TSX drops after Canadian index edges higher in prior session

Introduction & Market Context

Viper Energy Inc. (NASDAQ:VNOM) released its Q3 2025 investor presentation on November 4, 2025, highlighting strong operational performance and strategic initiatives despite a negative market reaction. The company, which owns royalty interests in oil and natural gas properties primarily in the Permian Basin, saw its stock decline 2.11% to close at $37.82, with an additional 1.14% drop in premarket trading, despite significantly exceeding earnings expectations.

Viper reported earnings per share of $1.04, dramatically outperforming analyst forecasts of $0.37, representing an earnings surprise of 181.08%. Revenue reached $418 million, exceeding expectations of $395.91 million by 5.58%. The company’s business model, which requires zero capital expenditure to support its free cash flow profile, continues to deliver substantial returns to shareholders.

Quarterly Performance Highlights

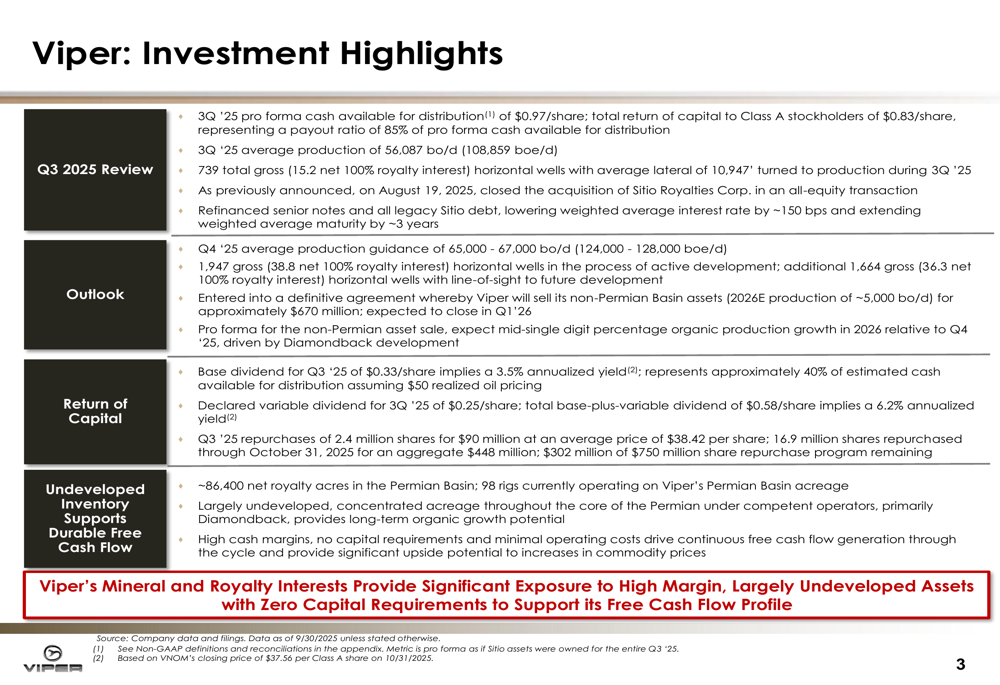

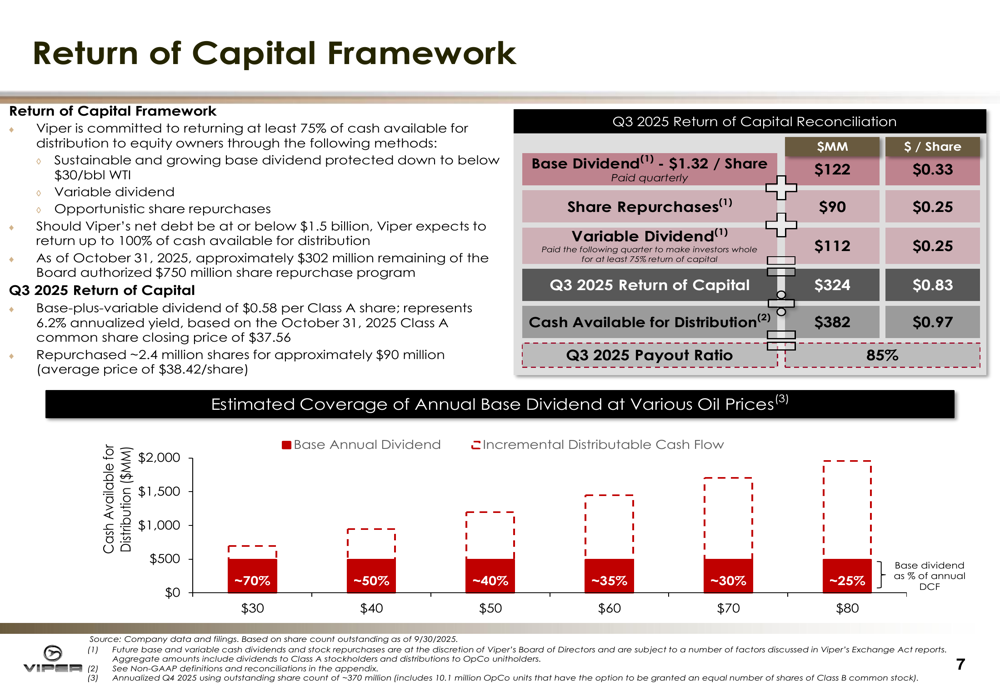

Viper Energy delivered impressive Q3 2025 results, with cash available for distribution reaching $0.97 per share. The company returned 85% of this cash to Class A stockholders, amounting to $0.83 per share. Average production for the quarter stood at 56,087 barrels of oil per day (bo/d) and 108,859 barrels of oil equivalent per day (boe/d).

