BofA update shows where active managers are putting money

Introduction & Market Context

Vivid Seats Inc. (NASDAQ:SEAT) presented its Q2 2025 financial results on August 5, 2025, revealing significant declines across all key metrics amid what the company described as "uncertainty in current industry environment." The ticket marketplace reported a dramatic widening of its net loss to $263.3 million, compared to just $1.2 million in the same quarter last year, while announcing a $25 million cost reduction program.

The company’s stock, which had already fallen 35.66% following disappointing Q1 results earlier this year, continued its downward trend. SEAT shares are currently trading near $1.32, approaching their 52-week low of $1.30 and significantly below their 52-week high of $5.00.

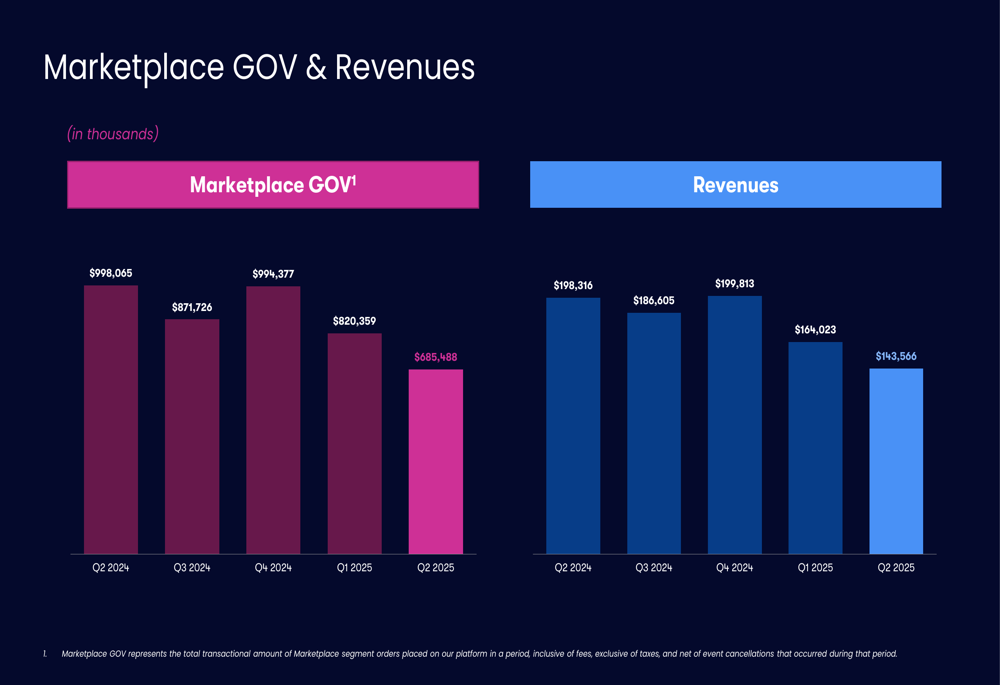

As shown in the following financial overview slide, Vivid Seats’ performance deteriorated substantially in the second quarter:

Quarterly Performance Highlights

Vivid Seats reported Q2 2025 Marketplace Gross Order Value (GOV) of $685 million, representing a 31.3% decline from $998 million in Q2 2024. Revenue fell to $144 million, down 27.6% year-over-year from $198 million. Adjusted EBITDA, a key profitability metric for the company, plummeted 67.5% to $14 million compared to $44 million in the prior-year period.

The five-quarter trend clearly illustrates the company’s deteriorating performance trajectory across both GOV and revenue metrics:

