Goldman Sachs expects Nvidia ’beat and raise,’ lifts price target to $240

Introduction & Market Context

Vestum AB (STO:VESTUM) presented its Q2 2025 interim report on July 14, 2025, highlighting a second consecutive quarter of organic growth despite an overall sales decline. The company, which closed at 8.68 SEK on October 14, down 0.81% for the day, continues to navigate a mixed market environment with varying performance across its business segments.

The industrial group’s presentation revealed a strategic focus on the UK water infrastructure sector, which aligns with the company’s expectations for significant growth opportunities under the AMP8 investment plan, though short-term market caution remains.

Quarterly Performance Highlights

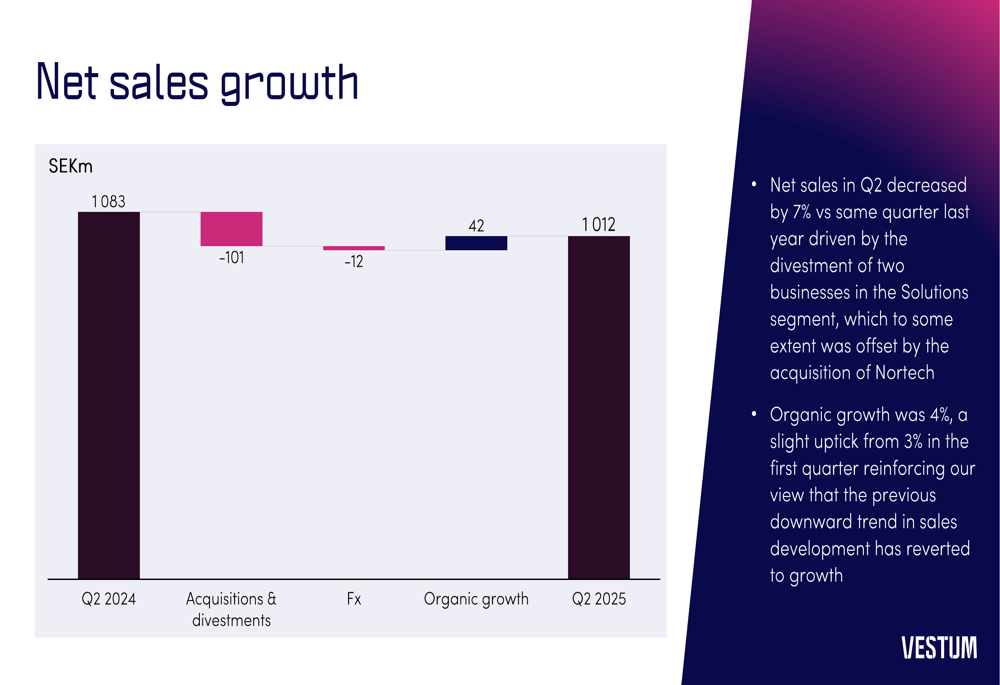

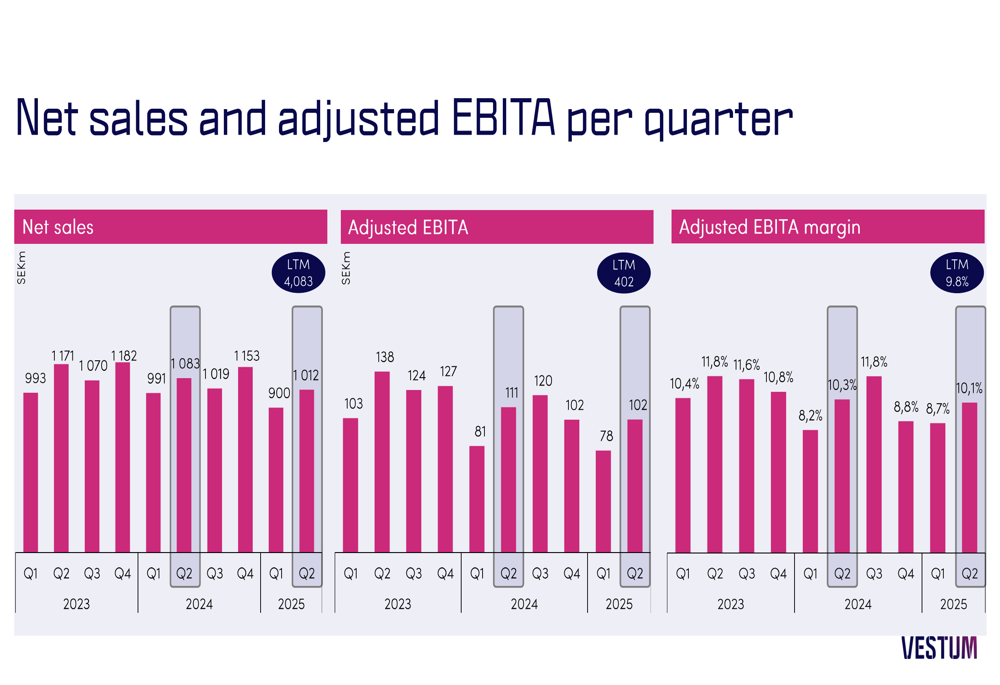

