Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

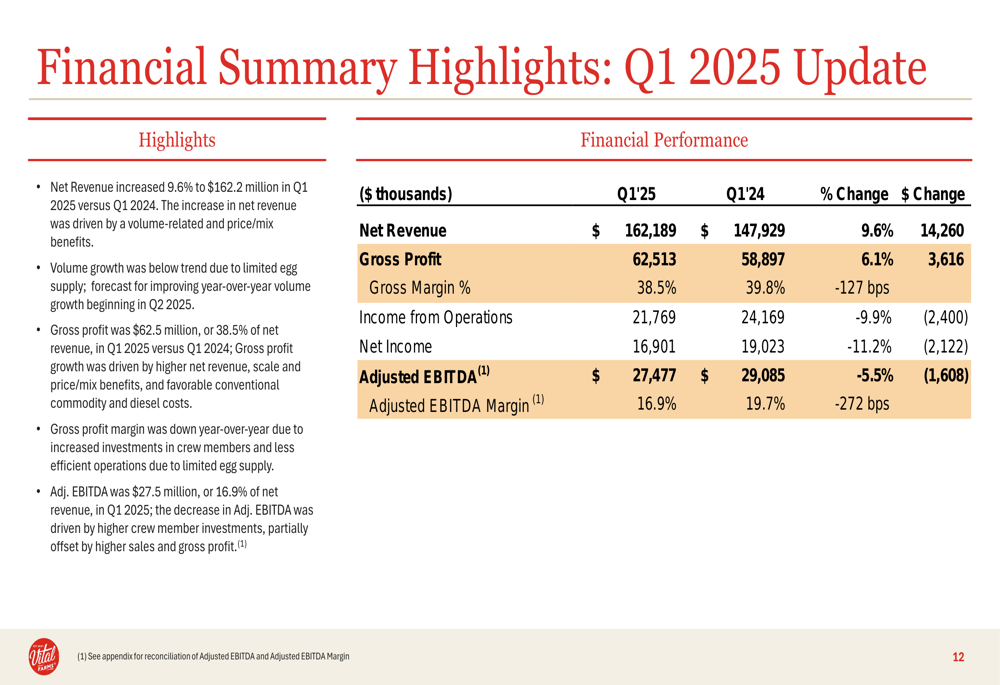

Vital Farms, Inc. (NASDAQ:VITL) released its Q1 2025 corporate presentation on May 8, revealing mixed financial results with continued revenue growth but declining profitability metrics. The ethical egg producer reported a 9.6% year-over-year revenue increase to $162.2 million, while experiencing margin compression and reduced earnings per share. Despite these challenges, the company reiterated its full-year 2025 guidance and maintained its ambitious 2027 targets.

The stock has been under pressure, trading down 2.7% in pre-market activity to $34.95, extending its decline following yesterday’s close at $35.92. This reaction suggests investors may be concerned about the company’s slowing growth trajectory and profitability challenges, despite its continued expansion in brand awareness and consumer reach.

