Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

Vitesse Energy Inc. (NYSE:VTS) released its corporate presentation on May 6, 2025, highlighting its strategy as a predominantly non-operated working interest owner in the Bakken oil field of North Dakota. The presentation comes on the heels of a disappointing Q4 2024 earnings report where the company missed both EPS and revenue forecasts significantly.

Despite these challenges, Vitesse’s stock has remained relatively stable, closing at $21.36 on May 5, 2025, with a slight increase of 0.05%. The company continues to position itself as a high-yield dividend play in the energy sector, emphasizing its long-term inventory and capital allocation strategy.

Executive Summary

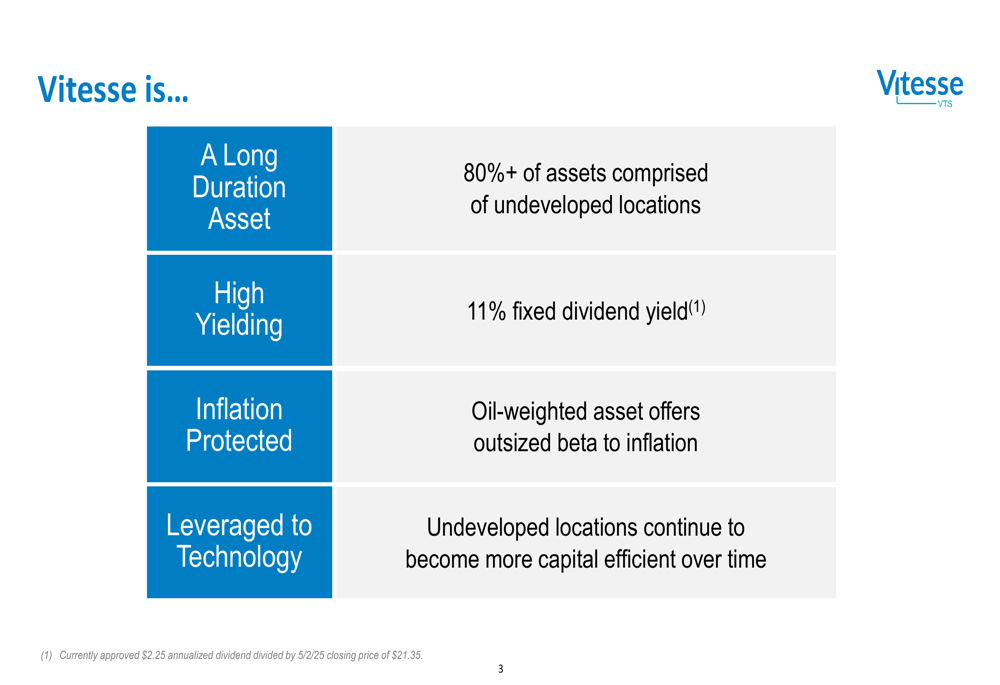

Vitesse Energy’s presentation emphasizes four key attributes that define its investment proposition: a long-duration asset base with over 80% comprised of undeveloped locations, a high 11% fixed dividend yield, inflation protection through its oil-weighted portfolio, and leverage to technological improvements that increase capital efficiency over time.

As shown in the following slide detailing these key attributes:

