Moody’s upgrades Agnico Eagle’s rating to A3 on debt reduction

Introduction & Market Context

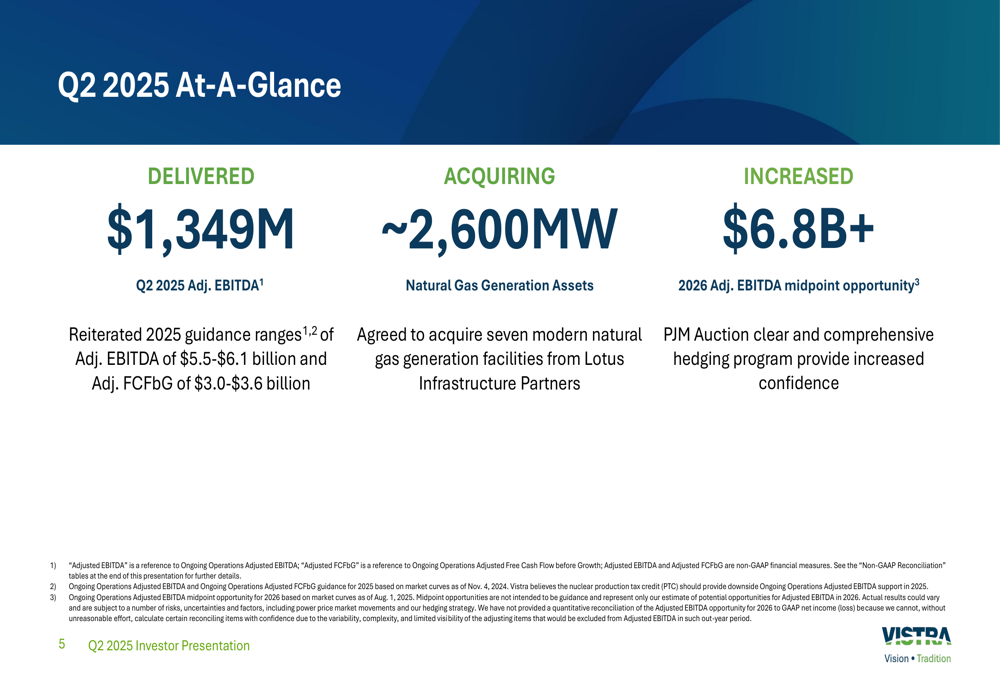

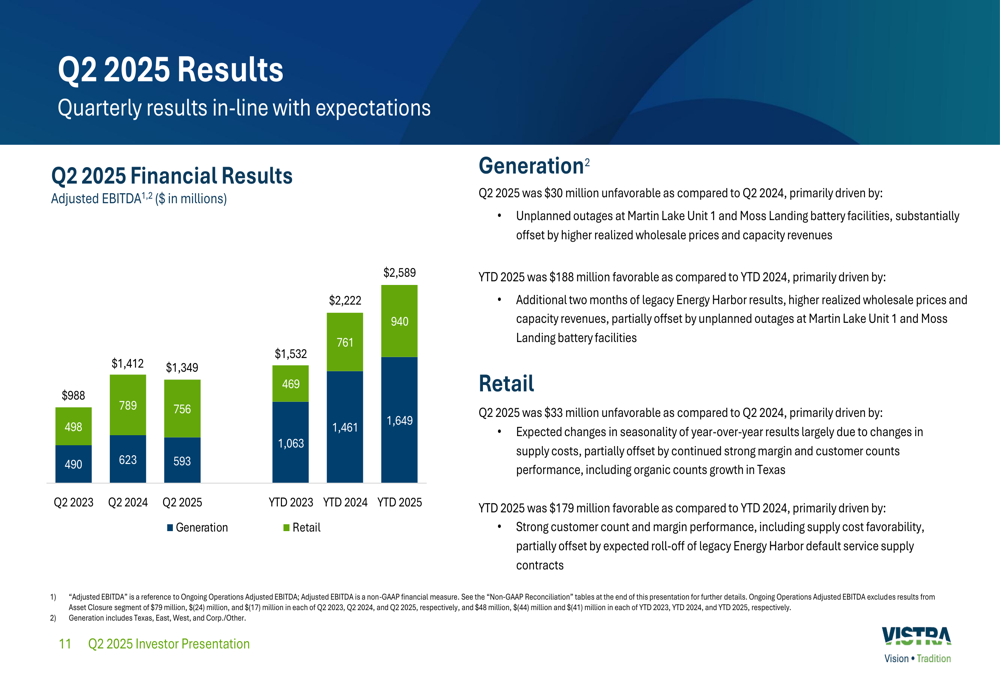

Vistra Energy Corp (NYSE:VST) reported second quarter 2025 Adjusted EBITDA of $1,349 million, slightly below the $1,412 million recorded in the same period last year, according to the company’s Q2 2025 earnings presentation released on August 7, 2025. The integrated power provider’s shares were trading down 3.46% in premarket at $193.91, following the announcement.