Quarterly Performance Highlights

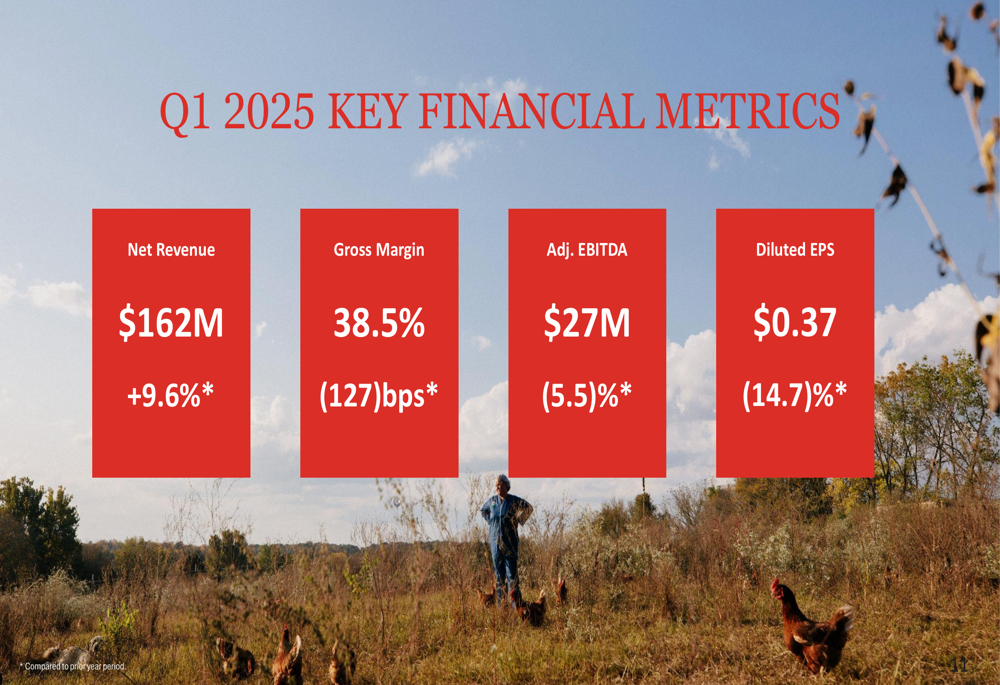

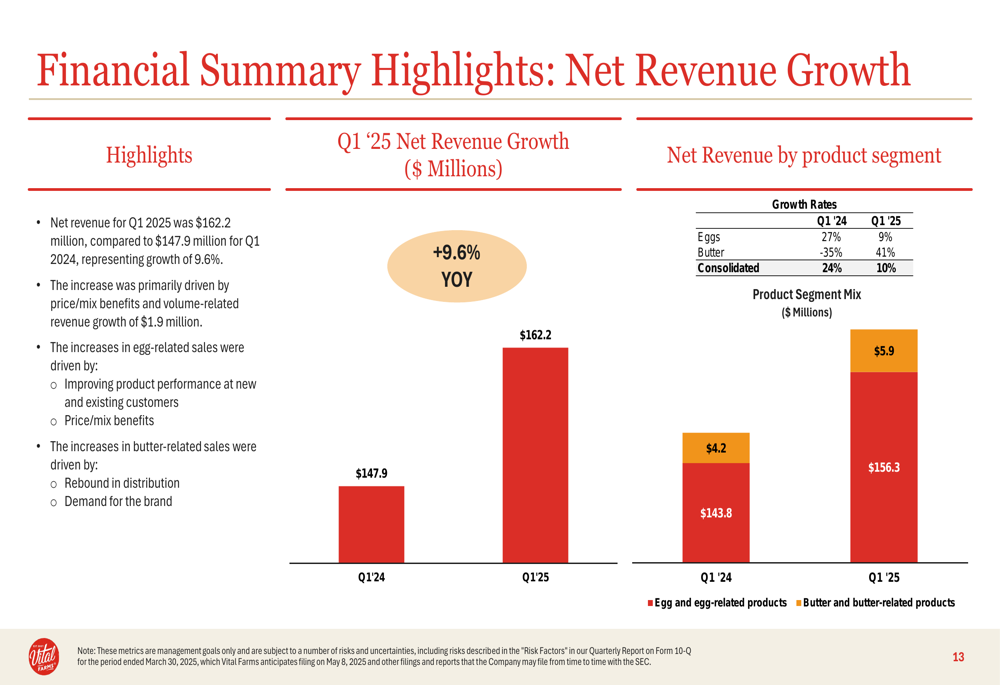

Vital Farms delivered a 9.6% year-over-year revenue increase to $162.2 million in Q1 2025, primarily driven by price/mix benefits and volume-related revenue growth, though the company noted that volume growth was below trend.

As shown in the following financial metrics summary:

The company reported a gross margin of 38.5%, representing a 127 basis point decrease compared to the prior year period. Adjusted EBITDA declined 5.5% to $27 million, while diluted earnings per share fell 14.7% to $0.37.

A more detailed breakdown of the financial performance reveals the pressure points affecting the company’s profitability:

Detailed Financial Analysis

Vital Farms’ revenue growth was driven by increases in both egg and butter product segments, with particularly strong performance in the butter category. Egg-related sales grew 9% year-over-year to $156.3 million, while butter-related sales surged 41% to $5.9 million, though from a much smaller base.