As shown in the following investment highlights slide, Viper maintained its commitment to shareholder returns through a base dividend of $0.33 per share (implying a 3.5% annualized yield), a variable dividend of $0.25 per share, and the repurchase of 2.4 million shares for $90 million:

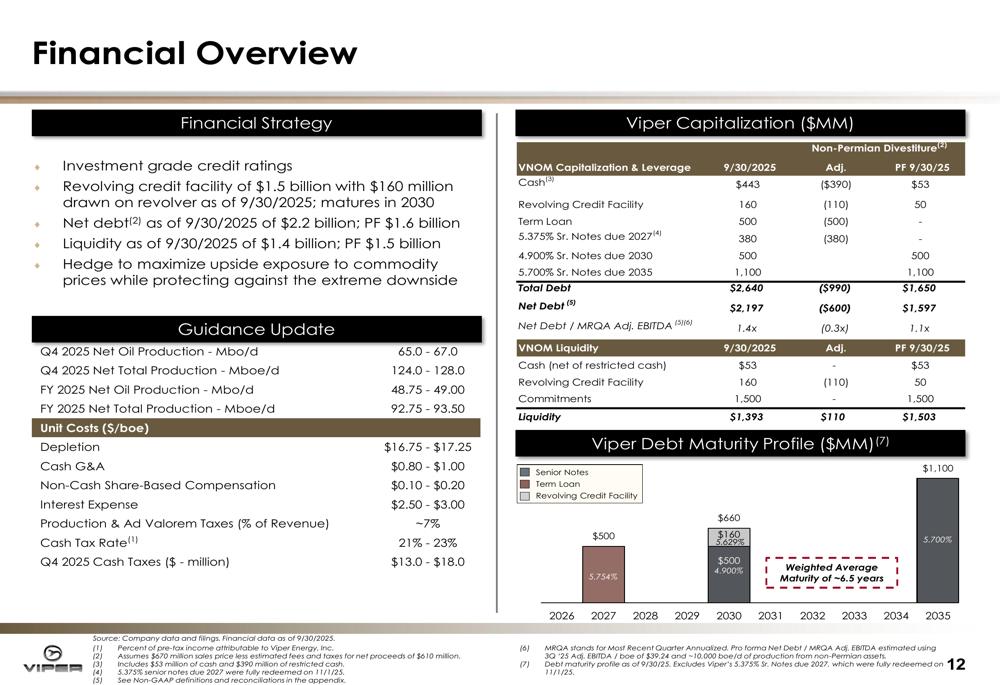

The company’s financial overview reveals a market capitalization of $13.9 billion, net debt of $2.2 billion, and an enterprise value of $16.1 billion. With approximately 95,846 net royalty acres, Viper has established itself as a significant player in the Permian Basin, owning interests in approximately 50% of all oil and gas wells in the region.

Strategic Initiatives

A key strategic development highlighted in the presentation is Viper’s definitive agreement to sell its non-Permian Basin assets for approximately $670 million. These assets represent approximately 5,000 bo/d of expected 2026 production. This divestiture aligns with the company’s strategy to focus on its core Permian Basin operations, where it holds approximately 86,400 net royalty acres.

CEO Kaes Van’t Hof emphasized during the earnings call that "Viper presents a differentiated investment opportunity within the broader energy space," highlighting the company’s unique position and strategic direction. The company plans to use proceeds from the asset sale to pay down debt, which would improve its leverage ratio from 1.4x to 1.1x on a pro forma basis.