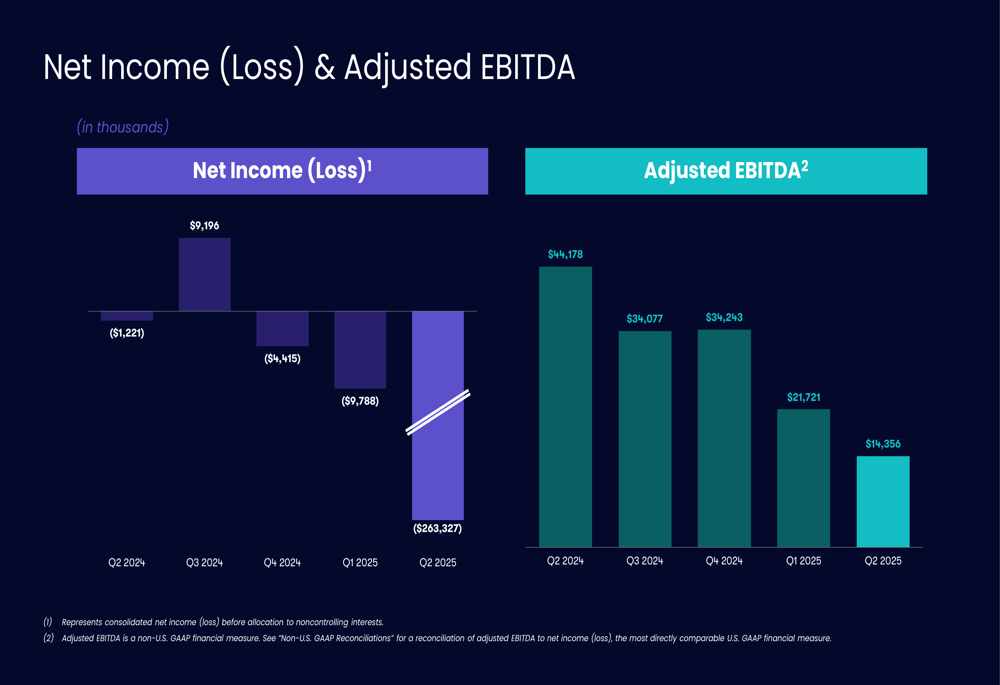

Even more concerning is the dramatic worsening of Vivid Seats’ net loss, which ballooned to $263.3 million in Q2 2025 from just $1.2 million in Q2 2024. This represents a net loss per share of $1.07, compared to $0.01 in the same period last year. Adjusted EBITDA has also shown a consistent downward trend over the past five quarters:

Detailed Financial Analysis

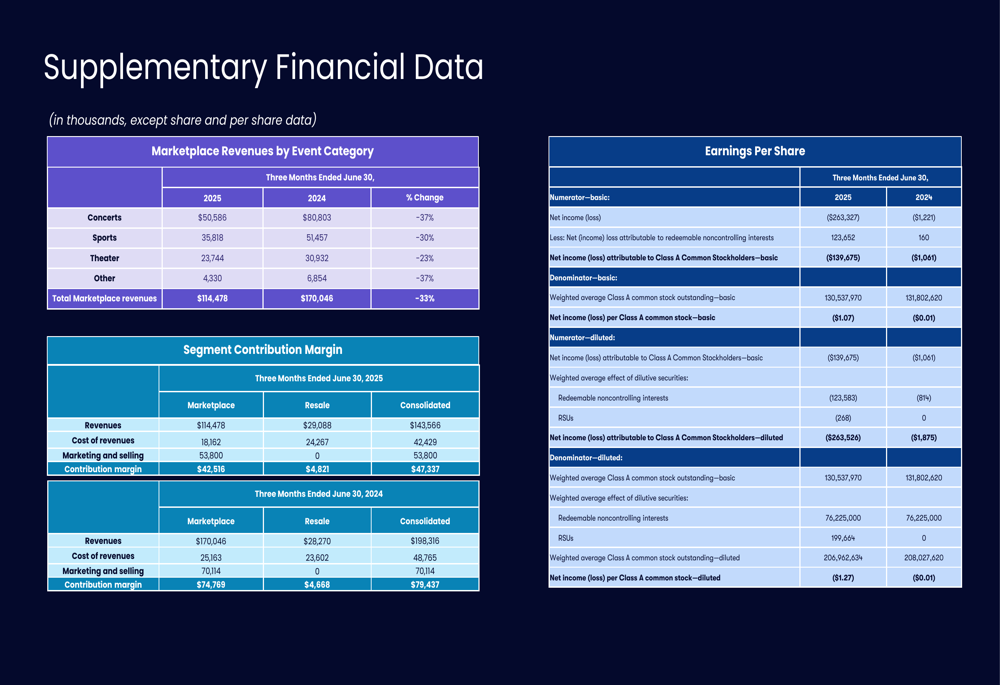

A closer examination of Vivid Seats’ revenue by event category reveals double-digit declines across all segments. Concerts, which represent the largest portion of the company’s business, saw the steepest drop at 37%, followed by the "Other" category (also down 37%), Sports (down 30%), and Theater (down 23%).