The following chart illustrates the revenue growth by product segment:

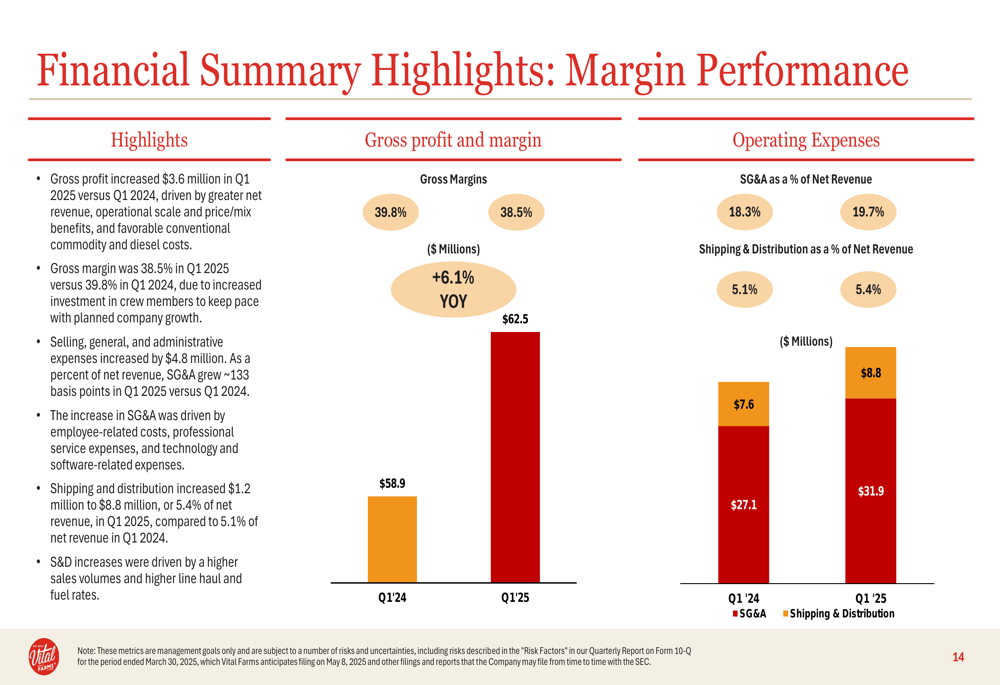

Despite the revenue growth, profitability metrics declined across the board. Gross profit increased by $3.6 million, but gross margin contracted to 38.5% from 39.8% in the prior year period, which the company attributed to increased investments in crew members. Operating expenses also increased, with selling, general, and administrative expenses rising by $4.8 million and shipping and distribution costs increasing by $1.2 million.

The margin performance is illustrated in the following chart:

