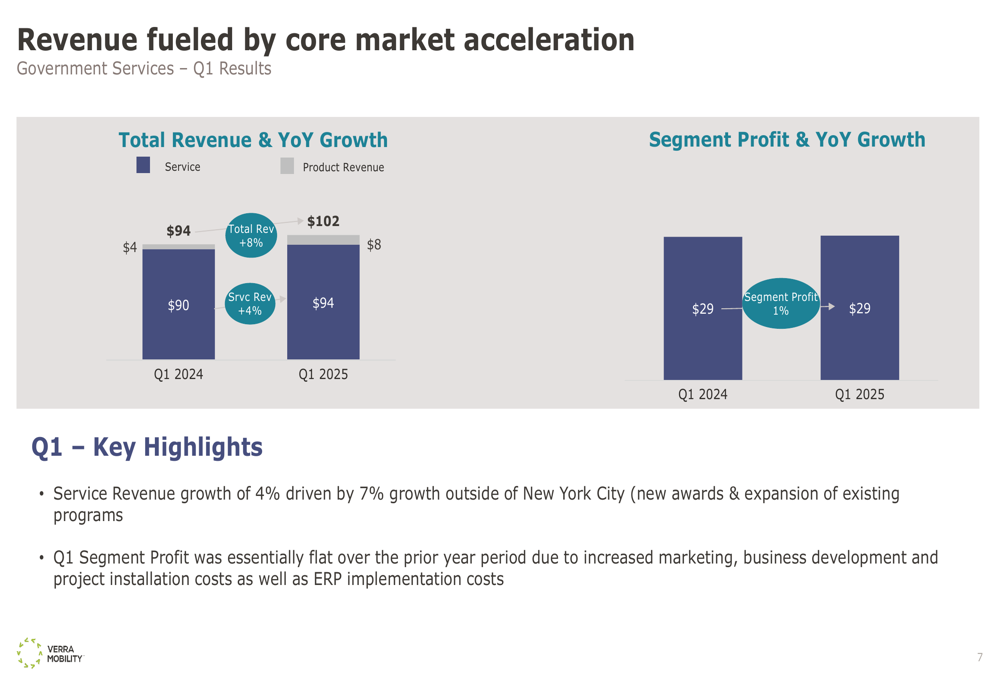

The Government Solutions segment, which provides traffic safety systems to municipalities, saw total revenue increase 8% to $102 million, with service revenue specifically growing 4%. Segment profit remained flat at $29 million due to increased marketing, business development, and project installation costs, as well as ERP implementation expenses.