The company’s segment contribution margin data shows that while the Marketplace segment generated $42.5 million in contribution margin, this was partially offset by much thinner margins in the Resale segment. The consolidated contribution margin of $47.3 million was insufficient to cover other operating expenses, contributing to the substantial net loss.

The detailed breakdown of revenue by category and segment contribution margins provides additional insight into the company’s financial challenges:

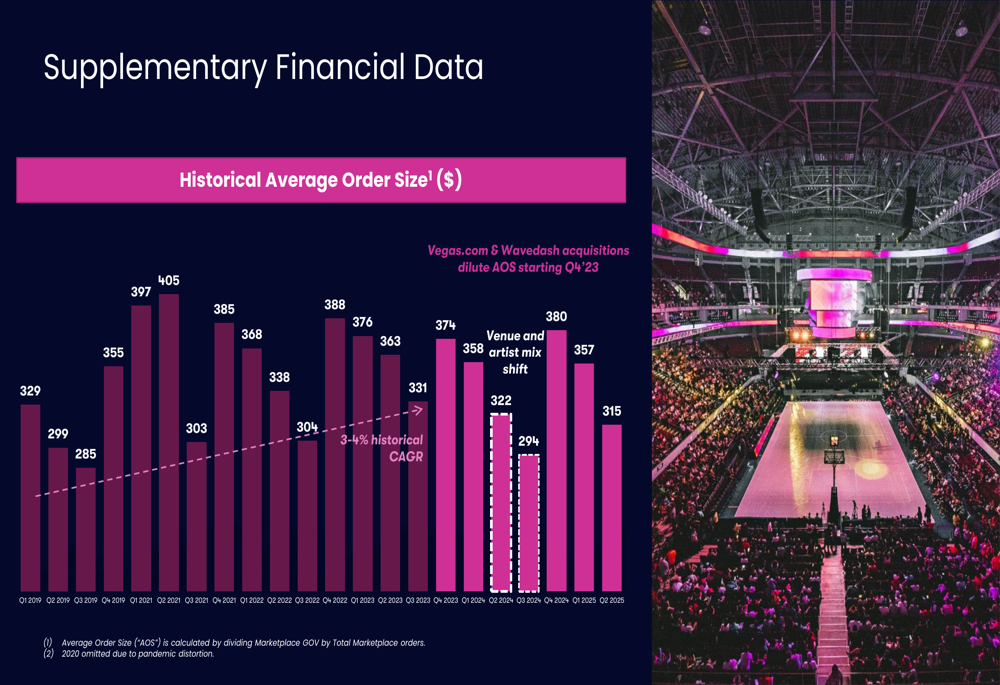

The average order size (AOS) has also shown a concerning trend, with recent quarters showing dilution in this key metric compared to historical levels:

Strategic Initiatives

In response to these challenges, Vivid Seats announced a cost reduction program targeting $25 million in annualized savings by the end of 2025. The company described this initiative as both "right-sizing for the current environment and long-term structural efficiency improvements," suggesting a recognition that some of the current challenges may be persistent rather than temporary.