Despite the quarterly year-over-year decline, Vistra’s year-to-date Adjusted EBITDA of $2,548 million represents a significant improvement over the $2,178 million reported for the first half of 2024. The company also announced a substantial acquisition of natural gas generation assets while reaffirming its full-year 2025 guidance.

As shown in the following quarterly performance overview, Vistra highlighted three key achievements for the quarter:

Quarterly Performance Highlights

Vistra’s Q2 2025 financial performance showed mixed results compared to the prior year. The generation segment reported a $30 million year-over-year decline, primarily attributed to unplanned outages at Martin Lake Unit 1 and Moss Landing battery facilities. However, this was partially offset by higher realized wholesale prices and capacity revenues. The retail segment similarly experienced a $33 million decrease compared to Q2 2024.

The following chart illustrates Vistra’s quarterly and year-to-date Adjusted EBITDA performance:

Despite these quarterly challenges, Vistra’s year-to-date performance remains strong, with the generation segment showing a $188 million improvement and the retail segment delivering a $179 million increase compared to the first half of 2024. This positive momentum follows a challenging first quarter, when Vistra missed analyst expectations with an EPS of $0.45 against a forecast of $1.19.

Strategic Initiatives

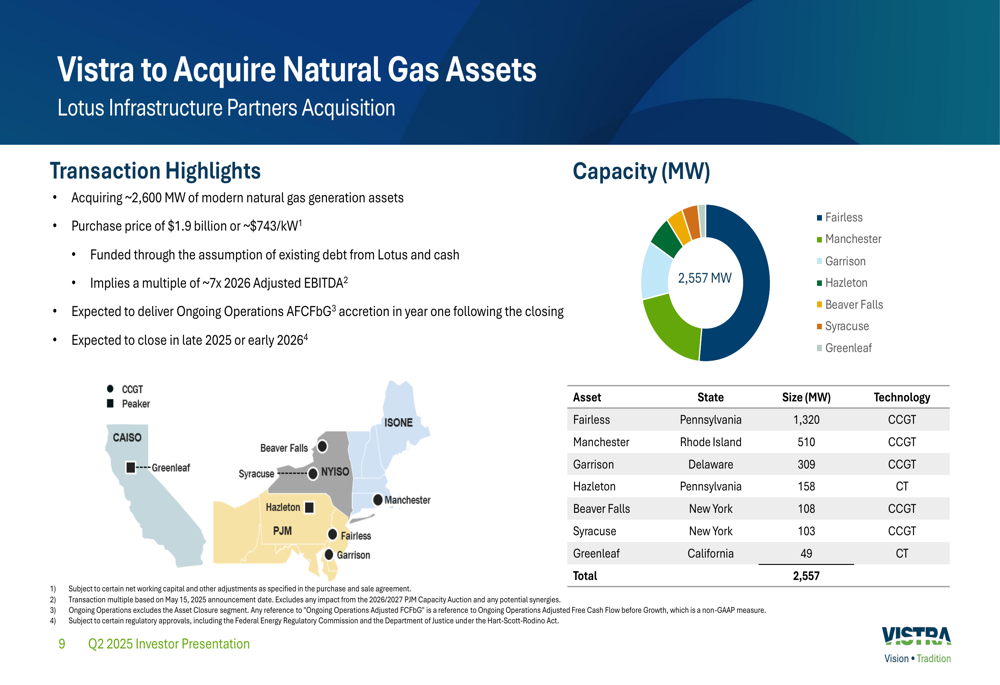

A centerpiece of Vistra’s strategic growth plan is the acquisition of approximately 2,600 MW of natural gas generation assets from Lotus Infrastructure Partners for $1.9 billion, or about $743/kW. The transaction, expected to close in late 2025 or early 2026, includes seven modern facilities across multiple states and is projected to deliver accretion to Adjusted Free Cash Flow before Growth in its first year.

The following slide details the acquisition’s specifics, including the geographic distribution and technical specifications of the assets:

This acquisition aligns with Vistra’s strategic priorities, which include maintaining an integrated business model, implementing disciplined capital allocation, maintaining a resilient balance sheet, and executing a strategic energy transition. The company has successfully relicensed its Perry Nuclear Power Plant through 2046 and is exploring potential nuclear uprates and coal-to-gas conversions.