Vestum reported net sales of 1,012 SEKm for Q2 2025, representing a 7% decrease compared to the same period last year. However, the company achieved 4% organic growth, improving from 3% in Q1, signaling a potential reversal of previous downward trends.

As shown in the following quarterly performance overview, Vestum maintained stable profitability with an adjusted EBITA of 102 SEKm and a margin of 10.1%:

The decline in net sales was primarily attributed to divestments in the Solutions segment, partially offset by the acquisition of Nortech. Currency effects also had a negative impact of 12 SEKm on sales figures.

The following waterfall chart clearly illustrates the factors contributing to the sales change:

Segment Analysis

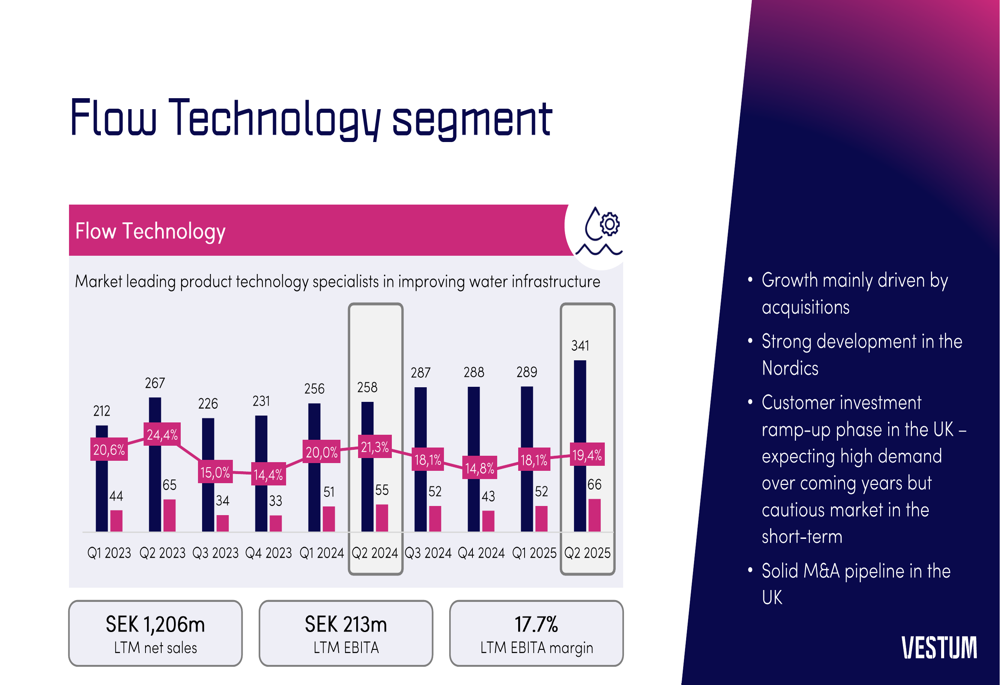

Vestum’s three business segments showed divergent performance, with Flow Technology emerging as the standout performer.