Competitive Industry Position

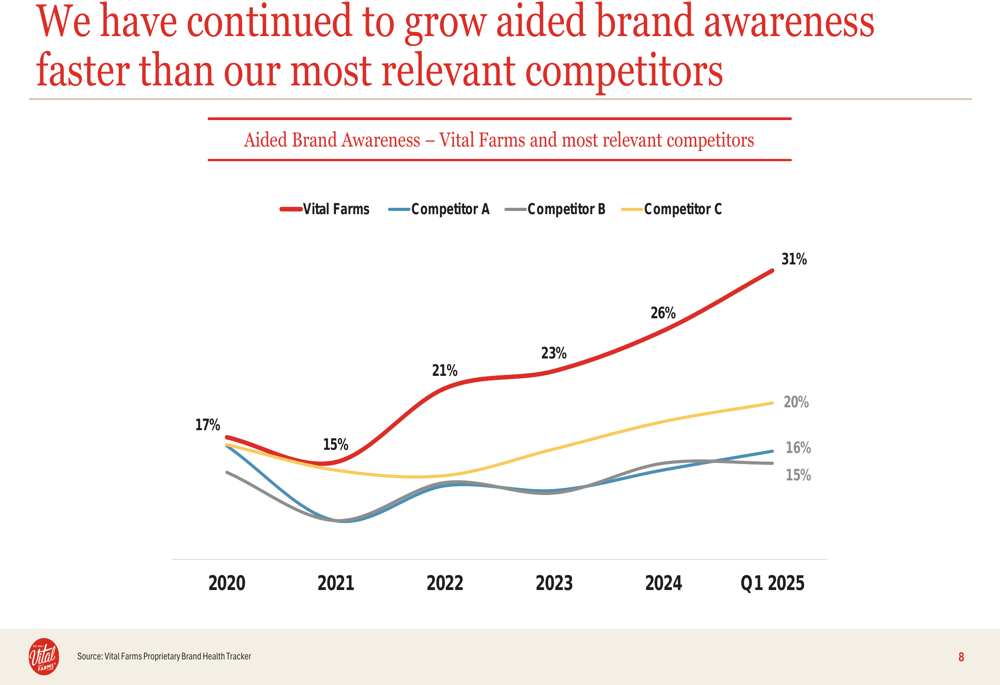

Vital Farms continues to strengthen its competitive position in the premium egg market. The company’s aided brand awareness has grown significantly from 17% in 2020 to 31% in Q1 2025, outpacing its closest competitors who have shown relatively flat or modest growth in brand awareness during the same period.

The following chart demonstrates Vital Farms’ brand awareness advantage:

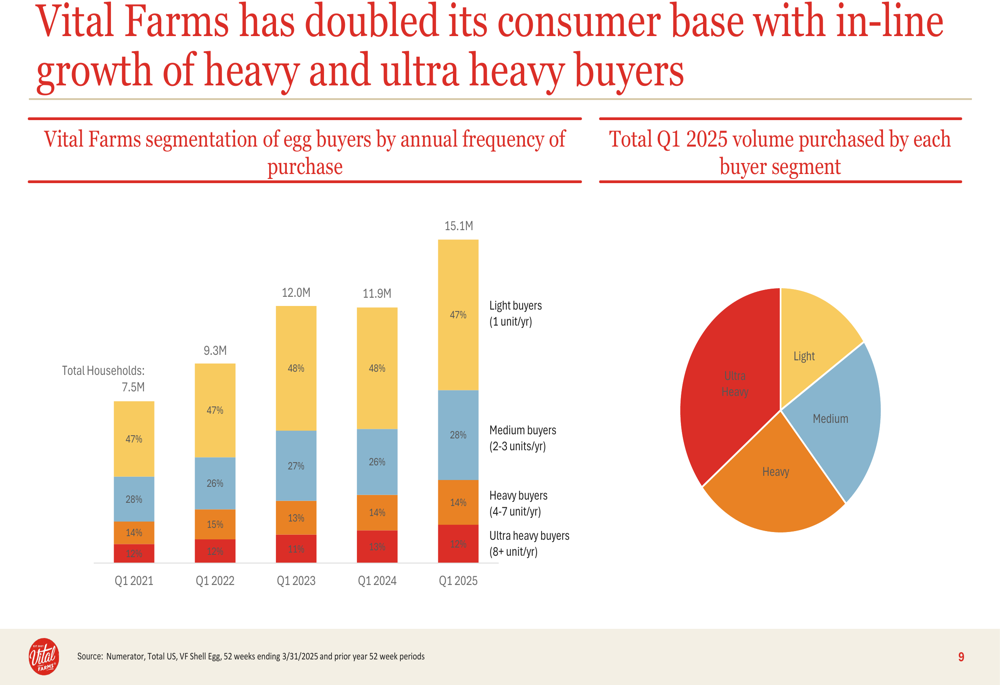

The company has also successfully expanded its consumer base, doubling from 7.5 million households in Q1 2021 to 15.1 million in Q1 2025. Light buyers (purchasing 1 unit per year) represent the largest segment at 47% of the consumer base, while ultra-heavy buyers (8+ units per year) account for 12%.