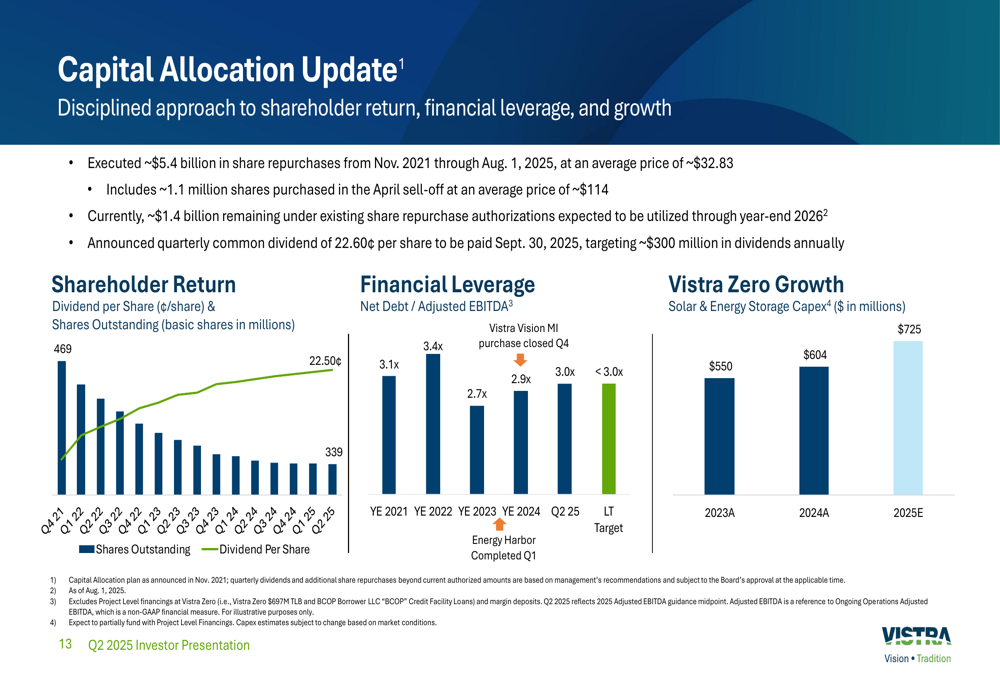

Vistra highlighted its capital allocation strategy, noting that it has executed approximately $5.4 billion in share repurchases from November 2021 through August 1, 2025, at an average price of about $32.83 per share. The company currently has approximately $1.4 billion remaining under its existing share repurchase authorizations.

Forward-Looking Statements

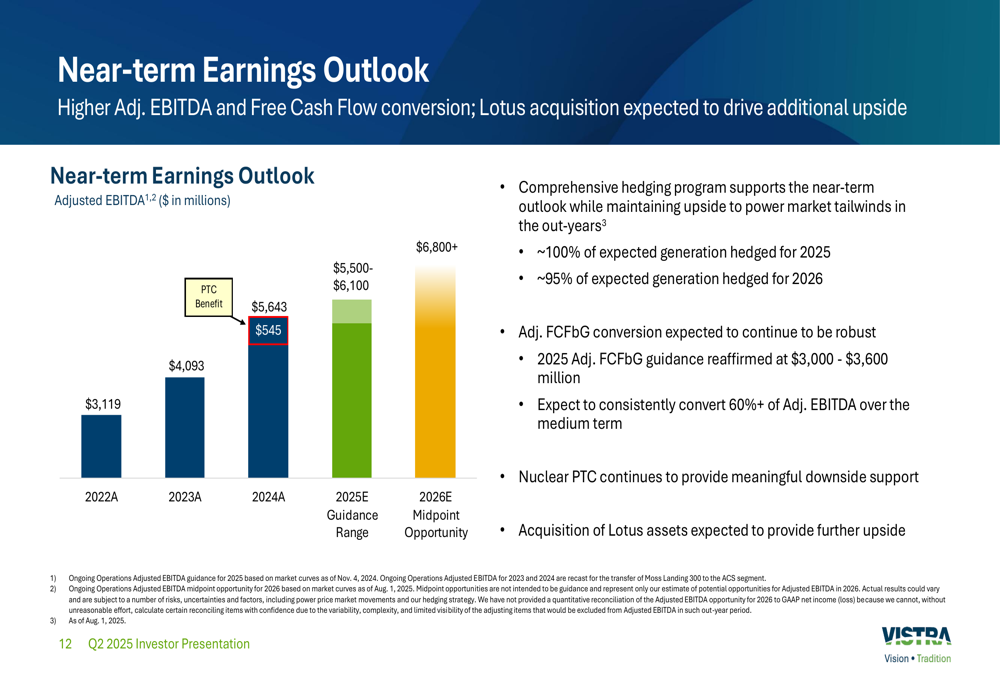

Vistra reaffirmed its 2025 guidance, projecting Adjusted EBITDA between $5,500 million and $6,100 million, and Adjusted Free Cash Flow before Growth between $3,000 million and $3,600 million. Looking further ahead, the company increased its 2026 Adjusted EBITDA midpoint opportunity to over $6,800 million, citing confidence from the PJM Auction clear and its comprehensive hedging program.