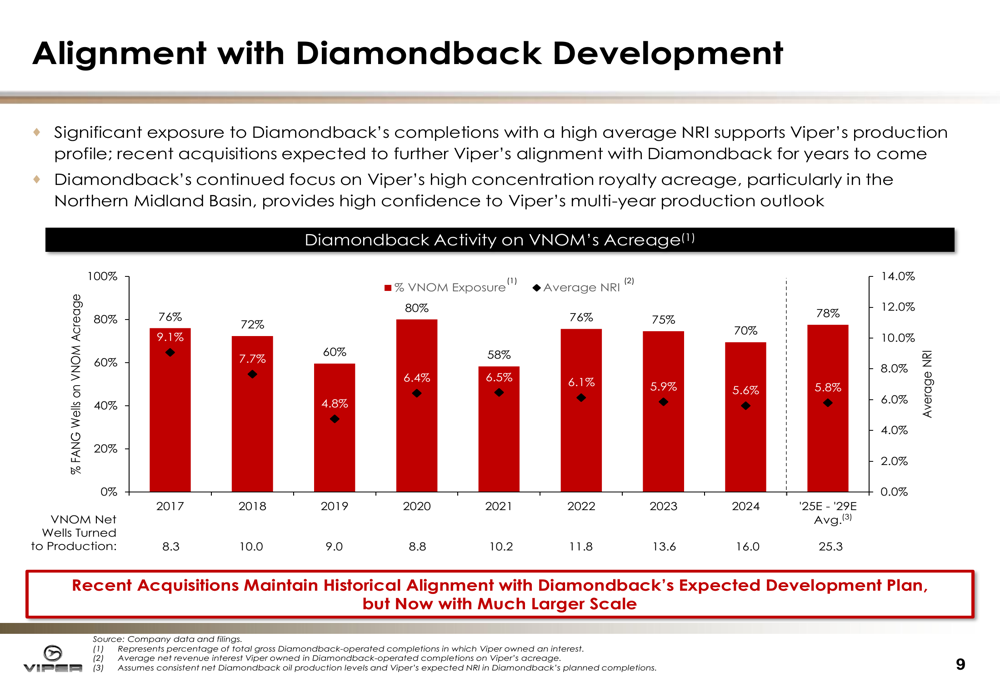

Viper’s relationship with Diamondback Energy, which owns approximately 42% of Viper’s outstanding common stock, continues to provide operational advantages. The following slide illustrates the alignment between Diamondback’s development activities and Viper’s acreage:

Detailed Financial Analysis

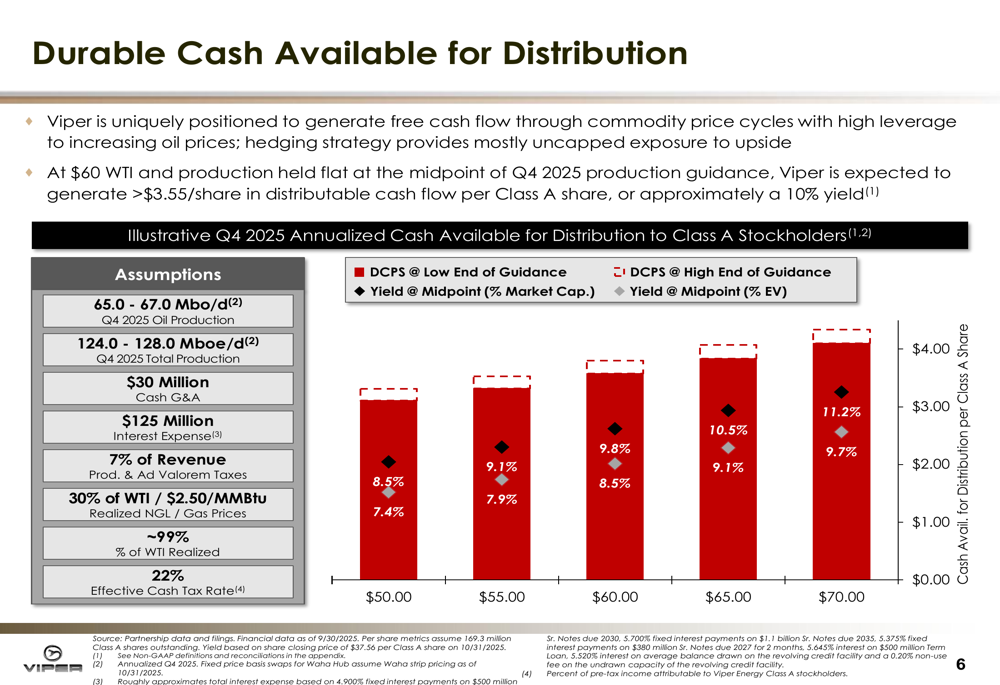

Viper’s financial model demonstrates resilience across various oil price scenarios. The company projects durable cash available for distribution even in lower price environments, with significant upside potential at higher oil prices. The following chart illustrates the annualized cash available for distribution to Class A stockholders under different WTI price scenarios for Q4 2025:

The company’s return of capital framework emphasizes a commitment to returning at least 75% of cash available for distribution to shareholders. For Q3 2025, this included a base dividend of $122 million, a variable dividend of $112 million, and share repurchases of $90 million, resulting in an 85% payout ratio.

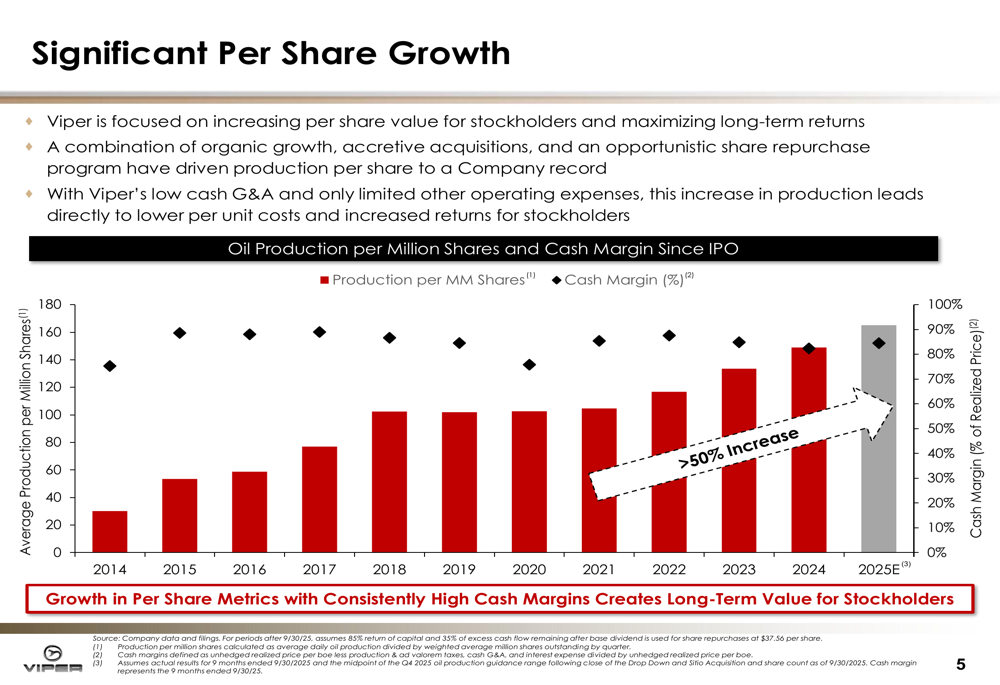

Viper has demonstrated impressive per-share growth since its IPO, with production per million shares increasing from 20 in 2014 to 160 in 2025E, while cash margin has expanded from 0% to 80% over the same period. This focus on per-share metrics underscores management’s commitment to maximizing long-term shareholder value.

Forward-Looking Statements

Looking ahead, Viper provided Q4 2025 production guidance of 65,000-67,000 bo/d (124,000-128,000 boe/d), representing a 20% year-over-year increase. The company anticipates mid-single-digit organic oil production growth in 2026, contrasting with market expectations of zero oil growth in the Permian Basin next year.

Management indicated during the earnings call that they plan to "be a little aggressive as we head into year-end with the buybacks," suggesting continued commitment to shareholder returns. With the planned debt reduction following the non-Permian asset sale, the company aims to return nearly 100% of cash available for distribution going forward.

Viper’s value proposition, as summarized in the presentation, centers on sustainable free cash flow, substantial remaining inventory, organic growth, and durable return of capital:

Despite these positive developments and strong financial performance, investors appear cautious, possibly due to broader market concerns about oil price volatility, potential regulatory changes affecting the energy sector, and economic uncertainties. The disconnect between Viper’s robust operational results and its stock performance highlights the complex factors influencing energy sector valuations in the current market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.