This consumer base growth is illustrated in the following chart:

Strategic Initiatives

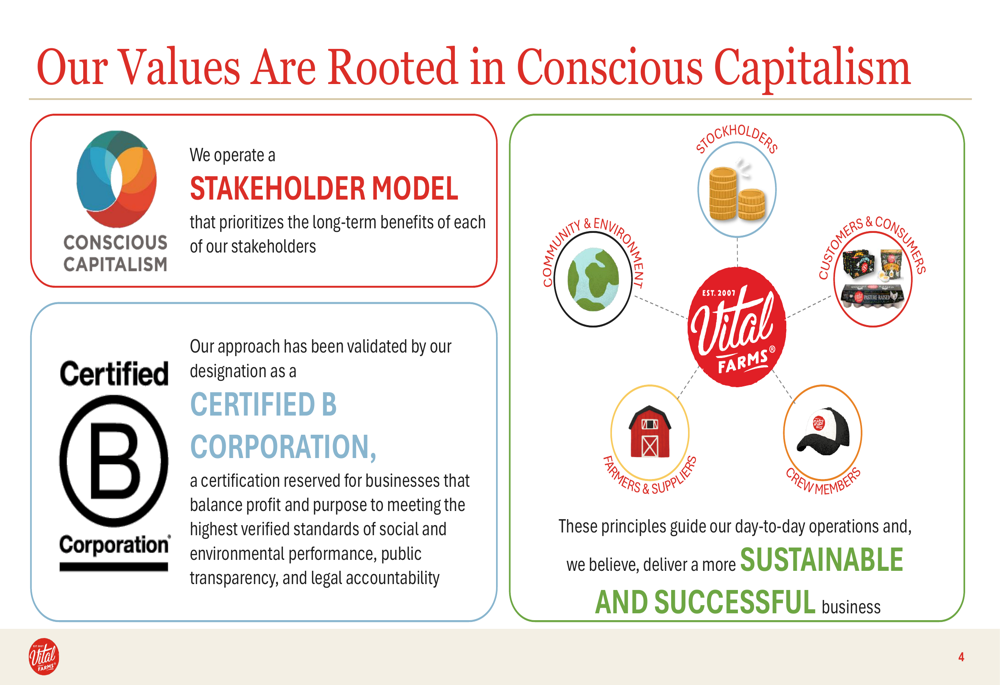

Vital Farms continues to position itself as an ethical alternative to factory farming, emphasizing its commitment to conscious capitalism and sustainable practices. The company operates with a stakeholder model that balances the interests of stockholders, community and environment, customers and consumers, crew members, and farmers and suppliers.

The company’s stakeholder approach is visualized in this diagram:

Vital Farms’ business model is built on a network of over 450 family farms, primarily located in the "Pasture Belt" across the United States where climate conditions are suitable for year-round production. The company aggregates products at its Egg Central Station in Springfield, Missouri, where they are processed under quality control before being distributed to approximately 26,000 retail stores nationwide.

The company’s quality-at-scale model is illustrated in the following diagram:

Forward-Looking Statements

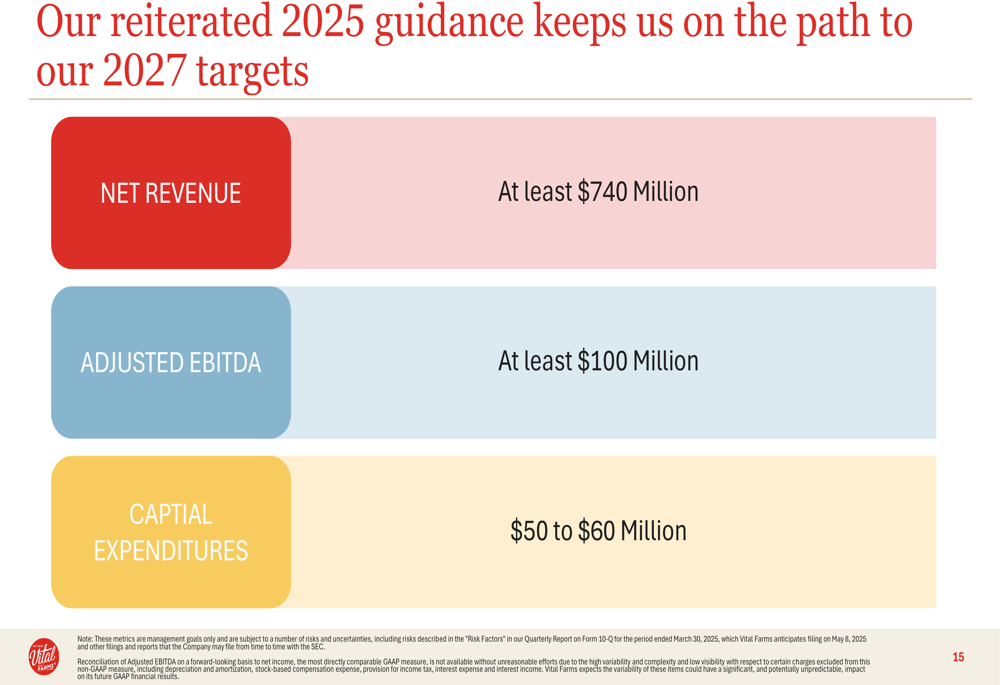

Despite the mixed Q1 results, Vital Farms reiterated its full-year 2025 guidance, projecting net revenue of at least $740 million, adjusted EBITDA of at least $100 million, and capital expenditures between $50 million and $60 million.

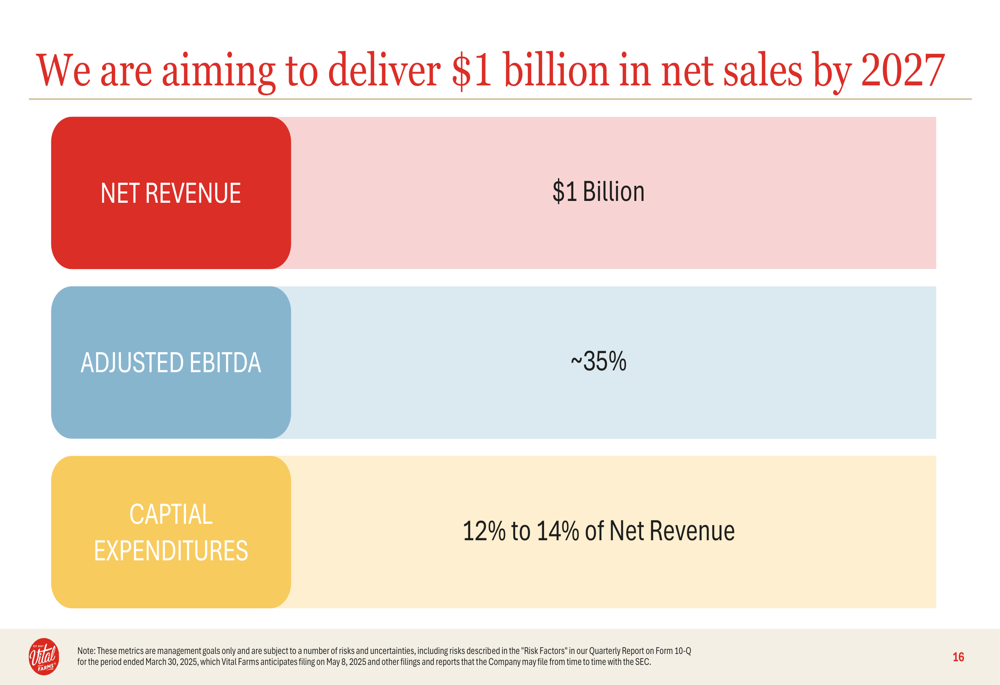

Looking further ahead, the company maintained its ambitious 2027 targets, aiming to reach $1 billion in net revenue with an adjusted EBITDA margin of approximately 35% and capital expenditures representing 12% to 14% of net revenue.

These targets align with the company’s long-term growth strategy, though they may face challenges given the current margin pressures and slowing volume growth. The Q4 2024 earnings call had previously highlighted tight supply in the premium egg market as an ongoing challenge, along with potential risks from avian influenza and supply chain disruptions.

Vital Farms’ ability to achieve these targets will likely depend on its success in expanding distribution, growing consumer awareness, and managing costs while maintaining its commitment to ethical farming practices and stakeholder value creation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.