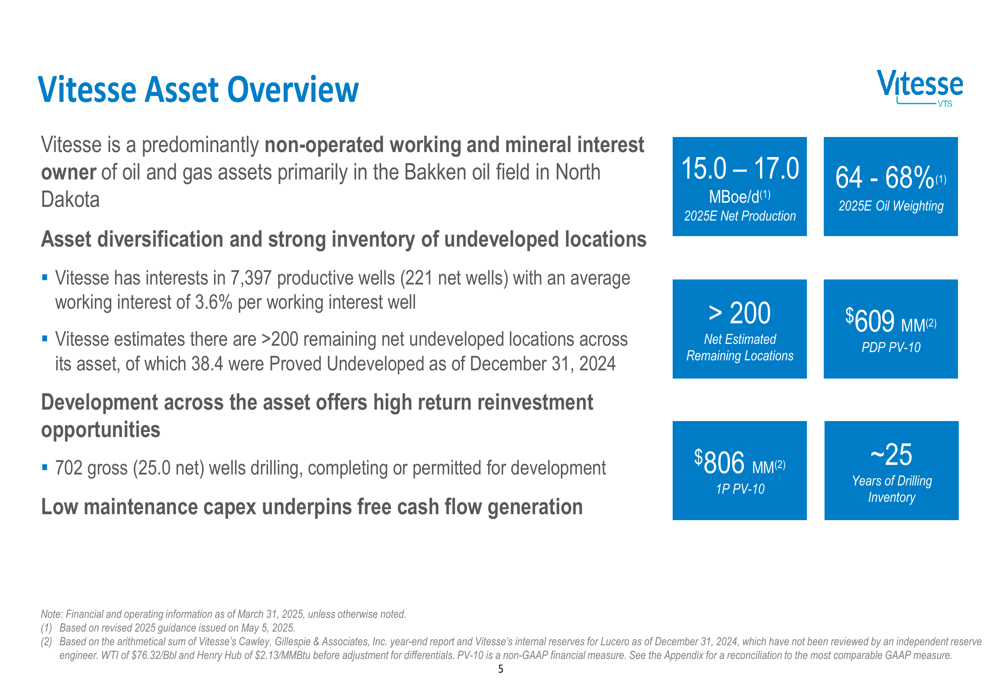

The company maintains interests in 7,397 productive wells (221 net wells) across the Williston Basin with an average working interest of 3.6% per well. Vitesse estimates it has more than 200 remaining net undeveloped locations, representing approximately 25 years of drilling inventory.

Strategic Initiatives

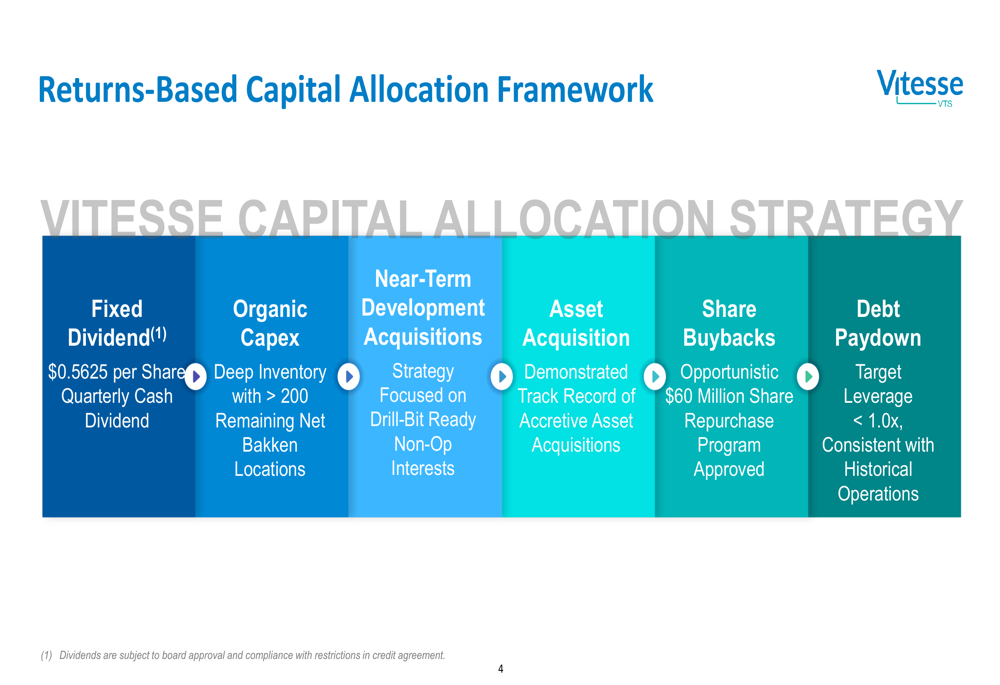

Vitesse’s capital allocation strategy centers on maintaining its quarterly dividend of $0.5625 per share while balancing organic capital expenditures, strategic acquisitions, share repurchases, and debt management. The company has approved an opportunistic $60 million share repurchase program and targets a leverage ratio below 1.0x.

The following slide illustrates this balanced approach to capital allocation:

CEO Bob Garrity emphasized in the recent earnings call that "Our product is our dividend and everything we do is focused on supporting that dividend," highlighting the centrality of the dividend to Vitesse’s business model. The company’s current annualized dividend of $2.25 represents an 11% yield based on the May 2, 2025 closing price of $21.35.

Detailed Financial Analysis

For 2025, Vitesse has issued production guidance of 15.0-17.0 MBoe/d with 64-68% oil weighting, representing a 35% increase from 2024 levels. This guidance was revised on May 5, 2025, as noted in the company’s asset overview:

The company reports a PDP PV-10 (Proved Developed Producing reserves at a 10% discount rate) of $609 million and a 1P PV-10 (Proved reserves) of $806 million. However, these forward-looking metrics should be viewed in context of Vitesse’s recent financial performance, which included an EPS of -0.285 for Q4 2024, significantly below the forecasted 0.58, and revenue of $59.8 million against expectations of $71.18 million.