The Flow Technology segment demonstrated robust growth with Q2 2025 sales reaching 341 SEKm and an impressive adjusted EBITA margin of 19.4%. This segment has shown consistent strength, particularly in Nordic markets, while positioning for future growth in the UK:

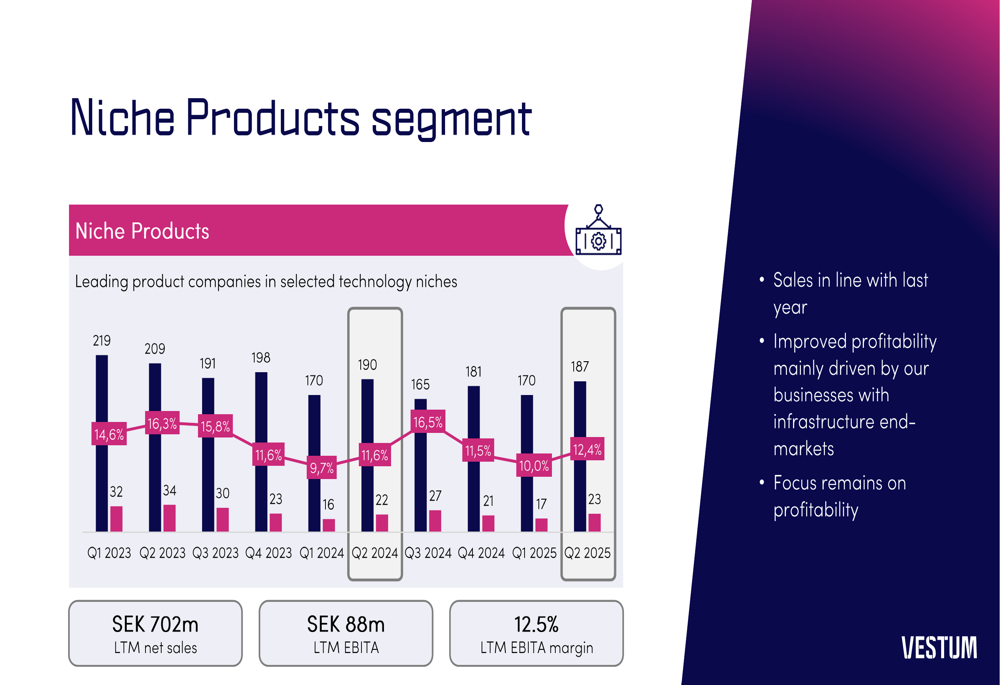

The Niche Products segment maintained stable performance with Q2 2025 sales of 187 SEKm, matching the previous year, while improving its adjusted EBITA margin to 12.4%. This improvement was primarily driven by businesses serving infrastructure end-markets:

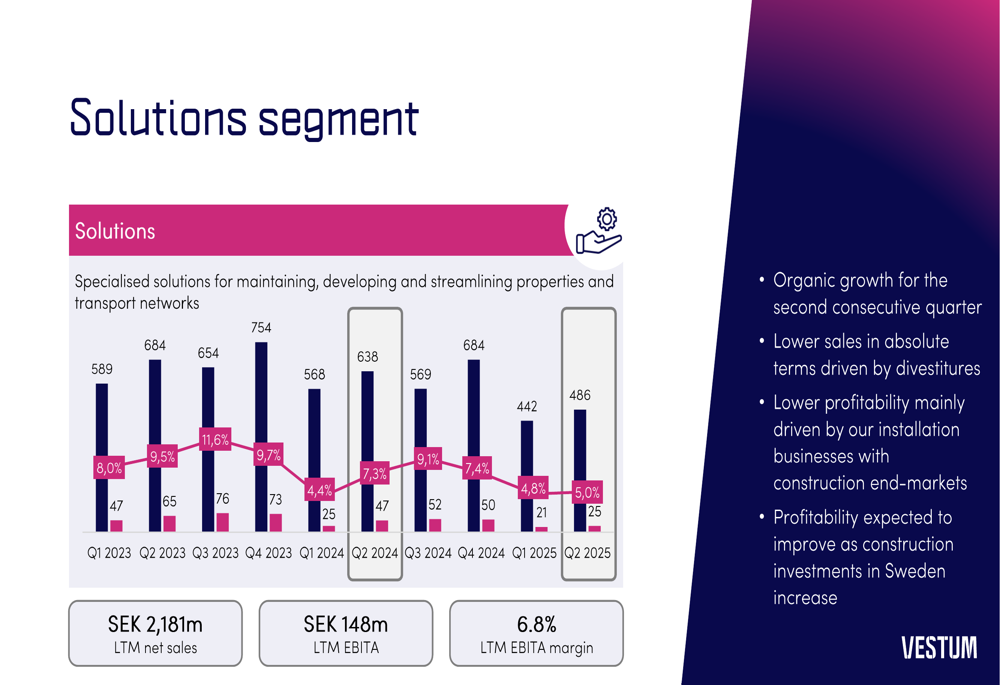

In contrast, the Solutions segment continued to face challenges, particularly in installation businesses with construction end-markets. Q2 2025 sales were 486 SEKm with an adjusted EBITA margin of just 5.0%, though the segment did achieve organic growth for the second consecutive quarter:

The quarterly trend data for the entire company shows how these segment performances have contributed to overall results:

Financial Position and Cash Flow

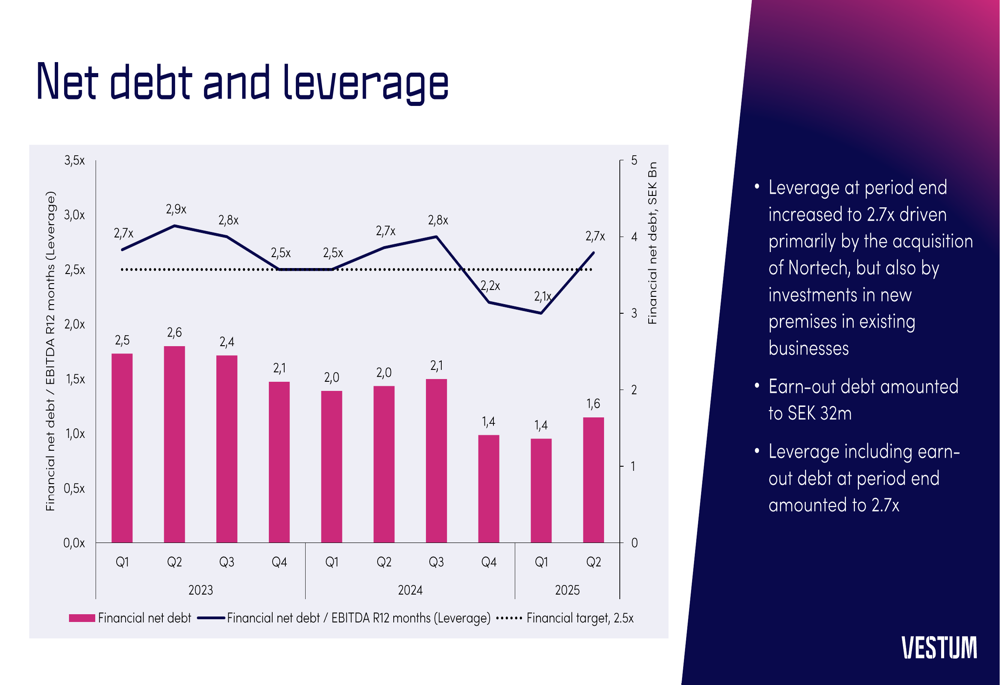

Vestum’s financial position saw some changes during the quarter, with leverage increasing to 2.65x, primarily driven by the acquisition of Nortech and investments in new facilities for existing businesses.