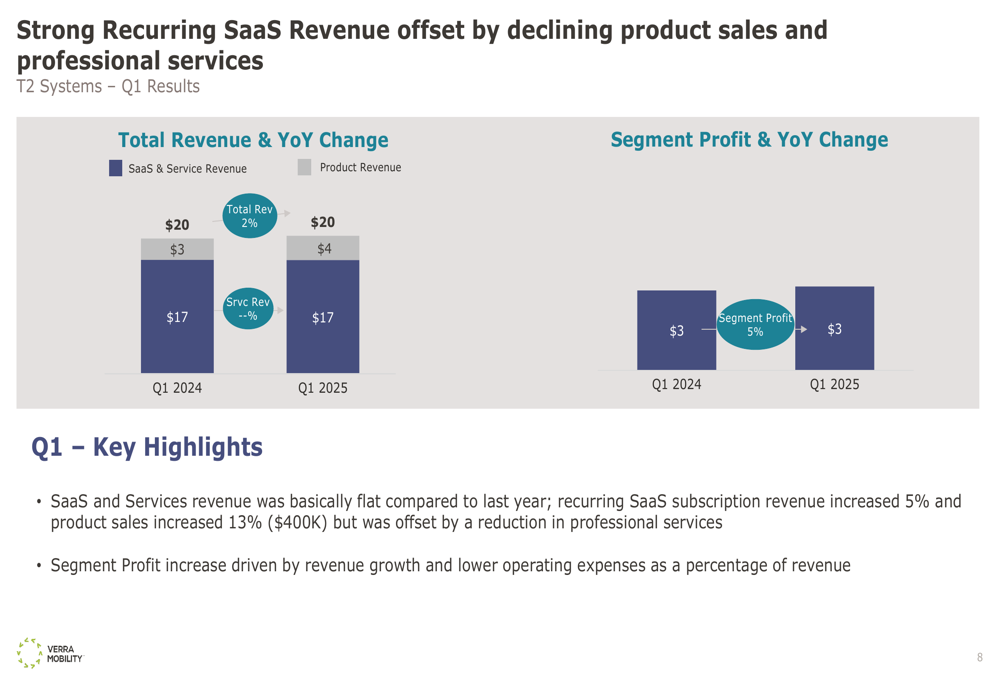

The Parking Solutions segment (T2 Systems) reported flat revenue of $20 million compared to Q1 2024. While recurring SaaS subscription revenue increased 5% and product sales grew 13%, these gains were offset by a reduction in professional services. Segment profit increased 5% to $3 million, driven by revenue growth and lower operating expenses as a percentage of revenue.

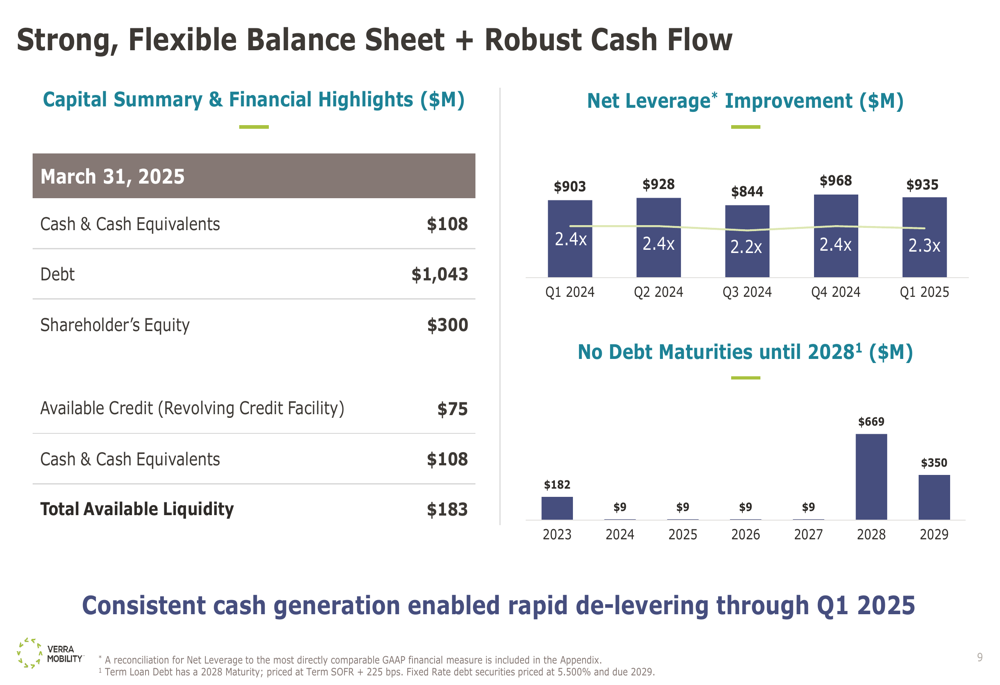

Balance Sheet and Cash Flow

Verra Mobility maintained a strong balance sheet with $108 million in cash and cash equivalents as of March 31, 2025. The company’s total debt stood at $1.043 billion, resulting in net debt of $935 million and a net leverage ratio of 2.3x, an improvement from 2.4x in Q4 2024.

The company’s consistent cash generation has enabled rapid deleveraging, with no debt maturities until 2028. Total (EPA:TTEF) available liquidity was $183 million, including $75 million available under its revolving credit facility.

As illustrated in the following chart of net leverage improvement:

Free cash flow conversion improved to 43% of adjusted EBITDA on a trailing twelve-month basis, up from 38% in 2024. This improvement reflects the company’s focus on operational efficiency and cash generation.