The following chart illustrates Vistra’s historical performance and future earnings outlook:

Management emphasized that the Lotus acquisition is expected to provide further upside to these projections. The company’s comprehensive hedging program is designed to support near-term outlook while maintaining upside exposure to power market tailwinds in later years.

Competitive Industry Position

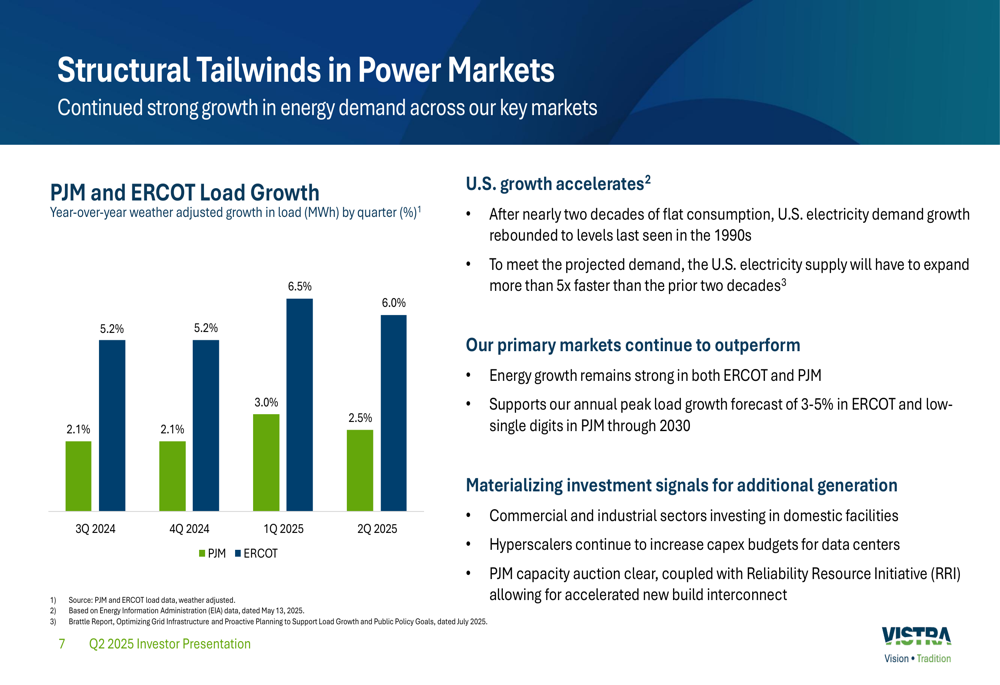

Vistra is capitalizing on structural tailwinds in power markets, particularly the accelerating electricity demand growth in its core ERCOT (Texas) and PJM markets. The company reported that ERCOT experienced 6.0% year-over-year weather-adjusted load growth in Q2 2025, while PJM saw 2.5% growth during the same period.

The following chart illustrates these growth trends across recent quarters:

This growth is driven largely by commercial and industrial investments, particularly from data centers and AI infrastructure. Vistra noted that after nearly two decades of flat consumption, U.S. electricity demand has rebounded to levels last seen in the 1990s, requiring the electricity supply to expand more than five times faster than in the prior two decades.