The company’s net debt and leverage trends are illustrated in the following chart:

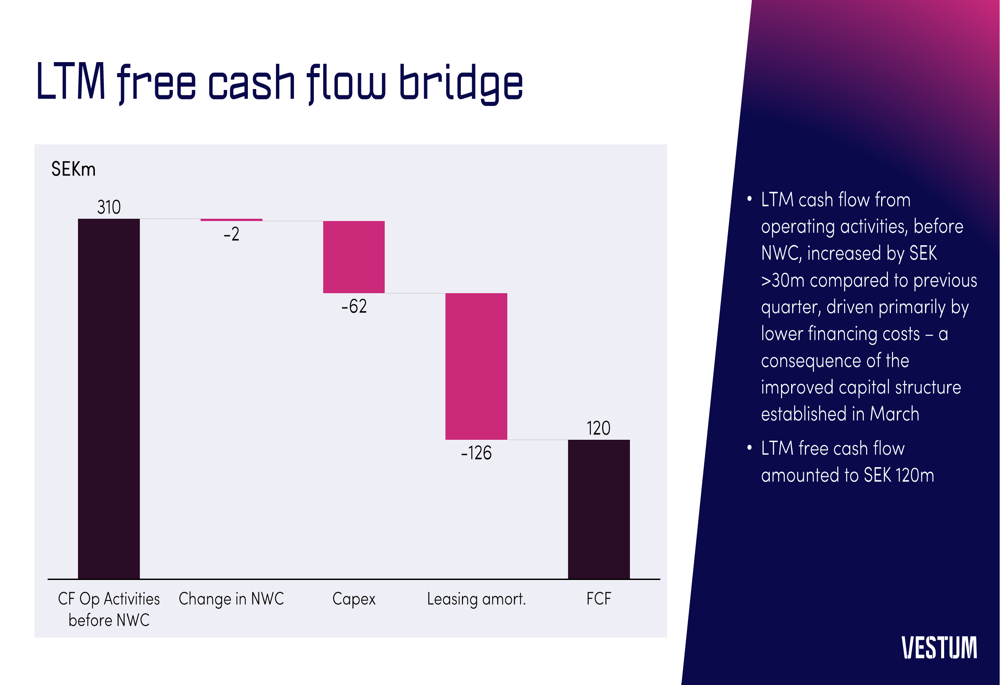

Despite the increased leverage, Vestum reported improved cash flow generation, with LTM free cash flow reaching 120 SEKm. This improvement was attributed to lower financing costs resulting from the improved capital structure established in March:

During the earnings call, management indicated that while they generally aim to maintain leverage below 3x EBITDA, they might exceed this threshold for strategic acquisitions, particularly in the UK water infrastructure sector.

Strategic Initiatives and Outlook

Vestum’s presentation highlighted several strategic priorities and provided insights into the company’s outlook. The company completed one acquisition during the quarter and emphasized its selective approach to M&A, particularly focusing on opportunities in the UK water infrastructure market.

Management expressed caution regarding short-term market conditions but maintained a positive mid-term outlook. For the Solutions segment, profitability is expected to improve as construction investments in Sweden increase from current historically low levels.

The Flow Technology segment is positioned for strong growth in coming years, particularly in the UK where customer investments are in a ramp-up phase that is expected to drive high demand, though with some short-term caution.

As summarized in the company’s presentation:

CEO Simon Göthberg emphasized during the earnings call that the company would not "opportunistically go ahead and make acquisitions across northern Europe just to make acquisitions," underscoring Vestum’s disciplined approach to growth.

With a market capitalization of approximately 339.7 million USD and analyst consensus indicating strong buy recommendations with 33% upside potential, Vestum continues to navigate a challenging but potentially rewarding market environment while maintaining its focus on organic growth and strategic acquisitions in key sectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.