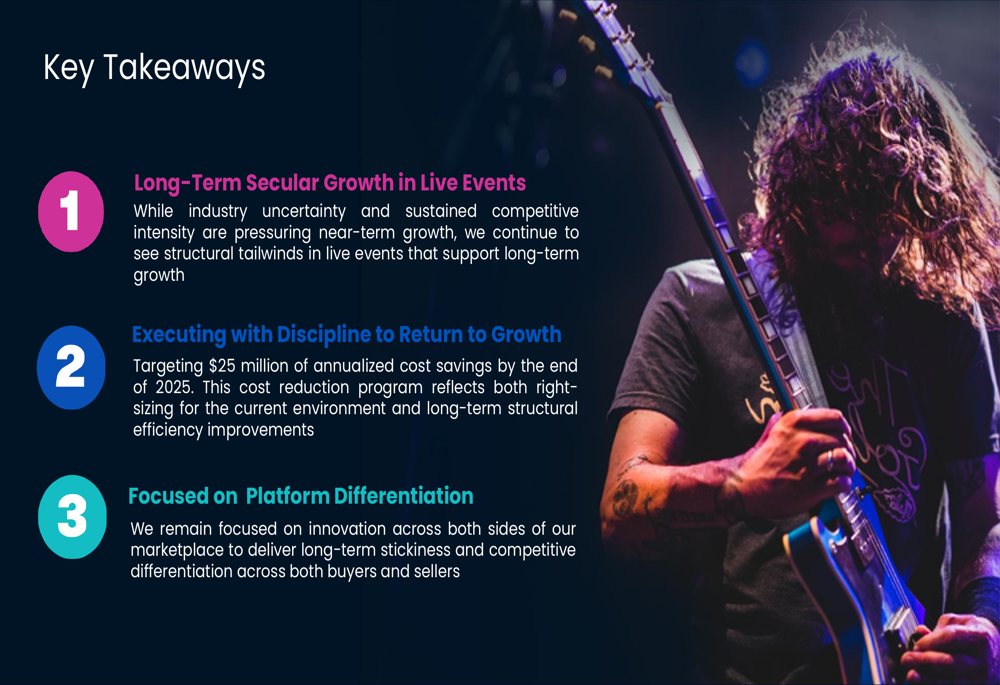

Despite the difficult quarter, Vivid Seats emphasized three key strategic priorities going forward:

The company maintains that long-term secular growth trends in live events remain intact, despite near-term pressures. Management is focusing on executing with discipline to return to growth while emphasizing platform differentiation to create "long-term stickiness" across both buyers and sellers.

Forward-Looking Statements

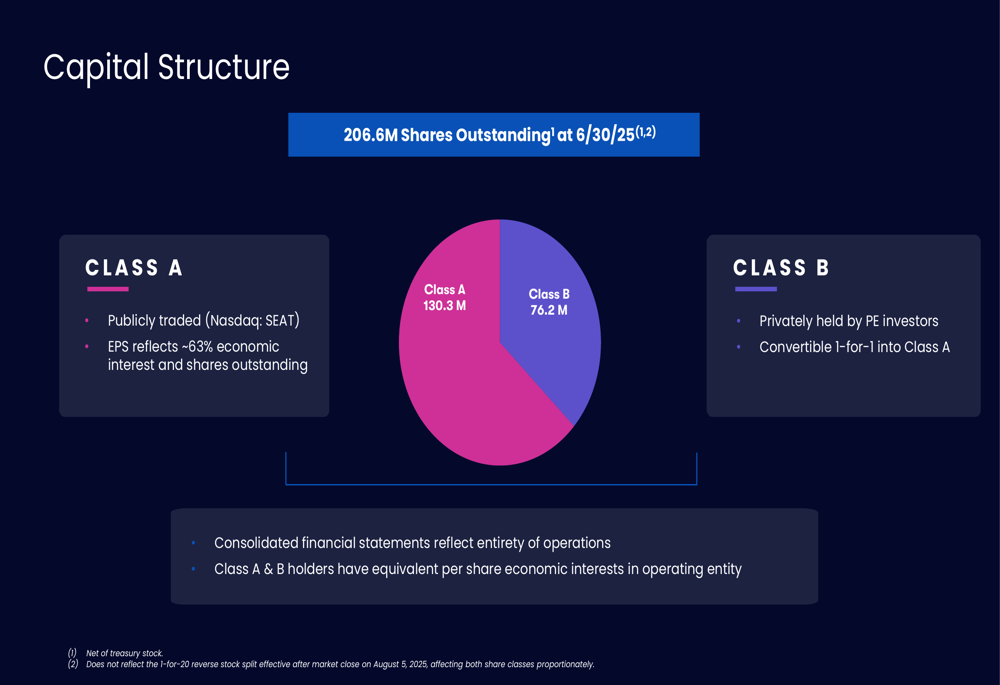

Vivid Seats’ capital structure consists of 206.6 million shares outstanding, divided between 130.3 million publicly traded Class A shares and 76.2 million privately held Class B shares. This structure, which the company outlined in its presentation, provides context for understanding the per-share impact of the company’s financial performance:

Looking ahead, Vivid Seats appears to be taking a more cautious approach following the suspension of its full-year guidance after Q1 results. The implementation of the cost reduction program suggests management is preparing for a potentially prolonged period of challenging market conditions, despite maintaining optimism about long-term industry tailwinds.

The stark contrast between the company’s Q2 2025 performance and the same period last year raises questions about whether the current challenges represent a cyclical downturn or a more fundamental shift in the ticket resale marketplace. With competitors also facing similar industry headwinds, Vivid Seats’ ability to execute its cost reduction program while maintaining platform differentiation will be crucial to its recovery prospects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.