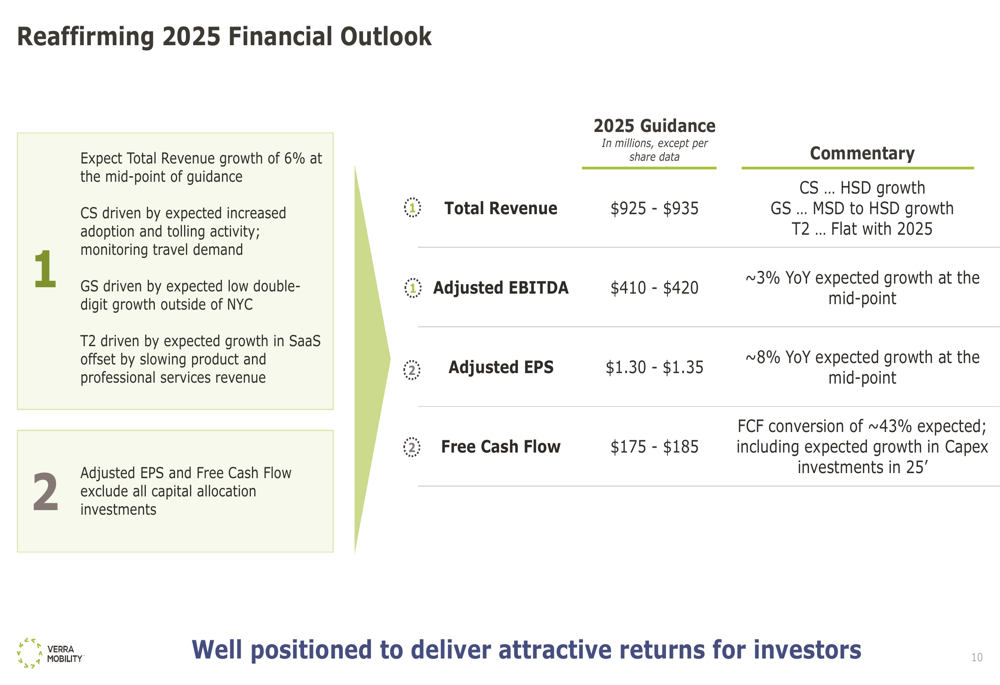

2025 Outlook and Guidance

Verra Mobility reaffirmed its full-year 2025 financial guidance, projecting:

- Total revenue of $925-935 million (6% growth at midpoint)

- Adjusted EBITDA of $410-420 million (3% growth at midpoint)

- Adjusted EPS of $1.30-1.35 (8% growth at midpoint)

- Free cash flow of $175-185 million (43% conversion of adjusted EBITDA)

The company noted that while it is maintaining its guidance, there is some risk to the lower end due to uncertain travel demand. By segment, Commercial Services is expected to deliver high single-digit growth, Government Solutions is projected to achieve mid-to-high single-digit growth, while Parking Solutions is expected to remain flat compared to 2024.

Additional guidance assumptions include a fully diluted share count of approximately 163 million shares, an effective tax rate of 28.5-29.5%, and capital expenditures of approximately $90 million, which includes incremental investments for revenue-generating cameras in Government Solutions and ERP implementation.

Strategic Initiatives and Future Growth

Verra Mobility highlighted several strategic wins that could drive future growth. Most notably, the company was selected by the New York City Department of Transportation for automated enforcement safety programs, with an expected five-year contract. This represents a significant opportunity in one of the company’s key markets.

The company also reported solid Q1 bookings in Government Solutions, with potential for up to $6 million of incremental full run-rate annual recurring revenue. These new contracts and expansions of existing programs contributed to the 7% service revenue growth outside of New York City.

The long-term growth trajectory remains strong, with total revenue CAGR of 16% and service revenue CAGR of 18% from 2021 to Q1 2025 (trailing twelve months). The company’s adjusted EBITDA has grown at a 13% CAGR over the same period.

Despite these positive developments, Verra Mobility’s stock has faced pressure in recent months. After trading at $25.6 following Q4 2024 earnings, the stock closed at $22.25 on May 7, 2025, though it gained 0.41% in after-hours trading following the earnings presentation.

The company’s focus on high-margin recurring revenue, strategic contract wins, and strong cash flow generation positions it well for continued growth, even as it navigates potential uncertainties in travel demand that could impact its Commercial Services segment in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.