Vitesse’s total debt at year-end 2024 stood at $117 million, with full-year Adjusted EBITDA of $156.8 million. The company has implemented a hedging strategy with 53% of oil production hedged at $71.16 per barrel, providing some protection against market volatility.

Competitive Industry Position

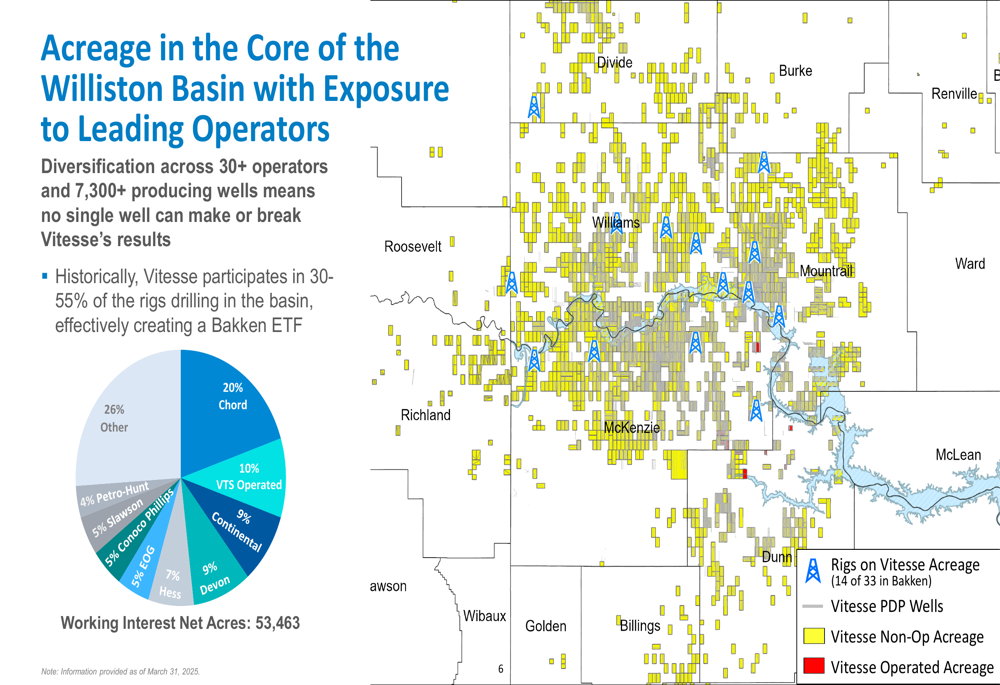

Vitesse’s acreage is diversified across more than 30 operators in the Williston Basin, with the company participating in 30-55% of the rigs drilling in the basin. This diversification strategy means that no single well can significantly impact Vitesse’s overall results.

The following map illustrates Vitesse’s acreage position and operator distribution:

Major operators on Vitesse’s acreage include Chord (20%), Devon (9%), Hess (NYSE:HES) (7%), ConocoPhillips (NYSE:COP) (5%), Slawson (5%), and Petro-Hunt (4%), with the remaining 26% distributed among other operators. This diversification provides operational stability while allowing Vitesse to benefit from the expertise of established industry players.