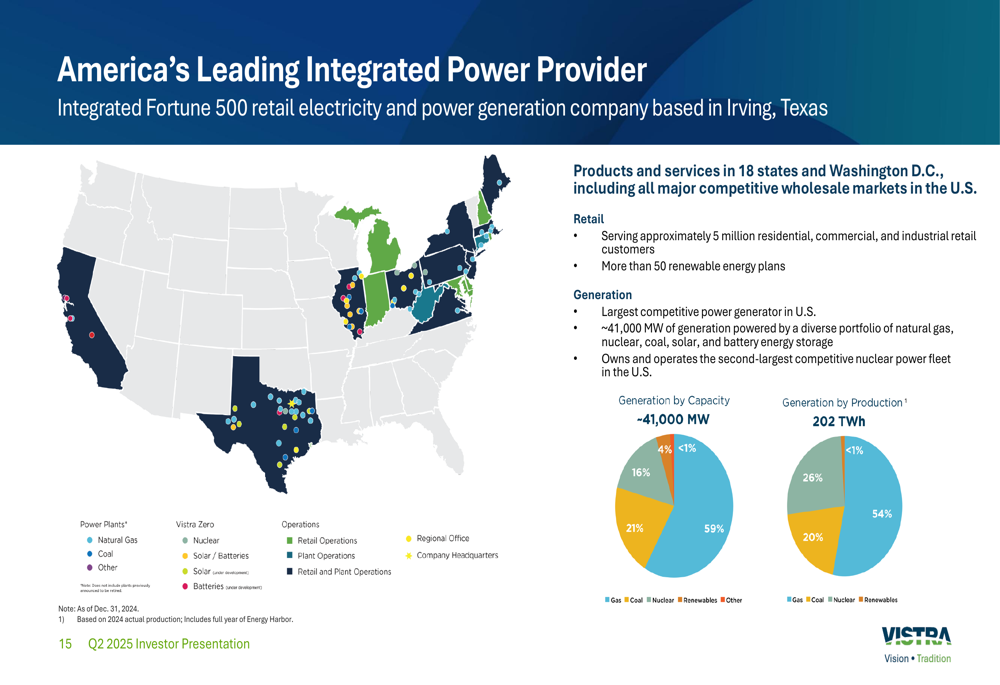

As America’s leading integrated power provider, Vistra operates a diverse generation portfolio of approximately 41,000 MW, making it the largest competitive power generator in the U.S. The company serves approximately 5 million retail customers and owns the second-largest nuclear power fleet in the country.

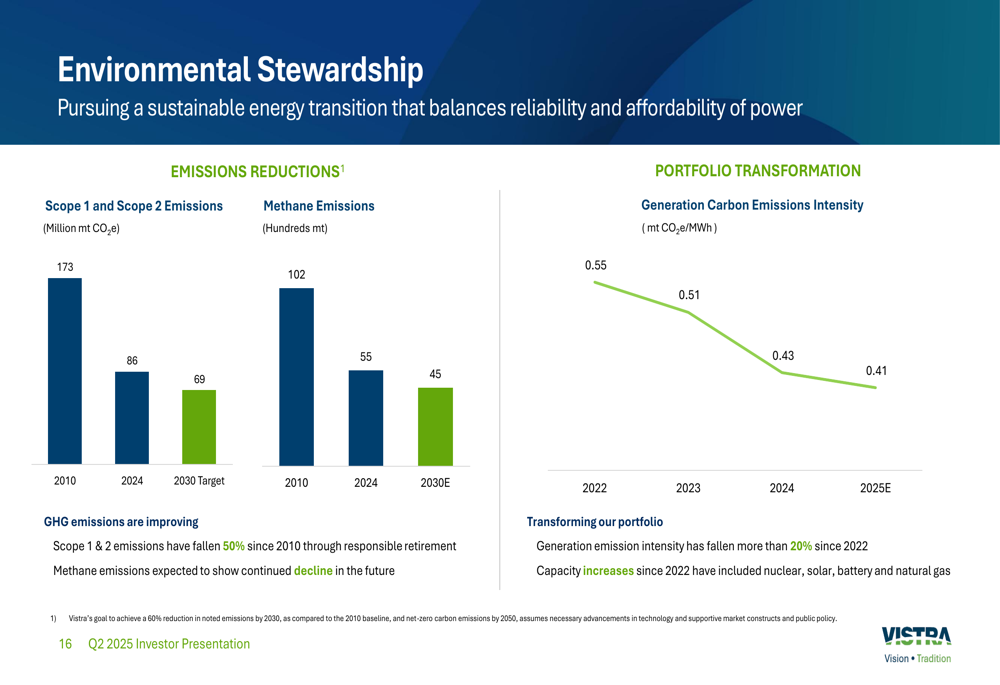

Vistra is also advancing its environmental stewardship goals, showing progress in reducing greenhouse gas emissions and improving its generation carbon emission intensity. The company’s transformation includes increasing capacity through nuclear, solar, batteries, and natural gas assets.

In conclusion, while Vistra’s Q2 2025 results showed a slight year-over-year decline, the company’s year-to-date performance remains strong. The acquisition of natural gas assets from Lotus Infrastructure Partners represents a significant strategic expansion, positioning Vistra to capitalize on growing electricity demand, particularly from data centers and AI infrastructure. Despite trading down in premarket, the company has reaffirmed its full-year guidance and increased its 2026 earnings outlook, signaling confidence in its long-term growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.