Forward-Looking Statements

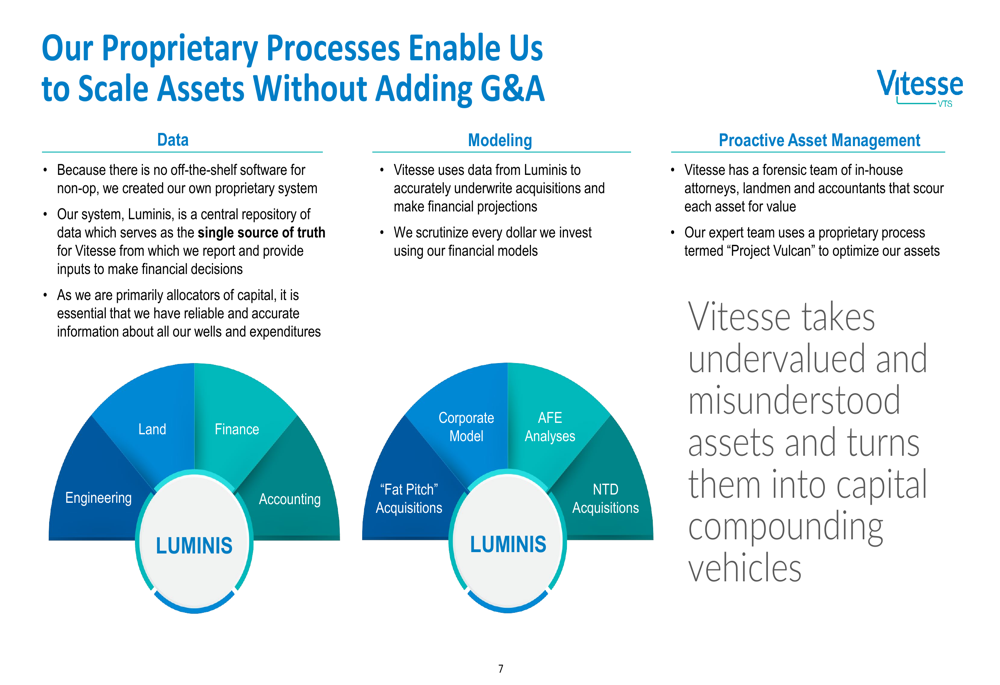

A distinctive aspect of Vitesse’s strategy is its proprietary data management system called "Luminis," which serves as the central repository for well and financial data. The company uses this system to underwrite acquisitions, make financial projections, and optimize asset management.

The following slide details how these proprietary processes enable Vitesse to scale without adding significant G&A costs:

Vitesse’s management believes these systems provide a competitive advantage in identifying undervalued assets and optimizing returns. The company has completed nearly 200 acquisitions and divestitures totaling $757 million, demonstrating its active portfolio management approach.

Investment Considerations

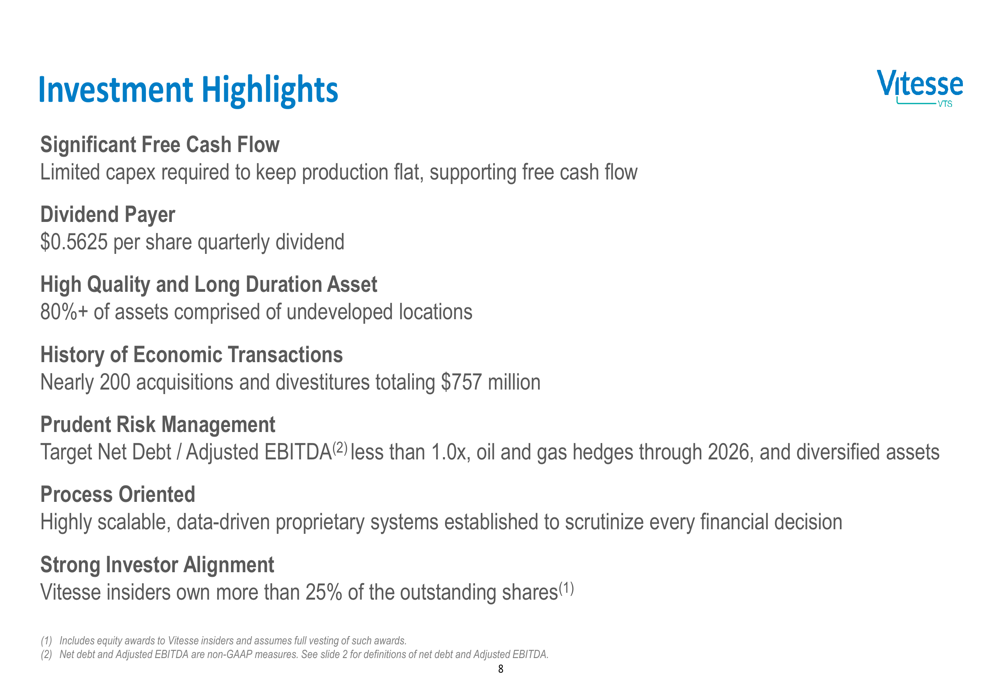

While Vitesse presents an attractive dividend yield and long-term inventory, investors should consider several risk factors highlighted in both the presentation and recent earnings report. These include potential operational challenges due to gas processing capacity limitations, market volatility in oil and gas prices, and the company’s recent earnings miss.

The following slide summarizes Vitesse’s investment highlights:

Strong insider alignment is emphasized, with company insiders owning more than 25% of outstanding shares. This alignment of interests between management and shareholders may provide some reassurance despite recent financial underperformance.

For investors focused on valuation metrics, Vitesse trades at an EV/EBITDA multiple of 4.84x according to recent data, suggesting a relatively attractive valuation compared to peers, though this must be balanced against the company’s recent financial results and ongoing market challenges in the energy sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.